2019 City Wide Development Charges Background Study

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

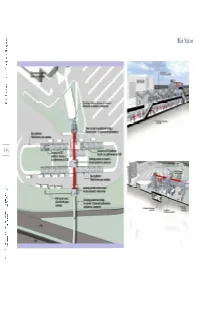

Appendix 5 Station Descriptions And

Appendix 5 Station Descriptions and Technical Overview Stage 2 light rail transit (LRT) stations will follow the same standards, design principles, and connectivity and mobility requirements as Stage 1 Confederation Line. Proponent Teams were instructed, through the guidelines outlined in the Project Agreement (PA), to design stations that will integrate with Stage 1, which include customer facilities, accessibility features, and the ability to support the City’s Transportation Master Plan (TMP) goals for public transit and ridership growth. The station features planned for the Stage 2 LRT Project will be designed and built on these performance standards which include: Barrier-free path of travel to entrances of stations; Accessible fare gates at each entrance, providing easy access for customers using mobility devices or service animals; Tactile wayfinding tiles will trace the accessible route through the fare gates, to elevators, platforms and exits; Transecure waiting areas on the train platform will include accessible benches and tactile/Braille signs indicating the direction of service; Tactile warning strips and inter-car barriers to keep everyone safely away from the platform edge; Audio announcements and visual displays for waiting passengers will precede each train’s arrival on the platform and will describe the direction of travel; Service alerts will be shown visually on the passenger information display monitors and announced audibly on the public-address system; All wayfinding and safety signage will be provided following the applicable accessibility standards (including type size, tactile signage, and appropriate colour contrast); Clear, open sight lines and pedestrian design that make wayfinding simple and intuitive; and, Cycling facilities at all stations including shelter for 80 per cent of the provided spaces, with additional space protected to ensure cycling facilities can be doubled and integrated into the station’s footprint. -

4005 Strandherd Drive TIA Report

August 2019 4005 Strandherd Drive TIA Report 4005 Strandherd Drive TIA Strategy Report prepared for: grc Architects 47 Clarence Street, Suite 401 Ottawa, Ontario K1N 9K1 prepared by: 1223 Michael Street North Suite 100 Ottawa, ON K1J 7T2 August 13, 2019 476618-01000 Table of Contents 1. SCREENING FORM................................................................................................................................................................ 1 2. DESCRIPTION OF PROPOSED DEVELOPMENT .................................................................................................................... 1 2.1. PROPOSED DEVELOPMENT ......................................................................................................................................... 1 3. EXISTING CONDITIONS ......................................................................................................................................................... 3 3.1. AREA ROAD NETWORK ................................................................................................................................................ 3 3.2. PEDESTRIAN/CYCLING NETWORK .............................................................................................................................. 3 3.3. TRANSIT NETWORK ..................................................................................................................................................... 3 3.4. EXISTING STUDY AREA INTERSECTION ...................................................................................................................... -

Transit Commission

Transit Commission Tax Supported Programs Tabled November 8, 2017 Table of Contents Transit Commission Briefing Note......................................................................................................................................................................1 Operating Resource Requirement.....................................................................................................................................3 User Fees..........................................................................................................................................................................4 Capital Program Funding Summary..................................................................................................................................7 Supplemental Operating & Capital Information.................................................................................................................9 Analysis..................................................................................................................................................................9 Explanatory Notes................................................................................................................................................10 Capital Budget.....................................................................................................................................................12 Project Details..........................................................................................................................................13 -

Project Synopsis

Final Draft Road Network Development Report Submitted to the City of Ottawa by IBI Group September 2013 Table of Contents 1. Introduction .......................................................................................... 1 1.1 Objectives ............................................................................................................ 1 1.2 Approach ............................................................................................................. 1 1.3 Report Structure .................................................................................................. 3 2. Background Information ...................................................................... 4 2.1 The TRANS Screenline System ......................................................................... 4 2.2 The TRANS Forecasting Model ......................................................................... 4 2.3 The 2008 Transportation Master Plan ............................................................... 7 2.4 Progress Since 2008 ........................................................................................... 9 Community Design Plans and Other Studies ................................................................. 9 Environmental Assessments ........................................................................................ 10 Approvals and Construction .......................................................................................... 10 3. Needs and Opportunities .................................................................. -

Transit Project Timelines Issue 2.0 for May 16, 2018 Nov, 2008 Transportation Master Plan Update and Nov., 2013 New Transportation Master Plan

Transit Project Timelines Issue 2.0 for May 16, 2018 Nov, 2008 Transportation Master Plan Update and Nov., 2013 New Transportation Master Plan BRT to Kanata LRT Stage 1 LRT Stage 2 Baseline Road Rapid ( “the West Transitway “Confederation Line” (three extensions to the Transit Corridor Extension”) (Blair to Tunney’s Pasture) Confederation Line) (Heron to Bayshore) Extensions to Trillium Line are another project - Nov. 2008 - decision to - Jan. 2010 EA approved study Bayshore to Moodie extension - Oct. 2012 “West - In 2011 council Transitway Extension” accelerated completion EPR approved (also date by a year referred to in Stage 2 - Dec. 2012 contract documents) awarded - 2013 construction begins - 2013 project approved - Sep. 2015 bridge over HA - Feb 2017 - decision to postponed to LRT stage 2 study Bayshore to Moodie - Moodie Bridge safety extension improvements postponed - June 2016 Rideau St. sinkhole - summer 2017 RFP sent out - June 2017 meetings about - Until fall 2017 LRT was to - fall 2017 Bayshore to - fall 2017 EPR approved Moodie extension have ended at Bayshore Moodie LRT extension - fall 2017 approved - After 2017 LRT (stage 2) approved ends at Moodie - Dec. 2017 Bayshore to Moodie extension open as part of bus route - CBLCA continues to work - Feb. 2018 EPR approved with city and contractors - July-Nov, 2018 Corkstown end of Nov. 2018 Blair to - Q4, 2018? Stage 2 contract sidewalk construction Tunney’s Pasture LRT to be awarded open - 2019 plan to start - 2020 “construction construction (as soon as could begin on first -

No. 48, Port Lands Flood Protection and Enabling Infrastructure, Page 54 Credit: Waterfront Toronto/Vid Ingelevics/Ryan Walker

2021 No. 48, Port Lands Flood Protection and Enabling Infrastructure, Page 54 Credit: Waterfront Toronto/Vid Ingelevics/Ryan Walker Top100 Projects 2021 Changing the Language of Top100 Projects — 2021 An annual report inserted in Infrastructure ReNew Canada’s had an interesting encounter following the release of last January/February 2021 issue year’s report, and I wanted to share in an effort to get I feedback from the rest of the industry. MANAGING Andrew Macklin We had released the 2020 Top100 Projects report and were EDITOR [email protected] getting set for the Key Players and Owners Dinner, which we host every February in Toronto as a celebration of the accomplishments GROUP Todd Latham PUBLISHER of the industry in developing infrastructure megaprojects. I had heard through one of my colleagues that a couple of well-respected PUBLISHER Nick Krukowski members of the industry wanted to chat with me at the event and I should seek them out. So I did. ART DIRECTOR AND Donna Endacott SENIOR DESIGN My first thought was that, not having nearly the expertise as many of you, that I had somehow managed to royally screw something ASSOCIATE Simran Chattha up. Or perhaps they wanted to tell me that I should try a different EDITOR tact to the report? Maybe a new idea for adding a complementary DIGITAL MARKETING Becky Umweni piece for this report? But as it turned out, they wanted to have a COORDINATOR conversation with me about… language. DIGITAL The language of this report has become, to some, quite convoluted. Connie Vitello EDITOR As different jurisdictions use the language familiar to them, it can often mean that, from one project to the next, different words are EVENT Natasha Mawji MANAGER used to describe the same thing. -

Ottawa Transportation Report.Pdf

OTTAWA THE IMPACT OF TRANSPORTATION IMPROVEMENTS ON HOUSING VALUES IN THE OTTAWA REGION Don R Campbell, Senior Analyst Melanie Reuter, Director of Research Allyssa Epp, Research Analyst WWW.REINCANADA.COM AUTHORS Don R. Campbell, Senior Analyst, REIN Ltd Melanie Reuter, Director of Research, REIN Ltd Allyssa Fischer, Research Analyst, REIN Ltd © The Real Estate Investment Network Ltd. 6 – 27250 58 Cr Langley, BC V4W 3W7 Tel (604) 856-2825 Fax (604) 856-0091 E-Mail: [email protected] Web Page: www.reincanada.com Important Disclaimer: This Report, or any seminars or updates given in relation thereto, is sold, or otherwise provided, on the understanding that the authors – Don R. Campbell, Melanie Reuter, Allyssa Fischer, and The Real Estate Investment Network Ltd and their instructors, are not responsible for any results or results of any actions taken in reliance upon any information contained in this report, or conveyed by way of the said seminars, nor for any errors contained therein or presented thereat or omissions in relation thereto. It is further understood that the said authors and instructors do not purport to render legal, accounting, tax, investment, financial planning or other professional advice. The said authors and instructors hereby disclaim all and any liability to any person, whether a purchaser of this Report, a student of the said seminars, or otherwise, arising in respect of this Report, or the said seminars, and of the consequences of anything done or purported to be done by any such person in reliance, whether in whole or part, upon the whole or any part of the contents of this Report or the said seminars. -

300 Tremblay Road TIA Strategy Report

300 Tremblay Road TIA Strategy Report Prepared for: TCU Development Corporation 150 Isabella Street, Suite 100 Ottawa, ON K1S 5H3 Prepared by: Parsons 1223 Michael Street North, Suite 100 Ottawa, ON K1J 7T2 477570 - 01000 1335 & 1339 Bank Street –Scoping Report 1 Document Control Page CLIENT: TCU Development Corporation PROJECT NAME: 300 Tremblay Road REPORT TITLE: TIA Step 4 Strategy Report PARSONS PROJECT NO: 477570-01000 VERSION: Draft DIGITAL MASTER: \\XCCAN57FS01\Data\ISO\477570\1000\DOCS\STEP3-Forecasting\300 Tremblay - TIA Step 3 Forecasting Report.docx ORIGINATOR Juan Lavin, E.I.T. REVIEWER: Matt Mantle, P.Eng. AUTHORIZATION: CIRCULATION LIST: Mike Giampa, P.Eng. 1. TIA Step 1 Screening Form – July 9, 2020 2. TIA Step 2 Scoping Report – July 27, 2020 HISTORY: 3. TIA Step 3 Forecasting Report – August 21, 2020 4. TIA Step 4 Strategy Report – September 18, 2020 300 Tremblay Road – Strategy Report i TABLE OF CONTENTS DOCUMENT CONTROL PAGE ...................................................................................................................................... I 1. SCREENING FORM .............................................................................................................................................. 1 2. SCOPING REPORT ............................................................................................................................................... 1 2.1. EXISTING AND PLANNED CONDITIONS .................................................................................................. 1 -

Recommended Plan.Pdf

Blair Station 9-34 Maintenance and Storage Facility Track redundancy within the facility will be provided to ensure The proposed Maintenance and Storage Facility is an integral the ability to move LRVs under vehicle or system failure part of the project, as it will: conditions. • House and service all of the trains needed to operate the The preferred site for the Maintenance and Storage Facility has line been determined based on the following criteria: • Service vehicles to be used on future LRT lines • Site Characteristics (topography, grade, land use compatibility, expansion capability and environmental • House the operations control centre (signalling, considerations) communications) for the line • Facility Operations (turnaround loops, track redundancy, • Be the primary heavy maintenance facility for the LRT layout efficiency and municipal services) network Maintenance of the LRVs is crucial to maintain vehicle • System Operations (connectivity to the line, efficiency and manufacturer's warranties, minimize long term operating costs access to freight rail), and and provide for system safety and reliability. The Maintenance • Relative Costs (capital, operating, maintenance and and Storage Facility will accommodate the following elements property ownership and acquisition) on-site: The proposed Maintenance and Storage Facility for the DOTT 9-35 • Main facility building housing offices, roster areas, meeting project will be located on lands to the west of the existing OC rooms and control equipment Transpo headquarters and bus maintenance facility located on • Storage yard for regular cleaning and minor maintenance the north side of Belfast Road, west of St. Laurent Boulevard and south of the VIA rail corridor. In order to access this • Repair areas for heavy and light maintenance areas for location, a connecting track is required between the DOTT vehicles alignment and the Maintenance and Storage Facility. -

Template – RFQ Advertisement

INVITATION TO SUBMIT AN EXPRESSION OF INTEREST (EOI) AS TO THE AVAILABILITY OF SPACE FOR LEASE IN THE CITY OF OTTAWA (ONTARIO) FILE NUMBER 5225-2-2020-7 Public Works and Government Services Canada (PWGSC) is asking interested parties to provide information for a potential lease of space that meets the following criteria: Section A: Lease Components 1. a lease term of approximately ten (10) years, commencing on or about May 1, 2021, plus an option to extend the lease for one (1) additional period of five (5) years; 2. approximately 1,488 usable square metres (um2) of contiguous warehouse space, approximately 166 usable square metres (um2) of contiguous office space, four (4) regular and one (1) accessible parking spaces; 3. the proposed space must be available approximately twenty-six (26) weeks prior to the above-noted lease commencement date so all spaces may be prepared for occupancy; 4. the proposed space must be located in the city of Ottawa and within the following boundaries (the geographical boundaries include sites on either side of the roads): North: Ottawa River (including whole of Chaudière, Albert and Victoria islands) East: Trim Road, Navan Road, Milton Road South: Russel Road, Leitrim Road, Limebank Road, Earl Armstrong Road, Strandherd Drive West: Woodroffe Avenue, Carling Avenue, Woodroffe Avenue; Click here for a visual display of the above boundaries. Please note that this information is for presentation only and that the boundaries have precedence. 5. the proposed warehouse space should satisfy or be capable of satisfying the following criteria: (a) be contiguous with the office space; (b) minimum clear (ie: to the underside of lighting/sprinklers, etc.) nominal ceiling height: 6.7 metres (m); (c) minimum loading dock requirements: two (2) loading docks; . -

Mcgarry Terrace & Longfields Drive

DEVELOPMENT LAND FOR SALE MCGARRY TERRACE & LONGFIELDS DRIVE OTTAWA, ONTARIO STRANDHERD DRIVE GREENBANK ROAD 1034 MCGARRY TERRACE & 1117 LONGFIELDS DRIVE MCGARRY TERRACE & LONGFIELDS DRIVE | OTTAWA, ONTARIO DRIVE | OTTAWA, & LONGFIELDS TERRACE MCGARRY CBRE | MARKETING FLYER THE OPPORTUNITY CBRE Limited (“CBRE” or the “Advisor”) has been retained by the Vendor to act as its exclusive advisor to AREA CONTEXT facilitate the sale of 1034 McGarry Terrace and 1117 Longfields Drive (the “Property or Properties”), The Subject Properties are located in Ottawa’s southwest, in the community of Barrhaven. The surrounding area development land located in Ottawa, Ontario. Situated in the suburb of Ottawa’s Barrhaven neighbourhood, is predominantly made up of large format commercial/retail and restaurant uses, a range of residential dwelling the Property occupies a prominent position on the corner of Marketplace Avenue and Longfields Drive. types, and institutional uses that primarily serve members of the local community. The site is being sold on an as is where is basis on behalf of Cameron Stephens Financial Corporation in its The following identifies the land uses that surround the site: capacity as court ordered receiver for 1897365 Ontario Inc. NORTH: The 3.2 acre site is currently vacant. The Property is approved for a high mixed-use designation which allows The lands directly to the north of the Subject Properties consist of vacant lots that are zoned Mixed-Use Centre for apartments, retail, office and service commercial activities. The Property is designated for development to (heading towards Strandherd Drive) and a senior living residence at the corner of Strandherd Drive and Longfields a maximum of 16 storeys and the net density target for residential uses is 250 units per hectare. -

PORTFOLIO: CITY MANAGER's OFFICE PURCHASE ORDERS ≥ $10,000 AWARDED UNDER DELEGATION of AUTHORITY Document 1 for the PERIOD JULY 1, 2014 to SEPTEMBER 30, 2014

PORTFOLIO: CITY MANAGER'S OFFICE PURCHASE ORDERS ≥ $10,000 AWARDED UNDER DELEGATION OF AUTHORITY Document 1 FOR THE PERIOD JULY 1, 2014 TO SEPTEMBER 30, 2014 Professional / Follow-on / Item # PO Port Dept Branch Description Consulting Amount Vendor Non-Competitive Rationale Amendment Services 1 45078173 CMO CCS CPOS Standing offer to supply and deliver Records Management Materials on an as and when E $ 76,320.00 TAB PRODUCTS OF CANADA requested basis. WILLOWDALE ON 2 45070493 CMO CCS CPOS Courier services for standard light delivery materials for the City of Ottawa. A $ 28,757.38 ALL CANADIAN COURIER OTTAWA ON 3 45074332 CMO CCS CPOS Data entry services for the Courthouse and Provincial Offence Services branch to capture PO E $ 42,739.20 CRITICALCONTROL SOLUTIONS INC Section 22(1)(c) ticket information. MARKHAM ON Only one source of supply acceptable and cost effective 4 45078474 CMO CCS CPOS Print and deliver City of Ottawa Maintenance Activity Sheets, per Category A General $ 11,163.93 RR DONNELLEY Printing and Supporting Services. OTTAWA ON 5 45077752 CMO CCS CPOS Provide print production and document management services to support the 2014 $ 15,264.00 GILMORE DOCULINK Municipal Elections. KANATA ON 6 45078558 CMO CCS CPOS Supply, delivery and warehouse City of Ottawa payroll pressure seal direct deposit forms E $ 17,872.11 RR DONNELLEY Section 22(1)(e) on an as and when requested basis OTTAWA ON Security or Confidentiality Matters 7 45078230 CMO CCS EA Rental for one (1) month of fifty (50) iPhones for use by Elections staff for the 2014 $ 12,572.33 IT XCHANGE Municipal Election.