Tna Convention & Coin Show Tna Convention & Coin Show

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Public Option in Housing Finance

The Public Option in Housing Finance Adam J. Levitin†* and Susan M. Wachter** The U.S. housing finance system presents a conundrum for the scholar of regulation because it defies description using the traditional regulatory vocabulary of command-and-control, taxation, subsidies, cap-and-trade permits, and litigation. Instead, since the New Deal, the housing finance market has been regulated primarily by government participation in the market through a panoply of institutions. The government’s participation in the market has shaped the nature of the products offered in the market. We term this form of regulation “public option” regulation. This Article presents a case study of this “public option” as a regulatory mode. It explains the public option’s rise as a governmental gap-filling response to market failures. The public option, however, took on a life of its own as the federal government undertook financial innovations that the private market had eschewed, in particular the development of the “American mortgage” — a long-term, fixed-rate fully amortizing mortgage. These innovations were trend-setting and set the tone for entire housing finance market, serving as functional regulation. The public option was never understood as a regulatory system due to its ad hoc nature. As a result, its integrity was not protected. Key parts of the system were privatized without a substitution of alternative regulatory measures. The consequence was a return to the very market failures that led to the public option in the first place, followed by another round of ad hoc public options in housing finance. This history suggests that an † Copyright © 2013 Adam J. -

Catalog DD Feb 8 Auction

Sale Location Hampton Inn Springboro OHIO Elite Winter Coin Currency Auction Feb 8 Rolling M Auctions 1 1833 Bust Dime Last 3 High Awesome Choice UNC 39 1946-S BTW Half Dollar NGC MS-65 Good Strike Tone 2 1921-D Mercury Dime Rainbow Color Key Date 40 1824/4 Bust Half Dollar VG 3 1805 Bust Dime Heraldic Eagle Very Good 41 1802/1 Bust Dollar XF45 Original Luster Mintage 41,650 4 1829 Bust Half Dime Choice UNC Toned MS-61/62 LM-1 42 1795 Flowing Hair Dollar 3 Leaves PCGS VF Details Light Cleaning 5 1929 Silver 5 Bolivares Venezuela Scarce Original Tone 43 1898-O Morgan Dollar ICG 67 50129113001 Rainbow Color Rare 6 1623 Silver 1/6 Thaler Poland King Sigismund III Scarce 44 1898-O Morgan Dollar PCGS MS-67 Bright White Spectacular 7 1842 Silver 4RBS NGC MS-63 High Grade Scarce Attractive 45 1896-O Morgan Dollar PGCS MS-61 Bright White 8 1844 Seated Dime VF Rare Mintage 72,500 46 1881-CC Morgan Dollar MS65 9 1831 Bust Half Dime Choice UNC Toned Original 47 1921 Peace Dollar PCGS MS-63 Key Date 10 1890-S Morgan Dollar Redfield Collection MS65 Toning 48 1875-S Trade Dollar AU 11 1891-S Morgan Dollar GEM BU Rainbow Tone Scarce 49 1876-S Trade Dollar AU 12 1892-CC Morgan Dollar NGC AU-50 50 1927 Peace Dollar PCGS MS-64 13 1897-S Morgan Dollar PCGS MS-65 51 1934-D Peace Dollar PCGS MS-64 Bright White 14 1883 Morgan Dollar PCGS MS-66 52 1882-CC Morgan Dollar PCGS MS-64 GSA 15 1877 Trade Dollar AU/UNC with P/L Quality 53 1879-O Morgan Dollar GEM BU 16 1886-S Morgan Dollar MS63 P/L 54 1882-O/S Morgan Dollar Choice UNC VAM 4 17 1909-S VDB Lincoln Cent -

Download (Pdf)

VOLUME 83 • NUMBER 12 • DECEMBER 1997 FEDERAL RESERVE BULLETIN BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM, WASHINGTON, D.C. PUBLICATIONS COMMITTEE Joseph R. Coyne, Chairman • S. David Frost • Griffith L. Garwood • Donald L. Kohn • J. Virgil Mattingly, Jr. • Michael J. Prell • Richard Spillenkothen • Edwin M. Truman The Federal Reserve Bulletin is issued monthly under the direction of the staff publications committee. This committee is responsible for opinions expressed except in official statements and signed articles. It is assisted by the Economic Editing Section headed by S. Ellen Dykes, the Graphics Center under the direction of Peter G. Thomas, and Publications Services supervised by Linda C. Kyles. Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis Table of Contents 947 TREASURY AND FEDERAL RESERVE OPEN formance can improve investor and counterparty MARKET OPERATIONS decisions, thus improving market discipline on banking organizations and other companies, During the third quarter of 1997, the dollar before the Subcommittee on Capital Markets, appreciated 5.0 percent against the Japanese yen Securities and Government Sponsored Enter- and 0.8 percent against the German mark. On a prises of the House Committee on Banking and trade-weighted basis against other Group of Ten Financial Services, October 1, 1997. currencies, the dollar appreciated 1.4 percent. The U.S. monetary authorities did not undertake 96\ Theodore E. Allison, Assistant to the Board of any intervention in the foreign exchange mar- Governors for Federal Reserve System Affairs, kets during the quarter. reports on the Federal Reserve's plans for deal- ing with some new-design $50 notes that 953 STAFF STUDY SUMMARY were imperfectly printed, including the Federal Reserve's view of the quality and quantity of In The Cost of Implementing Consumer Finan- $50 notes currently being produced by the cial Regulations, the authors present results for Bureau of Engraving and Printing, the options U.S. -

Alliance Coin & Banknote World Coinage

Alliance Coin & Banknote Summer 2019 Auction World Coinage 1. Afghanistan - Silver 2 1/2 Rupee SH1300 (1921/2) KM.878, VF Est $35 2. Alderney - 5 Pounds 1996 Queen's 70th Birthday (KM.15a), a lovely Silver Proof Est $40 with mixed bouquet of Shamrocks, Roses and Thistle (etc.) on reverse 3. A lovely Algerian Discovery Set - A 9-piece set of Proof 1997 Algerian coinage, each Est $900-1,000 PCGS certified as follows: 1/4 Dinar PR-67 DCAM, 1/2 Dinar PR-69 DCAM, Dinar PR-69 DCAM, 2 Dinar PR-69 DCAM, 5 Dinar PR-69 DCAM, 10 Dinar PR-67 DCAM, 20 Dinar (bimetal Lion) PR-69 DCAM, 50 Dinar (bimetal Gazelle) PR-68 DCAM, completed by a lovely [1994] 100 Dinars bimetal Horse issue, PR-68 DCAM. All unlisted in Proof striking, thus comprising the only single examples ever certified by PCGS, with the Quarter and Half Dinar pieces completely unrecorded even as circulation strikes! Set of 9 choice animal-themed coins, and a unique opportunity for the North African specialist 4. Australia - An original 1966 Proof Set of six coins, Penny to Silver 50 Cents, housed in Est $180-210 blue presentation case of issue with brilliant coinage, the Half Dollar evenly-toned. While the uncirculated sets of the same date are common, the Proof strikings remain very elusive (Krause value: $290) 5. Australia - 1969 Proof Set of 6 coins, Cent to 50 Cents (PS.31), lovely frosted strikings Est $125-140 in original plastic casing, the Five Cent slightly rotated (Cat. US $225) 6. -

Data Appendix

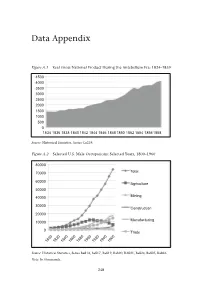

Data Appendix Figure A.1 Real Gross National Product During the Antebellum Era: 1834–1859 4500 4000 3500 3000 2500 2000 1500 1000 500 0 1834 1836 1838 1840 1842 1844 1846 1848 1850 1852 1854 18561858 Source: Historical Statistics, Series Ca219. Figure A.2 Selected U.S. Male Occupations: Selected Years, 1800–1960 80000 70000 Total 60000 Agriculture 50000 40000 Mining 30000 Construction 20000 Manufacturing 10000 0 Trade 1800 1820 1840 1860 1880 1900 1920 1940 1960 Source: Historical Statistics, Series Ba814, Ba817, Ba819, Ba820, BA821, Ba824, Ba825, Ba826. Note: In thousands. 248 Source Source Note Source Figure A.5 Figure A.4 Figure A.3 : ThisistheSchwert’sIndexofCommonStock. : HistoricalStatistics,SeriesAa36,Aa46, Aa56. : HistoricalStatistics,SeriesCh411. : HistoricalStatistics,SeriesCj979. 100000000 150000000 200000000 250000000 300000000 100000 120000 10 12 14 16 50000000 20000 40000 60000 80000 0 2 4 6 8 0 1802 0 U.S. PopulationforSelectedYears:1790–1990 Total NumberofU.S.BusinessFailures:1857–1997 1805 Stock IndexDuringtheAntebellumEra:1802–1870 1857 1790 1830 1860 1890 1920 1950 1990 1808 1863 1869 1811 1875 1814 1881 1817 1887 1820 1893 1823 1899 1826 1905 1829 1911 1832 1917 1835 1923 1838 1929 1841 1935 1941 1844 1947 1847 1953 1850 1959 1853 Total RuralPopulation Total UrbanPopulation Total Population Total 1965 1856 Data Appendix 1971 1859 1977 1862 1983 1865 1989 1995 1868 249 Note Source Note Source Figure A.8 up totheGreatDepression:1869–1929 Figure A.7 250 Source: Figure A.6 : ThisistheIndustrialsIndex. : ThisdataisfromGallman-Kuznetsestimationandin1929dollars. -

The Problem of Predatory Lending: Price Lauren E

Maryland Law Review Volume 65 | Issue 3 Article 3 Decisionmaking and the Limits of Disclosure: The Problem of Predatory Lending: Price Lauren E. Willis Follow this and additional works at: http://digitalcommons.law.umaryland.edu/mlr Part of the Banking and Finance Commons, and the Property Law and Real Estate Commons Recommended Citation Lauren E. Willis, Decisionmaking and the Limits of Disclosure: The Problem of Predatory Lending: Price, 65 Md. L. Rev. 707 (2006) Available at: http://digitalcommons.law.umaryland.edu/mlr/vol65/iss3/3 This Article is brought to you for free and open access by the Academic Journals at DigitalCommons@UM Carey Law. It has been accepted for inclusion in Maryland Law Review by an authorized administrator of DigitalCommons@UM Carey Law. For more information, please contact [email protected]. MARYLAND LAW REVIEW VOLUME 65 2006 NUMBER 3 © Copyright Maryland Law Review 2006 Articles DECISIONMAKING AND THE LIMITS OF DISCLOSURE: THE PROBLEM OF PREDATORY LENDING: PRICE LAUREN E. WILLIS* INTRODUCTION ................................................. 709 I. PREDATORY LENDING AND THE HOME LOAN MARKET ...... 715 A. The Home Lending Revolution ........................ 715 1. The Twentieth Century Marketplace: Standardized Terms, Limited and Advertised Prices, and Low Risk. 715 2. The Brave New World of ProliferatingProducts, Price, and R isk ........................................ 718 3. Evidence of Predatory Home Lending ............... 729 B. A New Definition of Predatory Lending ................. 735 II. FEDERAL LAW REGULATING THE PRICING OF HOME- SECURED LOANS: DISCLOSURE AS PANACEA ................ 741 A. The Rational Actor Decisionmaker Model ............... 741 B. CurrentFederal Law .................................. 743 C. Even a Rational Actor Could Not Use the Federal Disclosures to Price Shop in Today's Marketplace ....... -

The Real Bills Views of the Founders of the Fed

Economic Quarterly— Volume 100, Number 2— Second Quarter 2014— Pages 159–181 The Real Bills Views of the Founders of the Fed Robert L. Hetzel ilton Friedman (1982, 103) wrote: “In our book on U.S. mon- etary history, Anna Schwartz and I found it possible to use M one sentence to describe the central principle followed by the Federal Reserve System from the time it began operations in 1914 to 1952. That principle, to quote from our book, is: ‘Ifthe ‘money market’ is properly managed so as to avoid the unproductive use of credit and to assure the availability of credit for productive use, then the money stock will take care of itself.’” For Friedman, the reference to “the money stock”was synonymous with “the price level.”1 How did American monetary experience and debate in the 19th century give rise to these “real bills” views as a guide to Fed policy in the pre-World War II period? As distilled in the real bills doctrine, the founders of the Fed under- stood the Federal Reserve System as a decentralized system of reserve depositories that would allow the expansion and contraction of currency and credit based on discounting member-bank paper that originated out of productive activity. By discounting these “real bills,”the short- term loans that …nanced trade and goods in the process of production, policymakers ful…lled their responsibilities as they understood them. That is, they would provide the reserves required to accommodate the “legitimate,” nonspeculative, demands for credit.2 In so doing, they The author acknowledges helpful comments from Huberto Ennis, Motoo Haruta, Gary Richardson, Robert Sharp, Kurt Schuler, Ellis Tallman, and Alexander Wolman. -

Frank Certs a Ilraipt

ujm0p il iggEa3Bafa i ViSfc JJSSt 1 - - JgtfLaag vv Xt AMZBS OJ1 Jf ASsVIJH iawaiianaJDttjC pnarHasar4ia - c c a Sanparill Tjp fa w t m la s s rl Jl o ri CLlMIKD IiT uLian nach so J oo sin tee HE HAWAIIAN GAZETTE CO Limited SlUaei 2loehes sea tv n rw itmnvc aUUues Steches ass aee tm Ioi its W Every Tuesday Morning 4S leches tteel m Uoerl ieo se siset Quarter t Col eani em t9e itoe is M FI DOLLARS PER ANNUM Thifaoruoiama see t iae see as cl tl r Ilalfer Ones tiMi u e i nsr PATAIirFIX ADrAXCB TWTllvt ClBmn IS MM MoafTtorfwe One Celcma I Wtff 0 am SCPofloeoCTI I orris Mtlrorriliera SGU3 In Atltatuv nailnB rarda vtfi srrrmM A es flu incloeespostagesprfrald ariowedadlseeestfreitttfcertrateswhIeilawSsr MnsrrsimsestsT MAXAGEll vij a8reTTsinniTwiwrs7CTjsr R Atiraraleaadnrtissstsnta sottstbeeee ITl la BO wfH T-- ATKINSON I ROBERT CRIEVE withthe say whan ordered ef setlee W A them TheratefeharssaTectratttthabrcsIestst VOL XXI No 51 1886 mniiunf1 far Eaitani Amerleae adrerllaeneetsjer Off iueW lltaltlmgMeritalStvpirSi HONOLULU TUESDAY FEBRUARY 2 WHOLE No 1099 crivtum may be mada by bank tUelo er Ire seel Mad age stamps Only a Sons position and get back to nature again tlio bel- ¬ Srtsincss ter American Quick farts iUccIjamcal axis Ulctljnnitnl Cnrts Jnsttrawt JToticr3 3nsuroiue STotitts Xortign It waiotilya ttniple ballad rtrtisnntnts sour to a can lew throne Ttirrr were none hal fciiewbe anjrer Tho Sovoroicns or Christendom BISHOP CO CD C ROVE TELEPHONE 55 Boston Board of Underwriters F A SCIIAllFHR WXLLIAM O SMTXH And few thai Itwdcd Ibe eonc -

FDIC Banking Review, Vol. 17, No. 4

Banking Review 2005 VOLUME 17, NO. 4 The U.S. Federal Financial Regulatory System: Restructuring Federal Bank Regulation (page 1) by Rose Marie Kushmeider Most observers of the U.S. financial regulatory system would agree that if it did not exist, no one would invent it. Most, however, would also admit that the system–despite all its faults–has served both the financial services industry and consumers well. This paper looks at arguments for and against reform in the context of changes taking place within the industry and around the world in other financial regulatory systems. Consolidation in the U.S. Banking Industry: Is the “Long, Strange Trip” About to End? (page 31) by Kenneth D. Jones and Tim Critchfield Consolidation has been an enduring trend in the U.S. banking industry for more than two decades. This article provides an overview of the structural changes that have occurred and explores the empirical research to determine how consolidtion has affected such things as asset concentration, competition, banking efficiency and profitability, shareholder value, and the availability and pricing of banking services. Finally, the authors speculate on how the current forces of change might affect the industy’s structure going forward. The views expressed are those of the authors and do not necessarily reflect official positions of the Federal Deposit Insurance Corporation. Articles may be reprinted or abstracted if the FDIC Banking Review and author(s) are credited. Please provide the FDIC’s Division of Insurance and Research with a copy of any publications containing reprinted material. Acting Chairman Martin J. Gruenberg Director, Division of Insurance Arthur J. -

Central Banking in the United States: a Fragile Commitment to Price Stability and Independence

Contents ~ Foreword ~ Central Banking in the United States: A Fragile Commitment to Price Stability and Independence ~ Comparative Financial Statements ~ Directors ~ Officers Forevvord ~ ineteen ninety-one was a year of changes policy adjustments-and there will doubtless be and often the changes took unexpected turns. many - should focus on this goal. The long-awaited bank reform bill was passed, but disappointed many in its lack of vision. The Twenty-three directors, representing banking, economy, which many observers expected to business, agriculture, consumer, and labor inter recover, seemed to stall and then founder at the ests, guide the Federal Reserve Bank of Cleveland close of the year. and its Branches. Their contributions are highly valued, as is the participation of our Small Bank At the Federal Reserve Bank of Cleveland, and Small Business Advisory Councils. change also occurred with the departure of our president, W Lee Hoskins, and the appointment Special thanks are extended to those directors of our new president, Jerry L. Jordan. who have completed their terms of service on our boards. We are especially grateful for the leader Lee, who left to become president and chief ship of Kate Ireland (national chairman, Frontier executive officer of The Huntington National Nursing Service of Wendover, Kentucky), who Bank, made noteworthy contributions on several was chairman of our Cincinnati Branch board fronts. He developed influential public policy of directors. We also appreciate the contributions positions on the importance of price stability of Allen L. Davis (president and chief executive and financial regulatory reform. Under his officer of The Provident Bank, Cincinnati, Ohio), leadership, the Fourth District made signifi who served on our Cincinnati Branch board; and cant progress toward becoming the lowest-cost E. -

The National Monetary Commission: American Banking’S Debt to Europe

1 The National Monetary Commission: American Banking’s Debt to Europe Zack Saravay Honors Thesis Submitted to the Department of History, Georgetown University Advisor: Professor Katherine Benton-Cohen Honors Program Chairs: Professors Amy Leonard and Katherine Benton-Cohen 8 May 2017 2 Table of Contents ACKNOWLEDGEMENTS ........................................................................................................................ 3 INTRODUCTION ....................................................................................................................................... 4 HISTORIOGRAPHICAL REVIEW .................................................................................................................. 6 Creation of the Federal Reserve ........................................................................................................... 7 Progressive Era Economics ................................................................................................................ 13 BACKGROUND – THE NATIONAL BANKING SYSTEM (1863-1908) ......................................................... 15 CHAPTER I. ORIGINS OF THE NMC (1908) ...................................................................................... 25 THE BATTLE FOR CURRENCY REFORM ................................................................................................... 25 THE ALDRICH-VREELAND ACT ............................................................................................................... 28 COMPOSITION AND SCOPE OF -

Report of the Director of the Mint

Fiscal Year Ended June 30, 1915 EEPORT OF THE DIRECTOR OF THE MINT. TREASURY DEPARTMENT, BUREAU OF THE MINT, Washington, D. 0., Novemher 1, 1915. SIR: In compliance with the provisions of section 345, Revised Statutes of the United States, I have the honor to submit herewith a report covering the operations of the mints and assay offices of the United States for the fiscal year ended June 30, 1915, being the forty- third annual report of the Director of the Mint. There is also sub mitted for publication in connection therewith the annual report of this bureau upon the production and consumption of the precious metals in the United States for the calendar year 1914. OPERATIONS OF THE MINTS AND ASSAY OFFICES. In many ways the fiscal year 1915 was the most eventful in the history of the mmt service; certainly it was as regards the New York assay office and the San Francisco Mint. The movement of gold from the United States in the first three months and the movement of this metal to our shores in the last three months were on such a tremendous scale that the patience, skill, and capacity of the officials and employees at these institutions w^ere sorely taxed. Since July 1, 1915, the volume of business has increased so steadily and so rapidly that the records show the total value of the deposits at the New York assay office for the first four months of the fiscal year 1916 to be $126,224,600 or nearly that of the deposits for the whole of 1908—$131,X92',227—which has heretofore been this office's banner fiscal year.