Samia Umer June 2018 Is Valued at PKR 77.82

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

IN the SUPREME COURT of PAKISTAN (Appellate Jurisdiction)

IN THE SUPREME COURT OF PAKISTAN (Appellate Jurisdiction) Present: Mr. Justice Manzoor Ahmad Malik Mr. Justice Syed Mansoor Ali Shah C.P.1290-L/2019 (Against the Order of Lahore High Court, Lahore dated 31.01.2019, passed in W.P. No. 5898/2019) D. G. Khan Cement Company Ltd. ...….Petitioner(s) Versus Government of Punjab through its Chief Secretary, Lahore, etc. …….Respondent(s) For the petitioner(s): Mr. Salman Aslam Butt, ASC. For the respondent(s): Ms. Aliya Ejaz, Asstt. A.G. Dr. Khurram Shahzad, D.G. EPA. M. Nawaz Manik, Director Law, EPA. M. Younas Zahid, Dy. Director. Fawad Ali, Dy. Director, EPA (Chakwal). Kashid Sajjan, Asstt. Legal, EPA. Rizwan Saqib Bajwa, Manager GTS. Research Assistance: Hasan Riaz, Civil Judge-cum-Research Officer at SCRC.1 Date of hearing: 11.02.2021 JUDGEMENT Syed Mansoor Ali Shah, J.- The case stems from Notification dated 08.03.2018 (“Notification”) issued by the Industries, Commerce and Investment Department, Government of the Punjab (“Government”), under sections 3 and 11 of the Punjab Industries (Control on Establishment and Enlargement) Ordinance, 1963 (“Ordinance”), introducing amendments in Notification dated 17.09.2002 to the effect that establishment of new cement plants, and enlargement and expansion of existing cement plants shall not be allowed in the “Negative Area” falling within the Districts Chakwal and Khushab. 2. The petitioner owns and runs a cement manufacturing plant in Kahoon Valley in the Salt Range at Khairpur, District Chakwal and feels wronged of the Notification for the reasons, -

World Bank Document

ENVIRONMENTAL ASSESSMENT (EA) AND THE ENVIRONMENTAL AND SOCIAL MANAGEMENT FRAMEWORK Public Disclosure Authorized PUNJAB EDUCATION SECTOR REFORMS PROGRAM-II (PESRP-II) Public Disclosure Authorized PROGRAM DIRECTOR PUNJAB EDUCATION SECTOR REFORMS PROGRAM (PESRP) SCHOOL EDUCATION DEPARTMENT GOVERNMENT OF THE PUNJAB Tel: +92 42 923 2289~95 Fax: +92 42 923 2290 url: http://pesrp.punjab.gov.pk email: [email protected] Public Disclosure Authorized Revised and Updated for PERSP-II February 2012 Public Disclosure Authorized DISCLAIMER This environmental and social assessment report of the activities of the Punjab Education Sector Reforms Program of the Government of the Punjab, which were considered to impact the environment, has been prepared in compliance to the Environmental laws of Pakistan and in conformity to the Operational Policy Guidelines of the World Bank. The report is Program specific and of limited liability and applicability only to the extent of the physical activities under the PESRP. All rights are reserved with the study proponent (the Program Director, PMIU, PESRP) and the environmental consultant (Environs, Lahore). No part of this report can be reproduced, copied, published, transcribed in any manner, or cited in a context different from the purpose for which it has been prepared, except with prior permission of the Program Director, PESRP. EXECUTIVE SUMMARY This document presents the environmental and social assessment report of the various activities under the Second Punjab Education Sector Reforms Program (PESRP-II) – an initiative of Government of the Punjab for continuing holistic reforms in the education sector aimed at improving the overall condition of education and the sector’s service delivery. -

APPOINTMENT and CONDITIONS of SERVICE) REGULATIONS, 2016 AIM: to Enforce the MDA (Appointment and Conditions of Service) Regulations 2016

DIRECTORATE OF FINANCE AND ADMINISTRATION ADMIN BRANCH AGENDA NO. 01 MDA (APPOINTMENT AND CONDITIONS OF SERVICE) REGULATIONS, 2016 AIM: To enforce the MDA (Appointment and Conditions of Service) Regulations 2016. DETAILS/ EXISTING ARRANGEMENTS: 2. MDA (Appointments and Conditions of Service) Regulations, 1980 has remained enforced and are still under implementation since 1980. Over the period of 36 years, 68 meetings of Governing Body have been held and time to time various amendments have been made in the said Regulations and its schedule. If seen critically, the current schedule of Regulations is full of amendments, tailored promotion channels and abolished posts which were otherwise necessary for smooth functioning of MDA. 3. Across the board, it has been observed that promotion criteria for various posts have been shifted from seniority-cum-fitness basis to mandatory trainings and departmental training examination. Recently the instructions of Government of the Punjab for ensuring merit based promotions basing on mandatory training/promotion exam has been received, which is also being placed for adoption by MDA. The same has also been proposed for almost all the posts whether technical or general cadre so that merit based promotions may be ensured. 4. The regulations include two parts namely appointment and the condition of service for MDA employees and its Schedule. Extensive efforts have been put in for making this schedule practicable. An effort has been made that no post may remain stagnant and mostly post has been given promotion prospects. The same did not exist in the current Schedule. There were many discrepancies as already mentioned above which have also been rectified. -

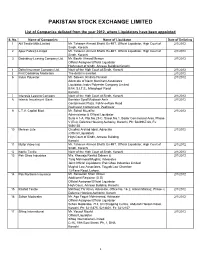

List of Liquidators

PAKISTAN STOCK EXCHANGE LIMITED List of Companies delisted from the year 2012, where Liquidators have been appointed S. No. Name of Companies Name of Liquidator Date of Delisting 1 Alif Textile Mills Limited Mr. Tahseen Ahmed Bhatti, Ex-MIT, Official Liquidator, High Court of 2/1/2012 Sindh, Karachi 2 Apex Fabrics Limited Mr. Tahseen Ahmed Bhatti, Ex-MIT, Official Liquidator, High Court of 2/1/2012 Sindh, Karachi 3 Dadabhoy Leasing Company Ltd. Mr. Bashir Ahmed Memon 2/1/2012 Official Assignee/Official Liquidator High Court of Sindh, Annexe Building,Karachi. 4 Delta Insurance Company Ltd. Nazir of the High Court of Sindh, Karachi 2/1/2012 5 First Dadabhoy Modaraba The detail is awaited. 2/1/2012 6 Indus Polyester Mr. Saleem Ghulam Hussain 2/1/2012 Advocate of Navin Merchant Associates Liquidator: Indus Polyester Company Limited B/54, S.I.T.E., Manghopir Road Karachi 7 Interasia Leasing Company Nazir of the High Court of Sindh, Karachi 2/1/2012 8 Islamic Investment Bank Barrister Syed Mudassir Amir 2/1/2012 Containment Plaza, Fakhr-e-Alam Road Peshawar Cantonment, Peshawar 9 L.T.V. Capital Mod. Mr. Sohail Muzaffar 2/1/2012 Administrator & Official Liquidator Suite # 1-A, Plot No.25-C, Street No.1, Badar Commercial Area, Phase- V (Ext), Defence Housing Authority, Karachi, Ph: 5843967-68, Fx: 5856135 10 Mehran Jute Chudhry Arshad Iqbal, Advocate 2/1/2012 (Official Liquidator) High Court of Sindh, Annexe Building Karachi. 11 Myfip Video Ind. Mr. Tahseen Ahmed Bhatti, Ex-MIT, Official Liquidator, High Court of 2/1/2012 Sindh, Karachi 12 Norrie Textile Nazir of the High Court of Sindh, Karachi 2/1/2012 13 Pak Ghee Industries M/s. -

Syed Mansoor Ali Shah, J

Stereo. H C J D A 38. Judgment Sheet IN THE LAHORE HIGH COURT LAHORE JUDICIAL DEPARTMENT Case No: W.P. 5406/2011 Syed Riaz Ali Zaidi Versus Government of the Punjab, etc. JUDGMENT Dates of hearing: 20.01.2015, 21.01.2015, 09.02.2015 and 10.02.2015 Petitioner by: Mian Bilal Bashir assisted by Raja Tasawer Iqbal, Advocates for the petitioner. Respondents by: Mian Tariq Ahmed, Deputy Attorney General for Pakistan. Mr. Muhammad Hanif Khatana, Advocate General, Punjab. Mr. Anwaar Hussain, Assistant Advocate General, Punjab. Tariq Mirza, Deputy Secretary, Finance Department, Government of the Punjab, Lahore. Nadeem Riaz Malik, Section Officer, Finance Department, Government of the Punjab, Lahore. Amici Curiae: M/s Tanvir Ali Agha, former Auditor General of Pakistan and Waqqas Ahmad Mir, Advocate. Assisted by: M/s. Qaisar Abbas and Mohsin Mumtaz, Civil Judges/Research Officers, Lahore High Court Research Centre (LHCRC). “The judiciary should not be left in a position of seeking financial and administrative sanctions for either the provision of infrastructure, staff and facilities for the judges from the Executive and the State, which happens W.P. No.5406/2011 2 to be one of the largest litigants….autonomy is required for an independent and vibrant judiciary, to strengthen and improve the justice delivery system, for enforcing the rule of law1.” Syed Mansoor Ali Shah, J:- This case explores the constitutionalism of financial autonomy and budgetary independence of the superior judiciary on the touchstone of the ageless constitutional values of independence of judiciary and separation of powers. 2. Additional Registrar of this High Court has knocked at the constitutional jurisdiction of this Court, raising the question of non-compliance of the executive authority of the Federation by the Provincial Government, as the direction of the Prime Minister to the Provincial Government to enhance the allowances of the staff of the superior judiciary goes unheeded. -

Lahore High Court Lahore

Stereo. H C J D A 38. Judgment Sheet IN THE LAHORE HIGH COURT LAHORE JUDICIAL DEPARTMENT Case No: W. P. No.115949/2017 Maple Leaf Cement Factory Versus Environmental Protection Ltd. Agency, etc. JUDGMENT Date of hearing: 21.12.2017 Petitioner by: M/s. Mansoor Usman Awan, Shazeen Abdullah and Hussain Ibrahim, Advocates. Respondent (s) M/s Asma Hamid and Anwaar Hussain, by: Additional Advocates General, Punjab. Mr. Arshad Mehmood, Secretary, Mines and Mineral, Government of the Punjab. Mr. Zafar Javaid, Director, Mines and Mineral, Government of the Punjab. Mr. Muhammad Javaid, Superintendent, Mines and Mineral, Government of the Punjab. Mian Ejaz Majeed, Deputy Director (L&E), EPA. Mr. Asim Rehman, Deputy Director (EIA), EPA. The fate of the Creation is the fate of the humanity. - E.O.Wilson1 Syed Mansoor Ali Shah, C.J:- Facts: Brief facts, as argued by the learned counsel for the petitioner, are that the cement plant of the petitioner was set up in the year 1956 by the West Pakistan Industrial Development Corporation with the 1 The Creation - An appeal to save life on Earth – by E.O.Wilson P.14 W.P. No.115949/2017 2 production capacity of 3000 tonnes per annum. The cement plant was privatized in the year 1992 when the petitioner company purchased the same. The production capacity of the plant at that time of the purchase of the plant by the petitioner was 4000 tonnes per annum. Later on the production capacity of the cement plant was enhanced by the petitioner and Line-II of the plant was added in the year 2007 with an additional production capacity of 7,000 tonnes per annum. -

The Pakistani Lawyers' Movement and the Popular

NOTES THE PAKISTANI LAWYERS’ MOVEMENT AND THE POPULAR CURRENCY OF JUDICIAL POWER “I support the lawyers,” said the Pakistani farmer on the train from Lahore, “because if Musharraf can do whatever he wants to this man, the Chief Justice of Pakistan, then none of us is safe.”1 It was the summer of 2008, and for several months Pakistani lawyers had been leading protests seeking the restoration to office of sixty-plus superior court judges,2 including Chief Justice Iftikhar Mohammad Chaudhry, who had been suspended by President Pervez Musharraf.3 The farm- er’s response to questions about his thoughts on the protests was typi- cal of Pakistanis at the time in its clear-headed articulation of the symbolic importance of the lawyers’ struggle and in its implicit under- standing of the central function of an independent judiciary. Indeed, the Chief Justice was the closest to a personal embodiment of “the law” that one could find in Pakistan. If even he served at the pleasure of a dictator — so the story went —the capacity of the law to constrain this dictator and protect ordinary Pakistanis was perilously weak. In March 2007, Chaudhry refused the urging of five generals to re- sign and was removed by Musharraf. Two years later, with Musharraf in exile and a civilian government in power, nationwide protests re- turned Chaudhry to his position atop the nation’s highest court.4 Af- ter twenty-four months of struggle, the lawyers’ movement thus ended with an improbable victory. Moreover, in a nation where the courts historically have followed the dictates of the military and allowed for the repeated subversion of the country’s constitutions,5 the restoration ––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––– 1 Interview with Pakistani farmer, on train from Lahore, Pak. -

Annual Report 2015–2016

SUPREME COURT OF PAKISTAN ANNUAL REPORT June 2015 - May 2016 ANNUAL REPORT June 2015 - May 2016 Supreme Court of Pakistan ANNUAL REPORT June 2015 - May 2016 Supreme Court of Pakistan Constitution Avenue, Islamabad Ph: 051-9220581-600 Fa x: 051-9215306 E-mail: [email protected] Web: www.supremecourt.gov.pk Branch Registry Lahore Nabha Road. Ph: 042-99212401-4 Fax: 042-99212406 Branch Registry Karachi MR Kiyani Road. Ph: 021-99212306-8 Fax: 021-99212305 Branch Registry Peshawar Khyber Road. Ph: 091-9213601-5 Fax: 091-9213599 Branch Registry Quetta High Court of Balochistan Building Quetta. Ph: 081-9201365 Fax: 081-9202244 Published by: Supreme Court of Pakistan Compiled & edited by: Khawaja Daud Ahmad, Additional Registrar (Administration) Saleem Ahmad, Librarian, Supreme Court of Pakistan ii Supreme Court of Pakistan ANNUAL REPORT June 2015 - May 2016 CONTENTS 1. Foreword by the Chief Justice of Pakistan 1 2. Registrar’s Report 2 3. Profile of the Chief Justice and Judges 5 3.1 Profile of the Chief Justice of Pakistan 6 3.2 Profile of Judges of the Supreme Court of Pakistan 7 3.3 Chief Justices & Judges Retired During June 2015 to 34 May 2016 4. Supreme Court of Pakistan 35 4.1 Introduction 36 4.2 Seat of Supreme Court 37 4.3 Branch Registries 37 4.4 Supreme Court Composition, June 2015 to May 2016 39 4.5 Jurisdiction of the Supreme Court 40 4.6 Procedure for the Appointment of Judges of the 42 Supreme Court of Pakistan 4.7 Judicial Commission of Pakistan 43 4.8 Composition of the Judicial Commission of Pakistan 45 4.9 Judicial Commission of Pakistan Rules, 2010 45 4.10 Oath of Office 46 4.11 The Supreme Judicial Council of Pakistan 47 4.12 Code of Conduct for Judges of the Supreme Court and 48 the High Courts 4.13 The Supreme Judicial Council Procedure of Inquiry, 50 2005 4.14 Supreme Judicial Council – Reference No. -

A Historic Journey of the Lahore City, to Attain Its Identity Through Architecture

ISSN 2411-958X (Print) European Journal of May-August 2017 ISSN 2411-4138 (Online) Interdisciplinary Studies Volume 3, Issue 3 A Historic Journey of the Lahore City, to Attain Its Identity through Architecture Najma Kabir Associate Professor, Department of Architecture, University of South Asia, Lahore, Pakistan Ghulam Abbas Prof. Department of Architecture and Planning, University of Engineering & Technology Lahore, Pakistan Khizar Hayat Director Design, Central Design Office (WATER) Water and Power Development Authority, Lahore, Pakistan Abstract Lahore is a historical and the second largest city of Pakistan. It has a unique geographical location as it is located on the main trade and invasion routes to South Asia. Its history dates back to 1000BC, when its foundations were laid by the Hindu prince Loh, son of Rama Chandra. After the invasion of Mahmud of Ghazni in 1000AD, the city of Lahore has grown, flourished, suffered invasions and destruction, and yet survived through the Sultanate (1206-1524), the Mughal (1524-1712) and Sikh (1764-1849) periods with an uneven, yet unbroken, cultural evolution. This is evident in the form of monuments and artefacts that developed and evolved over time. The research paper discusses how architecture and contemporary arts in Lahore developed with time through the examples of representative buildings as case studies. It also discusses the impacts of cultural, religious and social factors on the art and architecture during different rules and how they are embodied in the city of Lahore to contribute towards its unique identity. The Mughals, who ruled for almost three centuries, were famous as great builders. They laid the infrastructure of Lahore and built finest architectural monuments. -

Measuring the Status of Library Management Systems: a Case of Higher Education Institutions in Lahore

University of Nebraska - Lincoln DigitalCommons@University of Nebraska - Lincoln Library Philosophy and Practice (e-journal) Libraries at University of Nebraska-Lincoln March 2021 Measuring the Status of Library Management Systems: A Case of Higher Education Institutions in Lahore Muhammad Naveed Assistant Librarian, Lahore High Court Multan Bench Nadeem Siddique HoD Library, Lahore University of Management Sciences (LUMS) Hafiz Muhammad Adil Lecturer, Deptt of Library & Information Science, Govt. Degree College (B) Bedian Road, Lahore, [email protected] Follow this and additional works at: https://digitalcommons.unl.edu/libphilprac Part of the Library and Information Science Commons Naveed, Muhammad; Siddique, Nadeem; and Adil, Hafiz Muhammad, "Measuring the Status of Library Management Systems: A Case of Higher Education Institutions in Lahore" (2021). Library Philosophy and Practice (e-journal). 5134. https://digitalcommons.unl.edu/libphilprac/5134 Measuring the Status of Library Management Systems: A Case of Higher Education Institutions in Lahore By Muhammad Naveed Assistant Librarian, Lahore High Court Multan Bench [email protected] Nadeem Siddique HoD Library, Lahore University of Management Sciences (LUMS) [email protected] Hafiz Muhammad Adil Lecturer: Department of Library & Information Science, Govt. Degree College, Bedian, Lahore [email protected] Abstract Purpose: The aim of this study was to measure the status of automation, training of staff and level of implementation towards library management systems in public and private university libraries in Lahore, Pakistan. Design/methodology/approach: This study used a quantitative research approach. A Survey was carried out to collect data from the respondents. A structured research instrument was formulated after a review of the literature to collect data from the university libraries of Lahore city. -

S.M.C. 8 2018.Pdf

IN THE SUPREME COURT OF PAKISTAN (Appellate/Original Jurisdiction) PRESENT: MR. JUSTICE MIAN SAQIB NISAR, HCJ MR. JUSTICE GULZAR AHMED MR. JUSTICE SH. AZMAT SAEED MR. JUSTICE MUSHIR ALAM MR. JUSTICE UMAR ATA BANDIAL MR. JUSTICE IJAZ UL AHSAN MR. JUSTICE MAZHAR ALAM KHAN MIANKHEL SUO MOTU CASE NO.8 OF 2018 AND CIVIL MISC. APPLICATION NO.649-L OF 2018 IN SUO MOTU CASE NO.8 OF 2018 S.M.C.8/2018: Regarding dual nationality of Parliamentarians C.M.A.649-L/2018: Impleadment application by Shahzad Ali Khan In attendance: Syed Nayyar Abbas Rizvi, Addl. A.G.P. a/w Barrister Minaal Tariq Syed Ali Zafar, ASC (For Mr. Haroon Akhtar) Mr. Aleem Baig Chughtai, ASC (For Mrs. Nuzhat Sadiq) Mr. Hamid Khan, Sr. ASC Mr. Rashid Hanif, ASC (For Ch. Muhammad Sarwar) Mr. Ahmer Bilal Soofi, ASC (For Ms. Saadia Abbasi) Sardar M. Latif Khan Khosa, Sr. ASC (In C.M.A.649-L/2018) Mr. Bilal Hassan Minto, ASC (Amicus Curiae) Mr. Muhammad Arshad, D.G. (Law) (For ECP) Date of hearing: 17.10.2018 SMC No.8/2018, etc. 2 JUDGMENT SH. AZMAT SAEED, J.- During the course of hearing of Suo Motu Case No.3 of 2018, pertaining to dual nationality of Civil Servants and Officials of Autonomous Bodies, etc., it came to light that at least four newly elected Senators, namely, Ch. Muhammad Sarwar, Mr. Haroon Akhtar Khan, Ms. Nuzhat Sadiq and Ms. Saadia Abbasi, held dual nationality and apparently no conclusive evidence of their having renounced or relinquished such foreign nationality was available. -

OSAMA SIDDIQUE E-Mail: [email protected] Phone: 92-300-4022815 Weblink: Mia.Edu/Drosamasiddique

DR. OSAMA SIDDIQUE E-Mail: [email protected] Phone: 92-300-4022815 Weblink: https://independent.acade mia.edu/DrOsamaSiddique Education Harvard Law School – S.J.D (Doctor of Juridical Science) (2008 - 2011) Awards & Distinctions: Distinction – Orals Examination – 2009 Full Study Grant from the Graduate Program and the Islamic Legal Studies Program – 2008 - 2011 Study Grant for Field Work from the South Asia Institute at Harvard University – 2009 Harvard Law School – LL.M (Master of Law) (1997) Awards & Distinctions: Admitted to the S.J.D Program – 1998 (Did not take up the offer) Travel Grant for Field Work from the Islamic Legal Studies Program – 1997 - 1998 University of Oxford – B.A (Hons) Jurisprudence (1996), M.A (1998) Awards & Distinctions: Full Bursary by the Cambridge Common Wealth Trust to study at Peterhouse College, University of Cambridge. (1996) President – Oxford University Law Faculty Joint Consultative Committee (OULFJCC) – 1995 Rhodes Internship Award to intern at Center for Socio-Legal Studies, Durban, South Africa – 1993 Rhodes Scholar for Pakistan - 1992 Lahore University of Management Sciences (LUMS) – M.B.A (1993) Awards & Distinctions: Graduated in top 1/3rd of the Class Government College, Lahore – B.A (1990) Awards & Distinctions: Graduated among the top three candidates in the Punjab province Joint Editor of the College Magazine ‘The Ravi’ – 1988-1990 President of the College Debating Team - 1990 Member of the College Tennis Team – 1988 -1990 1 Silver Pen Award for winning Seven All-Pakistan Inter-Collegiate