Reports of Select Committees on the 2014/15 Annual Reviews of Crown

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Annual Report 2019

ANNUAL REPORT SEPTEMBER 2019 Obligations creating opportunity “The best thing a senior leader can do is become incredibly interested, not in how the organisation failed to prevent the event, but in how the organisation failed to control the event…the presence of control is the magic potion for leaders.” Todd Conklin to Forum members, July 2019. www.zeroharm.org.nz Who we are The Forum is a group of CEOs, directors and country heads who are committed to becoming better leaders of health and safety in our organisations and industries. What we want for New Zealand Safe, healthy and productive workplaces. Why we’re here To engage, educate and elevate New Zealand CEOs so they have the skills and confidence to lead healthy and safe organisations. What we’ll do • Build CEO competence • Help CEOs influence and enable the workforce and supply chain • Connect CEOs to take more effective action • Help CEOs work with others to build the movement • Assess progress to deliver on our promises. “Every time I go to a Forum event I come away with a gem. I don’t walk away without thinking, wow, that was interesting.” “The Forum is a great vehicle, it’s a place I can be challenged in my views, learn from others and have a chance to refocus.” “The Forum’s Executive Leadership Programme is the best thing I ever did – it was real, gave me simple tactics and focused my energy on the heart and the mind of leadership.” CEO members 2019 3 Our members George Reed Craig Davidson Andrew Tombs Dean Brown General Manager Managing Director NZ CEO CEO 1st Maintenance -

Nelson Airport's New Terminal – Overview of the Design of a Large

Conference issue Nelson Airport’s new terminal – overview of the design of a large-span engineered timber specialist building Evzˇen Novak, Samantha Zondag, Sarah Berry and Simon Hardy Engineered timber in the Nelson Airport Terminal under construction. Photo courtesy of David Evison Abstract more closely reflects the needs of the end users of the building. In providing this viewpoint, the authors hope The Nelson Airport Terminal is a new large-span that it facilitates a raised producer awareness of the building that replaces the existing terminal building at issues facing the incorporation of engineered timber the airport. The structure and interior of the building into any building and, more fundamentally, an increase relies on engineered timber (LVL and plywood) to in the use of engineered timber in the building stock achieve the open spans required and create a unique New Zealand produces each year. airport environment. Beginning with the brief and a short description This paper serves to outline a significant end use of the building, the paper goes on to discuss the design for engineered timber and sets out, from a designer’s drivers for the building and how the selected drivers perspective, the journey from initial idea to end result. supported the use of engineered timber, one very major The designer’s perspective is clearly not the same as element of the design strategy. An overview of the the producer’s. In general, the designer’s perspective design and construction processes, particularly dealing NZ Journal of Forestry, November 2018, Vol. 63, No. 3 11 Conference issue with innovations such as the use of resilient slip friction Initially, the design team investigated whether an joints (RSFJs) and pre-fabrication, is provided along expansion of the existing terminal would be feasible, or if with some preliminary learnings. -

Owner's Expectations Manual

Owner’s Expectations Manual Owner’s Owner’s Expectations Manual | Crown Ownership Monitoring | Crown Unit Crown Ownership Monitoring Unit July 2012 © Crown Copyright reserved ISBN 978-0-478-39662-1 (Print) ISBN 978-0-478-39663-8 (Online) This work is licensed under the Creative Commons Attribution 3.0 New Zealand licence. In essence, you are free to copy, distribute and adapt the work, as long as you attribute the work to the Crown and abide by the other licence terms. To view a copy of this licence, visit http://creativecommons.org/licenses/by/3.0/nz/. Please note that no departmental or governmental emblem, logo or Coat of Arms may be used in any way which infringes any provision of the Flags, Emblems, and Names Protection Act 1981. Attribution to the Crown should be in written form and not by reproduction of any such emblem, logo or Coat of Arms. Internet The URL for this document on the Treasury’s Crown Ownership Monitoring Unit’s website at July 2012 is http://www.comu.govt.nz/publications/guidance/owners-expectations-manual/ Persistent URL http://purl.oclc.org/nzt/g-oem Table of Contents What’s New? .............................................................................................................................................................. 5 Summary of Significant Updates to the Owner’s Expectations Manual ........................................................................ 5 1 Introduction ...................................................................................................................................................... -

Act's Alternative Budget 2014

A budget for growth, a budget for prosperity, a budget for all New Zealanders ACT’S ALTERNATIVE BUDGET 2014 DR JAMIE WHYTE, ACT LEADER 10 May 2014 Today, I am pleased to present ACT’s alternative alternatives. We are reducing middle class and to the budget Bill English will present on corporate welfare because it is an expensive Thursday next week. It sets out ACT’s aspiration money-go-round of no benefit to New Zealand for a prosperous future for New Zealanders, society but only to bureaucrats and lobbyists. which cannot be achieved with the “tax and spend” policies of all the other parties. It is We demonstrate how New Zealand could now a budget that drives achievement through move to a top rate of income tax of 24% and a freedom, choice and responsibility. company tax rate of 24%. And we can do this without reducing spending for health, education ACT’s alternative budget is about growth, or welfare for low income earners. prosperity and fairness. We are putting workers, business owners, investors and entrepreneurs The budget I am presenting today is first. We are rejecting the tall poppy syndrome comprehensive and fully costed, using official and saying it is wrong to simply impose more Treasury figures. The benefits are understated. and more tax on the most successful New Zealanders. The Government’s budget is predicting 3% growth. Labour’s uncosted tax, spend and borrow In this alternative budget I am taking ACT back to policies will cost growth and jobs. My alternative its original role of providing economically sound budget will lift growth to 5%. -

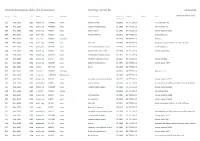

Reports of Select Committees on the 2014/15

I. 20B Reports of select committees on the 2014/15 annual reviews of Crown entities, Government departments and Offices of Parliament, public organisations, and State enterprises Fifty-first Parliament March 2016 I. 20B I. 20B Contents Crown entity/public Select Committee Date presented Page organisation/State enterprise Government of New Zealand for the Finance and Expenditure 04 Mar 2016 11 year ended 30 June 2015, Financial Statements of the Economic Development and Infrastructure Sector Accident Compensation Corporation Transport and Industrial 16 Mar 2016 37 Relations Air New Zealand Limited Finance and Expenditure 10 Mar 2016 65 Airways Corporation of New Zealand Transport and Industrial 09 Mar 2016 93 Limited Relations Broadcasting Commission Commerce 18 Mar 2016 95 Broadcasting Standards Authority Commerce 23 Feb 2016 99 Canterbury Earthquake Recovery Government Administration 18 Mar 2016 101 Authority Civil Aviation Authority of New Transport and Industrial 09 Mar 2016 93 Zealand Relations Commerce Commission Commerce 11 Mar 2016 107 Crown Fibre Holdings Limited Commerce 15 Feb 2016 111 Earthquake Commission (reported with the Finance and Expenditure 10 Mar 2016 117 Report from the Controller and Auditor- General, Earthquake Commission: Managing the Canterbury Home Repair Programme – follow-up audit) Electricity Authority Commerce 15 Feb 2016 141 Electricity Corporation of New Zealand Commerce 23 Feb 2016 99 Limited External Reporting Board Commerce 23 Feb 2016 99 FairWay Resolution Limited Transport and Industrial 16 Mar 2016 -

Covid-19 Impact on Kiwifruit Industry

VOL 95 | NO 04 | AUGUST 2020 HORTICULTURE NEW ZEALAND Covid-19 impact on kiwifruit industry In this issue 14 Attracting the 30 Co-operation key to 36 We pulled it off: harvesting next generation coping with Covid-19 through a pandemic NEW Break the cycle fast! Unique, fast acting and systemic control of Codling Moth, Leaf Roller Caterpillar and Bronze Beetle in Pipfruit. • New chemistry with a unique spectrum of pest control • Strong proven activity against all life stages of moths • Fast cessation of feeding with systemic activity and excellent length of activity • Soft on key beneficials Insist on Vayego from Bayer today! We’re with you in the field | cropscience.bayer.co.nz Registered pursuant to the ACVM act 1997, No P9623. See www.foodsafety.govt.nz for registration conditions. Approved pursuant to the HSNO Act 1996, No HSR101424. See www.epa.govt.nz for approval conditions. Vayego® is a registered Trademark of the Bayer Group. © Bayer New Zealand 2020. BAC 1951 NEW 53 16 Break the cycle fast! 26 Contents AUGUST 2020 42 Up Front Your Industry 48 An Adventure in Olives 2 President’s Word: 23 Citrus grower — Russell Borman 50 Automation and Agritech What’s going to be involved 26 Business leader turned get Funding Boost in growing New Zealand? mandarin grower Technical 4 The Chief Executive: 27 Ready for lockdown audit Covid-19 has changed the world 28 Employing people who lost 53 Strategies for chemical crop their jobs due to Covid-19 management Your Levy at Work 30 Co-operation and strong 58 MetService update: La Niña Watch 8 Natural resources and environment relationships key to coping 60 Canopy Management — looking 10 Farm Environment Plan update with Covid-19 back, looking ahead Unique, fast acting and systemic control of Codling 11 GAP, safety and technology 32 Zespri — Covid-19 64 Drainage problems in a drought? 12 Different rules create concern 34 Good planning key to response What’s New Moth, Leaf Roller Caterpillar and Bronze Beetle in Pipfruit. -

Contents Page for Jenny Cassie's Crown Entities Act Seminars

4. CAPACITY AND POWERS OF CROWN ENTITIES Jenny Cassie, Barrister Introduction This chapter discusses the provisions of the Crown Entities Act which relate to the capacity and exercise of powers of statutory entities and, to a more limited degree, Crown entity companies and Crown entity subsidiaries. The commentary covers the generic model as covered by the Act and does not, for example, cover the exercise of powers by statutory officers whose powers must be exercised independently of an entity.72 Legal status Statutory entities, Crown entity companies and Crown entity subsidiaries are all bodies corporate and are therefore legal entities which exist separately from their members, office holders, employees and, importantly, the Crown.73 This separation is illustrated most acutely by the position of statutory entities that are corporations sole. A single person, for example, the Privacy Commissioner, may have corporate status by virtue of being declared a corporation sole. This enables an artificial line to be drawn between the person as an individual and the office as a legal person. Crown entity status contrasts with Departments, which are legally part of the Crown. Departments, having no separate legal status, can be established and disestablished by the Government by executive action. By contrast, a “statutory entity” can only be established or disestablished by legislation. Setting up Crown entity companies requires registration of a company with Ministers as shareholders.74 Capacity of statutory entities “Capacity” describes the legal ability or qualification of an entity to do something. The general rule regarding the capacity of corporations is that:75 The powers of a corporation created by statute are limited and circumscribed by the statutes which regulate it and extend no further than is expressly stated therein, or is necessarily and properly required for carrying into effect the purposes of its incorporation, or may be fairly regarded as incidental to, or consequential on, those things which the legislature has authorised. -

British Aerospace Bae J31 Jetstream Sorting: Serial Nr

British Aerospace BAe J31 Jetstream Sorting: Serial Nr. 29.08.2021 Ser.Nr. Type F/F Status Immatr. Operator Last Operator in service Engines Owner Rem. @airlinefleet.info M/Y until 601 BAe.J3102 1982 broken up G-WMCC none Maersk Air UK 08-1996 GA TPE331-10 Air Commuter ntu 602 BAe.J3101 1982 broken up N422MX none Eastern Metro Express 01-1998 GA TPE331-10 Mall Airways ntu 603 BAe.J3103 1982 broken up N603JS none Gold Aviation 01-2001 GA TPE331-10 broken up by 08-2005 604 BAe.J3101 1982 perm_wfu N78019 none Personal Airliner 05-2011 GA TPE331-10 to be broken up 605 BAe.J3102 1982 in service N408PP Corporate 06-2013 GA TPE331-10 Phil Pate 606 BAe.J3102 1982 perm_wfu LN-FAV none Coast Air 02-2007 GA TPE331-10 Royal Norwegian Air Force as instr. airframe 607 BAe.J3102 1983 perm_wfu N607BA none Professional Aviation Group 04-2008 GA TPE331-10 to be broken up 608 BAe.J3101 1983 broken up N608JX none Native American Air Serv. 03-1999 GA TPE331-10 broken up 03-2005 609 BAe.J3102 1983 broken up N609BA none Professional Aviation Group 05-2013 GA TPE331-10 610 BAe.J3103 1983 broken up G-JXTA none Jetstream Executive Travel 02-2011 GA TPE331-10 broken up 2016 611 BAe.J3101 1983 broken up N419MX none Eastern Metro Express 01-1991 GA TPE331-10 broken up 12-1997 612 BAe.J3102 1983 stored OM-NKD none SK Air 00-1999 GA TPE331-10 613 BAe.J3101 1983 in service N904EH Corporate 02-2019 GA TPE331-10 Aerostar 1 Inc. -

Briefing to the Incoming Minister for Broadcasting, Communications And

RELEASED UNDER THE OFFICIAL INFORMATION ACT Contents 1. Introduction .................................................................................................................................... 3 2. Portfolio overview ........................................................................................................................... 3 3. Portfolio responsibilities ................................................................................................................. 4 4. Responsibilities of the Ministry for Culture and Heritage .............................................................. 5 5. Opportunities and challenges for the broadcasting and digital media sector ............................... 7 6. Cross-government work on broadcasting issues ............................................................................ 8 7. Initial focus .................................................................................................................................... 10 8. About Manatū Taonga .................................................................................................................. 11 9. Annex 1: New Zealand’s Broadcasting Sector ............................................................................... 14 10. Annex 2: Broadcasting funded agencies ....................................................................................... 16 RELEASED UNDER THE OFFICIAL INFORMATION ACT 2 1. Introduction Mālō ni, Minister Faafoi. E te Minita, nau mai haere mai ki te kohinga wāhi whakapāho, -

Public Offices Subject to the Public Records Act 2005 Published September 2019 Arranged by Name of Organisation in A-Z Order

September 2019 Public Offices subject to the Public Records Act 2005 Published September 2019 Arranged by name of organisation in A-Z order. Name of organisation Organisational category Accident Compensation Corporation (ACC) Crown agent Accreditation Council Autonomous Crown entity AgResearch Limited Crown Research Institute Airways Corporation of New Zealand Limited State-Owned Enterprise Animal Control Products Limited (Pestoff) State-Owned Enterprise Ara Institute of Canterbury Tertiary education institution Armed Forces Canteen Council Executive branch of Government Arts Council of New Zealand (Creative NZ) Autonomous Crown entity AsureQuality Limited State-Owned Enterprise Auckland DHB District Health Board Auckland University of Technology (AUT) Tertiary education institution Bay of Plenty DHB District Health Board Broadcasting Commission (NZ On Air) Autonomous Crown entity Broadcasting Standards Authority Independent Crown Entity Callaghan Innovation Crown agent Callaghan Innovation Research Limited Crown entity subsidiary Canterbury DHB District Health Board Capital and Coast DHB District Health Board Central Regions' Technical Advisory Services Limited (TAS) Crown entity subsidiary Part of the Department of Internal Affairs Printed copies are uncontrolled 1 September 2019 Children's Commissioner Independent Crown entity Civil Aviation Authority of New Zealand Crown agent Commerce Commission Independent Crown entity Commercial Fisheries Services (FishServe)[Approved service Approved service delivery delivery organisation 2013-2023] -

Services at Holy Trinity

RICHMOND PARISH PROFILE WHO ARE WE? We are a committed group of Christians who endeavour to make our church a welcoming church to all. Many visitors have favourably commented on the friendly welcome they receive among us. We are in an evangelical diocese and most of our congregation tend in that direction. There are, however, a number of parishioners with a more liberal theology. Our focus tends towards what unites us rather than what we disagree on. We are a predominantly older congregation with a small number of children and very few members in the 20-40 age group bracket. We value our evangelical, Anglican heritage which does provide a unique flavour to the Richmond church scene. Our two Sunday morning services attract just over 80 people to our wooden church on the hill near the centre of the Richmond township. WHERE ARE WE? Although Richmond is geographically close to Nelson, it is administered by the Tasman District Council (www.tasman.govt.nz) which has its main council offices in Richmond. Richmond is a thriving, growing centre for the rural townships to the south and the west. The population was estimated to be 17,250 in June 2020. In the 2018 census the main ethnic breakdown of the Tasman Region was European (92.6%), Maori (8.7%), Asian (2.8%) and Pacific (1.6%). (These figures exceed 100% as people can associate with more than one ethnic group). Due both to an increasing influx of retirees and the ageing population Tasman District’s older residents (65+) are predicted to rise from 21% in 2018 to 32% in 20 years. -

Interim Report

PALMERSTON NORTH AIRPORT LIMITED INTERIM REPORT TO 31 DECEMBER 2020 FINAL INTERIM REPORT TO 31 DECEMBER 2020 PAGE 2 COMPANY DIRECTORY PALMERSTON NORTH AIRPORT LIMITED DIRECTORS: M A Georgel – Chair J E Nichols – Chair Audit & Risk Committee G F Gillespie S Vining C G Cardwell MANAGEMENT: D J Lanham Chief Executive G E Clark Commercial Manager J A Baker Finance Manager D J Yorke Infrastructure Manager D Balmer Marketing & Communications Manager B D Lawry Terminal Manager T B Cooney Safety and Security Manager B Parkinson Airfield Operations Manager REGISTERED OFFICE: Palmerston North Airport Terminal Building Airport Drive PALMERSTON NORTH 4442 Phone: +64 6 351 4415 e-mail: [email protected] Web: www.pnairport.co.nz TRADING BANKERS: Bank of New Zealand LEGAL ADVISORS: CR Law AUDITORS: Audit New Zealand (on behalf of The Auditor-General) INTERIM REPORT TO 31 DECEMBER 2020 PAGE 3 CONTENTS: PAGE: Joint Report of Chair and Chief Executive 4 Statement of Service Performance 6 Financial Statements 7 - 11 Notes to the Financial Statements 12 - 15 INTERIM REPORT TO 31 DECEMBER 2020 PAGE 4 JOINT REPORT OF THE CHAIR & CHIEF EXECUTIVE FOR THE SIX MONTHS ENDING 31 DECEMBER 2020 With a backdrop of the impact of the COVID-19 pandemic on financial performance, the company remained focused on the safety and wellbeing of its people, customers and tenants during the six months to December 2020. Highlights include zero lost time injuries, the ongoing development of the Company’s OneTeam Wellness programme, CAA certification of the Company’s Safety Management System (SMS), continued compliance with CAA Rule Part 139, and the ability to provide ongoing support to community groups including sponsorships and support of charities albeit on a smaller scale.