Business Plan for Chennai Port Trust Final Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

T.Y.B.A. Paper Iv Geography of Settlement © University of Mumbai

31 T.Y.B.A. PAPER IV GEOGRAPHY OF SETTLEMENT © UNIVERSITY OF MUMBAI Dr. Sanjay Deshmukh Vice Chancellor, University of Mumbai Dr.AmbujaSalgaonkar Dr.DhaneswarHarichandan Incharge Director, Incharge Study Material Section, IDOL, University of Mumbai IDOL, University of Mumbai Programme Co-ordinator : Anil R. Bankar Asst. Prof. CumAsst. Director, IDOL, University of Mumbai. Course Co-ordinator : Ajit G.Patil IDOL, Universityof Mumbai. Editor : Dr. Maushmi Datta Associated Prof, Dept. of Geography, N.K. College, Malad, Mumbai Course Writer : Dr. Hemant M. Pednekar Principal, Arts, Science & Commerce College, Onde, Vikramgad : Dr. R.B. Patil H.O.D. of Geography PondaghatArts & Commerce College. Kankavli : Dr. ShivramA. Thakur H.O.D. of Geography, S.P.K. Mahavidyalaya, Sawantiwadi : Dr. Sumedha Duri Asst. Prof. Dept. of Geography Dr. J.B. Naik, Arts & Commerce College & RPD Junior College, Sawantwadi May, 2017 T.Y.B.A. PAPER - IV,GEOGRAPHYOFSETTLEMENT Published by : Incharge Director Institute of Distance and Open Learning , University of Mumbai, Vidyanagari, Mumbai - 400 098. DTP Composed : Ashwini Arts Gurukripa Chawl, M.C. Chagla Marg, Bamanwada, Vile Parle (E), Mumbai - 400 099. Printed by : CONTENTS Unit No. Title Page No. 1 Geography of Rural Settlement 1 2. Factors of Affecting Rural Settlements 20 3. Hierarchy of Rural Settlements 41 4. Changing pattern of Rural Land use 57 5. Integrated Rural Development Programme and Self DevelopmentProgramme 73 6. Geography of Urban Settlement 83 7. Factors Affecting Urbanisation 103 8. Types of -

The Chennai Comprehensive Transportation Study (CCTS)

ACKNOWLEDGEMENT The consultants are grateful to Tmt. Susan Mathew, I.A.S., Addl. Chief Secretary to Govt. & Vice-Chairperson, CMDA and Thiru Dayanand Kataria, I.A.S., Member - Secretary, CMDA for the valuable support and encouragement extended to the Study. Our thanks are also due to the former Vice-Chairman, Thiru T.R. Srinivasan, I.A.S., (Retd.) and former Member-Secretary Thiru Md. Nasimuddin, I.A.S. for having given an opportunity to undertake the Chennai Comprehensive Transportation Study. The consultants also thank Thiru.Vikram Kapur, I.A.S. for the guidance and encouragement given in taking the Study forward. We place our record of sincere gratitude to the Project Management Unit of TNUDP-III in CMDA, comprising Thiru K. Kumar, Chief Planner, Thiru M. Sivashanmugam, Senior Planner, & Tmt. R. Meena, Assistant Planner for their unstinted and valuable contribution throughout the assignment. We thank Thiru C. Palanivelu, Member-Chief Planner for the guidance and support extended. The comments and suggestions of the World Bank on the stage reports are duly acknowledged. The consultants are thankful to the Steering Committee comprising the Secretaries to Govt., and Heads of Departments concerned with urban transport, chaired by Vice- Chairperson, CMDA and the Technical Committee chaired by the Chief Planner, CMDA and represented by Department of Highways, Southern Railways, Metropolitan Transport Corporation, Chennai Municipal Corporation, Chennai Port Trust, Chennai Traffic Police, Chennai Sub-urban Police, Commissionerate of Municipal Administration, IIT-Madras and the representatives of NGOs. The consultants place on record the support and cooperation extended by the officers and staff of CMDA and various project implementing organizations and the residents of Chennai, without whom the study would not have been successful. -

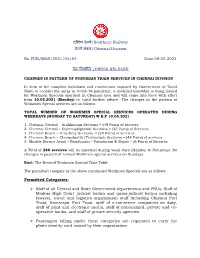

दक्षिण रेलवे/Southern Railway चेन्नै मंडल/Chennai Division No.PUB

दक्षिण रेलवे/Southern Railway चेन्नै मंडल/Chennai Division No.PUB/MAS/2021/05/04 Date:09.05.2021 प्रेस ववज्ञप्ति /PRESS RELEASE CHANGES IN PATTERN OF SUBURBAN TRAIN SERVICES IN CHENNAI DIVISION In view of the complete lockdown and restrictions imposed by Government of Tamil Nadu to contain the surge in Covid-19 pandemic, a modified timetable is being issued for Workmen Specials operated in Chennai area and will come into force with effect from 10.05.2021 (Monday) to ‘until further advice’. The changes in the pattern of Workmen Special services are as follows: TOTAL NUMBER OF WORKMEN SPECIAL SERVICES OPERATED DURING WEEKDAYS (MONDAY TO SATURDAY) W.E.F 10.05.2021 1. Chennai Central – Arakkonam Sections = (49 Pairs) of services 2. Chennai Central – Gummudipoondi Sections = (25 Pairs) of Services 3. Chennai Beach – Velachery Sections = (20 Pairs) of services 4 Chennai Beach – Chengalpattu/Tirumalpur Sections = (44 Pairs) of services 5. Shuttle Service Avadi – Pattabiram – Pattabiram E-Depot = (6 Pairs) of Services A Total of 288 services will be operated during week days (Monday to Saturday). No changes in pattern of revised Workmen special services on Sundays. Encl: The Revised Workmen Special Time Table The permitted category in the above mentioned Workmen Specials are as follows: Permitted Categories: ➢ Staff of all Central and State Government departments and PSUs, Staff of Madras High Court judicial bodies and quasi-judicial bodies including lawyers, travel and logistics organization staff including Chennai Port Trust, Kamarajar Port Trust, staff of e-commerce companies on duty, staff of print and electronic media, staff of nationalized, private and co- operative banks, and staff of private security agencies. -

Download 7.98 MB

Project Number: 52041-002 August 2021 Integrated High Impact Innovation in Sustainable Energy Technology Prefeasibility Analysis for Carbon Capture, Utilization and Storage (Subproject 2) Prepared by BCS Baliga, Ramesh Bhujade, Subhamoy Kar, Guido Magneschi, V Karthi Velan, Dewika Wattal, and Jun Zhang For ADB Energy Sector Group This the Government cannot be held liable for its contents. Project Number: 52041-002 Integrated High Impact Innovation in Sustainable Energy Technology - Prefeasibility Analysis for Carbon Capture, Utilization and Storage (Subproject 2) Prefeasibility Study on Carbon Capture and Utilization in Cement Industry of India August 2021 1 ABBREVIATIONS AND NOTES ABBREVIATIONS ADB Asian Development Bank CCS Carbon Capture and Storage CCU Carbon Capture and Utilization CCUS Carbon Capture Utilization and Storage CAPEX Capital expenditure CIF Cost, Insurance and Freight CO2 Carbon dioxide CSI Cement Sustainability Initiative CUP CO2 Utilization Plant DAC Direct air capture DBL Dalmia Bharat Limited DCBL Dalmia Cement (Bharat) Limited EA Executing Agency EOR Enhanced oil Recovery EGR Enhanced gas Recovery ECBM Enhanced coal bed methane FOB Free on Board FY Financial Year H2 Hydrogen IA Implementing Agency INDC Intended Nationally Determined Contributions IRR Internal Rate of Return MCA Multi Criteria Analysis MIRR Modified Internal Rate of Return MTPA Million Tonnes Per Annum NPV Net Present Value OPEX Operating expenditure SPV Special Purpose Vehicle 2 TA Technical Assistance tpa tonnes per annum TRL Technology readiness level VGF Viability Gap Funding WACC Weighted Average Cost of Capital WDV Written Down Value NOTES (i) The fiscal year (FY) of the Government and its agencies ends on March 31. (ii)In this report, "$" refers to US dollars, unless otherwise stated. -

Urban and Landscape Design Strategies for Flood Resilience In

QATAR UNIVERSITY COLLEGE OF ENGINEERING URBAN AND LANDSCAPE DESIGN STRATEGIES FOR FLOOD RESILIENCE IN CHENNAI CITY BY ALIFA MUNEERUDEEN A Thesis Submitted to the Faculty of the College of Engineering in Partial Fulfillment of the Requirements for the Degree of Masters of Science in Urban Planning and Design June 2017 © 2017 Alifa Muneerudeen. All Rights Reserved. COMMITTEE PAGE The members of the Committee approve the Thesis of Alifa Muneerudeen defended on 24/05/2017. Dr. Anna Grichting Solder Thesis Supervisor Qatar University Kwi-Gon Kim Examining Committee Member Seoul National University Dr. M. Salim Ferwati Examining Committee Member Qatar University Mohamed Arselene Ayari Examining Committee Member Qatar University Approved: Khalifa Al-Khalifa, Dean, College of Engineering ii ABSTRACT Muneerudeen, Alifa, Masters: June, 2017, Masters of Science in Urban Planning & Design Title: Urban and Landscape Design Strategies for Flood Resilience in Chennai City Supervisor of Thesis: Dr. Anna Grichting Solder. Chennai, the capital city of Tamil Nadu is located in the South East of India and lies at a mere 6.7m above mean sea level. Chennai is in a vulnerable location due to storm surges as well as tropical cyclones that bring about heavy rains and yearly floods. The 2004 Tsunami greatly affected the coast, and rapid urbanization, accompanied by the reduction in the natural drain capacity of the ground caused by encroachments on marshes, wetlands and other ecologically sensitive and permeable areas has contributed to repeat flood events in the city. Channelized rivers and canals contaminated through the presence of informal settlements and garbage has exasperated the situation. Natural and man-made water infrastructures that include, monsoon water harvesting and storage systems such as the Temple tanks and reservoirs have been polluted, and have fallen into disuse. -

Rpr-2009-7-1

ACKNOWLEDGEMENT The Comprehensive Asia Development Plan (CADP) is the crystallization of various academic efforts, especially the strong leadership, rigorous analysis, deep insight and relentless efforts of Dr. Fukunari Kimura and Mr. So Umezaki, with support from many other scholars including, Dr. Mitsuyo Ando, Dr. Haryo Aswicahyono, Dr. Ruth Banomyong, Dr. Truong Chi Binh, Dr. Nguyen Binh Giang, Dr. Toshitaka Gokan, Dr. Kazunobu Hayakawa, Dr. Socheth Hem, Dr. Patarapong Intarakumnerd, Dr. Masami Ishida, Mr. Toru Ishihara and his team, Dr. Ikumo Isono, Dr. Souknilan Keola, Dr. Somrote Komolavanij, Dr. Toshihiro Kudo, Dr. Satoru Kumagai, Dr. Moe Kyaw, Dr. Mari-Len Macasaquit, Dr. Tomohiro Machikita, Mr. Mitsuhiro Maeda, Dr. Sunil Mani, Dr. Toru Mihara, Dr. Avvari V. Mohan, Dr. Siwage Dharma Negara, Dr. Leuam Nhongvongsithi, Dr. Ayako Obashi, Dr. Apichat Sopadang, Dr. Chang Yii Tan, Dr. Masatsugu Tsuji, Dr. Yasushi Ueki and Dr. Korrakot Yaibuathet. ERIA also owes grateful thanks to research groups in Nippon Koei and the National University of Singapore. ERIA is also grateful for valuable guidance and instructions provided by the ASEAN Secretariat and inter-alia His Excellency Dr. Surin Pitsuwan, Secretary-General of ASEAN, in making the CADP properly responsive to the needs of policy makers and in providing great support for our activities. Additionally ERIA would like to express its deepest gratitude to the Asian Development Bank (ADB), the United Nations Economic and Social Commission for Asia and the Pacific (UNESCAP), and various donor agencies including the Japan International Cooperation Agency (JICA) for providing valuable information related to infrastructure projects, and other inputs. Especially we thank ADB for making time to conduct informal discussions with our team, and for the insights provided which were really useful for our analysis. -

The Law and Policy of Rainwater Harvesting: a Comparative Analysis of Australia, India, and the United States

The Law and Policy of Rainwater Harvesting: A Comparative Analysis of Australia, India, and the United States Brianne Holland-Stergar* ABSTRACT Rainwater harvesting is increasingly being turned to as a viable water conservation measure in the face of increasing water shortages. Legislatures at local, state, and national levels have begun implementing legislation that regulates rainwater harvesting; in some cases, governments choose to make the practice mandatory. This article examines four mandatory rainwater harvesting policies implemented in Australia, India, and the United States. The article summarizes the relative success of each policy’s adoption, and then moves on to discuss the impact of the policy on overall water conservation. In comparing the relative success of the policies, one finds that while financial investment plays an important role in determining the impact of the programs, other factors, such as the leniency of the mandate, cost to consumer, and support from non-governmental organizations play an important role in determining whether the policies are adopted. Furthermore, policymakers can encourage greater water conservation by incentivizing behavioral change and creating more robust financial incentives. * UCLA School of Law, J.D. Candidate, 2018; Harvard University, B.A., 2013; Arizona State University, M.Ed., 2015. © 2018 Brianne Holland-Stergar. All rights reserved. 127 128 JOURNAL OF ENVIRONMENTAL LAW Vol: 36:1 TABLE OF CONTENTS INTRODUCTION ........................................................................................ -

Tamil Nadu AAR

Tax alert: ITC on inward supply used to provide free medical facilities to employees not available – Tamil Nadu AAR Issued on: 27 September 2019 Summary The Tamil Nadu Advance Ruling Authority (AAR), in a recent case, has held that the applicant providing free medical facilities to the employees, pensioners, and their dependents in in-house hospital as a part of the mandated rules is not entitled to take credit of input tax paid on the inward supply of medicines/medical equipment used therein. The AAR stated that the medicines are used by the employees and dependents and hence are for personal consumption, disentitling the applicant for availing input tax credit (ITC) on said supplies. Facts of the case Benefits only to the employees: The applicant The applicant1 is engaged in the supply of port services submitted that the hospital caters only to the and incidental supply of goods like disposal of employees, their dependents, pensioners, and their discarded assets. spouses for in-patient and out-patient treatment. No outsiders are treated in the hospital except on The applicant is required to provide health and medical recommendation of the employees, and the payment cover to its employees and pensioners under relevant for that is recovered from the salary of such employees. regulations2. The applicant is maintaining an in-house hospital within its port premises for providing these Mandatory requirement as per relevant regulations: health and medical covers exclusively to its employees The applicant is mandatorily required to provide such and pensioners. health and medical cover to the employees and pensioners under the relevant regulations2. -

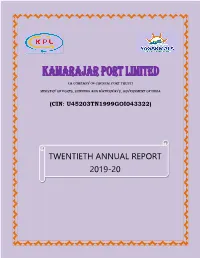

Twentieth Annual Report 2019-20

(A Company of Chennai Port Trust) Ministry of Ports, Shipping and Waterways, Government of India (CIN: U45203TN1999GOI043322) TWENTIETH ANNUAL REPORT 2019-20 KAMARAJAR PORT LIMITED Board of Directors DIN Shri Sunil Paliwal, Chairman-cum-Managing Director 01310101 Shri P. Raveendran, Nominee Director- ChPT 07640613 Shri S. Balaji Arunkumar, Nominee Director- ChPT 07526368 Shri V.M.V. Subba Rao, Independent Director 02435597 Capt. Anoop Kumar Sharma, Independent Director 03531392 Smt. Sarla Balagopal, Independent Director 01572718 Key Officials Depositories Shri Sanjay Kumar, National Securities Depository Limited General Manager (CS & BD) Central Depositories Services (India) Limited Shri M. Gunasekaran, Registered Office General Manager (Finance) cum CFO 2nd Floor (North Wing) & 3rd Floor Jawahar Building, Capt. A.K. Gupta, 17, Rajaji Salai, Chennai - 600 001. General Manager (Marine Services) Ph: 044 - 25251666-70 / Fax : 044 - 25251665 Shri V. Krishnasamy, Registrar & Share Transfer Agent General Manager (Operation) Link Intime India Private Limited Shri P. Radhakrishnan, C-101, 247 Park, L.B.S Marg Deputy General Manager (Civil) Vikhroli (West), Mumbai – 400 083. Ph : 022 – 49186000 / Fax : 022 - 49186060 Smt. Jayalakshmi Srinivasan Statutory Auditors Company Secretary M/s. B. Thiyagarajan & Co. Debenture Trustees Chartered Accountants (i) SBICAP Trustee Company Ltd Internal Auditors Mistry Bhavan, 4th Floor, M/s. Joseph & Rajaram 122, Dinshaw Vachha Road, Chartered Accountants Churchgate, Mumbai – 400 020. Ph: 022 – 43025555 Secretarial -

CADP 2.0) Infrastructure for Connectivity and Innovation

The Comprehensive Asia Development Plan 2.0 (CADP 2.0) Infrastructure for Connectivity and Innovation November 2015 Economic Research Institute for ASEAN and East Asia The findings, interpretations, and conclusions expressed herein do not necessarily reflect the views and policies of the Economic Research Institute for ASEAN and East Asia, its Governing Board, Academic Advisory Council, or the institutions and governments they represent. All rights reserved. Material in this publication may be freely quoted or reprinted with proper acknowledgement. Cover Art by Artmosphere ERIA Research Project Report 2014, No.4 National Library of Indonesia Cataloguing in Publication Data ISBN: 978-602-8660-88-4 Contents Acknowledgement iv List of Tables vi List of Figures and Graphics viii Executive Summary x Chapter 1 Development Strategies and CADP 2.0 1 Chapter 2 Infrastructure for Connectivity and Innovation: The 7 Conceptual Framework Chapter 3 The Quality of Infrastructure and Infrastructure 31 Projects Chapter 4 The Assessment of Industrialisation and Urbanisation 41 Chapter 5 Assessment of Soft and Hard Infrastructure 67 Development Chapter 6 Three Tiers of Soft and Hard Infrastructure 83 Development Chapter 7 Quantitative Assessment on Hard/Soft Infrastructure 117 Development: The Geographical Simulation Analysis for CADP 2.0 Appendix 1 List of Prospective Projects 151 Appendix 2 Non-Tariff Barriers in IDE/ERIA-GSM 183 References 185 iii Acknowledgements The original version of the Comprehensive Asia Development Plan (CADP) presents a grand spatial design of economic infrastructure and industrial placement in ASEAN and East Asia. Since the submission of such first version of the CADP to the East Asia Summit in 2010, ASEAN and East Asia have made significant achievements in developing hard infrastructure, enhancing connectivity, and participating in international production networks. -

MM Vol. XXIII No. 20.Pmd

Registered with the Reg. No. TN/CH(C)/374/12-14 Registrar of Newspapers Licenced to post without prepayment for India under R.N.I. 53640/91 Licence No. TN/PMG(CCR)/WPP-506/12-14 Publication: 15th & 28th of every month Rs. 5 per copy (Annual Subscription: Rs. 100/-) WE CARE FOR MADRAS THAT IS CHENNAI INSIDE • Short ‘N’ Snappy • Attention-drawing calendar • A doyen of Philately • What’s in street names? • What ails TN cricket? Vol. XXIII No. 20 MUSINGS February 1-15, 2014 If Chennai is to be 52 places for the G Can we recognise that the footpath is a necessity for a tourist walking and easy access traveller in 2014 and therefore cannot be encroached upon? (according to the New York Times) destination... G Can we, while designing our buildings, respect the Witness a city in transformation, glimpse exotic animals, neighbours’ space and also explore the past and enjoy that beach before the crowds. Chennai, in the State of Tamil Nadu (and formerly ensure that those who “known as Madras), was long considered the gateway to are otherwise abled can 1. Cape Town, 26. Chennai, India popular South Indian tourist destinations like Kerala but South Africa 27. Seychelles easily gain access to our 2. Christchurch, 28. Krabi, Thailand was overlooked as an attraction itself. It is, however, a na- buildings? tional cultural capital and home to several dance and mu- New Zealand 29. Aspen, Colo. G Can we have a law to pro- 3. North Coast, California 30. Highlands, Iceland sic schools like Kalakshetra for dance and the Music Acad- 4. -

Igcs Bulletin

IGCS BULLETIN VOL 3: ISSUE 3 July 2014 Dear Readers, Sustainable Management of Re- Contents sources with a structured pro- This issue of the IGCS Bulletin gramme comprising lectures, student contains an interesting student projects, field visits and cultural trips. project: ‘Transportation and Mobility 2 Going by the feedback, the two week IGCS NEWS Issues in Thyagaraya Nagar, programme was a hit with the twen- Chennai’, a vibrant commercial 5 ty five Indian and German student PROJECT REPORT: centre in Chennai. The article is participants. Kudos to Prof Kranert written by Ms Sonam Sahu and TRANSPORTATION AND MOBILITY and his team for the successful fellow team members of IGCS Winter ISSUES IN THYAGARAYA NAGAR, event! A Steering Committee School held in IIT Madras in March meeting was also held in Stuttgart. CHENNAI 2014. It provides a good portrayal of traffic concerns, lessons learnt and If the first quarter of 2014 was FEATURE: 9 suggestions for improvement. eventful with visits by short-term professors, the second quarter was SOLID WASTE MANAGEMENT Solid waste management has equally Gemütlichkeit (sociable). Two IN CHENNAI become a major environmental German students joined our IGCS concern in the country. Chennai, the family in July and two more are fourth largest metropolitan city in expected to join us in August. India is facing an uphill task in Wholeheartedly…Welcome to IGCS! keeping the city clean with its growing solid waste generation. This This issue also contain the regular is the topic of the feature article section on Forthcoming Conferences titled: ‘Solid Waste Management in Happy Reading!! Chennai’, written by Ruben Sudhakar and Ajit Kolar.