Monetary Failures of the Great Depression

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Free to Choose Video Tape Collection

http://oac.cdlib.org/findaid/ark:/13030/kt1n39r38j No online items Inventory to the Free to Choose video tape collection Finding aid prepared by Natasha Porfirenko Hoover Institution Library and Archives © 2008 434 Galvez Mall Stanford University Stanford, CA 94305-6003 [email protected] URL: http://www.hoover.org/library-and-archives Inventory to the Free to Choose 80201 1 video tape collection Title: Free to Choose video tape collection Date (inclusive): 1977-1987 Collection Number: 80201 Contributing Institution: Hoover Institution Library and Archives Language of Material: English Physical Description: 10 manuscript boxes, 10 motion picture film reels, 42 videoreels(26.6 Linear Feet) Abstract: Motion picture film, video tapes, and film strips of the television series Free to Choose, featuring Milton Friedman and relating to laissez-faire economics, produced in 1980 by Penn Communications and television station WQLN in Erie, Pennsylvania. Includes commercial and master film copies, unedited film, and correspondence, memoranda, and legal agreements dated from 1977 to 1987 relating to production of the series. Digitized copies of many of the sound and video recordings in this collection, as well as some of Friedman's writings, are available at http://miltonfriedman.hoover.org . Creator: Friedman, Milton, 1912-2006 Creator: Penn Communications Creator: WQLN (Television station : Erie, Pa.) Hoover Institution Library & Archives Access The collection is open for research; materials must be requested at least two business days in advance of intended use. Publication Rights For copyright status, please contact the Hoover Institution Library & Archives. Acquisition Information Acquired by the Hoover Institution Library & Archives in 1980, with increments received in 1988 and 1989. -

Some Unpleasant Monetarist Arithmetic Thomas Sargent, ,, ^ Neil Wallace (P

Federal Reserve Bank of Minneapolis Quarterly Review Some Unpleasant Monetarist Arithmetic Thomas Sargent, ,, ^ Neil Wallace (p. 1) District Conditions (p.18) Federal Reserve Bank of Minneapolis Quarterly Review vol. 5, no 3 This publication primarily presents economic research aimed at improving policymaking by the Federal Reserve System and other governmental authorities. Produced in the Research Department. Edited by Arthur J. Rolnick, Richard M. Todd, Kathleen S. Rolfe, and Alan Struthers, Jr. Graphic design and charts drawn by Phil Swenson, Graphic Services Department. Address requests for additional copies to the Research Department. Federal Reserve Bank, Minneapolis, Minnesota 55480. Articles may be reprinted if the source is credited and the Research Department is provided with copies of reprints. The views expressed herein are those of the authors and not necessarily those of the Federal Reserve Bank of Minneapolis or the Federal Reserve System. Federal Reserve Bank of Minneapolis Quarterly Review/Fall 1981 Some Unpleasant Monetarist Arithmetic Thomas J. Sargent Neil Wallace Advisers Research Department Federal Reserve Bank of Minneapolis and Professors of Economics University of Minnesota In his presidential address to the American Economic in at least two ways. (For simplicity, we will refer to Association (AEA), Milton Friedman (1968) warned publicly held interest-bearing government debt as govern- not to expect too much from monetary policy. In ment bonds.) One way the public's demand for bonds particular, Friedman argued that monetary policy could constrains the government is by setting an upper limit on not permanently influence the levels of real output, the real stock of government bonds relative to the size of unemployment, or real rates of return on securities. -

Forms of Government

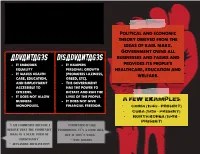

communism An economic ideology Political and economic theory derived from the ideas of karl marx. Government owns all Advantages DISAdvantages businesses and farms and - It embodies - It hampers provides its people's equality personal growth healthcare, education and - It makes health (promotes laziness, welfare. care, education, greed, etc). and employment - The government accessible to has the power to citizens. dictate and run the - It does not allow lives of the people. business - It does not give A Few Examples: monopolies. financial freedom. - China (1949 – Present) - Cuba (1959 – Present) - North Korea (1948 – Present) “I am communist because I “Communism is like believe that the comMunist prohibition. It’s a good idea, ideal is a state form of but it won’t work.” christianity” - will Rogers - Alexander Zhuravlyovv Socialism Government owns many of An Economic Ideology the larger industries and provide education, health and welfare services while Advantages DISAdvantages allowing citizens some - There is a balance - Bureaucracy hampers economic choices between wealth and the delivery of earnings services. - There is equal access - People are to health care and unmotivated to A Few Examples: education develop Vietnam - It breaks down social entrepreneurial skills. Laos barriers - The government has Denmark too much control Finland “The meaning of peace is “Socialism is workable only the absence of opposition to in heaven where it isn’t need socialism” and in where they’ve got it.” - Karl Marx - Cecil Palmer Capitalism Free-market -

Liberty, Property and Rationality

Liberty, Property and Rationality Concept of Freedom in Murray Rothbard’s Anarcho-capitalism Master’s Thesis Hannu Hästbacka 13.11.2018 University of Helsinki Faculty of Arts General History Tiedekunta/Osasto – Fakultet/Sektion – Faculty Laitos – Institution – Department Humanistinen tiedekunta Filosofian, historian, kulttuurin ja taiteiden tutkimuksen laitos Tekijä – Författare – Author Hannu Hästbacka Työn nimi – Arbetets titel – Title Liberty, Property and Rationality. Concept of Freedom in Murray Rothbard’s Anarcho-capitalism Oppiaine – Läroämne – Subject Yleinen historia Työn laji – Arbetets art – Level Aika – Datum – Month and Sivumäärä– Sidoantal – Number of pages Pro gradu -tutkielma year 100 13.11.2018 Tiivistelmä – Referat – Abstract Murray Rothbard (1926–1995) on yksi keskeisimmistä modernin libertarismin taustalla olevista ajattelijoista. Rothbard pitää yksilöllistä vapautta keskeisimpänä periaatteenaan, ja yhdistää filosofiassaan klassisen liberalismin perinnettä itävaltalaiseen taloustieteeseen, teleologiseen luonnonoikeusajatteluun sekä individualistiseen anarkismiin. Hänen tavoitteenaan on kehittää puhtaaseen järkeen pohjautuva oikeusoppi, jonka pohjalta voidaan perustaa vapaiden markkinoiden ihanneyhteiskunta. Valtiota ei täten Rothbardin ihanneyhteiskunnassa ole, vaan vastuu yksilöllisten luonnonoikeuksien toteutumisesta on kokonaan yksilöllä itsellään. Tutkin työssäni vapauden käsitettä Rothbardin anarko-kapitalistisessa filosofiassa. Selvitän ja analysoin Rothbardin ajattelun keskeisimpiä elementtejä niiden filosofisissa, -

Free to Choose

June 9, 2005 COMMENTARY Free to Choose By MILTON FRIEDMAN June 9, 2005; Page A16 Little did I know when I published an article in 1955 on "The Role of Government in Education" that it would lead to my becoming an activist for a major reform in the organization of schooling, and indeed that my wife and I would be led to establish a foundation to promote parental choice. The original article was not a reaction to a perceived deficiency in schooling. The quality of schooling in the United States then was far better than it is now, and both my wife and I were satisfied with the public schools we had attended. My interest was in the philosophy of a free society. Education was the area that I happened to write on early. I then went on to consider other areas as well. The end result was "Capitalism and Freedom," published seven years later with the education article as one chapter. With respect to education, I pointed out that government was playing three major roles: (1) legislating compulsory schooling, (2) financing schooling, (3) administering schools. I concluded that there was some justification for compulsory schooling and the financing of schooling, but "the actual administration of educational institutions by the government, the 'nationalization,' as it were, of the bulk of the 'education industry' is much more difficult to justify on [free market] or, so far as I can see, on any other grounds." Yet finance and administration "could readily be separated. Governments could require a minimum of schooling financed by giving the parents vouchers redeemable for a given sum per child per year to be spent on purely educational services. -

Friedman's Monetary Framework

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by Research Papers in Economics Friedman’s Monetary Framework: Some Lessons Ben S. Bernanke t is an honor and a pleasure to have this opportunity, on the anniversary of Milton and Rose Friedman’s popular classic, Free to Choose, to speak on I Milton Friedman’s monetary framework and his contributions to the theory and practice of monetary policy. About a year ago, I also had the honor, at a conference at the University of Chicago in honor of Milton’s ninetieth birthday, to discuss the contribution of Friedman’s classic 1963 work with Anna Schwartz, A Monetary History of the United States.1 I mention this earlier talk not only to indicate that I am ready and willing to praise Friedman’s contributions wherever and whenever anyone will give me a venue but also because of the critical influ- ence of A Monetary History on both Friedman’s own thought and on the views of a generation of monetary policymakers. In their Monetary History, Friedman and Schwartz reviewed nearly a cen- tury of American monetary experience in painstaking detail, providing an his- torical analysis that demonstrated the importance of monetary forces in the economy far more convincingly than any purely theoretical or even economet- ric analysis could ever do. Friedman’s close attention to the lessons of history for economic policy is an aspect of his approach to economics that I greatly admire. Milton has never been a big fan of government licensing of profession- als, but maybe he would make an exception in the case of monetary policy- makers. -

Is Neoliberalism Consistent with Individual Liberty? Friedman, Hayek and Rand on Education Employment and Equality

International Journal of Teaching and Education Vol. IV, No. 4 / 2016 DOI: 10.20472/TE.2016.4.4.003 IS NEOLIBERALISM CONSISTENT WITH INDIVIDUAL LIBERTY? FRIEDMAN, HAYEK AND RAND ON EDUCATION EMPLOYMENT AND EQUALITY IRIT KEYNAN Abstract: In their writings, Milton Friedman, Friedrich August von Hayek and Ayn Rand have been instrumental in shaping and influencing neoliberalism through their academic and literary abilities. Their opinions on education, employment and inequality have stirred up considerable controversy and have been the focus of many debates. This paper adds to the debate by suggesting that there is an internal inconsistency in the views of neoliberalism as reflected by Friedman, Hayek and Rand. The paper contends that whereas their neoliberal theories promote liberty, the manner in which they conceptualize this term promotes policies that would actually deny the individual freedom of the majority while securing liberty and financial success for the privileged few. The paper focuses on the consequences of neoliberalism on education, and also discusses how it affects employment, inequality and democracy. Keywords: Neoliberalism; liberty; free market; equality; democracy; social justice; education; equal opportunities; Conservativism JEL Classification: B20, B31, P16 Authors: IRIT KEYNAN, College for Academic Studies, Israel, Email: [email protected] Citation: IRIT KEYNAN (2016). Is neoliberalism consistent with individual liberty? Friedman, Hayek and Rand on education employment and equality. International Journal of Teaching and Education, Vol. IV(4), pp. 30-47., 10.20472/TE.2016.4.4.003 Copyright © 2016, IRIT KEYNAN, [email protected] 30 International Journal of Teaching and Education Vol. IV, No. 4 / 2016 I. Introduction Neoliberalism gradually emerged as a significant ideology during the twentieth century, in response to the liberal crisis of the 1930s. -

100 Years Since the Birth of Milton Friedman Marek Loužek 1

REVIEW OF ECONOMIC PERSPECTIVES – NÁRODOHOSPODÁ ŘSKÝ OBZOR, VOL. 12, ISSUE 3, 2012, pp. 185–203 , DOI: 10.2478/v10135-012-0008-4 100 Years since the Birth of Milton Friedman Marek Loužek 1 Abstract: The paper deals with the economic theory of Milton Friedman. Its first part outlines the life of Milton Friedman. The second part examines his economic theories – “Essays in Positive Economics” (1953), “Studies in the Quantity Theory of Money“ (1956), “A Theory of the Consumption Function” (1957), “A Program for Monetary Stability” (1959), “A Monetary History of the United States 1897 to 1960” (1963), and “Price Theory” (1976). His Nobel Prize lecture and American Economic Association lecture in 1967 are discussed, too. The third part analyzes Friedman’s methodology. Milton Friedman was the most influential economist of the second half of the 20th century. He is best known for his theoretical and empirical research, especially consumption analysis, monetary history and theory, and for his demonstration of the complexity of stabilization policy. Key words: Chicago School of Economics, Milton Friedman, monetarism, quantitative theory of money, theory of consumption function JEL Classification: B212, B31, E40, N10, 011 Milton Friedman was born one hundred years ago, which gives us an opportunity to commemorate this famous economist who has become a legend of economic theory indeed, and with his permanent income hypothesis, foundation of monetarism and the methodology of positive economics will forever be an inseparable part of economic theory. Why was Friedman’s economics such a revolutionary one, and why can we still learn much from him? Milton Friedman’s work is vivid and encompasses a broad scale, from highly expert and technical essays, to popular articles published in Newsweek, and to political- philosophical books. -

To: University of Texas Faculty From: Andrew Koppelman This Workshop

To: University of Texas faculty From: Andrew Koppelman This workshop paper is the introduction and first chapter of a book in progress. It runs a little long. For those pressed for time, please focus on pp. 3-17, 46-47, and 52-61. The Corruption of Libertarianism: How a Philosophy of Freedom was Betrayed by Delusion and Greed Andrew Koppelman* Draft: Aug. 22, 2019 Please do not cite or quote Introduction.............................................. 3 Libertarian political philosophy has produced astonishing cruelty ...................................................... 3 But its best known form is a corrupted variant ............... 6 It began as a plea for freedom and prosperity ................ 8 And now takes multiple forms ................................. 9 some of them not very nice .................................. 10 Hayek has something valuable to offer today’s debates about inequality .................................................. 13 Unlike the delusionary romanticism of Murray Rothbard, Robert Nozick, and Ayn Rand ........................................ 15 Libertarianism is vulnerable to corruption .................. 17 And even in its most attractive form, it is an inadequate political philosophy, and points beyond itself .............. 20 Chapter One: Prosperity.................................. 23 In the 1930s, almost everyone wanted central economic planning ............................................................ 23 Modern libertarianism was born with Hayek’s protest against that idea ................................................... 25 * John Paul Stevens Professor of Law and Professor (by courtesy) of Political Science, Department of Philosophy Affiliated Faculty, Northwestern University. Please send comments, correction of errors, and grievances to [email protected]. 1 Hayek introduced the idea of markets as a way to cope with too much information – more than any planner could know ......... 27 And thought that, if the human race was going to become less poor, undeserved inequality had to be accepted ............. -

Milton Friedman,Adaptive Expectations,Permanent Income

Discuss this article at Journaltalk: http://journaltalk.net/articles/5802 ECON JOURNAL WATCH 10(2) May 2013: 180-183 Mistah Friedman? He Dead. James K. Galbraith1 LINK TO ABSTRACT I knew Milton Friedman slightly. We met on three occasions. Once was at my parents’ home in Cambridge in the late 1970s, to my surprise since I didn’t suspect that my father and he were on speaking terms. Once was by happenstance at Alta in 1983; we skied together for three days. And once in 1990 he invited me to debate, along with David Brooks, for the re-release of the first hour of Free to Choose. I think there were two Milton Friedmans. One was an economist in the Age of Keynes, but in that special enclave, Chicago, which rejected every part of the New Deal including the Wagner Act, Social Security, public works and jobs programs, and also the early postwar resolve that “maximum employment, production and purchasing power” should be our national goal. In those years, too, Swedish social democracy and the British move to national health care were models, the next big thing in many American eyes. In protected isolation and non- conformity, Chicago rejected them all. At that moment, Friedman’s genius lay in his line of attack. He did not reject Keynesian models outright; rather he probed for vulnerability to clever modification. Though he had published essays tying economics to logical pos- itivism, hypothesis testing and evidence had nothing to do with his method here, which was that of the pure thought experiment. Two episodes stand out in memory: those of the permanent income hypothesis and the effect of adaptive expectations on the Phillips curve. -

Milton Friedman's Contributions to Macroeconomics and Teir Influence

A Service of Leibniz-Informationszentrum econstor Wirtschaft Leibniz Information Centre Make Your Publications Visible. zbw for Economics Laidler, David Working Paper Milton Friedman's contributions to macroeconomics and teir Influence EPRI Working Paper, No. 2012-2 Provided in Cooperation with: Economic Policy Research Institute (EPRI), Department of Economics, University of Western Ontario Suggested Citation: Laidler, David (2012) : Milton Friedman's contributions to macroeconomics and teir Influence, EPRI Working Paper, No. 2012-2, The University of Western Ontario, Economic Policy Research Institute (EPRI), London (Ontario) This Version is available at: http://hdl.handle.net/10419/70286 Standard-Nutzungsbedingungen: Terms of use: Die Dokumente auf EconStor dürfen zu eigenen wissenschaftlichen Documents in EconStor may be saved and copied for your Zwecken und zum Privatgebrauch gespeichert und kopiert werden. personal and scholarly purposes. Sie dürfen die Dokumente nicht für öffentliche oder kommerzielle You are not to copy documents for public or commercial Zwecke vervielfältigen, öffentlich ausstellen, öffentlich zugänglich purposes, to exhibit the documents publicly, to make them machen, vertreiben oder anderweitig nutzen. publicly available on the internet, or to distribute or otherwise use the documents in public. Sofern die Verfasser die Dokumente unter Open-Content-Lizenzen (insbesondere CC-Lizenzen) zur Verfügung gestellt haben sollten, If the documents have been made available under an Open gelten abweichend von diesen Nutzungsbedingungen -

The Essential MILTON FRIEDMAN FRIEDMAN

The Essential MILTON The Essential MILTON FRIEDMAN FRIEDMAN Milton Friedman was one of the most influential economists The Essential of all time. He revolutionized the way economists think about consumption, about money, about stabilization policy, and about unemployment. He demonstrated the power of committing oneself to a few simple assumptions about human behaviour and then relentlessly pursuing their logical implications. He developed and taught new ways of interpreting data, testing his theories by their MILTON ability to explain multiple disparate phenomena. His successes were spectacular and his techniques were widely emulated. But Friedman’s influence extended beyond economists. To the public at large, he was the world’s foremost advocate for economic and FRIEDMAN personal freedom. In the United States, he helped to end the military draft, to broaden educational choice, and to change the regulatory climate. Worldwide, almost all central banks now follow policies that are grounded in Friedman’s insights and recommendations. This book briefly summarizes Friedman’s extraordinary contributions to economic theory, Landsburg Steven economic practice, economic policy, and economic literacy. 978-0-88975-542-0 by Steven Landsburg The Essential Milton Friedman by Steven E. Landsburg Fraser Institute www.fraserinstitute.org Copyright © by the Fraser Institute. All rights reserved. No part of this book may be reproduced in any manner whatsoever without written permission except in the case of brief quotations embodied in critical articles and reviews. Th e author of this publication has worked independently and opinions expressed by him are, therefore, his own, and do not necessarily refl ect the opinions of the Fraser Institute or its supporters, directors, or staff .