Eac Regional Transport Strategy March 2011

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

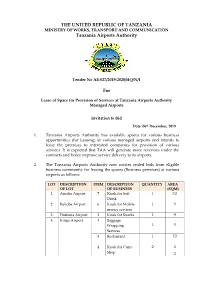

THE UNITED REPUBLIC of TANZANIA Tanzania Airports Authority

THE UNITED REPUBLIC OF TANZANIA MINISTRY OF WORKS, TRANSPORT AND COMMUNICATION Tanzania Airports Authority Tender No AE-027/2019-2020/HQ/N/1 For Lease of Space for Provision of Services at Tanzania Airports Authority Managed Airports Invitation to Bid Date: 06th December, 2019 1. Tanzania Airports Authority has available spaces for various business opportunities (for Leasing) at various managed airports and intends to lease the premises to interested companies for provision of various services. It is expected that TAA will generate more revenues under the contracts and hence improve service delivery to its airports. 2. The Tanzania Airports Authority now invites sealed bids from eligible business community for leasing the spaces (Business premises) at various airports as follows: LOT DESCRIPTION ITEM DESCRIPTION QUANTITY AREA OF LOT OF BUSINESS (SQM) 1. Arusha Airport 7 Kiosk for Soft 1 33 Drink 2. Bukoba Airport 6 Kiosk for Mobile 1 4 money services 3. Dodoma Airport 3 Kiosk for Snacks 1 4 4. Iringa Airport 1 Baggage Wrapping 1 4 Services 3 Restaurant 1 72 4 Kiosk for Curio 2 3 Shop 3 LOT DESCRIPTION ITEM DESCRIPTION QUANTITY AREA OF LOT OF BUSINESS (SQM) 5 Kiosk for Retail 1 3.5 shop 5. Kigoma Airport 1 Baggage Wrapping 1 4 Services 2 Restaurant 1 19.49 3 Kiosk for Retail 2 19.21 shop 4 Kiosk for Snacks 1 9 5 Kiosk for Curio 1 6.8 Shop 6. Kilwa Masoko 1 Restaurant 1 40 Airport 2 Kiosk for soft 1 9 drinks 7. Lake Manyara 2 Kiosk for Curio 10 84.179 Airport Shop 3 Kiosk for Soft 1 9 Drink 4 Kiosk for Ice 1 9 Cream and Beverage Outlet 5 Car Wash 1 49 6 Kiosk for Mobile 1 2 money services 8. -

V9.5 on Ipad Introduction

Pilot’s Guide to FOREFLIGHT MOBILE 55th Edition Covers ForeFlight Mobile v9.5 on iPad Introduction ...............................................................................................19 iPad Tips ....................................................................................................................................19 Setting-up ForeFlight Mobile ..............................................................21 Planning a Flight ......................................................................................22 Planning a fight using the Flights form ........................................................................22 Destination Services ................................................................................................................................23 Navlog, Briefng, Messages ...................................................................................................................24 Planning a fight on Maps using the Flight Plan Editor ..........................................25 Planning a fight on Maps using Touch .........................................................................26 Planning a fight on Maps using Search ........................................................................27 Scheduled Flight Search on Maps ......................................................................................................29 Airports ........................................................................................................31 About the Design ..................................................................................................................32 -

Aeronautical Information Promulgation Advice Form

UNITED REPUBLIC OF TANZANIA DAILY NOTAM TANZANIA CIVIL AVIATION AUTHORITY Aeronautical Information Management LIST TEL: 255 22 2110223/224 International NOTAM Office FAX: 255 22 2110264 AFTN: HTDAYNYX P. O. Box 18001, E-mail: [email protected] 25 JAN 2021 [email protected] DAR ES SALAAM Website: www.tcaa.go.tz TANZANIA Document No: Page 1 of 10 Title: Daily List of Valid NOTAM TCAA/FRM/ANS/AIM-33 THE FOLLOWING NOTAM SERIES (A, B & C) WERE STILL VALID AT 0001 UTC. 2021: 0026, 0025, 0024, 0023, 0019, 0016, 0014, 0011, 0008, 0007, SERIES:A 0006, 0005 AND 0001. 2020: 0343, 0341, 0339, 0336, 0331, 0328, 0315, 0312, 0309, 0308, 0304, 0303, 0300, 0296 AND 0295. 210121 KILIMANJARO INTERNATIONAL AIRPORT HTKJ A0026/21 2101250000/2101262359 ILS KK 110.9MHZ RWY 09 SUBJ INTRP DUE MAINT . 210121 DAR ES SALAAM FIR HTDC A0025/21 2101230000/2101252359 DVOR KV 115.3MHZ SUBJ INTRP DUE MAINT. 200121 MWANZA AIRPORT HTMW 2001211315/2104211530 EST A0024/21 NEW PAPI RWY 12/30 INSTL, AWAITING FLTCK. 200121 MUSOMA AIRPORT HTMU A0023/21 2001211310/2104301530 EST NDB MU 312 KHZ U/S 210120 JULIUS NYERERE INTL AIRPORT HTDA 2101201454/2104191530 EST HTDA/HKNA AND HTDA/FAOR CIRCUITS WILL BE SWITCHED FM AFTN TO A0019/21 AMHS, USERS TO EXP INTERMITTENT COM FOR BOTH INCOMING AND OUTGOING DATA COM. This is a controlled Document Document No: TCAA/FRM/ANS/AIM-33 Title: Daily List of Valid NOTAM Page 2 of 10 210114 DAR ES SALAAM FIR HTDC 2101141137/2104111530 EST A0016/21 MV 115.7MHZ DVOR/DME OPR BUT GND CHECKED ONLY, AWAITING FLTCK. -

Hotuba Ya Waziri Wa Uchukuzi, Mhe. Dkt

HOTUBA YA WAZIRI WA UCHUKUZI, MHE. DKT. HARRISON G. MWAKYEMBE (MB), AKIWASILISHA BUNGENI MAKADIRIO YA MAPATO NA MATUMIZI YA FEDHA KWA MWAKA 2013/2014 UTANGULIZI 1. Mheshimiwa Spika, baada ya Mwenyekiti wa Kamati ya Kudumu ya Bunge ya Miundombinu iliyochambua bajeti ya Wizara ya Uchukuzi kuweka mezani taarifa ya Kamati mbele ya Bunge lako Tukufu, naomba sasa kutoa hoja kwamba Bunge lako likubali kupokea, kujadili na kupitisha Mpango na Makadirio ya Mapato na Matumizi ya Fedha ya Wizara ya Uchukuzi kwa mwaka wa fedha 2013/2014. 2. Mheshimiwa Spika, naomba nianze kwa kumshukuru Mwenyezi Mungu kwa kutujalia uhai na kutuwezesha kukutana tena leo kujadili maendeleo ya Sekta ya Uchukuzi, Hali ya Hewa na Taifa letu kwa ujumla. 3. Mheshimiwa Spika, napenda vilevile nimpongeze kwa namna ya pekee Mhe. Dkt. Jakaya Mrisho Kikwete, Rais wa Jamhuri ya Muungano wa Tanzania kwa kuchaguliwa kwa mara nyingine tena kuwa Mwenyekiti wa Chama 1 cha Mapinduzi. Kuchaguliwa kwake, tena kwa kishindo, ni ushahidi tosha wa imani kubwa waliyonayo wana CCM kwake kutokana na kazi nzuri aliyoifanya miaka mitano ya kwanza ya uongozi wake. Aidha, nawapongeza Rais wa Zanzibar, Mhe. Dkt. Ali Mohamed Shein kwa kuchaguliwa kuwa Makamu Mwenyekiti wa CCM (Zanzibar), Mhe. Philip Mangula kuwa Makamu Mwenyekiti wa CCM (Tanzania Bara) na Mhe. Abdulrahman Kinana kuwa Katibu Mkuu wa CCM. Binafsi nina imani kubwa kuwa safu hii mpya ya uongozi yenye rekodi ndefu ya utendaji uliotukuka nje na ndani ya Chama cha Mapinduzi itatusogeza karibu zaidi na malengo tuliyojiwekea kama Taifa ya kuwa nchi ya kipato cha kati ifikapo mwaka 2025. 4. Mheshimiwa Spika, niruhusu vilevile nitumie fursa hii kuwashukuru Mhe. -

Massdot Aeronautics Division Offices the Logan Office Center One Harborside Drive, Suite 205N East Boston, MA 02128-2909

MASSACHUSETTS STATEWIDE AIRPORT SYSTEM PLAN MASSDOT AERONAUTICS DIVISION MASSACHUSETTS STATEWIDE AIRPORT SYSTEM PLAN (MSASP) PROJECT MANAGEMENT TEAM (PMT) MEETING #2 MEETING NOTES Thursday, December 10, 2009 (1 PM– 3 PM) MassDOT Aeronautics Division Offices The Logan Office Center One Harborside Drive, Suite 205N East Boston, MA 02128-2909 1. MEETING ATTENDANCE PMT Member Attendees: Member Name Affiliation Chris Willenborg MassDOT Aeronautics, Administrator Denise Garcia MassDOT Aeronautics, Manager of Aviation Planning William Benjamin Former MAC Commissioner Craig Dotlo (via phone) Aircraft Owners and Pilots Association (AOPA) Flavio Leo Massport Russ Maguire Massachusetts Airport Management Association (MAMA) Paul Nelson Massachusetts Executive Office of Transportation (EOT) Michelle Ricci (via phone) Federal Aviation Administration (FAA) Arthur Robert Massachusetts Office of Business Development (MOBD) Dean Saucier (via phone) National Business Aviation Association (NBAA) Absent PMT Member Attendees: Harold Bevis Delta Airlines / Air Transport Association (ATA) Dan Wolf Cape Air Other Meeting Attendees: Steven Rawding MassDOT Aeronautics, Aviation Planner Katie Servis MassDOT Aeronautics, Environmental Analyst Bob Mallard Airport Solutions Group (ASG) - Study Project Manager Pam Keidel-Adams Wilbur Smith Associates – Project Team Member James Miklas Wilbur Smith Associates – Project Team Member Marc Champigny Louis Berger Group – Project Team Member Nick Stefaniak Louis Berger Group – Project Team Member Jeremy Martelle Louis Berger -

Scalability of the Air Transportation System and Development of Multi-Airport Systems: a Worldwide Perspective

Scalability of the Air Transportation System and Development of Multi-Airport Systems: A Worldwide Perspective by Philippe A. Bonnefoy B. Ing., Mechanical Engineering, École Polytechnique de Montréal, Canada, 2002 S.M., Aeronautics & Astronautics, Massachusetts Institute of Technology, 2005 Submitted to the engineering systems division in partial fulfillment of the requirements for the degree of DOCTOR OF PHILOSOPHY at the MASSACHUSETTS INSTITUTE OF TECHNOLOGY June 2008 2008 Philippe A. Bonnefoy, All rights reserved. The author hereby grants to MIT the permission to reproduce and to distribute publicly paper and electronic copies of this thesis document in whole or in part. Signature of Author: ______________________________________________________ Philippe A. Bonnefoy Engineering Systems Division May 30th 2008 Certified by: _____________________________________________________________ R. John Hansman, Professor Department of Aeronautics and Astronautics and Engineering Systems Thesis Supervisor Certified by: _____________________________________________________________ Cynthia Barnhart, Professor Department of Civil and Environmental Engineering and Engineering Systems Certified by: _____________________________________________________________ Richard de Neufville, Professor Department of Civil and Environmental Engineering and Engineering Systems Certified by: _____________________________________________________________ Amedeo Odoni, Professor Department of Aeronautics and Astronautics and Civil and Environmental Engineering Accepted -

Dodoma Aprili, 2019

JAMHURI YA MUUNGANO WA TANZANIA WIZARA YA UJENZI, UCHUKUZI NA MAWASILIANO HOTUBA YA WAZIRI WA UJENZI, UCHUKUZI NA MAWASILIANO MHESHIMIWA MHANDISI ISACK ALOYCE KAMWELWE (MB), AKIWASILISHA BUNGENI MPANGO NA MAKADIRIO YA MAPATO NA MATUMIZI YA FEDHA KWA MWAKA WA FEDHA 2019/2020 DODOMA APRILI, 2019 HOTUBA YA WAZIRI WA UJENZI, UCHUKUZI NA MAWASILIANO MHESHIMIWA MHANDISI ISACK ALOYCE KAMWELWE (MB), AKIWASILISHA BUNGENI MPANGO NA MAKADIRIO YA MAPATO NA MATUMIZI YA FEDHA KWA MWAKA WA FEDHA 2019/2020 A. UTANGULIZI 1. Mheshimiwa Spika, baada ya Mwenyekiti wa Kamati ya Kudumu ya Bunge ya Miundombinu kuweka mezani Taarifa ya Utekelezaji wa Mpango na Bajeti ya Wizara, naomba sasa kutoa hoja kwamba Bunge lako Tukufu likubali kupokea na kujadili Taarifa ya Utekelezaji wa Mpango na Bajeti ya Wizara ya Ujenzi, Uchukuzi na Mawasiliano kwa mwaka wa fedha 2018/2019. Aidha, naomba Bunge lako Tukufu lijadili na kupitisha Mpango na Bajeti ya Wizara kwa mwaka wa fedha 2019/2020. 2. Mheshimiwa Spika, nianze kwa kumshukuru Mwenyezi Mungu kwa kutujalia uhai na kutuwezesha kukutana tena leo kujadili maendeleo ya shughuli zinazosimamiwa na sekta za Ujenzi, Uchukuzi na Mawasiliano. 3. Mheshimiwa Spika, nitumie fursa 1 hii kuwapongeza Mheshimiwa Dkt. John Pombe Joseph Magufuli, Rais wa Jamhuri ya Muungano wa Tanzania, Mheshimiwa Dkt. Alli Mohammed Shein, Rais wa Serikali ya Mapinduzi ya Zanzibar, Mheshimiwa Samia Suluhu Hassan, Makamu wa Rais wa Jamhuri ya Muungano wa Tanzania na Mheshimiwa Kassim Majaliwa Majaliwa (Mb.), Waziri Mkuu wa Jamhuri ya Muungano wa Tanzania kwa uongozi wao thabiti ambao umewezesha kutekelezwa kwa mafanikio makubwa Ilani ya Uchaguzi ya CCM ya mwaka 2015, ahadi za Viongozi pamoja na kutatua kero mbalimbali za wananchi. -

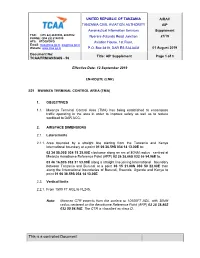

This Is a Controlled Document

UNITED REPUBLIC OF TANZANIA AIRAC TANZANIA CIVIL AVIATION AUTHORITY AIP Aeronautical Information Services Supplement FAX: (255 22) 2844300, 2844302 Nyerere /Kitunda Road Junction 21/19 PHONE: (255 22) 2198100 AFS: HTDQYOYO Aviation House, 1st Floor, Email: [email protected], [email protected] Website: www.tcaa.go.tz P.O. Box 2819, DAR ES SALAAM 01 August 2019 Document No: Title: AIP Supplement Page 1 of 3 TCAA/FRM/ANS/AIS - 56 Effective Date: 12 September 2019 EN-ROUTE (ENR) S21 MWANZA TERMINAL CONTROL AREA (TMA) 1. OBJECTIVES 1.1. Mwanza Terminal Control Area (TMA) has being established to encompass traffic operating in the area in order to improve safety as well as to reduce workload to DAR ACC. 2. AIRSPACE DIMENSIONS 2.1. Lateral limits 2.1.1. Area bounded by a straight line starting from the Tanzania and Kenya International boundary at a point 01 06 36.59S 034 14 13.00E to; 02 34 58.00S 034 15 35.00E clockwise along an arc of 80NM radius centred at Mwanza Aerodrome Reference Point (ARP) 02 26 38.86S 032 55 54.96E to, 03 46 16.00S 032 37 53.00E along a straight line joining International boundary between Tanzania and Burundi at a point 03 15 21.00S 030 50 22.00E then along the International boundaries of Burundi, Rwanda, Uganda and Kenya to point 01 06 36.59S 034 14 13.00E 2.2. Vertical limits 2.2.1. From 1500 FT AGL to FL245. Note: Mwanza CTR extends from the surface to 10500FT AGL, with 30NM radius centered on the Aerodrome Reference Point (ARP) 02 26 38.86S 032 55 54.96E. -

Chapter 6: System Recommendations

6. System Recommendations 6.1. Introduction This chapter builds on the findings of Chapter 5. System Performance by establishing future performance targets and making recommendations for South Dakota’s aviation system to achieve those future targets. This chapter is organized around the three system goals established at the beginning of the study and includes a review of each goal’s associated performance measures (PMs) to identify gaps in system performance. Performance gaps are determined by comparing the existing performance (presented in Chapter 5) to the future performance targets established by the South Dakota Department of Transportation Office of Aeronautics Services (SDDOT) and stakeholder groups to identify the number of airports, by state role and system-wide, that are not meeting each PM. Evaluating the existing performance against future performance targets provides a list of airports that are deficient in meeting the PM and therefore are candidates for system plan project recommendations. However, it is important to note that while these lists of airports by PM are helpful in understanding the system gaps, resources are limited and therefore an airport’s mention in this chapter is not a guarantee of project funding. For more information on SDSASP recommended projects, including anticipated costs and project priorities, see Chapter 7. System Needs and Project Costs. As a supplement to this recommendations chapter, Appendix E – NPIAS Analysis and Recommendations offers recommendations related to airport inclusion and exclusion from National Plan of Integrated Airport Systems (NPIAS) and changes to ASSET classifications for SDSASP airports. While this information does not pertain directly to the recommendations included in this chapter, it does provide additional context as it relates to system recommendations. -

Tanzania Travel Guide

Tanzania Travel Guide Lake Malawi in Africa Tanzania is located in the eastern region of Africa. It shares its borders with Kenya, Rwanda, Uganda, Congo, Burundi, Zambia, Mozambique, and Malawi. The Indian Ocean also borders the country. Dodoma is the capital city of Tanzania, and Dar Es Salaam is the commercial capital of the country. The country achieved its independence from Britain on December 9th, 1961. The official languages of Tanzania are Swahili and English. Arabic is also spoken widely in Tanzania. Tanzania is divided into 26 regions or " mkoa" like Arusha, Dodoma, Dar Es Salaam, Kigoma, etc. The best time to visit the country is between May to July, or you could also go between the months November to March. Try and avoid going to Tanzania during the rainy season, which begins from April and lasts for a month. Some of the tourist attractions in Tanzania are: National Museum, Dar es Salaam Serengeti National Park Mikumi National Park Selous Game Reserve Gombe National Park Ngorongoro Crater Mount Kilimanjaro Getting In Tanzania can be accessed not only with the help of flights but, trains, buses, etc., are available to the outsiders with the help of which the people can connect with this country. The country with its two international airports of Julius Nyerere International Airport and Kilimanjaro International Airport, is responsible for maintaining relations with a lot of other countries on the globe. The international airlines which frequently brings the foreigners from the distant countries are: Air Comores International -

Safetaxi Full Coverage List – 21S5 Cycle

SafeTaxi Full Coverage List – 21S5 Cycle Australia Australian Capital Territory Identifier Airport Name City Territory YSCB Canberra Airport Canberra ACT Oceanic Territories Identifier Airport Name City Territory YPCC Cocos (Keeling) Islands Intl Airport West Island, Cocos Island AUS YPXM Christmas Island Airport Christmas Island AUS YSNF Norfolk Island Airport Norfolk Island AUS New South Wales Identifier Airport Name City Territory YARM Armidale Airport Armidale NSW YBHI Broken Hill Airport Broken Hill NSW YBKE Bourke Airport Bourke NSW YBNA Ballina / Byron Gateway Airport Ballina NSW YBRW Brewarrina Airport Brewarrina NSW YBTH Bathurst Airport Bathurst NSW YCBA Cobar Airport Cobar NSW YCBB Coonabarabran Airport Coonabarabran NSW YCDO Condobolin Airport Condobolin NSW YCFS Coffs Harbour Airport Coffs Harbour NSW YCNM Coonamble Airport Coonamble NSW YCOM Cooma - Snowy Mountains Airport Cooma NSW YCOR Corowa Airport Corowa NSW YCTM Cootamundra Airport Cootamundra NSW YCWR Cowra Airport Cowra NSW YDLQ Deniliquin Airport Deniliquin NSW YFBS Forbes Airport Forbes NSW YGFN Grafton Airport Grafton NSW YGLB Goulburn Airport Goulburn NSW YGLI Glen Innes Airport Glen Innes NSW YGTH Griffith Airport Griffith NSW YHAY Hay Airport Hay NSW YIVL Inverell Airport Inverell NSW YIVO Ivanhoe Aerodrome Ivanhoe NSW YKMP Kempsey Airport Kempsey NSW YLHI Lord Howe Island Airport Lord Howe Island NSW YLIS Lismore Regional Airport Lismore NSW YLRD Lightning Ridge Airport Lightning Ridge NSW YMAY Albury Airport Albury NSW YMDG Mudgee Airport Mudgee NSW YMER -

The United Republic of Tanzania Ministry of Works, Transport and Communication Tanzania Airports Authority Proposed Projects

THE UNITED REPUBLIC OF TANZANIA MINISTRY OF WORKS, TRANSPORT AND COMMUNICATION TANZANIA AIRPORTS AUTHORITY PROPOSED PROJECTS WRITE UP FOR THE BELGIAN TRADE MISSION TO TANZANIA NOVEMBER, 2 0 1 6 , S No. REMARKS I. PROJECT NAME Upgrading of MWANZA AIRPORT PROJECT CODE 4209 PROJECT LOCATION IATA:MWZ; ICA0:1-1.TMW; with elevation above mean sea level (AMSL) 3763ft/1147m FEASIBILITY STUDY Feasibility Study for construction of new terminal building REMARKS and landside pavements, parallel taxiway, widening of runway 45wide to 60m including relocation of AGL System and improvement of storm water drainage was completed in June, 2016 STATUS Contractor for extension of runway, rehabilitation of taxiway to bitumen standard, extension of existing apron and cargo apron, construction of control tower, cargo building, power house and water supply system has resumed to site. ncti, ahold03-)3 ConSkiNclp4) N_ Teicyrri2 WORKS REQUIRING and landside paveThents, parallel taxiway, widening of runway FUNDING 45wide to 60m including relocation of AGL System and improvement of storm water drainage PROJECT COST ESTIMATES/ USD.113 Million FINANCING GAP1 • Improved efficiency and comfort upon construction of new terminal building. • Improved efficiency upon installation of AGL and NAVAIDS • Improved safety upon Construction of Fire Station and PROJECT BENEFITS associated equipment • Improved safety and security upon construction of Control Tower • Improved security upon implementation of security programs. FINANCING MODE PPP, EPC, Bilateral and Multilateral Financing