Highlights Tanzania Food Security Update: November 15, 2000

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

THE UNITED REPUBLIC of TANZANIA Tanzania Airports Authority

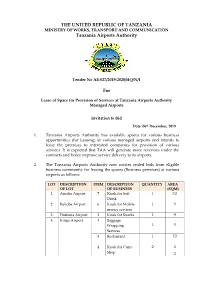

THE UNITED REPUBLIC OF TANZANIA MINISTRY OF WORKS, TRANSPORT AND COMMUNICATION Tanzania Airports Authority Tender No AE-027/2019-2020/HQ/N/1 For Lease of Space for Provision of Services at Tanzania Airports Authority Managed Airports Invitation to Bid Date: 06th December, 2019 1. Tanzania Airports Authority has available spaces for various business opportunities (for Leasing) at various managed airports and intends to lease the premises to interested companies for provision of various services. It is expected that TAA will generate more revenues under the contracts and hence improve service delivery to its airports. 2. The Tanzania Airports Authority now invites sealed bids from eligible business community for leasing the spaces (Business premises) at various airports as follows: LOT DESCRIPTION ITEM DESCRIPTION QUANTITY AREA OF LOT OF BUSINESS (SQM) 1. Arusha Airport 7 Kiosk for Soft 1 33 Drink 2. Bukoba Airport 6 Kiosk for Mobile 1 4 money services 3. Dodoma Airport 3 Kiosk for Snacks 1 4 4. Iringa Airport 1 Baggage Wrapping 1 4 Services 3 Restaurant 1 72 4 Kiosk for Curio 2 3 Shop 3 LOT DESCRIPTION ITEM DESCRIPTION QUANTITY AREA OF LOT OF BUSINESS (SQM) 5 Kiosk for Retail 1 3.5 shop 5. Kigoma Airport 1 Baggage Wrapping 1 4 Services 2 Restaurant 1 19.49 3 Kiosk for Retail 2 19.21 shop 4 Kiosk for Snacks 1 9 5 Kiosk for Curio 1 6.8 Shop 6. Kilwa Masoko 1 Restaurant 1 40 Airport 2 Kiosk for soft 1 9 drinks 7. Lake Manyara 2 Kiosk for Curio 10 84.179 Airport Shop 3 Kiosk for Soft 1 9 Drink 4 Kiosk for Ice 1 9 Cream and Beverage Outlet 5 Car Wash 1 49 6 Kiosk for Mobile 1 2 money services 8. -

Aeronautical Information Promulgation Advice Form

UNITED REPUBLIC OF TANZANIA DAILY NOTAM TANZANIA CIVIL AVIATION AUTHORITY Aeronautical Information Management LIST TEL: 255 22 2110223/224 International NOTAM Office FAX: 255 22 2110264 AFTN: HTDAYNYX P. O. Box 18001, E-mail: [email protected] 25 JAN 2021 [email protected] DAR ES SALAAM Website: www.tcaa.go.tz TANZANIA Document No: Page 1 of 10 Title: Daily List of Valid NOTAM TCAA/FRM/ANS/AIM-33 THE FOLLOWING NOTAM SERIES (A, B & C) WERE STILL VALID AT 0001 UTC. 2021: 0026, 0025, 0024, 0023, 0019, 0016, 0014, 0011, 0008, 0007, SERIES:A 0006, 0005 AND 0001. 2020: 0343, 0341, 0339, 0336, 0331, 0328, 0315, 0312, 0309, 0308, 0304, 0303, 0300, 0296 AND 0295. 210121 KILIMANJARO INTERNATIONAL AIRPORT HTKJ A0026/21 2101250000/2101262359 ILS KK 110.9MHZ RWY 09 SUBJ INTRP DUE MAINT . 210121 DAR ES SALAAM FIR HTDC A0025/21 2101230000/2101252359 DVOR KV 115.3MHZ SUBJ INTRP DUE MAINT. 200121 MWANZA AIRPORT HTMW 2001211315/2104211530 EST A0024/21 NEW PAPI RWY 12/30 INSTL, AWAITING FLTCK. 200121 MUSOMA AIRPORT HTMU A0023/21 2001211310/2104301530 EST NDB MU 312 KHZ U/S 210120 JULIUS NYERERE INTL AIRPORT HTDA 2101201454/2104191530 EST HTDA/HKNA AND HTDA/FAOR CIRCUITS WILL BE SWITCHED FM AFTN TO A0019/21 AMHS, USERS TO EXP INTERMITTENT COM FOR BOTH INCOMING AND OUTGOING DATA COM. This is a controlled Document Document No: TCAA/FRM/ANS/AIM-33 Title: Daily List of Valid NOTAM Page 2 of 10 210114 DAR ES SALAAM FIR HTDC 2101141137/2104111530 EST A0016/21 MV 115.7MHZ DVOR/DME OPR BUT GND CHECKED ONLY, AWAITING FLTCK. -

Dodoma Aprili, 2019

JAMHURI YA MUUNGANO WA TANZANIA WIZARA YA UJENZI, UCHUKUZI NA MAWASILIANO HOTUBA YA WAZIRI WA UJENZI, UCHUKUZI NA MAWASILIANO MHESHIMIWA MHANDISI ISACK ALOYCE KAMWELWE (MB), AKIWASILISHA BUNGENI MPANGO NA MAKADIRIO YA MAPATO NA MATUMIZI YA FEDHA KWA MWAKA WA FEDHA 2019/2020 DODOMA APRILI, 2019 HOTUBA YA WAZIRI WA UJENZI, UCHUKUZI NA MAWASILIANO MHESHIMIWA MHANDISI ISACK ALOYCE KAMWELWE (MB), AKIWASILISHA BUNGENI MPANGO NA MAKADIRIO YA MAPATO NA MATUMIZI YA FEDHA KWA MWAKA WA FEDHA 2019/2020 A. UTANGULIZI 1. Mheshimiwa Spika, baada ya Mwenyekiti wa Kamati ya Kudumu ya Bunge ya Miundombinu kuweka mezani Taarifa ya Utekelezaji wa Mpango na Bajeti ya Wizara, naomba sasa kutoa hoja kwamba Bunge lako Tukufu likubali kupokea na kujadili Taarifa ya Utekelezaji wa Mpango na Bajeti ya Wizara ya Ujenzi, Uchukuzi na Mawasiliano kwa mwaka wa fedha 2018/2019. Aidha, naomba Bunge lako Tukufu lijadili na kupitisha Mpango na Bajeti ya Wizara kwa mwaka wa fedha 2019/2020. 2. Mheshimiwa Spika, nianze kwa kumshukuru Mwenyezi Mungu kwa kutujalia uhai na kutuwezesha kukutana tena leo kujadili maendeleo ya shughuli zinazosimamiwa na sekta za Ujenzi, Uchukuzi na Mawasiliano. 3. Mheshimiwa Spika, nitumie fursa 1 hii kuwapongeza Mheshimiwa Dkt. John Pombe Joseph Magufuli, Rais wa Jamhuri ya Muungano wa Tanzania, Mheshimiwa Dkt. Alli Mohammed Shein, Rais wa Serikali ya Mapinduzi ya Zanzibar, Mheshimiwa Samia Suluhu Hassan, Makamu wa Rais wa Jamhuri ya Muungano wa Tanzania na Mheshimiwa Kassim Majaliwa Majaliwa (Mb.), Waziri Mkuu wa Jamhuri ya Muungano wa Tanzania kwa uongozi wao thabiti ambao umewezesha kutekelezwa kwa mafanikio makubwa Ilani ya Uchaguzi ya CCM ya mwaka 2015, ahadi za Viongozi pamoja na kutatua kero mbalimbali za wananchi. -

This Is a Controlled Document

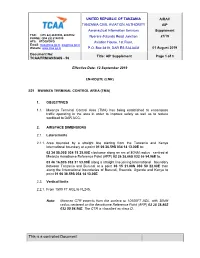

UNITED REPUBLIC OF TANZANIA AIRAC TANZANIA CIVIL AVIATION AUTHORITY AIP Aeronautical Information Services Supplement FAX: (255 22) 2844300, 2844302 Nyerere /Kitunda Road Junction 21/19 PHONE: (255 22) 2198100 AFS: HTDQYOYO Aviation House, 1st Floor, Email: [email protected], [email protected] Website: www.tcaa.go.tz P.O. Box 2819, DAR ES SALAAM 01 August 2019 Document No: Title: AIP Supplement Page 1 of 3 TCAA/FRM/ANS/AIS - 56 Effective Date: 12 September 2019 EN-ROUTE (ENR) S21 MWANZA TERMINAL CONTROL AREA (TMA) 1. OBJECTIVES 1.1. Mwanza Terminal Control Area (TMA) has being established to encompass traffic operating in the area in order to improve safety as well as to reduce workload to DAR ACC. 2. AIRSPACE DIMENSIONS 2.1. Lateral limits 2.1.1. Area bounded by a straight line starting from the Tanzania and Kenya International boundary at a point 01 06 36.59S 034 14 13.00E to; 02 34 58.00S 034 15 35.00E clockwise along an arc of 80NM radius centred at Mwanza Aerodrome Reference Point (ARP) 02 26 38.86S 032 55 54.96E to, 03 46 16.00S 032 37 53.00E along a straight line joining International boundary between Tanzania and Burundi at a point 03 15 21.00S 030 50 22.00E then along the International boundaries of Burundi, Rwanda, Uganda and Kenya to point 01 06 36.59S 034 14 13.00E 2.2. Vertical limits 2.2.1. From 1500 FT AGL to FL245. Note: Mwanza CTR extends from the surface to 10500FT AGL, with 30NM radius centered on the Aerodrome Reference Point (ARP) 02 26 38.86S 032 55 54.96E. -

Tanzania Travel Guide

Tanzania Travel Guide Lake Malawi in Africa Tanzania is located in the eastern region of Africa. It shares its borders with Kenya, Rwanda, Uganda, Congo, Burundi, Zambia, Mozambique, and Malawi. The Indian Ocean also borders the country. Dodoma is the capital city of Tanzania, and Dar Es Salaam is the commercial capital of the country. The country achieved its independence from Britain on December 9th, 1961. The official languages of Tanzania are Swahili and English. Arabic is also spoken widely in Tanzania. Tanzania is divided into 26 regions or " mkoa" like Arusha, Dodoma, Dar Es Salaam, Kigoma, etc. The best time to visit the country is between May to July, or you could also go between the months November to March. Try and avoid going to Tanzania during the rainy season, which begins from April and lasts for a month. Some of the tourist attractions in Tanzania are: National Museum, Dar es Salaam Serengeti National Park Mikumi National Park Selous Game Reserve Gombe National Park Ngorongoro Crater Mount Kilimanjaro Getting In Tanzania can be accessed not only with the help of flights but, trains, buses, etc., are available to the outsiders with the help of which the people can connect with this country. The country with its two international airports of Julius Nyerere International Airport and Kilimanjaro International Airport, is responsible for maintaining relations with a lot of other countries on the globe. The international airlines which frequently brings the foreigners from the distant countries are: Air Comores International -

The United Republic of Tanzania Ministry of Works, Transport and Communication Tanzania Airports Authority Proposed Projects

THE UNITED REPUBLIC OF TANZANIA MINISTRY OF WORKS, TRANSPORT AND COMMUNICATION TANZANIA AIRPORTS AUTHORITY PROPOSED PROJECTS WRITE UP FOR THE BELGIAN TRADE MISSION TO TANZANIA NOVEMBER, 2 0 1 6 , S No. REMARKS I. PROJECT NAME Upgrading of MWANZA AIRPORT PROJECT CODE 4209 PROJECT LOCATION IATA:MWZ; ICA0:1-1.TMW; with elevation above mean sea level (AMSL) 3763ft/1147m FEASIBILITY STUDY Feasibility Study for construction of new terminal building REMARKS and landside pavements, parallel taxiway, widening of runway 45wide to 60m including relocation of AGL System and improvement of storm water drainage was completed in June, 2016 STATUS Contractor for extension of runway, rehabilitation of taxiway to bitumen standard, extension of existing apron and cargo apron, construction of control tower, cargo building, power house and water supply system has resumed to site. ncti, ahold03-)3 ConSkiNclp4) N_ Teicyrri2 WORKS REQUIRING and landside paveThents, parallel taxiway, widening of runway FUNDING 45wide to 60m including relocation of AGL System and improvement of storm water drainage PROJECT COST ESTIMATES/ USD.113 Million FINANCING GAP1 • Improved efficiency and comfort upon construction of new terminal building. • Improved efficiency upon installation of AGL and NAVAIDS • Improved safety upon Construction of Fire Station and PROJECT BENEFITS associated equipment • Improved safety and security upon construction of Control Tower • Improved security upon implementation of security programs. FINANCING MODE PPP, EPC, Bilateral and Multilateral Financing -

2004 Air Accidents/Incidents

2004 AIR ACCIDENTS / INCIDENTS ACCIDENT INVESTIGATION BRANCH Ministry of Communications & Transport TANZANIA CIVIL AVIATION AUTHORITY TYPE & REG. DATE & TIM LOCATION COMMANDER AGE OPERATOR TYPE OF ACCIDENT UTCC & EXPERIENCE 1. PA 23-250 AZTEC 25.1.2004 DAR ES SALAAM KASAMBALA GAPCO (T) LTD A/C EXECUTED A BELLY LDG 5H-GAP 56 YEARS 11.10 HRS NTERNATIONAL 9200HRS DAR ES SALAAM INJURIES: Fatal 0, Serious 0, None 3 2. BELL 206 L3 17.2.2004 KIRAWIRA FOREST GLENTON COMBES MAIN ROTOR STRUCK A BRANCH OF A TREE DURING 33 YEARS CLIMB ZS-RFA 1435 HRS SERENGETI 7000 HRS INJURIES: Fatal 0, Serious 0, None 3 3. CESSNA 404 15.3.2004 ZANAIR LTD LEFT MAIN LDG GEAR SHOCK STRUT SEPARATED ARUSHA AIRPORT W.M. NTAMBULA DURING T-O ROLL. A/C MADE EMERGENCY LDG AT 5H-ZAY 1325 HRS ZANZIBAR DAR ES SALAAM INJURIES: Fatal 0, Serious 0, None 10 4. 17.3.2004 MTO WA MBU FRED LAWUO REGIONAL AIR A/C FORECE LANDED FOLLOWING ENGINE FAILURE CESSNA 208 48 YEARS AFTER TAKE OFF. COLLIDED ON THE EDGE OF A 5H - MUA 0615 HRS MANYARA REGION 14000 HRS ROAD. A/C DESTROYED ARUSHA INJURIES: Fatal 0, Serious 5, Minor 3 5. CESSNA 421 25.3.2004 TPC AIRSTRIP LANDING GEAR COLLAPSED DURING LANDING ROLL 5h-PKC 0850 HRS MOSHI INJURIES: Fatal 0, Serious 0, None 1 6. LET 410 21.5.2004 SHINYANGA AIRPORT CAPT. KUNDU PRECISIONAIR A/C ABORTED TAKE OFF FOLLOWING ENGINE FIRE 49 YEARS 5H-PAJ 1140 HRS 8400 HRS ARUSHA INJURIES: Fatal 0, Serious 0, None 13 7. -

Eac Regional Transport Strategy March 2011

East African Community Secretariat THE EAST AFRICAN TRADE AND TRANSPORT FACILITATION PROJECT EAST AFRICAN TRANSPORT STRATEGY AND REGIONAL ROAD SECTOR DEVELOPMENT PROGRAM FINAL REPORT PART II: EAC REGIONAL TRANSPORT STRATEGY MARCH 2011 Prepared By: Africon Ltd EAC Transport Strategy and Regional Roads Sector Development Program STRUCTURE OF DOCUMENT This report is made up of four parts: Part I provides the general background to the study. It reports on the analyses that are common to and form the foundation of the Transport Strategy and Roads Development Program, including the regional corridors, the economy and demography of the region, transport demand and transport modelling, and the principles for project identification and prioritisation. Part II (this document) is the Transport Strategy. It covers the policy/institutional arrangements in the transport sector in the EAC and its member countries. It then provides an overview of regional issues and identifies regional interventions in each of the transport modes, i.e. roads, rail, ports, pipelines, airports and border posts. It concludes by presenting the prioritised interventions together with an implementation approach. Part III is the Roads Development Program. It covers the regional roads network, and analyses roads needs from capacity and condition perspectives. It also develops some cross-cutting themes (regional roads classification system, regional roads management system and regional overload control). Regional roads projects are identified and described. Part IV is the list of transport projects, together with short profiles for the priority projects. Parts II and III are drafted so that they can be read stand-alone, i.e. in isolation of the other three parts. -

Hotuba Ya Waziri Wa Ujenzi, Uchukuzi Na Mawasiliano Mheshimiwa Prof

HOTUBA YA WAZIRI WA UJENZI, UCHUKUZI NA MAWASILIANO MHESHIMIWA PROF. MAKAME M. MBARAWA (MB), AKIWASILISHA BUNGENI MPANGO NA MAKADIRIO YA MAPATO NA MATUMIZI YA FEDHA KWA MWAKA WA FEDHA 2017/2018 A. UTANGULIZI 1. Mheshimiwa Spika, baada ya Mwenyekiti wa Kamati ya Kudumu ya Bunge ya Miundombinu iliyochambua Bajeti ya Wizara ya Ujenzi, Uchukuzi na Mawasiliano kuweka mezani Taarifa ya Utekelezaji wa Mpango na Bajeti ya Wizara, naomba sasa kutoa hoja kwamba Bunge lako Tukufu likubali kupokea na kujadili Taarifa ya Utekelezaji wa Mpango na Bajeti ya Wizara ya Ujenzi, Uchukuzi na Mawasiliano kwa mwaka wa fedha 2016/2017. Aidha, naomba Bunge lako Tukufu lijadili na kupitisha Mpango na Bajeti ya Wizara kwa mwaka wa fedha 2017/2018. 2. Mheshimiwa Spika, naomba nianze kwa kumshukuru Mwenyezi Mungu kwa kutujalia uhai na kutuwezesha sote kukutana tena leo kujadili maendeleo ya sekta za Ujenzi, Uchukuzi na Mawasiliano. 3. Mheshimiwa Spika, kipekee naomba kuwapongeza sana Mheshimiwa Dkt. John Pombe Joseph Magufuli, Rais wa Jamhuri ya Muungano wa Tanzania, Mhe. Samia Suluhu Hassan, 1 Makamu wa Rais wa Jamhuri ya Muungano wa Tanzania na Mhe. Kassim Majaliwa Majaliwa (Mb.), Waziri Mkuu wa Jamhuri ya Muungano wa Tanzania kwa kuiongoza vema nchi yetu. 4. Mheshimiwa Spika, napenda nimpongeze kwa namna ya pekee Mheshimiwa Dkt. John Pombe Joseph Magufuli, Rais wa Jamhuri ya Muungano wa Tanzania, kwa kuendelea kuiongoza nchi yetu kwa umahiri mkubwa na kudumisha umoja, amani na utulivu. Mheshimiwa Rais ameendelea kusimamia utekelezaji wa Ilani ya Uchaguzi ya CCM ya mwaka 2015 na kutekeleza kwa kiwango kikubwa ahadi za Serikali kwa wananchi. Ama kwa hakika uongozi wake mahiri umekuwa dira sahihi katika kuleta mabadiliko ya kweli ambayo Watanzania wameyasubiri kwa muda mrefu. -

Jamhuri Ya Muungano Wa Tanzania Wizara Ya Ujenzi Na Uchukuzi

JAMHURI YA MUUNGANO WA TANZANIA WIZARA YA UJENZI NA UCHUKUZI HOTUBA YA WAZIRI WA UJENZI NA UCHUKUZI, MHESHIMIWA MHANDISI DKT. LEONARD MADARAKA CHAMURIHO (MB), AKIWASILISHA BUNGENI MPANGO NA MAKADIRIO YA MAPATO NA MATUMIZI YA FEDHA KWA MWAKA WA FEDHA 2021/22 DODOMA MEI, 2021 HOTUBA YA WAZIRI WA UJENZI NA UCHUKUZI, MHESHIMIWA MHANDISI DKT. LEONARD MADARAKA CHAMURIHO (MB), AKIWASILISHA BUNGENI MPANGO NA MAKADIRIO YA MAPATO NA MATUMIZI YA FEDHA KWA MWAKA WA FEDHA 2021/22 A. UTANGULIZI 1. Mheshimiwa Spika, baada ya Kamati ya Kudumu ya Bunge ya Miundombinu kuchambua Bajeti ya Wizara ya Ujenzi na Uchukuzi, na Mwenyekiti wa Kamati hiyo kuwasilisha Taarifa ya Utekelezaji wa Mpango na Bajeti ya Wizara, naomba sasa kutoa hoja kwamba Bunge lako Tukufu likubali kupokea na kujadili Taarifa ya Utekelezaji wa Mpango na Bajeti ya Wizara ya Ujenzi na Uchukuzi kwa mwaka wa fedha 2020/21. Aidha, naomba Bunge lako Tukufu lijadili na kupitisha Mpango na Bajeti ya Wizara kwa mwaka wa fedha 2021/22. 2. Mheshimiwa Spika, nianze kwa unyenyekevu mkubwa kumshukuru Mwenyezi Mungu, mwingi wa rehma, kwa afya njema na uzima aliotujaalia. 3. Mheshimiwa Spika, naomba kuchukua fursa hii, kwa masikitiko makubwa, kuungana na Waheshimiwa Wabunge waliotangulia kutoa pole kwako wewe binafsi, Bunge lako Tukufu na watanzania wote kwa ujumla kufuatia kifo cha mpendwa wetu Hayati Dkt. John Pombe Joseph Magufuli, aliyekuwa Rais wa Jamhuri ya Muungano wa Tanzania kilichotokea tarehe 17 Machi, 2021. Hakika tutamkumbuka shujaa huyu wa Afrika kwa uzalendo, ujasiri, vita dhidi ya ufisadi na uongozi 3 wake mahiri ulioacha alama kubwa kwa Taifa letu na Afrika kwa ujumla. -

Headquarters

THE UNITED REPUBLIC OF TANZANIA MINISTRY OF WORKS, TRANSPORT AND COMMUNICATION GENERAL PROCUREMENT NOTICE (GOODS, WORKS, NON-CONSULTANCY SERVICES AND CONSULTANCY SERVICES) FINANCIAL YEAR 2020/21 1. The Tanzania National Roads Agency (TANROADS) has received/will receive funds from the Government of the United Republic of Tanzania and from various Donors towards the cost of the development and maintenance of the trunk and regionals road network in mainland Tanzania and intends to apply part of the proceeds on payment for the goods, works, non-consultancy and consultancy services to be procured in the Financial Year 2020/21. 2. The Chief Executive, TANROADS, on behalf of the Government of the United Republic of Tanzania now notifies potential bidders of the procurement opportunities for the Financial Year 2020/21 as indicated in the Table hereunder. 1 GOODS, WORKS, NON-CONSULTANCY SERVICES AND DISPOSAL OF PUBLIC ASSETS S/No. Description Tender No. Lot No. PRE-QUALIFICATION INVITATION FOR BIDS AND Procurement EVALUATION Method Invitation Closing- Notification Bid Bid Closing Date Date Opening of Invitation - Opening Contract Applicants Date Date Award 1 2 3 4 5 6 7 8 9 10 GOODS AND NON-CONSULTANCY SERVICES 1. 1Supply of 50Nos Rollers Test Weights AE/001/2020- N/A SHOPPING N/A N/A N/A 22-Oct-20 05-Nov-20 15-Dec-20 4for Calibration of Fixed Weighbridge 21/HQ/G/05 2. 1Supply of Fully Furnished MINOR AE/001/2020- 8Electromechanically Tool Boxes (8 N/A VALUE N/A N/A N/A 22-Oct-20 05-Nov-20 15-Dec-20 21/HQ/G/06 Nos) 3. -

KODY LOTNISK ICAO Niniejsze Zestawienie Zawiera 8372 Kody Lotnisk

KODY LOTNISK ICAO Niniejsze zestawienie zawiera 8372 kody lotnisk. Zestawienie uszeregowano: Kod ICAO = Nazwa portu lotniczego = Lokalizacja portu lotniczego AGAF=Afutara Airport=Afutara AGAR=Ulawa Airport=Arona, Ulawa Island AGAT=Uru Harbour=Atoifi, Malaita AGBA=Barakoma Airport=Barakoma AGBT=Batuna Airport=Batuna AGEV=Geva Airport=Geva AGGA=Auki Airport=Auki AGGB=Bellona/Anua Airport=Bellona/Anua AGGC=Choiseul Bay Airport=Choiseul Bay, Taro Island AGGD=Mbambanakira Airport=Mbambanakira AGGE=Balalae Airport=Shortland Island AGGF=Fera/Maringe Airport=Fera Island, Santa Isabel Island AGGG=Honiara FIR=Honiara, Guadalcanal AGGH=Honiara International Airport=Honiara, Guadalcanal AGGI=Babanakira Airport=Babanakira AGGJ=Avu Avu Airport=Avu Avu AGGK=Kirakira Airport=Kirakira AGGL=Santa Cruz/Graciosa Bay/Luova Airport=Santa Cruz/Graciosa Bay/Luova, Santa Cruz Island AGGM=Munda Airport=Munda, New Georgia Island AGGN=Nusatupe Airport=Gizo Island AGGO=Mono Airport=Mono Island AGGP=Marau Sound Airport=Marau Sound AGGQ=Ontong Java Airport=Ontong Java AGGR=Rennell/Tingoa Airport=Rennell/Tingoa, Rennell Island AGGS=Seghe Airport=Seghe AGGT=Santa Anna Airport=Santa Anna AGGU=Marau Airport=Marau AGGV=Suavanao Airport=Suavanao AGGY=Yandina Airport=Yandina AGIN=Isuna Heliport=Isuna AGKG=Kaghau Airport=Kaghau AGKU=Kukudu Airport=Kukudu AGOK=Gatokae Aerodrome=Gatokae AGRC=Ringi Cove Airport=Ringi Cove AGRM=Ramata Airport=Ramata ANYN=Nauru International Airport=Yaren (ICAO code formerly ANAU) AYBK=Buka Airport=Buka AYCH=Chimbu Airport=Kundiawa AYDU=Daru Airport=Daru