Rpr-2009-7-1

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

International Institute for Skill Development

INTERNATIONAL INSTITUTE FOR SKILL DEVELOPMENT DEPARTMENT OF SKILL DEVELOPMENT MINISTRY OF LABOUR THAILAND Picture Reference : https://bit.ly/2Ix0qvS 1 222 Moo 2 Wieng Chiang Saen Chiang Rai 57150 Thailand INTERNATIONAL INSTITUTE FOR SKILL DEVELOPMENT DEPARTMENT OF SKILL DEVELOPMENT MINISTRY OF LABOUR THAILAND Introduction Course Title : Leadership Duration : 30 Hours / week Background and Rational International Institute for Skill Development (IISD) is situated in Chiang Rai province near the Golden Triangle. To become the institute of excellence for skill development promoting GMS and IMT-GT Country’s economic growth and also workers can compete successfully in the region and global markets that offer Planning, Organizing and Implementation of Training. The PD Training Leadership Development Training Course provides those currently in leadership positions, or those new to a leadership role, with the insight, awareness and techniques to lead more effectively. Great leaders set the pace for their team and have an impact on organizational culture and staff moral through their actions. Program Objectives Leadership skills are essential for sustainable corporate development. They are also a key factor in successful management. This course aims to: 1. Understand and apply situational leadership 2. Learn new leadership and management techniques. 3. Develop leader competencies. 4. Exchange knowledge and skills between the GMS and IM-TGT Country. Training Period The participants will receive 30 hours of the training in both theories and practices. The participants must have the training period is not less than 80 percent for eligible exam. Certificate Full Name: Skill Development Certificate in Leadership Course Middle Name: SDC in LDS The participants who pass the assessment and training course in skilled worker in upgrading training of leadership course including 30 hours will receive a certificate. -

The Chennai Comprehensive Transportation Study (CCTS)

ACKNOWLEDGEMENT The consultants are grateful to Tmt. Susan Mathew, I.A.S., Addl. Chief Secretary to Govt. & Vice-Chairperson, CMDA and Thiru Dayanand Kataria, I.A.S., Member - Secretary, CMDA for the valuable support and encouragement extended to the Study. Our thanks are also due to the former Vice-Chairman, Thiru T.R. Srinivasan, I.A.S., (Retd.) and former Member-Secretary Thiru Md. Nasimuddin, I.A.S. for having given an opportunity to undertake the Chennai Comprehensive Transportation Study. The consultants also thank Thiru.Vikram Kapur, I.A.S. for the guidance and encouragement given in taking the Study forward. We place our record of sincere gratitude to the Project Management Unit of TNUDP-III in CMDA, comprising Thiru K. Kumar, Chief Planner, Thiru M. Sivashanmugam, Senior Planner, & Tmt. R. Meena, Assistant Planner for their unstinted and valuable contribution throughout the assignment. We thank Thiru C. Palanivelu, Member-Chief Planner for the guidance and support extended. The comments and suggestions of the World Bank on the stage reports are duly acknowledged. The consultants are thankful to the Steering Committee comprising the Secretaries to Govt., and Heads of Departments concerned with urban transport, chaired by Vice- Chairperson, CMDA and the Technical Committee chaired by the Chief Planner, CMDA and represented by Department of Highways, Southern Railways, Metropolitan Transport Corporation, Chennai Municipal Corporation, Chennai Port Trust, Chennai Traffic Police, Chennai Sub-urban Police, Commissionerate of Municipal Administration, IIT-Madras and the representatives of NGOs. The consultants place on record the support and cooperation extended by the officers and staff of CMDA and various project implementing organizations and the residents of Chennai, without whom the study would not have been successful. -

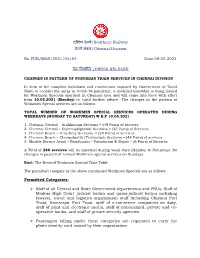

दक्षिण रेलवे/Southern Railway चेन्नै मंडल/Chennai Division No.PUB

दक्षिण रेलवे/Southern Railway चेन्नै मंडल/Chennai Division No.PUB/MAS/2021/05/04 Date:09.05.2021 प्रेस ववज्ञप्ति /PRESS RELEASE CHANGES IN PATTERN OF SUBURBAN TRAIN SERVICES IN CHENNAI DIVISION In view of the complete lockdown and restrictions imposed by Government of Tamil Nadu to contain the surge in Covid-19 pandemic, a modified timetable is being issued for Workmen Specials operated in Chennai area and will come into force with effect from 10.05.2021 (Monday) to ‘until further advice’. The changes in the pattern of Workmen Special services are as follows: TOTAL NUMBER OF WORKMEN SPECIAL SERVICES OPERATED DURING WEEKDAYS (MONDAY TO SATURDAY) W.E.F 10.05.2021 1. Chennai Central – Arakkonam Sections = (49 Pairs) of services 2. Chennai Central – Gummudipoondi Sections = (25 Pairs) of Services 3. Chennai Beach – Velachery Sections = (20 Pairs) of services 4 Chennai Beach – Chengalpattu/Tirumalpur Sections = (44 Pairs) of services 5. Shuttle Service Avadi – Pattabiram – Pattabiram E-Depot = (6 Pairs) of Services A Total of 288 services will be operated during week days (Monday to Saturday). No changes in pattern of revised Workmen special services on Sundays. Encl: The Revised Workmen Special Time Table The permitted category in the above mentioned Workmen Specials are as follows: Permitted Categories: ➢ Staff of all Central and State Government departments and PSUs, Staff of Madras High Court judicial bodies and quasi-judicial bodies including lawyers, travel and logistics organization staff including Chennai Port Trust, Kamarajar Port Trust, staff of e-commerce companies on duty, staff of print and electronic media, staff of nationalized, private and co- operative banks, and staff of private security agencies. -

Download 7.98 MB

Project Number: 52041-002 August 2021 Integrated High Impact Innovation in Sustainable Energy Technology Prefeasibility Analysis for Carbon Capture, Utilization and Storage (Subproject 2) Prepared by BCS Baliga, Ramesh Bhujade, Subhamoy Kar, Guido Magneschi, V Karthi Velan, Dewika Wattal, and Jun Zhang For ADB Energy Sector Group This the Government cannot be held liable for its contents. Project Number: 52041-002 Integrated High Impact Innovation in Sustainable Energy Technology - Prefeasibility Analysis for Carbon Capture, Utilization and Storage (Subproject 2) Prefeasibility Study on Carbon Capture and Utilization in Cement Industry of India August 2021 1 ABBREVIATIONS AND NOTES ABBREVIATIONS ADB Asian Development Bank CCS Carbon Capture and Storage CCU Carbon Capture and Utilization CCUS Carbon Capture Utilization and Storage CAPEX Capital expenditure CIF Cost, Insurance and Freight CO2 Carbon dioxide CSI Cement Sustainability Initiative CUP CO2 Utilization Plant DAC Direct air capture DBL Dalmia Bharat Limited DCBL Dalmia Cement (Bharat) Limited EA Executing Agency EOR Enhanced oil Recovery EGR Enhanced gas Recovery ECBM Enhanced coal bed methane FOB Free on Board FY Financial Year H2 Hydrogen IA Implementing Agency INDC Intended Nationally Determined Contributions IRR Internal Rate of Return MCA Multi Criteria Analysis MIRR Modified Internal Rate of Return MTPA Million Tonnes Per Annum NPV Net Present Value OPEX Operating expenditure SPV Special Purpose Vehicle 2 TA Technical Assistance tpa tonnes per annum TRL Technology readiness level VGF Viability Gap Funding WACC Weighted Average Cost of Capital WDV Written Down Value NOTES (i) The fiscal year (FY) of the Government and its agencies ends on March 31. (ii)In this report, "$" refers to US dollars, unless otherwise stated. -

An Empirical Analysis of Malaysian Housing Market: Switching and Non-Switching Models

Lincoln University Digital Thesis Copyright Statement The digital copy of this thesis is protected by the Copyright Act 1994 (New Zealand). This thesis may be consulted by you, provided you comply with the provisions of the Act and the following conditions of use: you will use the copy only for the purposes of research or private study you will recognise the author's right to be identified as the author of the thesis and due acknowledgement will be made to the author where appropriate you will obtain the author's permission before publishing any material from the thesis. An Empirical Analysis of Malaysian Housing Market: Switching and Non-Switching Models A thesis submitted in partial fulfilment of the requirements for the Degree of Doctoral of Philospohy in Finance at Lincoln University by Zaemah Zainuddin Lincoln University 2010 Abstract of a thesis submitted in partial fulfilment of the requirements for the Degree of PhD in Finance.ct AN EMPIRICAL ANALYSIS OF MALAYSIAN HOUSING MARKET: SWITCHING AND NON-SWITCHING MODELS by Zaemah Zainuddin Increasing inflows of foreign investment particularly in the real estate sector in the early 1990s, has contributed to the building up of “bubble” in the economies of several Asian countries. In 2004, house prices increased rapidly in several countries such as South Korea, Hong Kong and Singapore (World Report, 2004). The rapid increase in prices has led economists to believe that a ‘bubble’ has form in the housing market. A housing market bubble occurs when house price increases are not justified by macroeconomic fundamentals and other underlying factors (Xia and Tan 2006). -

Tamil Nadu AAR

Tax alert: ITC on inward supply used to provide free medical facilities to employees not available – Tamil Nadu AAR Issued on: 27 September 2019 Summary The Tamil Nadu Advance Ruling Authority (AAR), in a recent case, has held that the applicant providing free medical facilities to the employees, pensioners, and their dependents in in-house hospital as a part of the mandated rules is not entitled to take credit of input tax paid on the inward supply of medicines/medical equipment used therein. The AAR stated that the medicines are used by the employees and dependents and hence are for personal consumption, disentitling the applicant for availing input tax credit (ITC) on said supplies. Facts of the case Benefits only to the employees: The applicant The applicant1 is engaged in the supply of port services submitted that the hospital caters only to the and incidental supply of goods like disposal of employees, their dependents, pensioners, and their discarded assets. spouses for in-patient and out-patient treatment. No outsiders are treated in the hospital except on The applicant is required to provide health and medical recommendation of the employees, and the payment cover to its employees and pensioners under relevant for that is recovered from the salary of such employees. regulations2. The applicant is maintaining an in-house hospital within its port premises for providing these Mandatory requirement as per relevant regulations: health and medical covers exclusively to its employees The applicant is mandatorily required to provide such and pensioners. health and medical cover to the employees and pensioners under the relevant regulations2. -

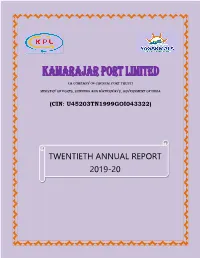

Twentieth Annual Report 2019-20

(A Company of Chennai Port Trust) Ministry of Ports, Shipping and Waterways, Government of India (CIN: U45203TN1999GOI043322) TWENTIETH ANNUAL REPORT 2019-20 KAMARAJAR PORT LIMITED Board of Directors DIN Shri Sunil Paliwal, Chairman-cum-Managing Director 01310101 Shri P. Raveendran, Nominee Director- ChPT 07640613 Shri S. Balaji Arunkumar, Nominee Director- ChPT 07526368 Shri V.M.V. Subba Rao, Independent Director 02435597 Capt. Anoop Kumar Sharma, Independent Director 03531392 Smt. Sarla Balagopal, Independent Director 01572718 Key Officials Depositories Shri Sanjay Kumar, National Securities Depository Limited General Manager (CS & BD) Central Depositories Services (India) Limited Shri M. Gunasekaran, Registered Office General Manager (Finance) cum CFO 2nd Floor (North Wing) & 3rd Floor Jawahar Building, Capt. A.K. Gupta, 17, Rajaji Salai, Chennai - 600 001. General Manager (Marine Services) Ph: 044 - 25251666-70 / Fax : 044 - 25251665 Shri V. Krishnasamy, Registrar & Share Transfer Agent General Manager (Operation) Link Intime India Private Limited Shri P. Radhakrishnan, C-101, 247 Park, L.B.S Marg Deputy General Manager (Civil) Vikhroli (West), Mumbai – 400 083. Ph : 022 – 49186000 / Fax : 022 - 49186060 Smt. Jayalakshmi Srinivasan Statutory Auditors Company Secretary M/s. B. Thiyagarajan & Co. Debenture Trustees Chartered Accountants (i) SBICAP Trustee Company Ltd Internal Auditors Mistry Bhavan, 4th Floor, M/s. Joseph & Rajaram 122, Dinshaw Vachha Road, Chartered Accountants Churchgate, Mumbai – 400 020. Ph: 022 – 43025555 Secretarial -

CADP 2.0) Infrastructure for Connectivity and Innovation

The Comprehensive Asia Development Plan 2.0 (CADP 2.0) Infrastructure for Connectivity and Innovation November 2015 Economic Research Institute for ASEAN and East Asia The findings, interpretations, and conclusions expressed herein do not necessarily reflect the views and policies of the Economic Research Institute for ASEAN and East Asia, its Governing Board, Academic Advisory Council, or the institutions and governments they represent. All rights reserved. Material in this publication may be freely quoted or reprinted with proper acknowledgement. Cover Art by Artmosphere ERIA Research Project Report 2014, No.4 National Library of Indonesia Cataloguing in Publication Data ISBN: 978-602-8660-88-4 Contents Acknowledgement iv List of Tables vi List of Figures and Graphics viii Executive Summary x Chapter 1 Development Strategies and CADP 2.0 1 Chapter 2 Infrastructure for Connectivity and Innovation: The 7 Conceptual Framework Chapter 3 The Quality of Infrastructure and Infrastructure 31 Projects Chapter 4 The Assessment of Industrialisation and Urbanisation 41 Chapter 5 Assessment of Soft and Hard Infrastructure 67 Development Chapter 6 Three Tiers of Soft and Hard Infrastructure 83 Development Chapter 7 Quantitative Assessment on Hard/Soft Infrastructure 117 Development: The Geographical Simulation Analysis for CADP 2.0 Appendix 1 List of Prospective Projects 151 Appendix 2 Non-Tariff Barriers in IDE/ERIA-GSM 183 References 185 iii Acknowledgements The original version of the Comprehensive Asia Development Plan (CADP) presents a grand spatial design of economic infrastructure and industrial placement in ASEAN and East Asia. Since the submission of such first version of the CADP to the East Asia Summit in 2010, ASEAN and East Asia have made significant achievements in developing hard infrastructure, enhancing connectivity, and participating in international production networks. -

Download in English

DDrraafftteedd 22000088 AAvian and Human Influenza Pandemic Preparedness Plan in 4 Piloted Districts of Chiang Rai Province, Thailand The Migrant Health Project in Chiang Rai Province A Collaboration between the Ministry of Public Health and the International Public Health and the International Organization for Migration, Thailand a DDrraafftteedd 22000088 AAvian and Human Influenza Pandemic Preparedness Plan in 4 Piloted Districts of Chiang Rai Province, Thailand The Migrant Health Project in Chiang Rai Province A Collaboration between the Ministry of Public Health and the International Organization for Migration, Thailand b Title : Draft of Avian and Human Influenza Pandemic Preparedness Plan in 4 Pilot Districts, Chiang Rai Province, Thailand in 2008 Advisers : Dr. Surin Sumnaphan : Dr. Nigoon Jitthai : Ms. Ratchanee Buranakitpibul Editorial Team : Dr. Nigoon Jitthai Dr. Sushera Bunluesin Mr. Vittaya Sumitmoh Ms. Lissa Giurissevich Publisher : International Organization for Migration (IOM) Graphic Design : Mr. Manit Kaewkunta Published Date : 1st Edition , May 2009 Copies : 300 Printer : Baan Copy Center, 132/13, Moo 4, Ban Doo Sub-district, Muang District, Chiang Rai Province, 57100 Tel: 053-776-432 c PPrreeffaaccee Poultry influenza or Human influenza type H5N1 has spread in many parts of the world since 2003. A large number of poultry has been infected with H5N1 in Thailand, in addition to disease, ill health and mortality experienced in human cases infected with H5N1. These cases are the cause for significant concerns about the H5N1 strain and its potential impact on the social and economical environment. Therefore, the Migrant Health Project in Chiang Rai Province, a collaboration between the Ministry of Public Health and the International Organization for Migration Thailand, have taken steps to raise awareness about Avian and Human Influenza pandemic preparedness. -

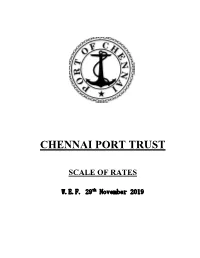

Scale of Rates

CHENNAI PORT TRUST SCALE OF RATES W.E.F. 29th November 2019 DETAILS OF TAMP ORDERS Sl. TAMP Order Details Gazette Valid upto No No. / Date Notification No. / Date A TAMP Orders on the proposals of ChPT 01 TAMP/56/2014- Revision of Estate G.No.13 / 23.01.2020 CHPT Rentals 09.01.2015 /20.12.2014 02 TAMP/12/2019- Mandatory user charges G.No.297 / Rs.155/- MUC/ for tracking of 21.08.2019 from 6.9.19 24.07.2019 containers towards to 5.9.2020 Logistics Data Bank and Rs.165/- Service to be from rendered by DMICDC 6.9.2020 to 5.9.2021 03 TAMP/30/2019- General Revision of G.No.376 / 28.11.2022 CHPT / Scale of Rates 30.10.2019 10.10.2019 (excluding estate rental) B TAMP Orders based on Government directions 01 TAMP/04/2004- Regulation of Port dues G.No.467 / CHPT / and other charges from 27.12.2016 -- 16.12.2016 the vessels of Bangladesh as per Standard Operating Procedure / Coastal Shipping Agreement DETAILS OF CONCESSION SCHEMES AS PER GOVEREMENTDIRECTION/CHPT BOARD APPROVAL Sl. Details of Board Extent of Concession Period of No Schemes Resolution validity (BR) / Trade Notice No. / Date A Schemes applicable for all Port users 01 Concession on BR.27 / 15% concession for all 31.03.2020 Vessel Related 24.5.2019 Costal Container Charges (VRC) Trade notice / vessels for Container 31.05.19 vessels 02 Concession on BR.27 / Addition Upfront 31.03.2020 VRC to EXIM 24.5.2019 concession in VRC to containers Trade notice / EXIM container 31.05.19 vessels ranging from 20% to 50% additional loyalty discounts at the end of the year 03 Waiver of Port BR.45 / 80% Waiver of Port 04.05.2020 Railway Charges 26.5.2019 Railway charges (Haulage and Port Trade notice / (Haulage and Terminal 04.09.19 Terminal Handling Handling Charges) for Charges) containers handled by M/s.CONCOR through rail wagons from Chennai Port to ICD / Tondiarpet to facilitate Direct Port Delivery/ Direct Port Entry. -

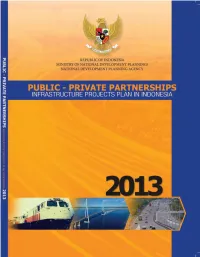

PPP Book 2013.Pdf

REPUBLIC OF INDONESIA MINISTRY OF NATIONAL DEVELOPMENT PLANNING/ NATIONAL DEVELOPMENT PLANNING AGENCY PUBLIC PRIVATE PARTNERSHIPS INFRASTRUCTURE PROJECTS PLAN IN INDONESIA 2013 Jakarta, November 2013 ii PUBLIC PRIVATE PARTNERSHIPS INFRASTRUCTURE PROJECTS PLAN IN INDONESIA FOREWORD BY THE MINISTER OF NATIONAL DEVELOPMENT PLANNING AND HEAD OF NATIONAL DEVELOPMENT PLANNING AGENCY (BAPPENAS) he Government of Indonesia is consistently sustaining the momentum of Public Private Partnership (PPP) development in order to accelerate the provision of infrastructure. The TPPP model has gained increasing in presence since the pronouncement of the Master plan for the Acceleration and Expansion of Indonesia’s Economic Development (MP3EI) in 2011. The MP3EI reiterates the Government of Indonesia’s determination to use the PPPs as one of the keys to financing the country’s economic development. The Government holds a proactive approach and continues to evaluate and strengthen policy in order to support the provision of infrastructure using PPPs. Firstly, through the establishment of the regulatory framework for PPPs, comprising Presidential Regulation 67/2005 on Cooperation between Government and Business Entities in Infrastructure Provision and its subsequent amendments PR 13/2010, PR 56/2011 and PR 66/2013. Secondly, by providing supporting regulations to address major issues affecting the implementation of PPP projects, v.g.Law 2/2012 on land acquisition for public infrastructure projects and Regulation 223/PMK.011/2012 of the Ministry of Finance on the Viability Gap Fund. Bappenas has also updated Ministerial Regulation on PPP Operational Guidelines 4/2010 with Ministerial Regulation 3/2012 to reflect the evolution of the legal framework and to improve the PPP preparation process. -

The Politics of Environmental and Water Pollution in East Java 321

A WORLD OF WATER V ER H A N DEL ING E N VAN HET KONINKLIJK INSTITUUT VOOR TAAL-, LAND- EN VOLKENKUNDE 240 A WORLD OF WATER Rain, rivers and seas in Southeast Asian histories Edited by PETER BOOMGAARD KITLV Press Leiden 2007 Published by: KITLV Press Koninklijk Instituut voor Taal-, Land- en Volkenkunde (Royal Netherlands Institute of Southeast Asian and Caribbean Studies) PO Box 9515 2300 RA Leiden The Netherlands website: www.kitlv.nl e-mail: [email protected] KITLV is an institute of the Royal Netherlands Academy of Arts and Sciences (KNAW) Cover: Creja ontwerpen, Leiderdorp ISBN 90 6718 294 X © 2007 Koninklijk Instituut voor Taal-, Land- en Volkenkunde No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording, or any information storage and retrieval system, without permission from the copyright owner. Printed in the Netherlands Table of contents Preface vii Peter Boomgaard In a state of flux Water as a deadly and a life-giving force in Southeast Asia 1 Part One Waterscapes Heather Sutherland Geography as destiny? The role of water in Southeast Asian history 27 Sandra Pannell Of gods and monsters Indigenous sea cosmologies, promiscuous geographies and the depths of local sovereignty 71 Manon Osseweijer A toothy tale A short history of shark fisheries and trade in shark products in twentieth-century Indonesia 103 Part Two Hazards of sea and water James F. Warren A tale of two centuries The globalization of maritime raiding and piracy in Southeast Asia at the end of the eighteenth and twentieth centuries 125 vi Contents Greg Bankoff Storms of history Water, hazard and society in the Philippines, 1565-1930 153 Part Three Water for agriculture Robert C.