WITIDN AIRLINES and BETWEEN AIRLINES and the INDUSTRY Dawna L

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Community Outreach

Truckee Tahoe Airport District COMMUNITY OUTREACH Neighborhood Meetings October 2016 Draft Acknowledgements We wish to thank our supportive community who provided their insight and thoughtful feedback. TRUCKEE TAHOE AIRPORT DISTRICT BOARD AIRPORT COMMUNITY ADVISORY TEAM Lisa Wallace, President Kathryn Rohlf, Community Member/Chair James W. Morrison, Vice President Joe Polverari, Pilot Member/Vice Chair Mary Hetherington Christopher Gage, Pilot Member John B. Jones, Jr. Leigh Golden, Pilot Member J. Thomas Van Berkem Kent Hoopingarner, Community Member/Treasurer Lisa Krueger, Community Member AIRPORT STAFF Kevin Smith, General Manager BRIDGENET INTERNATIONAL Hardy Bullock, Director of Aviation Cindy Gibbs, Airspace Study Project Manager and Community Services Marc R. Lamb, Aviation and FRESHTRACKS COMMUNICATIONS Community Services Manager Seana Doherty, Owner/Founder Michael Cooke, Aviation and Phebe Bell, Facilitator Community Services Manager Amanda Wiebush, Associate Jill McClendon, Aviation and Community Greyson Howard,Mead &Associate Hunt, Inc. M & H Architecture, Inc. Services Program Coordinator 133 Aviation Boulevard, Suite 100 Lauren C. Tapia, District Clerk MEAD & HUNT,Santa INC. Rosa, California 95403 Mitchell Hooper,707-526-5010 West Coast Aviation meadhunt.com Planning Manager Brad Musinski, Aviation Planner Maranda Thompson, Aviation Planner TABLE OF CONTENTS 1 INTRODUCTION AND PROGRAM DESIGN .............................................. 1 2 NEIGHBORHOOD FEEDBACK ..................................................................... 5 APPENDICES A. Meeting Materials B. Public Comments C. Advertising and Marketing Efforts Introduction and ProgramMead & Hunt, Inc. Design M & H Architecture, Inc. 133 Aviation Boulevard, Suite 100 Santa Rosa, California 95403 707-526-5010 meadhunt.com INTRODUCTION Purpose The Truckee Tahoe Airport District (TTAD) understands that community input is incredibly valuable in developing good policies and making sound decisions about Truckee Tahoe Airport (TRK). -

Civilian Involvement in the 1990-91 Gulf War Through the Civil Reserve Air Fleet Charles Imbriani

Florida State University Libraries Electronic Theses, Treatises and Dissertations The Graduate School 2012 Civilian Involvement in the 1990-91 Gulf War Through the Civil Reserve Air Fleet Charles Imbriani Follow this and additional works at the FSU Digital Library. For more information, please contact [email protected] THE FLORIDA STATE UNIVERSITY COLLEGE OF ARTS AND SCIENCE CIVILIAN INVOLVEMENT IN THE 1990-91 GULF WAR THROUGH THE CIVIL RESERVE AIR FLEET By CHARLES IMBRIANI A Dissertation submitted to the Interdisciplinary Program in the Humanities in partial fulfillment of the requirements for the degree of Doctor of Philosophy Degree Awarded: Fall Semester, 2012 Charles Imbriani defended this dissertation on October 4, 2012. The members of the supervisory committee were: Peter Garretson Professor Directing Dissertation Jonathan Grant University Representative Dennis Moore Committee Member Irene Zanini-Cordi Committee Member The Graduate School has verified and approved the above-named committee members, and certifies that the dissertation has been approved in accordance with university requirements. ii DEDICATION This dissertation is dedicated to Fred (Freddie) Bissert 1935-2012. I first met Freddie over forty years ago when I stared working for Pan American World Airways in New York. It was twenty-two year later, still with Pan Am, when I took a position as ramp operations trainer; and Freddie was assigned to teach me the tools of the trade. In 1989 while in Berlin for training, Freddie and I witnessed the abandoning of the guard towers along the Berlin Wall by the East Germans. We didn’t realize it then, but we were witnessing the beginning of the end of the Cold War. -

Runway Excursion During Landing, Delta Air Lines Flight 1086, Boeing MD-88, N909DL, New York, New York, March 5, 2015

Runway Excursion During Landing Delta Air Lines Flight 1086 Boeing MD-88, N909DL New York, New York March 5, 2015 Accident Report NTSB/AAR-16/02 National PB2016-104166 Transportation Safety Board NTSB/AAR-16/02 PB2016-104166 Notation 8780 Adopted September 13, 2016 Aircraft Accident Report Runway Excursion During Landing Delta Air Lines Flight 1086 Boeing MD-88, N909DL New York, New York March 5, 2015 National Transportation Safety Board 490 L’Enfant Plaza, S.W. Washington, D.C. 20594 National Transportation Safety Board. 2016. Runway Excursion During Landing, Delta Air Lines Flight 1086, Boeing MD-88, N909DL, New York, New York, March 5, 2015. Aircraft Accident Report NTSB/AAR-16/02. Washington, DC. Abstract: This report discusses the March 5, 2015, accident in which Delta Air Lines flight 1086, a Boeing MD-88 airplane, N909DL, was landing on runway 13 at LaGuardia Airport, New York, New York, when it departed the left side of the runway, contacted the airport perimeter fence, and came to rest with the airplane’s nose on an embankment next to Flushing Bay. The 2 pilots, 3 flight attendants, and 98 of the 127 passengers were not injured; the other 29 passengers received minor injuries. The airplane was substantially damaged. Safety issues discussed in the report relate to the use of excessive engine reverse thrust and rudder blanking on MD-80 series airplanes, the subjective nature of braking action reports, the lack of procedures for crew communications during an emergency or a non-normal event without operative communication systems, inaccurate passenger counts provided to emergency responders following an accident, and unclear policies regarding runway friction measurements and runway condition reporting. -

United States Court of Appeals for the DISTRICT of COLUMBIA CIRCUIT

USCA Case #11-1018 Document #1351383 Filed: 01/06/2012 Page 1 of 12 United States Court of Appeals FOR THE DISTRICT OF COLUMBIA CIRCUIT Argued November 8, 2011 Decided January 6, 2012 No. 11-1018 REPUBLIC AIRLINE INC., PETITIONER v. UNITED STATES DEPARTMENT OF TRANSPORTATION, RESPONDENT On Petition for Review of an Order of the Department of Transportation Christopher T. Handman argued the cause for the petitioner. Robert E. Cohn, Patrick R. Rizzi and Dominic F. Perella were on brief. Timothy H. Goodman, Senior Trial Attorney, United States Department of Transportation, argued the cause for the respondent. Robert B. Nicholson and Finnuala K. Tessier, Attorneys, United States Department of Justice, Paul M. Geier, Assistant General Counsel for Litigation, and Peter J. Plocki, Deputy Assistant General Counsel for Litigation, were on brief. Joy Park, Trial Attorney, United States Department of Transportation, entered an appearance. USCA Case #11-1018 Document #1351383 Filed: 01/06/2012 Page 2 of 12 2 Before: HENDERSON, Circuit Judge, and WILLIAMS and RANDOLPH, Senior Circuit Judges. Opinion for the Court filed by Circuit Judge HENDERSON. KAREN LECRAFT HENDERSON, Circuit Judge: Republic Airline Inc. (Republic) challenges an order of the Department of Transportation (DOT) withdrawing two Republic “slot exemptions” at Ronald Reagan Washington National Airport (Reagan National) and reallocating those exemptions to Sun Country Airlines (Sun Country). In both an informal letter to Republic dated November 25, 2009 and its final order, DOT held that Republic’s parent company, Republic Airways Holdings, Inc. (Republic Holdings), engaged in an impermissible slot-exemption transfer with Midwest Airlines, Inc. (Midwest). -

My Personal Callsign List This List Was Not Designed for Publication However Due to Several Requests I Have Decided to Make It Downloadable

- www.egxwinfogroup.co.uk - The EGXWinfo Group of Twitter Accounts - @EGXWinfoGroup on Twitter - My Personal Callsign List This list was not designed for publication however due to several requests I have decided to make it downloadable. It is a mixture of listed callsigns and logged callsigns so some have numbers after the callsign as they were heard. Use CTL+F in Adobe Reader to search for your callsign Callsign ICAO/PRI IATA Unit Type Based Country Type ABG AAB W9 Abelag Aviation Belgium Civil ARMYAIR AAC Army Air Corps United Kingdom Civil AgustaWestland Lynx AH.9A/AW159 Wildcat ARMYAIR 200# AAC 2Regt | AAC AH.1 AAC Middle Wallop United Kingdom Military ARMYAIR 300# AAC 3Regt | AAC AgustaWestland AH-64 Apache AH.1 RAF Wattisham United Kingdom Military ARMYAIR 400# AAC 4Regt | AAC AgustaWestland AH-64 Apache AH.1 RAF Wattisham United Kingdom Military ARMYAIR 500# AAC 5Regt AAC/RAF Britten-Norman Islander/Defender JHCFS Aldergrove United Kingdom Military ARMYAIR 600# AAC 657Sqn | JSFAW | AAC Various RAF Odiham United Kingdom Military Ambassador AAD Mann Air Ltd United Kingdom Civil AIGLE AZUR AAF ZI Aigle Azur France Civil ATLANTIC AAG KI Air Atlantique United Kingdom Civil ATLANTIC AAG Atlantic Flight Training United Kingdom Civil ALOHA AAH KH Aloha Air Cargo United States Civil BOREALIS AAI Air Aurora United States Civil ALFA SUDAN AAJ Alfa Airlines Sudan Civil ALASKA ISLAND AAK Alaska Island Air United States Civil AMERICAN AAL AA American Airlines United States Civil AM CORP AAM Aviation Management Corporation United States Civil -

July/August 2000 Volume 26, No

Irfc/I0 vfa£ /1 \ 4* Limited Edition Collectables/Role Model Calendars at home or in the office - these photo montages make a statement about who we are and what we can be... 2000 1999 Cmdr. Patricia L. Beckman Willa Brown Marcia Buckingham Jerrie Cobb Lt. Col. Eileen M. Collins Amelia Earhart Wally Funk julie Mikula Maj. lacquelyn S. Parker Harriet Quimby Bobbi Trout Captain Emily Howell Warner Lt. Col. Betty Jane Williams, Ret. 2000 Barbara McConnell Barrett Colonel Eileen M. Collins Jacqueline "lackie" Cochran Vicky Doering Anne Morrow Lindbergh Elizabeth Matarese Col. Sally D. Woolfolk Murphy Terry London Rinehart Jacqueline L. “lacque" Smith Patty Wagstaff Florene Miller Watson Fay Cillis Wells While They Last! Ship to: QUANTITY Name _ Women in Aviation 1999 ($12.50 each) ___________ Address Women in Aviation 2000 $12.50 each) ___________ Tax (CA Residents add 8.25%) ___________ Shipping/Handling ($4 each) ___________ City ________________________________________________ T O TA L ___________ S ta te ___________________________________________ Zip Make Checks Payable to: Aviation Archives Phone _______________________________Email_______ 2464 El Camino Real, #99, Santa Clara, CA 95051 [email protected] INTERNATIONAL WOMEN PILOTS (ISSN 0273-608X) 99 NEWS INTERNATIONAL Published by THE NINETV-NINES* INC. International Organization of Women Pilots A Delaware Nonprofit Corporation Organized November 2, 1929 WOMEN PILOTS INTERNATIONAL HEADQUARTERS Box 965, 7100 Terminal Drive OFFICIAL PUBLICATION OFTHE NINETY-NINES® INC. Oklahoma City, -

Federal Aviation Administration Curriculum Guide for Aviation

U.S. Department of Transportation Federal Aviation Administration FAA Headquarters Aviation Education Division FEDERAL AVIATION ADMINISTRATION CURRICULUM GUIDE FOR AVIATION MAGNET SCHOOLS PROGRAMS Prepared by Dr. Mervin K. Strickler, Jr. AHT-100-1-94 ABOUT THE AUTHOR Dr. Mervin K. Strickler, Jr., a native of Pennsylvania, graduated from Clarion State University. In 1951 he received his doctorate from Stanford University with specialization in aviation higher education. During his long and distinguished career he served as Director, USAF-Civil Air Patrol Aviation Education from 1951 to 1960, and as Director of the Federal Aviation Administration's Aviation Education Program from 1960 to 1979. From 1973 to 1979, he also worked with the Commonwealth of Independent States (then Soviet Union) as the FAA's representative for scientific and technical aviation education and training for all facets of civil aviation. He continues today as an international consultant on aviation education matters to industry, government, and all levels of education. Dr. Strickler's many publications and papers are included in libraries around the world. He is frequently called upon to speak at major aviation events and is well known nationally and internationally for his expertise in aviation education. PREFACE The Federal Aviation Administration's current interests, activities, projects and programs in aviation education represent and stem from a continuation and expansion of programs and similar initiatives of its predecessor organizations. Present programs are a result of the most recent FAA Administrator's Task Force Report on Aviation Education completed in 1990. The Report identified over fifty aviation education initiatives as appropriate to support the agency's objectives. -

Adaptive Connected.Xlsx

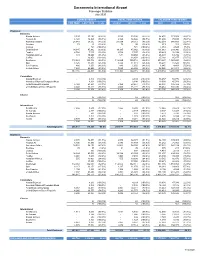

Sacramento International Airport Passenger Statistics July 2020 CURRENT MONTH FISCAL YEAR TO DATE CALENDAR YEAR TO DATE THIS YEAR LAST YEAR % +/(-) 2020/21 2019/20 % +/(-) 2020 2019 % +/(-) Enplaned Domestic Alaska Airlines 3,593 33,186 (89.2%) 3,593 33,186 (89.2%) 54,432 173,858 (68.7%) Horizon Air 6,120 14,826 (58.7%) 6,120 14,826 (58.7%) 31,298 75,723 (58.7%) American Airlines 28,089 54,512 (48.5%) 28,089 54,512 (48.5%) 162,319 348,689 (53.4%) Boutique 79 95 (16.8%) 79 95 (16.8%) 613 201 205.0% Contour - 721 (100.0%) - 721 (100.0%) 4,461 2,528 76.5% Delta Airlines 14,185 45,962 (69.1%) 14,185 45,962 (69.1%) 111,063 233,946 (52.5%) Frontier 4,768 7,107 (32.9%) 4,768 7,107 (32.9%) 25,423 38,194 (33.4%) Hawaiian Airlines 531 10,660 (95.0%) 531 10,660 (95.0%) 26,393 64,786 (59.3%) Jet Blue - 16,858 (100.0%) - 16,858 (100.0%) 25,168 85,877 (70.7%) Southwest 112,869 300,716 (62.5%) 112,869 300,716 (62.5%) 899,647 1,963,253 (54.2%) Spirit 8,425 11,318 (25.6%) 8,425 11,318 (25.6%) 38,294 15,526 146.6% Sun Country 886 1,650 (46.3%) 886 1,650 (46.3%) 1,945 4,401 (55.8%) United Airlines 7,620 46,405 (83.6%) 7,620 46,405 (83.6%) 98,028 281,911 (65.2%) 187,165 544,016 (65.6%) 187,165 544,016 (65.6%) 1,479,084 3,288,893 (55.0%) Commuters Alaska/Skywest - 4,304 (100.0%) - 4,304 (100.0%) 36,457 50,776 (28.2%) American/Skywest/Compass/Mesa - 8,198 (100.0%) - 8,198 (100.0%) 18,030 45,781 (60.6%) Delta/Skywest/Compass 5,168 23,651 (78.1%) 5,168 23,651 (78.1%) 62,894 146,422 (57.0%) United/Skywest/GoJet/Republic 4,040 16,221 (75.1%) 4,040 16,221 (75.1%) -

Overview and Trends

9310-01 Chapter 1 10/12/99 14:48 Page 15 1 M Overview and Trends The Transportation Research Board (TRB) study committee that pro- duced Winds of Change held its final meeting in the spring of 1991. The committee had reviewed the general experience of the U.S. airline in- dustry during the more than a dozen years since legislation ended gov- ernment economic regulation of entry, pricing, and ticket distribution in the domestic market.1 The committee examined issues ranging from passenger fares and service in small communities to aviation safety and the federal government’s performance in accommodating the escalating demands on air traffic control. At the time, it was still being debated whether airline deregulation was favorable to consumers. Once viewed as contrary to the public interest,2 the vigorous airline competition 1 The Airline Deregulation Act of 1978 was preceded by market-oriented administra- tive reforms adopted by the Civil Aeronautics Board (CAB) beginning in 1975. 2 Congress adopted the public utility form of regulation for the airline industry when it created CAB, partly out of concern that the small scale of the industry and number of willing entrants would lead to excessive competition and capacity, ultimately having neg- ative effects on service and perhaps leading to monopolies and having adverse effects on consumers in the end (Levine 1965; Meyer et al. 1959). 15 9310-01 Chapter 1 10/12/99 14:48 Page 16 16 ENTRY AND COMPETITION IN THE U.S. AIRLINE INDUSTRY spurred by deregulation now is commonly credited with generating large and lasting public benefits. -

Appendix C Informal Complaints to DOT by New Entrant Airlines About Unfair Exclusionary Practices March 1993 to May 1999

9310-08 App C 10/12/99 13:40 Page 171 Appendix C Informal Complaints to DOT by New Entrant Airlines About Unfair Exclusionary Practices March 1993 to May 1999 UNFAIR PRICING AND CAPACITY RESPONSES 1. Date Raised: May 1999 Complaining Party: AccessAir Complained Against: Northwest Airlines Description: AccessAir, a new airline headquartered in Des Moines, Iowa, began service in the New York–LaGuardia and Los Angeles to Mo- line/Quad Cities/Peoria, Illinois, markets. Northwest offers connecting service in these markets. AccessAir alleged that Northwest was offering fares in these markets that were substantially below Northwest’s costs. 171 9310-08 App C 10/12/99 13:40 Page 172 172 ENTRY AND COMPETITION IN THE U.S. AIRLINE INDUSTRY 2. Date Raised: March 1999 Complaining Party: AccessAir Complained Against: Delta, Northwest, and TWA Description: AccessAir was a new entrant air carrier, headquartered in Des Moines, Iowa. In February 1999, AccessAir began service to New York–LaGuardia and Los Angeles from Des Moines, Iowa, and Moline/ Quad Cities/Peoria, Illinois. AccessAir offered direct service (nonstop or single-plane) between these points, while competitors generally offered connecting service. In the Des Moines/Moline–Los Angeles market, Ac- cessAir offered an introductory roundtrip fare of $198 during the first month of operation and then planned to raise the fare to $298 after March 5, 1999. AccessAir pointed out that its lowest fare of $298 was substantially below the major airlines’ normal 14- to 21-day advance pur- chase fares of $380 to $480 per roundtrip and was less than half of the major airlines’ normal 7-day advance purchase fare of $680. -

RESOURCE Air Travel 2001

RESOURCE SYSTEMS GROUP INCORPORATED Air Travel 2001 What do they tell us about the future of US air travel? An Industry Report by Resource Systems Group, Inc. December 2001 331 Olcott Drive, White River Junction, Vermont 05001 802.295.4999 www.rsginc.com www.surveycafe.com TABLE OF CONTENTS INTRODUCTION..........................................................................................................................................2 THE SURVEY SAMPLE ..............................................................................................................................2 TRIP CHARACTERISTICS..........................................................................................................................2 RESERVATIONS AND TICKETING............................................................................................................3 CHOICE OF TICKETING LOCATIONS ....................................................................................................3 SATISFACTION WITH TICKETING OPTIONS ........................................................................................4 TICKETING SEGMENTS .........................................................................................................................7 AIRPORTS ..................................................................................................................................................7 AIRLINE RANKINGS.................................................................................................................................12 -

363 Part 238—Contracts With

Immigration and Naturalization Service, Justice § 238.3 (2) The country where the alien was mented on Form I±420. The contracts born; with transportation lines referred to in (3) The country where the alien has a section 238(c) of the Act shall be made residence; or by the Commissioner on behalf of the (4) Any country willing to accept the government and shall be documented alien. on Form I±426. The contracts with (c) Contiguous territory and adjacent transportation lines desiring their pas- islands. Any alien ordered excluded who sengers to be preinspected at places boarded an aircraft or vessel in foreign outside the United States shall be contiguous territory or in any adjacent made by the Commissioner on behalf of island shall be deported to such foreign the government and shall be docu- contiguous territory or adjacent island mented on Form I±425; except that con- if the alien is a native, citizen, subject, tracts for irregularly operated charter or national of such foreign contiguous flights may be entered into by the Ex- territory or adjacent island, or if the ecutive Associate Commissioner for alien has a residence in such foreign Operations or an Immigration Officer contiguous territory or adjacent is- designated by the Executive Associate land. Otherwise, the alien shall be de- Commissioner for Operations and hav- ported, in the first instance, to the ing jurisdiction over the location country in which is located the port at where the inspection will take place. which the alien embarked for such for- [57 FR 59907, Dec. 17, 1992] eign contiguous territory or adjacent island.