Tanzania Food Security Report: December 15, 2000

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

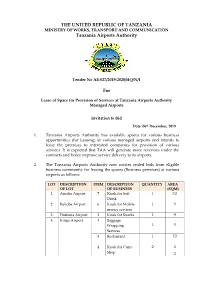

THE UNITED REPUBLIC of TANZANIA Tanzania Airports Authority

THE UNITED REPUBLIC OF TANZANIA MINISTRY OF WORKS, TRANSPORT AND COMMUNICATION Tanzania Airports Authority Tender No AE-027/2019-2020/HQ/N/1 For Lease of Space for Provision of Services at Tanzania Airports Authority Managed Airports Invitation to Bid Date: 06th December, 2019 1. Tanzania Airports Authority has available spaces for various business opportunities (for Leasing) at various managed airports and intends to lease the premises to interested companies for provision of various services. It is expected that TAA will generate more revenues under the contracts and hence improve service delivery to its airports. 2. The Tanzania Airports Authority now invites sealed bids from eligible business community for leasing the spaces (Business premises) at various airports as follows: LOT DESCRIPTION ITEM DESCRIPTION QUANTITY AREA OF LOT OF BUSINESS (SQM) 1. Arusha Airport 7 Kiosk for Soft 1 33 Drink 2. Bukoba Airport 6 Kiosk for Mobile 1 4 money services 3. Dodoma Airport 3 Kiosk for Snacks 1 4 4. Iringa Airport 1 Baggage Wrapping 1 4 Services 3 Restaurant 1 72 4 Kiosk for Curio 2 3 Shop 3 LOT DESCRIPTION ITEM DESCRIPTION QUANTITY AREA OF LOT OF BUSINESS (SQM) 5 Kiosk for Retail 1 3.5 shop 5. Kigoma Airport 1 Baggage Wrapping 1 4 Services 2 Restaurant 1 19.49 3 Kiosk for Retail 2 19.21 shop 4 Kiosk for Snacks 1 9 5 Kiosk for Curio 1 6.8 Shop 6. Kilwa Masoko 1 Restaurant 1 40 Airport 2 Kiosk for soft 1 9 drinks 7. Lake Manyara 2 Kiosk for Curio 10 84.179 Airport Shop 3 Kiosk for Soft 1 9 Drink 4 Kiosk for Ice 1 9 Cream and Beverage Outlet 5 Car Wash 1 49 6 Kiosk for Mobile 1 2 money services 8. -

Aeronautical Information Promulgation Advice Form

UNITED REPUBLIC OF TANZANIA DAILY NOTAM TANZANIA CIVIL AVIATION AUTHORITY Aeronautical Information Management LIST TEL: 255 22 2110223/224 International NOTAM Office FAX: 255 22 2110264 AFTN: HTDAYNYX P. O. Box 18001, E-mail: [email protected] 25 JAN 2021 [email protected] DAR ES SALAAM Website: www.tcaa.go.tz TANZANIA Document No: Page 1 of 10 Title: Daily List of Valid NOTAM TCAA/FRM/ANS/AIM-33 THE FOLLOWING NOTAM SERIES (A, B & C) WERE STILL VALID AT 0001 UTC. 2021: 0026, 0025, 0024, 0023, 0019, 0016, 0014, 0011, 0008, 0007, SERIES:A 0006, 0005 AND 0001. 2020: 0343, 0341, 0339, 0336, 0331, 0328, 0315, 0312, 0309, 0308, 0304, 0303, 0300, 0296 AND 0295. 210121 KILIMANJARO INTERNATIONAL AIRPORT HTKJ A0026/21 2101250000/2101262359 ILS KK 110.9MHZ RWY 09 SUBJ INTRP DUE MAINT . 210121 DAR ES SALAAM FIR HTDC A0025/21 2101230000/2101252359 DVOR KV 115.3MHZ SUBJ INTRP DUE MAINT. 200121 MWANZA AIRPORT HTMW 2001211315/2104211530 EST A0024/21 NEW PAPI RWY 12/30 INSTL, AWAITING FLTCK. 200121 MUSOMA AIRPORT HTMU A0023/21 2001211310/2104301530 EST NDB MU 312 KHZ U/S 210120 JULIUS NYERERE INTL AIRPORT HTDA 2101201454/2104191530 EST HTDA/HKNA AND HTDA/FAOR CIRCUITS WILL BE SWITCHED FM AFTN TO A0019/21 AMHS, USERS TO EXP INTERMITTENT COM FOR BOTH INCOMING AND OUTGOING DATA COM. This is a controlled Document Document No: TCAA/FRM/ANS/AIM-33 Title: Daily List of Valid NOTAM Page 2 of 10 210114 DAR ES SALAAM FIR HTDC 2101141137/2104111530 EST A0016/21 MV 115.7MHZ DVOR/DME OPR BUT GND CHECKED ONLY, AWAITING FLTCK. -

Kigoma Airport

The United Republic of Tanzania Ministry of Infrastructure Development Tanzania Airports Authority Feasibility Study and Detailed Design for the Rehabilitation and Upgrading of Kigoma Airport Preliminary Design Report Environmental Impact Assessment July 2008 In Association With : Sir Frederick Snow & Partners Ltd Belva Consult Limited Corinthian House, PO Box 7521, Mikocheni Area, 17 Lansdowne Road, Croydon, Rose Garden Road, Plot No 455, United Kingdom CR0 2BX, UK Dar es Salaam Tel: +44(02) 08604 8999 Tel: +255 22 2120447 Fax: +44 (02)0 8604 8877 Email: [email protected] Fax: +255 22 2120448 Web Site: www.fsnow.co.uk Email: [email protected] The United Republic of Tanzania Ministry of Infrastructure Development Tanzania Airports Authority Feasibility Study and Detailed Design for the Rehabilitation and Upgrading of Kigoma Airport Preliminary Design Report Environmental Impact Assessment Prepared by Sir Frederick Snow and Partners Limited in association with Belva Consult Limited Issue and Revision Record Rev Date Originator Checker Approver Description 0 July 08 Belva KC Preliminary Submission EXECUTIVE SUMMARY 1. Introduction The Government of Tanzania through the Tanzania Airports Authority is undertaking a feasibility study and detailed engineering design for the rehabilitation and upgrading of the Kigoma airport, located in Kigoma-Ujiji Municipality, Kigoma region. The project is part of a larger project being undertaken by the Tanzania Airport Authority involving rehabilitation and upgrading of high priority commercial airports across the country. The Tanzania Airport Authority has commissioned two companies M/S Sir Frederick Snow & Partners Limited of UK in association with Belva Consult Limited of Tanzania to undertake a Feasibility Study, Detail Engineering Design, Preparation of Tender Documents and Environmental and Social Impact Assessments of seven airports namely Arusha, Bukoba, Kigoma, Tabora, Mafia Island, Shinyanga and Sumbawanga. -

Dodoma Aprili, 2019

JAMHURI YA MUUNGANO WA TANZANIA WIZARA YA UJENZI, UCHUKUZI NA MAWASILIANO HOTUBA YA WAZIRI WA UJENZI, UCHUKUZI NA MAWASILIANO MHESHIMIWA MHANDISI ISACK ALOYCE KAMWELWE (MB), AKIWASILISHA BUNGENI MPANGO NA MAKADIRIO YA MAPATO NA MATUMIZI YA FEDHA KWA MWAKA WA FEDHA 2019/2020 DODOMA APRILI, 2019 HOTUBA YA WAZIRI WA UJENZI, UCHUKUZI NA MAWASILIANO MHESHIMIWA MHANDISI ISACK ALOYCE KAMWELWE (MB), AKIWASILISHA BUNGENI MPANGO NA MAKADIRIO YA MAPATO NA MATUMIZI YA FEDHA KWA MWAKA WA FEDHA 2019/2020 A. UTANGULIZI 1. Mheshimiwa Spika, baada ya Mwenyekiti wa Kamati ya Kudumu ya Bunge ya Miundombinu kuweka mezani Taarifa ya Utekelezaji wa Mpango na Bajeti ya Wizara, naomba sasa kutoa hoja kwamba Bunge lako Tukufu likubali kupokea na kujadili Taarifa ya Utekelezaji wa Mpango na Bajeti ya Wizara ya Ujenzi, Uchukuzi na Mawasiliano kwa mwaka wa fedha 2018/2019. Aidha, naomba Bunge lako Tukufu lijadili na kupitisha Mpango na Bajeti ya Wizara kwa mwaka wa fedha 2019/2020. 2. Mheshimiwa Spika, nianze kwa kumshukuru Mwenyezi Mungu kwa kutujalia uhai na kutuwezesha kukutana tena leo kujadili maendeleo ya shughuli zinazosimamiwa na sekta za Ujenzi, Uchukuzi na Mawasiliano. 3. Mheshimiwa Spika, nitumie fursa 1 hii kuwapongeza Mheshimiwa Dkt. John Pombe Joseph Magufuli, Rais wa Jamhuri ya Muungano wa Tanzania, Mheshimiwa Dkt. Alli Mohammed Shein, Rais wa Serikali ya Mapinduzi ya Zanzibar, Mheshimiwa Samia Suluhu Hassan, Makamu wa Rais wa Jamhuri ya Muungano wa Tanzania na Mheshimiwa Kassim Majaliwa Majaliwa (Mb.), Waziri Mkuu wa Jamhuri ya Muungano wa Tanzania kwa uongozi wao thabiti ambao umewezesha kutekelezwa kwa mafanikio makubwa Ilani ya Uchaguzi ya CCM ya mwaka 2015, ahadi za Viongozi pamoja na kutatua kero mbalimbali za wananchi. -

This Is a Controlled Document

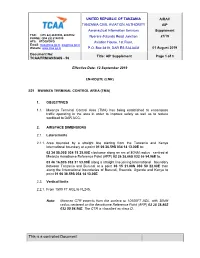

UNITED REPUBLIC OF TANZANIA AIRAC TANZANIA CIVIL AVIATION AUTHORITY AIP Aeronautical Information Services Supplement FAX: (255 22) 2844300, 2844302 Nyerere /Kitunda Road Junction 21/19 PHONE: (255 22) 2198100 AFS: HTDQYOYO Aviation House, 1st Floor, Email: [email protected], [email protected] Website: www.tcaa.go.tz P.O. Box 2819, DAR ES SALAAM 01 August 2019 Document No: Title: AIP Supplement Page 1 of 3 TCAA/FRM/ANS/AIS - 56 Effective Date: 12 September 2019 EN-ROUTE (ENR) S21 MWANZA TERMINAL CONTROL AREA (TMA) 1. OBJECTIVES 1.1. Mwanza Terminal Control Area (TMA) has being established to encompass traffic operating in the area in order to improve safety as well as to reduce workload to DAR ACC. 2. AIRSPACE DIMENSIONS 2.1. Lateral limits 2.1.1. Area bounded by a straight line starting from the Tanzania and Kenya International boundary at a point 01 06 36.59S 034 14 13.00E to; 02 34 58.00S 034 15 35.00E clockwise along an arc of 80NM radius centred at Mwanza Aerodrome Reference Point (ARP) 02 26 38.86S 032 55 54.96E to, 03 46 16.00S 032 37 53.00E along a straight line joining International boundary between Tanzania and Burundi at a point 03 15 21.00S 030 50 22.00E then along the International boundaries of Burundi, Rwanda, Uganda and Kenya to point 01 06 36.59S 034 14 13.00E 2.2. Vertical limits 2.2.1. From 1500 FT AGL to FL245. Note: Mwanza CTR extends from the surface to 10500FT AGL, with 30NM radius centered on the Aerodrome Reference Point (ARP) 02 26 38.86S 032 55 54.96E. -

European Investment in Tanzania: How European Investment Contributes to Industrialisation and Development in Tanzania

EU market study:EU market study 17/10/2016 11:54 Page 1 European Investment in Tanzania: How European investment contributes to industrialisation and development in Tanzania Funded by the European Union EU market study:EU market study 17/10/2016 11:54 Page 2 European Investment in Tanzania: How European investment contributes to industrialisation and development in Tanzania Funded by the European Commission Written by Ashley Elliot © European Commission, Dar es Salaam, 2016 The content of this publication does not reflect the official opinion of the European Commission. Responsibility for the information and views expressed in the publication lies entirely with the author. "EU" refers to the European Union, and "EU+SN" to the members of the European Union and the Economic Free Trade Area (EFTA), unless otherwise indicated. For further inquiries or clarifications please contact [email protected]. A project implemented by consortium led by POHL CONSULTING & ASSOCIATES GMBH EU market study:EU market study 17/10/2016 11:54 Page 3 European Investment in Tanzania: How European investment contributes to industrialisation and development in Tanzania Funded by the European Union EU market study:EU market study 17/10/2016 11:55 Page 4 European Investment in Tanzania: How European investment contributes to industrialisation and development in Tanzania Foreword by Ambassador Roeland van de Geer, Head of the Delegation of the European Union to Tanzania and the East African Community As the Government of Tanzania and international partners join forces to lift millions of Tanzanians out of poverty, the role of trade and investment in the fight against poverty is increasingly recognised. -

World Bank Document

Independent Evaluation Group (IEG) Implementation Completion Report (ICR) Review TZ-Transport Sector Support Project (P055120) Report Number : ICRR0021116 1. Project Data Public Disclosure Authorized Project ID Project Name P055120 TZ-Transport Sector Support Project Country Practice Area(Lead) Additional Financing Africa Transport & Digital Development P126206,P126206 L/C/TF Number(s) Closing Date (Original) Total Project Cost (USD) IDA-47240,IDA-49910 30-Jun-2015 281,700,000.00 Bank Approval Date Closing Date (Actual) Public Disclosure Authorized 27-May-2010 20-Jun-2017 IBRD/IDA (USD) Grants (USD) Original Commitment 270,000,000.00 0.00 Revised Commitment 329,000,000.00 0.00 Actual 320,608,489.77 0.00 Prepared by Reviewed by ICR Review Coordinator Group Public Disclosure Authorized Victoria Alexeeva Vibecke Dixon Christopher David Nelson IEGSD (Unit 4) 2. Project Objectives and Components a. Objectives Original objective The project development objective (PDO) was “to improve the condition of the national paved road network, to lower transport cost on selected roads, and to expand the capacity of selected regional airports” (Financing Agreement dated June 11, 2010; page 4). Revised objective Public Disclosure Authorized The PDO was revised slightly to reflect new activities added as part of an additional financing approved in June 2011 (over a year after the original project’s approval). The revised PDO was “to improve the condition of the national paved road network, to lower transport cost on selected roads and to Songo Songo island, Page 1 of 16 Independent Evaluation Group (IEG) Implementation Completion Report (ICR) Review TZ-Transport Sector Support Project (P055120) and to expand the capacity of selected airports” (Financing Agreement dated September 2, 2011; page 6). -

Tanzania Travel Guide

Tanzania Travel Guide Lake Malawi in Africa Tanzania is located in the eastern region of Africa. It shares its borders with Kenya, Rwanda, Uganda, Congo, Burundi, Zambia, Mozambique, and Malawi. The Indian Ocean also borders the country. Dodoma is the capital city of Tanzania, and Dar Es Salaam is the commercial capital of the country. The country achieved its independence from Britain on December 9th, 1961. The official languages of Tanzania are Swahili and English. Arabic is also spoken widely in Tanzania. Tanzania is divided into 26 regions or " mkoa" like Arusha, Dodoma, Dar Es Salaam, Kigoma, etc. The best time to visit the country is between May to July, or you could also go between the months November to March. Try and avoid going to Tanzania during the rainy season, which begins from April and lasts for a month. Some of the tourist attractions in Tanzania are: National Museum, Dar es Salaam Serengeti National Park Mikumi National Park Selous Game Reserve Gombe National Park Ngorongoro Crater Mount Kilimanjaro Getting In Tanzania can be accessed not only with the help of flights but, trains, buses, etc., are available to the outsiders with the help of which the people can connect with this country. The country with its two international airports of Julius Nyerere International Airport and Kilimanjaro International Airport, is responsible for maintaining relations with a lot of other countries on the globe. The international airlines which frequently brings the foreigners from the distant countries are: Air Comores International -

The United Republic of Tanzania Ministry of Works, Transport and Communication Tanzania Airports Authority Proposed Projects

THE UNITED REPUBLIC OF TANZANIA MINISTRY OF WORKS, TRANSPORT AND COMMUNICATION TANZANIA AIRPORTS AUTHORITY PROPOSED PROJECTS WRITE UP FOR THE BELGIAN TRADE MISSION TO TANZANIA NOVEMBER, 2 0 1 6 , S No. REMARKS I. PROJECT NAME Upgrading of MWANZA AIRPORT PROJECT CODE 4209 PROJECT LOCATION IATA:MWZ; ICA0:1-1.TMW; with elevation above mean sea level (AMSL) 3763ft/1147m FEASIBILITY STUDY Feasibility Study for construction of new terminal building REMARKS and landside pavements, parallel taxiway, widening of runway 45wide to 60m including relocation of AGL System and improvement of storm water drainage was completed in June, 2016 STATUS Contractor for extension of runway, rehabilitation of taxiway to bitumen standard, extension of existing apron and cargo apron, construction of control tower, cargo building, power house and water supply system has resumed to site. ncti, ahold03-)3 ConSkiNclp4) N_ Teicyrri2 WORKS REQUIRING and landside paveThents, parallel taxiway, widening of runway FUNDING 45wide to 60m including relocation of AGL System and improvement of storm water drainage PROJECT COST ESTIMATES/ USD.113 Million FINANCING GAP1 • Improved efficiency and comfort upon construction of new terminal building. • Improved efficiency upon installation of AGL and NAVAIDS • Improved safety upon Construction of Fire Station and PROJECT BENEFITS associated equipment • Improved safety and security upon construction of Control Tower • Improved security upon implementation of security programs. FINANCING MODE PPP, EPC, Bilateral and Multilateral Financing -

National Implementation Plan for the Stockholm Convention on Persistent Organic Pollutants (Pops)

UNITED REPUBLIC OF TANZANIA VICE PRESIDENT’S OFFICE NATIONAL IMPLEMENTATION PLAN FOR THE STOCKHOLM CONVENTION ON PERSISTENT ORGANIC POLLUTANTS (POPs) SEPTEMBER, 2018 Copyright ©2015 Division of Environment, Vice President’s Office, URT This publication may be reproduced for educational or non-profit purposes without special permission from the copyright holders provided acknowledgement of the source is made. The Vice President’s Office would appreciate receiving a copy of any publication that uses this publication as a source. For further information, please contact: Makole Street, LAPF Building, 7th Floor, P.O.Box 2502 40406 Dodoma, TANZANIA. Phone : +255 262329006 Fax : +255 262329007 NATIONAL IMPLEMENTATION PLAN FOR THE STOCKHOLM ii CONVENTION ON PERSISTENT ORGANIC POLLUTANTS (POPS) PREFACE Persistent Organic Pollutants (POPs) present unique challenge as they persist in the environment, exhibit long-range transport properties, bioaccumulate in fat tissues of living organisms and pose risks to human health and the environment. In view of the global nature of the challenges posed by POPs, the Stockholm Convention on POPs was adopted at a Conference of Plenipotentiaries on 22 May, 2001 in Stockholm, Sweden. It entered into force in May, 2004 and Tanzania ratified it on 30 April, 2004. The objective of the Convention is to protect human health and the environment from adverse effects of persistent organic pollutants. The initial list of chemicals controlled under the Convention included 12 chemicals which were popularly referred to as the ‘dirty dozen’. However, during meetings of the Conference of the Parties in 2009, 2011, 2013 and 2015, additional 14 new chemicals were included in the list, making a total of 26 controlled chemicals as of now. -

Preliminary Design Report Environmental Impact Assessment

The United Republic of Tanzania Ministry of Infrastructure Development Tanzania Airports Authority Feasibility Study and Detailed Design for the Rehabilitation and Upgrading of Bukoba Airport Preliminary Design Report Environmental Impact Assessment July 2008 In Association With : Sir Frederick Snow & Partners Ltd Belva Consult Limited Corinthian House, PO Box 7521, Mikocheni Area, 17 Lansdowne Road, Croydon, Rose Garden Road, Plot No 455, United Kingdom CR0 2BX, UK Dar es Salaam Tel: +44(02) 08604 8999 Tel: +255 22 2120447 Fax: +44 (02)0 8604 8877 Email: [email protected] Fax: +255 22 2120448 Web Site: www.fsnow.co.uk Email: [email protected] The United Republic of Tanzania Ministry of Infrastructure Development Tanzania Airports Authority Feasibility Study and Detailed Design for the Rehabilitation and Upgrading of Bukoba Airport Preliminary Design Report Environmental Impact Assessment Prepared by Sir Frederick Snow and Partners Limited in association with Belva Consult Limited Issue and Revision Record Rev Date Originator Checker Approver Description 0 July 08 Belva KC Preliminary Submission EXECUTIVE SUMMARY 1 Introduction The Government of Tanzania through the Tanzania Airports Authority is undertaking a feasibility study and detailed engineering design for the rehabilitation and upgrading of the Bukoba airport, located in Bukoba Municipality, Kagera region. The project is part of a larger project being undertaken by the Tanzania Airport Authority involving rehabilitation and upgrading of high priority commercial airports across the country. The Tanzania Airport Authority has commissioned two companies M/S Sir Frederick Snow & Partners Limited of UK in association with Belva Consult Limited of Tanzania to undertake a Feasibility Study, Detail Engineering Design, Preparation of Tender Documents and Environmental and Social Impact Assessments of seven airports namely Arusha, Bukoba, Kigoma, Tabora, Mafia Island, Shinyanga and Sumbawanga. -

2004 Air Accidents/Incidents

2004 AIR ACCIDENTS / INCIDENTS ACCIDENT INVESTIGATION BRANCH Ministry of Communications & Transport TANZANIA CIVIL AVIATION AUTHORITY TYPE & REG. DATE & TIM LOCATION COMMANDER AGE OPERATOR TYPE OF ACCIDENT UTCC & EXPERIENCE 1. PA 23-250 AZTEC 25.1.2004 DAR ES SALAAM KASAMBALA GAPCO (T) LTD A/C EXECUTED A BELLY LDG 5H-GAP 56 YEARS 11.10 HRS NTERNATIONAL 9200HRS DAR ES SALAAM INJURIES: Fatal 0, Serious 0, None 3 2. BELL 206 L3 17.2.2004 KIRAWIRA FOREST GLENTON COMBES MAIN ROTOR STRUCK A BRANCH OF A TREE DURING 33 YEARS CLIMB ZS-RFA 1435 HRS SERENGETI 7000 HRS INJURIES: Fatal 0, Serious 0, None 3 3. CESSNA 404 15.3.2004 ZANAIR LTD LEFT MAIN LDG GEAR SHOCK STRUT SEPARATED ARUSHA AIRPORT W.M. NTAMBULA DURING T-O ROLL. A/C MADE EMERGENCY LDG AT 5H-ZAY 1325 HRS ZANZIBAR DAR ES SALAAM INJURIES: Fatal 0, Serious 0, None 10 4. 17.3.2004 MTO WA MBU FRED LAWUO REGIONAL AIR A/C FORECE LANDED FOLLOWING ENGINE FAILURE CESSNA 208 48 YEARS AFTER TAKE OFF. COLLIDED ON THE EDGE OF A 5H - MUA 0615 HRS MANYARA REGION 14000 HRS ROAD. A/C DESTROYED ARUSHA INJURIES: Fatal 0, Serious 5, Minor 3 5. CESSNA 421 25.3.2004 TPC AIRSTRIP LANDING GEAR COLLAPSED DURING LANDING ROLL 5h-PKC 0850 HRS MOSHI INJURIES: Fatal 0, Serious 0, None 1 6. LET 410 21.5.2004 SHINYANGA AIRPORT CAPT. KUNDU PRECISIONAIR A/C ABORTED TAKE OFF FOLLOWING ENGINE FIRE 49 YEARS 5H-PAJ 1140 HRS 8400 HRS ARUSHA INJURIES: Fatal 0, Serious 0, None 13 7.