Download 7.98 MB

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Pre - Feasibility Report

BHAVYA CEMENTS LIMITED TANGEDA VILLAGE, DACHEPALLY MANDAL, GUNTUR DISTRICT, ANDHRA PRADESH Pre - Feasibility Report Submitted by: Bhavya Cements Ltd., IInd Bhavyas Spoorthi Bhavan, Plot No. A1, Film Nagar, Jubilee Hills, Hyderabad – 500 003. Phone: 040-23558384 Fax: 040-23558393. Email: - [email protected] Submitted to MINISTRY OF ENVIRONMENT, FOREST AND CLIMATE CHANGE GOVERNMENT OF INDIA INDIRA PARYAVARAN BHAWAN, JOR BAGH ROAD, ALIGANJ, NEW DELHI Pre-Feasibility Report Bhavya Cements Limited, Pre – Feasibility Report Bhavya Cements Limited, Tangeda Village, Dachepalli Mandal, Guntur District, Andhra Pradesh. 1 Executive Summary M/s. Bhavya Cements Ltd obtained Environmental Clearance for integrated Cement Plant of 4.0 Million TPA (Phase I : 4200 TPD and Phase II: 7700 TPD) Capacity, 15 MW captive power plant and Captive mining of Limestone at Thangeda Village, Dachepalle Mandal, Guntur Dist, Andhra Pradesh from Ministry of Environment, Forest and Climate Change (MoEFCC) vide letter no. F. No. J- 11011/1186/2007-IA II (I), dt. 22.09.2008, and secured extension of EC validity by letter dt.03.03.2016. The existing project for 3000 TPD of Clinker production and 4200 TPD of cement production is in operation. The consent to operate was obtained from AP Pollution Control Board vide letter no. APPCB/VJA/GTR/205/HO/CFO/2018, dt. 06.06.2018 valid till 31.08.2023. It is now proposed to modernize the Phase I project to enhance clinker manufacturing capacity by 1200 TPD to achieve 4200 TPD, and cement manufacturing capacity by 1680 TPD to achieve a total capacity of 5880 TPD. The modernization mainly entails increasing operational hours of limestone crusher, raw mill coal mill, and enhancing capacity of Cooler ESP transformer field and modernization of kiln. -

District Legal Services Authority, Ariyalur (District Court, Ariyalur) Dated: 11.01.2018

DISTRICT LEGAL SERVICES AUTHORITY, ARIYALUR (DISTRICT COURT, ARIYALUR) DATED: 11.01.2018 LIST OF THE CANDIDATES SHORT LISTED FOR THE POST OF JUNIOR ADMINISTRATIVE ASSISTANT (BC-CATEGORY) TO ATTEND THE INTERVIEW AT DISTRICT LEGAL SERVICES AUTHORITY, ARIYALUR (DISTRICT COURT, ARIYALUR) Sl. Application Name and Address Date & Time No. No. D. Antoni George S/o Durai Raj 1 Employment 3/ 209 North Street 30.01.2018 (ARD2014M00008452) Sembiyakudi Village 9.00 A.M. Kulamanickam Post Ariyalur TK & Dist 621 722 2 S. Selvaraju S/o Subbrayan 30.01.2018 Employment Poyyur (ARD1993M00019772) Karuppursenapathi Post 9.00 A.M. Ariyalur Dist 621 707 3 M. Paramasivam S/o Muthusamy Udayar 30.01.2018 Employment Middle Street (ARD1989M00013257) Rayampuram Post 9.00 A.M. Ariyalur TK & Dist 621 718 4 S. Pattu W/o Ravichandra bose 30.01.2018 Employment 72/8 Periyar Nagar (ARD2004F00000537) First Street 9.00 A.M. Ariyalur Dist 621 704 5 S. Karunanithi S/o Santhalingam 23/2nd Street 30.01.2018 Employment Sengunathapuram Post (ARD1994M00051423) 9.00 A.M. Udayarpalayam TK Ariyalur Dist 621 802 6 N.Govardhan, S/o.P.Nagaraj, 20, 3 B4/1, 30.01.2018 JAA-02 Thendral Nagar East Street, 9.00 A.M. Bodi Nayakkanur – PO Theni District 7 P.Raj, S/o. Pavunraj 30.01.2018 JAA-03 No.25, south street Elakkurichi– PO 9.00 A.M. Ariyalur. 8 A.Latha D/o. Annavi No.1/50 Maniya Nagar Ettarai – PO 30.01.2018 JAA-06 Kulumani – via, 9.00 A.M. Trichy 639 103. 9 M.Senthilmurugan S/o. -

The Chennai Comprehensive Transportation Study (CCTS)

ACKNOWLEDGEMENT The consultants are grateful to Tmt. Susan Mathew, I.A.S., Addl. Chief Secretary to Govt. & Vice-Chairperson, CMDA and Thiru Dayanand Kataria, I.A.S., Member - Secretary, CMDA for the valuable support and encouragement extended to the Study. Our thanks are also due to the former Vice-Chairman, Thiru T.R. Srinivasan, I.A.S., (Retd.) and former Member-Secretary Thiru Md. Nasimuddin, I.A.S. for having given an opportunity to undertake the Chennai Comprehensive Transportation Study. The consultants also thank Thiru.Vikram Kapur, I.A.S. for the guidance and encouragement given in taking the Study forward. We place our record of sincere gratitude to the Project Management Unit of TNUDP-III in CMDA, comprising Thiru K. Kumar, Chief Planner, Thiru M. Sivashanmugam, Senior Planner, & Tmt. R. Meena, Assistant Planner for their unstinted and valuable contribution throughout the assignment. We thank Thiru C. Palanivelu, Member-Chief Planner for the guidance and support extended. The comments and suggestions of the World Bank on the stage reports are duly acknowledged. The consultants are thankful to the Steering Committee comprising the Secretaries to Govt., and Heads of Departments concerned with urban transport, chaired by Vice- Chairperson, CMDA and the Technical Committee chaired by the Chief Planner, CMDA and represented by Department of Highways, Southern Railways, Metropolitan Transport Corporation, Chennai Municipal Corporation, Chennai Port Trust, Chennai Traffic Police, Chennai Sub-urban Police, Commissionerate of Municipal Administration, IIT-Madras and the representatives of NGOs. The consultants place on record the support and cooperation extended by the officers and staff of CMDA and various project implementing organizations and the residents of Chennai, without whom the study would not have been successful. -

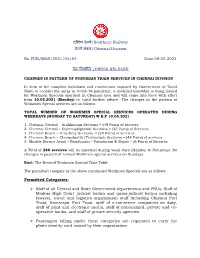

दक्षिण रेलवे/Southern Railway चेन्नै मंडल/Chennai Division No.PUB

दक्षिण रेलवे/Southern Railway चेन्नै मंडल/Chennai Division No.PUB/MAS/2021/05/04 Date:09.05.2021 प्रेस ववज्ञप्ति /PRESS RELEASE CHANGES IN PATTERN OF SUBURBAN TRAIN SERVICES IN CHENNAI DIVISION In view of the complete lockdown and restrictions imposed by Government of Tamil Nadu to contain the surge in Covid-19 pandemic, a modified timetable is being issued for Workmen Specials operated in Chennai area and will come into force with effect from 10.05.2021 (Monday) to ‘until further advice’. The changes in the pattern of Workmen Special services are as follows: TOTAL NUMBER OF WORKMEN SPECIAL SERVICES OPERATED DURING WEEKDAYS (MONDAY TO SATURDAY) W.E.F 10.05.2021 1. Chennai Central – Arakkonam Sections = (49 Pairs) of services 2. Chennai Central – Gummudipoondi Sections = (25 Pairs) of Services 3. Chennai Beach – Velachery Sections = (20 Pairs) of services 4 Chennai Beach – Chengalpattu/Tirumalpur Sections = (44 Pairs) of services 5. Shuttle Service Avadi – Pattabiram – Pattabiram E-Depot = (6 Pairs) of Services A Total of 288 services will be operated during week days (Monday to Saturday). No changes in pattern of revised Workmen special services on Sundays. Encl: The Revised Workmen Special Time Table The permitted category in the above mentioned Workmen Specials are as follows: Permitted Categories: ➢ Staff of all Central and State Government departments and PSUs, Staff of Madras High Court judicial bodies and quasi-judicial bodies including lawyers, travel and logistics organization staff including Chennai Port Trust, Kamarajar Port Trust, staff of e-commerce companies on duty, staff of print and electronic media, staff of nationalized, private and co- operative banks, and staff of private security agencies. -

Facility DEC ID: 4192600001 PERMIT Under the Environmental

Facility DEC ID: 4192600001 PERMIT Under the Environmental Conservation Law (ECL) IDENTIFICATION INFORMATION Permit Type: Air Title V Facility Permit ID: 4-1926-00001/00110 Mod 0 Effective Date: 10/18/2001 Expiration Date: 10/18/2006 Mod 1 Effective Date: 10/03/2003 Expiration Date: 10/18/2006 Permit Issued To: GLENS FALLS LEHIGH CEMENT CO INC 313 WARREN ST PO BOX 440 GLENS FALLS, NY 12801-0440 Contact: RICHARD MOSS GLENS FALLS LEHIGH CEMENT CO INC 313 WARREN STREET PO BOX 440 GLENS FALLS, NY 12801-0440 Facility: GLENS FALLS LEHIGH CEMENT COMPANY 120 ALPHA ROAD, OFF ROUTE 9W CEMENTON, NY 12415 Description: By acceptance of this permit, the permittee agrees that the permit is contingent upon strict compliance with the ECL, all applicable regulations, the General Conditions specified and any Special Conditions included as part of this permit. Permit Administrator: STEVE G SCHASSLER 1150 NORTH WESTCOTT RD SCHENECTADY, NY 12306-2014 Authorized Signature: _________________________________ Date: ___ / ___ / _____ Mod 1/FINAL Facility DEC ID: 4192600001 Notification of Other State Permittee Obligations Item A: Permittee Accepts Legal Responsibility and Agrees to Indemnification The permittee expressly agrees to indemnify and hold harmless the Department of Environmental Conservation of the State of New York, its representatives, employees, and agents ("DEC") for all claims, suits, actions, and damages, to the extent attributable to the permittee's acts or omissions in connection with the permittee's undertaking of activities in connection with, or operation and maintenance of, the facility or facilities authorized by the permit whether in compliance or not in compliance with the terms and conditions of the permit. -

Rpr-2009-7-1

ACKNOWLEDGEMENT The Comprehensive Asia Development Plan (CADP) is the crystallization of various academic efforts, especially the strong leadership, rigorous analysis, deep insight and relentless efforts of Dr. Fukunari Kimura and Mr. So Umezaki, with support from many other scholars including, Dr. Mitsuyo Ando, Dr. Haryo Aswicahyono, Dr. Ruth Banomyong, Dr. Truong Chi Binh, Dr. Nguyen Binh Giang, Dr. Toshitaka Gokan, Dr. Kazunobu Hayakawa, Dr. Socheth Hem, Dr. Patarapong Intarakumnerd, Dr. Masami Ishida, Mr. Toru Ishihara and his team, Dr. Ikumo Isono, Dr. Souknilan Keola, Dr. Somrote Komolavanij, Dr. Toshihiro Kudo, Dr. Satoru Kumagai, Dr. Moe Kyaw, Dr. Mari-Len Macasaquit, Dr. Tomohiro Machikita, Mr. Mitsuhiro Maeda, Dr. Sunil Mani, Dr. Toru Mihara, Dr. Avvari V. Mohan, Dr. Siwage Dharma Negara, Dr. Leuam Nhongvongsithi, Dr. Ayako Obashi, Dr. Apichat Sopadang, Dr. Chang Yii Tan, Dr. Masatsugu Tsuji, Dr. Yasushi Ueki and Dr. Korrakot Yaibuathet. ERIA also owes grateful thanks to research groups in Nippon Koei and the National University of Singapore. ERIA is also grateful for valuable guidance and instructions provided by the ASEAN Secretariat and inter-alia His Excellency Dr. Surin Pitsuwan, Secretary-General of ASEAN, in making the CADP properly responsive to the needs of policy makers and in providing great support for our activities. Additionally ERIA would like to express its deepest gratitude to the Asian Development Bank (ADB), the United Nations Economic and Social Commission for Asia and the Pacific (UNESCAP), and various donor agencies including the Japan International Cooperation Agency (JICA) for providing valuable information related to infrastructure projects, and other inputs. Especially we thank ADB for making time to conduct informal discussions with our team, and for the insights provided which were really useful for our analysis. -

Boral Berrima Cement Works

DETERMINATION OF A DEVELOPMENT APPLICATION FOR STATE SIGNIFICANT AND INTEGRATED DEVELOPMENT UNDER SECTION 80 OF THE ENVIRONMENTAL PLANNING AND ASSESSMENT ACT, 1979 I, the Minister for Infrastructure and Planning, under Section 80 of the Environmental Planning and Assessment Act 1979 ("the Act"), determine the development application ("the Application") referred to in Schedule 1 by granting consent subject to the conditions set out in Schedule 2. The reason for the imposition of conditions is to: a) minimise any adverse environmental impacts associated with the development; b) provide for the on-going environmental management of the development; and c) provide for regular monitoring and reporting on the development. Text in red is amendments made by MOD 2-1-2004-i (Non-Standard Fuels) modified 26 September 2005. Text in blue is amendments made by MOD 109-9-2006-i (remove prohibition of hazardous wastes) modified 22 September 2006. Text in green is amendments made by MOD 12-2-2007-I (trial use of tyre chips) modified 13 February 2007. Text in purple is amendments made by MOD 4 (variation to usage rate of coke fines) modified 24 April 2008. Text in orange is amendments made by MOD 5 (coal deliveries by rail) modified 31 August 2009. Text in navy is amendment made by MOD 6 (coal stockpiling for sale) modified 20 June 2012. Text in pink is amendments made by MOD 7 (GBFS processing) modified 16 April 2012. Text in light green is amendments made by Mod 8 (Approval / EPL Consistency) modified 5 August 2012. Text in light blue is amendments made by MOD 9 (Use of Waste Derived Fuels) modified 5 October 2016. -

Urban Development in Ariyalur District, Using Remote Sensing and Geographical Information System (Gis)

R.Vasanthi et al Int. Journal of Engineering Research and Applications www.ijera.com ISSN : 2248-9622, Vol. 4, Issue 1( Version 3), January 2014, pp.280-291 RESEARCH ARTICLE OPEN ACCESS Urban Development in Ariyalur District, Using Remote Sensing and Geographical Information System (Gis) 1 R.Vasanthi , 1R. Baskaran, and 2 G.Vanaraju. 1 Department of Industries and Earth sciences, Tamil University, Thanjavur – 613010, TamilNadu, India 2 Department of Geology, School of Geosciences, Bharathidasan University, Tiruchirappalli – 620024, Tamil Nadu, India Abstract The study is mainly based on visual interpretation of satellite imageries by studying the standard recognition elements such as color, tone, texture, Pattern etc., for the delineation of urban land use of the study area. After the visual interpretation of Satellite imageries direct field checks have been made. The primary data were acquired from the LANDSAT satellite imagery. The supplementary data were generated from the survey of India SOI topographical maps. A base map was prepared using survey of India toposheets having the index of numbers, 58M/4, 7, 8, 11, 12 and 58N/1 on a scale of 1:50,000 as an understanding of this study. Totally 6 toposheets have covered the study area. The geographical features like major road, railway, and drainage system, and elevation information, nature of River, tank, settlements and relevant information were incorporated in the base map. Arc GIS used to integrate the available data sources. LANDSAT MSS (1976), IRS P6-LISS III (2010) satellite data the urban land use classification were attempted. The classification followed here is based on unsupervised classification and interpretation; the data interpreted from the imagery were cross- checked in the field. -

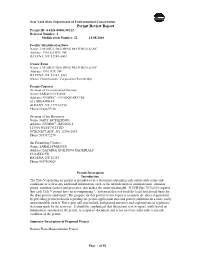

Permit Review Report Permit ID: 4-0124-00001/00112 Renewal Number: 1 Modification Number: 12 12/08/2014

New York State Department of Environmental Conservation Permit Review Report Permit ID: 4-0124-00001/00112 Renewal Number: 1 Modification Number: 12 12/08/2014 Facility Identification Data Name: LAFARGE BUILDING MATERIALS INC Address: 1916 US RTE 9W RAVENA, NY 12143-0003 Owner/Firm Name: LAFARGE BUILDING MATERIALS INC Address: 1916 RTE 9W RAVENA, NY 12143, USA Owner Classification: Corporation/Partnership Permit Contacts Division of Environmental Permits: Name: SARAH H EVANS Address: NYSDEC - HEADQUARTERS 625 BROADWAY ALBANY, NY 12233-1750 Phone:5184029156 Division of Air Resources: Name: GARY MCPHERSON Address: NYSDEC - REGION 4 1130 N WESTCOTT RD SCHENECTADY, NY 12306-2014 Phone:5183572278 Air Permitting Contact: Name: SARAH SWEENEY Address: LAFARGE BUILDING MATERIALS 1916 RTE 9W RAVENA, NY 12143 Phone:5187565028 Permit Description Introduction The Title V operating air permit is intended to be a document containing only enforceable terms and conditions as well as any additional information, such as the identification of emission units, emission points, emission sources and processes, that makes the terms meaningful. 40 CFR Part 70.7(a)(5) requires that each Title V permit have an accompanying "...statement that sets forth the legal and factual basis for the draft permit conditions". The purpose for this permit review report is to satisfy the above requirement by providing pertinent details regarding the permit/application data and permit conditions in a more easily understandable format. This report will also include background narrative and explanations of regulatory decisions made by the reviewer. It should be emphasized that this permit review report, while based on information contained in the permit, is a separate document and is not itself an enforceable term and condition of the permit. -

Tamil Nadu AAR

Tax alert: ITC on inward supply used to provide free medical facilities to employees not available – Tamil Nadu AAR Issued on: 27 September 2019 Summary The Tamil Nadu Advance Ruling Authority (AAR), in a recent case, has held that the applicant providing free medical facilities to the employees, pensioners, and their dependents in in-house hospital as a part of the mandated rules is not entitled to take credit of input tax paid on the inward supply of medicines/medical equipment used therein. The AAR stated that the medicines are used by the employees and dependents and hence are for personal consumption, disentitling the applicant for availing input tax credit (ITC) on said supplies. Facts of the case Benefits only to the employees: The applicant The applicant1 is engaged in the supply of port services submitted that the hospital caters only to the and incidental supply of goods like disposal of employees, their dependents, pensioners, and their discarded assets. spouses for in-patient and out-patient treatment. No outsiders are treated in the hospital except on The applicant is required to provide health and medical recommendation of the employees, and the payment cover to its employees and pensioners under relevant for that is recovered from the salary of such employees. regulations2. The applicant is maintaining an in-house hospital within its port premises for providing these Mandatory requirement as per relevant regulations: health and medical covers exclusively to its employees The applicant is mandatorily required to provide such and pensioners. health and medical cover to the employees and pensioners under the relevant regulations2. -

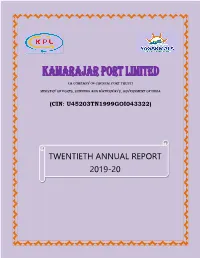

Twentieth Annual Report 2019-20

(A Company of Chennai Port Trust) Ministry of Ports, Shipping and Waterways, Government of India (CIN: U45203TN1999GOI043322) TWENTIETH ANNUAL REPORT 2019-20 KAMARAJAR PORT LIMITED Board of Directors DIN Shri Sunil Paliwal, Chairman-cum-Managing Director 01310101 Shri P. Raveendran, Nominee Director- ChPT 07640613 Shri S. Balaji Arunkumar, Nominee Director- ChPT 07526368 Shri V.M.V. Subba Rao, Independent Director 02435597 Capt. Anoop Kumar Sharma, Independent Director 03531392 Smt. Sarla Balagopal, Independent Director 01572718 Key Officials Depositories Shri Sanjay Kumar, National Securities Depository Limited General Manager (CS & BD) Central Depositories Services (India) Limited Shri M. Gunasekaran, Registered Office General Manager (Finance) cum CFO 2nd Floor (North Wing) & 3rd Floor Jawahar Building, Capt. A.K. Gupta, 17, Rajaji Salai, Chennai - 600 001. General Manager (Marine Services) Ph: 044 - 25251666-70 / Fax : 044 - 25251665 Shri V. Krishnasamy, Registrar & Share Transfer Agent General Manager (Operation) Link Intime India Private Limited Shri P. Radhakrishnan, C-101, 247 Park, L.B.S Marg Deputy General Manager (Civil) Vikhroli (West), Mumbai – 400 083. Ph : 022 – 49186000 / Fax : 022 - 49186060 Smt. Jayalakshmi Srinivasan Statutory Auditors Company Secretary M/s. B. Thiyagarajan & Co. Debenture Trustees Chartered Accountants (i) SBICAP Trustee Company Ltd Internal Auditors Mistry Bhavan, 4th Floor, M/s. Joseph & Rajaram 122, Dinshaw Vachha Road, Chartered Accountants Churchgate, Mumbai – 400 020. Ph: 022 – 43025555 Secretarial -

CADP 2.0) Infrastructure for Connectivity and Innovation

The Comprehensive Asia Development Plan 2.0 (CADP 2.0) Infrastructure for Connectivity and Innovation November 2015 Economic Research Institute for ASEAN and East Asia The findings, interpretations, and conclusions expressed herein do not necessarily reflect the views and policies of the Economic Research Institute for ASEAN and East Asia, its Governing Board, Academic Advisory Council, or the institutions and governments they represent. All rights reserved. Material in this publication may be freely quoted or reprinted with proper acknowledgement. Cover Art by Artmosphere ERIA Research Project Report 2014, No.4 National Library of Indonesia Cataloguing in Publication Data ISBN: 978-602-8660-88-4 Contents Acknowledgement iv List of Tables vi List of Figures and Graphics viii Executive Summary x Chapter 1 Development Strategies and CADP 2.0 1 Chapter 2 Infrastructure for Connectivity and Innovation: The 7 Conceptual Framework Chapter 3 The Quality of Infrastructure and Infrastructure 31 Projects Chapter 4 The Assessment of Industrialisation and Urbanisation 41 Chapter 5 Assessment of Soft and Hard Infrastructure 67 Development Chapter 6 Three Tiers of Soft and Hard Infrastructure 83 Development Chapter 7 Quantitative Assessment on Hard/Soft Infrastructure 117 Development: The Geographical Simulation Analysis for CADP 2.0 Appendix 1 List of Prospective Projects 151 Appendix 2 Non-Tariff Barriers in IDE/ERIA-GSM 183 References 185 iii Acknowledgements The original version of the Comprehensive Asia Development Plan (CADP) presents a grand spatial design of economic infrastructure and industrial placement in ASEAN and East Asia. Since the submission of such first version of the CADP to the East Asia Summit in 2010, ASEAN and East Asia have made significant achievements in developing hard infrastructure, enhancing connectivity, and participating in international production networks.