Some Unpleasant Monetarist Arithmetic Thomas Sargent, ,, ^ Neil Wallace (P

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

REP21 December 1974

World Bank Reprint Series: Number Twenty-one REP21 December 1974 Public Disclosure Authorized V.V. Bhatt Some Aspects of Financial Policies and Central Banking in Developing Countries Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Reprinted from World Development 2 (October-December 1974) World Development Vol.2, No.10-12, October-Deceinber 1974, pp. 59-67 59 Some Aspects of Financial Policies and Central Banking in Developing Countries V. V. BHATT Economic Development Institute of the International Bank for Reconstruction and Development mechanism and agency as provided by the existence of a Central Bank. What needs special emphasis at an international level is the rationale and urgency of evolving a sound financial structure through the efficient performance of the twin interrelated functions-as promoters and as regulators of the financial system-by Central Banks. 1. SOME ASPECTS OF FINANCIAL POLICIES .. ~~~The main object of this Section is to show the Economic development is not only facilitated but its . pace is quickened by the appropriate development of the significance of saving and flow-of-funds analysis as an financial system--structure of financial institutions, indicator of a set of financial policies-policies relating instruments and interest rates.1 to the structure of financial institutions, instruments and Instrumentsand interest rates.r interest rates-essential for resource mobilization and In any strategy of development, therefore, it is allocation consistent with a country's development essential to emphasize the evolution of a sound and . 6 c well-integrated financial system from the point of view objectives. In a large number of developing countries, the only both of resource mobilization and efficient allocation.2 reliable data available for understanding the trends in the In Section I of this paper, an attempt is made to economy and for policy purposes relate to monetary delineate the broad contours of a set of financial policies flows and the balance of payments. -

Saving in a Financial Institution

SAVING IN A FINANCIAL INSTITUTION i Silverback Consultants Ltd acknowledges the contributions of: Somkwe John-Nwosu Chinyere Agwu Nene Williams Temiloluwa Bamigbola The Consumer Protection Department of The Central Bank of Nigeria. Hajiya Khadijah Kasim Edited by Hajiya Umma Dutse Copyright © 2017 All rights reserved. No part of this publication may be reproduced, distributed, or transmitted in any form or by any means, including photocopying, recording, or other electronic or mechanical methods, without the prior written permission of the publisher, except in the case of brief quotations embodied in critical reviews and certain other non-commercial uses permitted by copyright law. ISBN This material was produced by the Consumer Protection Department of the Central Bank of Nigeria in Collaboration with Silverback Consultants Ltd. 1 01 Introduction 02 Importance of Saving 03 Where to Save Saving at Home (Advantages and Disadvantages) Saving in a Bank and Other Financial Institutions Types of Banks and Other Financial Institutions 04 How to Save What to Consider in Choosing a Bank or Other Financial Institutions Types of Accounts Operating Bank Accounts Electronic Payment Channels 05 Managing Accounts Reconciling Account Complaints Protecting Banking Instruments Protecting Electronic Transactions Rights and Responsibilities of a Bank Customer 06 Conclusion 07 Frequently Used Banking Terms 2 01. Introduction Almost everyone has an idea of what is saving and must have saved in one form or another. This could be towards buying something needed or towards a future project such as building a house, paying school fees, marriage, hospital bills, repay loans or simply for a rainy day. People set aside certain amounts or engage in contributions (esusu, adashe). -

Free to Choose Video Tape Collection

http://oac.cdlib.org/findaid/ark:/13030/kt1n39r38j No online items Inventory to the Free to Choose video tape collection Finding aid prepared by Natasha Porfirenko Hoover Institution Library and Archives © 2008 434 Galvez Mall Stanford University Stanford, CA 94305-6003 [email protected] URL: http://www.hoover.org/library-and-archives Inventory to the Free to Choose 80201 1 video tape collection Title: Free to Choose video tape collection Date (inclusive): 1977-1987 Collection Number: 80201 Contributing Institution: Hoover Institution Library and Archives Language of Material: English Physical Description: 10 manuscript boxes, 10 motion picture film reels, 42 videoreels(26.6 Linear Feet) Abstract: Motion picture film, video tapes, and film strips of the television series Free to Choose, featuring Milton Friedman and relating to laissez-faire economics, produced in 1980 by Penn Communications and television station WQLN in Erie, Pennsylvania. Includes commercial and master film copies, unedited film, and correspondence, memoranda, and legal agreements dated from 1977 to 1987 relating to production of the series. Digitized copies of many of the sound and video recordings in this collection, as well as some of Friedman's writings, are available at http://miltonfriedman.hoover.org . Creator: Friedman, Milton, 1912-2006 Creator: Penn Communications Creator: WQLN (Television station : Erie, Pa.) Hoover Institution Library & Archives Access The collection is open for research; materials must be requested at least two business days in advance of intended use. Publication Rights For copyright status, please contact the Hoover Institution Library & Archives. Acquisition Information Acquired by the Hoover Institution Library & Archives in 1980, with increments received in 1988 and 1989. -

How the Rational Expectations Revolution Has Enriched

How the Rational Expectations Revolution Has Changed Macroeconomic Policy Research by John B. Taylor STANFORD UNIVERSITY Revised Draft: February 29, 2000 Written versions of lecture presented at the 12th World Congress of the International Economic Association, Buenos Aires, Argentina, August 24, 1999. I am grateful to Jacques Dreze for helpful comments on an earlier draft. The rational expectations hypothesis is by far the most common expectations assumption used in macroeconomic research today. This hypothesis, which simply states that people's expectations are the same as the forecasts of the model being used to describe those people, was first put forth and used in models of competitive product markets by John Muth in the 1960s. But it was not until the early 1970s that Robert Lucas (1972, 1976) incorporated the rational expectations assumption into macroeconomics and showed how to make it operational mathematically. The “rational expectations revolution” is now as old as the Keynesian revolution was when Robert Lucas first brought rational expectations to macroeconomics. This rational expectations revolution has led to many different schools of macroeconomic research. The new classical economics school, the real business cycle school, the new Keynesian economics school, the new political macroeconomics school, and more recently the new neoclassical synthesis (Goodfriend and King (1997)) can all be traced to the introduction of rational expectations into macroeconomics in the early 1970s (see the discussion by Snowden and Vane (1999), pp. 30-50). In this lecture, which is part of the theme on "The Current State of Macroeconomics" at the 12th World Congress of the International Economic Association, I address a question that I am frequently asked by students and by "non-macroeconomist" colleagues, and that I suspect may be on many people's minds. -

Interest Rates and Expected Inflation: a Selective Summary of Recent Research

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Explorations in Economic Research, Volume 3, number 3 Volume Author/Editor: NBER Volume Publisher: NBER Volume URL: http://www.nber.org/books/sarg76-1 Publication Date: 1976 Chapter Title: Interest Rates and Expected Inflation: A Selective Summary of Recent Research Chapter Author: Thomas J. Sargent Chapter URL: http://www.nber.org/chapters/c9082 Chapter pages in book: (p. 1 - 23) 1 THOMAS J. SARGENT University of Minnesota Interest Rates and Expected Inflation: A Selective Summary of Recent Research ABSTRACT: This paper summarizes the macroeconomics underlying Irving Fisher's theory about tile impact of expected inflation on nomi nal interest rates. Two sets of restrictions on a standard macroeconomic model are considered, each of which is sufficient to iniplv Fisher's theory. The first is a set of restrictions on the slopes of the IS and LM curves, while the second is a restriction on the way expectations are formed. Selected recent empirical work is also reviewed, and its implications for the effect of inflation on interest rates and other macroeconomic issues are discussed. INTRODUCTION This article is designed to pull together and summarize recent work by a few others and myself on the relationship between nominal interest rates and expected inflation.' The topic has received much attention in recent years, no doubt as a consequence of the high inflation rates and high interest rates experienced by Western economies since the mid-1960s. NOTE: In this paper I Summarize the results of research 1 conducted as part of the National Bureaus study of the effects of inflation, for which financing has been provided by a grait from the American life Insurance Association Heiptul coinrnents on earlier eriiins of 'his p,irx'r serv marIe ti PhillipCagan arid l)y the mnibrirs Ut the stall reading Committee: Michael R. -

Forms of Government

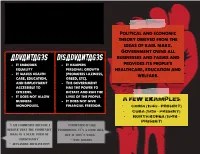

communism An economic ideology Political and economic theory derived from the ideas of karl marx. Government owns all Advantages DISAdvantages businesses and farms and - It embodies - It hampers provides its people's equality personal growth healthcare, education and - It makes health (promotes laziness, welfare. care, education, greed, etc). and employment - The government accessible to has the power to citizens. dictate and run the - It does not allow lives of the people. business - It does not give A Few Examples: monopolies. financial freedom. - China (1949 – Present) - Cuba (1959 – Present) - North Korea (1948 – Present) “I am communist because I “Communism is like believe that the comMunist prohibition. It’s a good idea, ideal is a state form of but it won’t work.” christianity” - will Rogers - Alexander Zhuravlyovv Socialism Government owns many of An Economic Ideology the larger industries and provide education, health and welfare services while Advantages DISAdvantages allowing citizens some - There is a balance - Bureaucracy hampers economic choices between wealth and the delivery of earnings services. - There is equal access - People are to health care and unmotivated to A Few Examples: education develop Vietnam - It breaks down social entrepreneurial skills. Laos barriers - The government has Denmark too much control Finland “The meaning of peace is “Socialism is workable only the absence of opposition to in heaven where it isn’t need socialism” and in where they’ve got it.” - Karl Marx - Cecil Palmer Capitalism Free-market -

A Primer on Modern Monetary Theory

2021 A Primer on Modern Monetary Theory Steven Globerman fraserinstitute.org Contents Executive Summary / i 1. Introducing Modern Monetary Theory / 1 2. Implementing MMT / 4 3. Has Canada Adopted MMT? / 10 4. Proposed Economic and Social Justifications for MMT / 17 5. MMT and Inflation / 23 Concluding Comments / 27 References / 29 About the author / 33 Acknowledgments / 33 Publishing information / 34 Supporting the Fraser Institute / 35 Purpose, funding, and independence / 35 About the Fraser Institute / 36 Editorial Advisory Board / 37 fraserinstitute.org fraserinstitute.org Executive Summary Modern Monetary Theory (MMT) is a policy model for funding govern- ment spending. While MMT is not new, it has recently received wide- spread attention, particularly as government spending has increased dramatically in response to the ongoing COVID-19 crisis and concerns grow about how to pay for this increased spending. The essential message of MMT is that there is no financial constraint on government spending as long as a country is a sovereign issuer of cur- rency and does not tie the value of its currency to another currency. Both Canada and the US are examples of countries that are sovereign issuers of currency. In principle, being a sovereign issuer of currency endows the government with the ability to borrow money from the country’s cen- tral bank. The central bank can effectively credit the government’s bank account at the central bank for an unlimited amount of money without either charging the government interest or, indeed, demanding repayment of the government bonds the central bank has acquired. In 2020, the cen- tral banks in both Canada and the US bought a disproportionately large share of government bonds compared to previous years, which has led some observers to argue that the governments of Canada and the United States are practicing MMT. -

Modern Monetary Theory: a Marxist Critique

Class, Race and Corporate Power Volume 7 Issue 1 Article 1 2019 Modern Monetary Theory: A Marxist Critique Michael Roberts [email protected] Follow this and additional works at: https://digitalcommons.fiu.edu/classracecorporatepower Part of the Economics Commons Recommended Citation Roberts, Michael (2019) "Modern Monetary Theory: A Marxist Critique," Class, Race and Corporate Power: Vol. 7 : Iss. 1 , Article 1. DOI: 10.25148/CRCP.7.1.008316 Available at: https://digitalcommons.fiu.edu/classracecorporatepower/vol7/iss1/1 This work is brought to you for free and open access by the College of Arts, Sciences & Education at FIU Digital Commons. It has been accepted for inclusion in Class, Race and Corporate Power by an authorized administrator of FIU Digital Commons. For more information, please contact [email protected]. Modern Monetary Theory: A Marxist Critique Abstract Compiled from a series of blog posts which can be found at "The Next Recession." Modern monetary theory (MMT) has become flavor of the time among many leftist economic views in recent years. MMT has some traction in the left as it appears to offer theoretical support for policies of fiscal spending funded yb central bank money and running up budget deficits and public debt without earf of crises – and thus backing policies of government spending on infrastructure projects, job creation and industry in direct contrast to neoliberal mainstream policies of austerity and minimal government intervention. Here I will offer my view on the worth of MMT and its policy implications for the labor movement. First, I’ll try and give broad outline to bring out the similarities and difference with Marx’s monetary theory. -

Perceived Financial Preparedness, Saving Habits, and Financial Security CFPB Office of Research

Perceived Financial Preparedness, Saving Habits, and Financial Security CFPB Office of Research SEPTEMBER 2020 The Consumer Financial Protection Bureau’s (CFPB, the Bureau) Start Small, Save Up initiative aims to promote the importance of building a basic savings cushion and saving habits among U.S. consumers as a pathway to increased financial well-being and financial security.1 Having a savings cushion or a habit of saving can help consumers feel more in control of their finances and allow them to weather financial shocks more easily. Indeed, previous research shows that many consumers experience financial shocks, and that savings can help buffer against shocks and provide financial security.2 Further, previous research has also found a relationship between savings and financial well-being that suggests that having savings can help consumers feel more financially secure.3 This brief uses data from the Bureau’s Making Ends Meet survey to explore consumers’ savings- related behaviors, experiences, and outcomes. We examine subjective experiences primarily as they relate to financial well-being and feelings of control over finances,4 while consumers’ objective financial situations are explored using self-reported responses to questions about difficulty paying bills, saving habits, and money in checking and savings accounts. Focusing on these and other financial factors, such as income, allows us to better understand how consumers 1 This Office of Research research brief (No. 2020-2) was written by Caroline Ratcliffe, Melissa Knoll, Leah Kazar, Maxwell Kennady, and Marie Rush. 2 McKernan, Ratcliffe, Kalish, and Braga (2016); Mills et al. (2016); Mills et al. (2019); Ratcliffe, Burke, Gardner, and Knoll (2020). -

The-Great-Depression-Glossary.Pdf

The Great Depression | Glossary of Terms Glossary of Terms Balanced budget – Government revenues equal expenditures on an annual basis. (Lesson 5) Bank failure – When a bank’s liabilities (mainly deposits) exceed the value of its assets. (Lesson 3) Bank panic – When a bank run begins at one bank and spreads to others, causing people to lose confidence in banks. (Lesson 3) Bank reserves – The sum of cash that banks hold in their vaults and the deposits they maintain with Federal Reserve banks. (Lesson 3) Bank run – When many depositors rush to the bank to withdraw their money at the same time. (Lesson 3) Bank suspensions – Comprises all banks closed to the public, either temporarily or permanently, by supervisory authorities or by the banks’ boards of directors because of financial difficulties. Banks that close under a special holiday declaration and remained closed only during the designated holiday are not counted as suspensions. (Lesson 4) Banks – Businesses that accept deposits and make loans. (Lesson 2) Budget deficit – When government expenditures exceed revenues. (Lesson 4) Budget surplus – When government revenues exceed expenditures. (Lesson 4) Consumer confidence – The relationship between how consumers feel about the economy and their spending and saving decisions. (Lesson 5) Consumer Price Index (CPI) – A measure of the prices paid by urban consumers for a market basket of consumer goods and services. (Lesson 1) Deflation – A general downward movement of prices for goods and services in an economy. (Lessons 1, 3 and 6) Depression – A very severe recession; a period of severely declining economic activity spread across the economy (not limited to particular sectors or regions) normally visible in a decline in real GDP, real income, employment, industrial production, wholesale-retail credit and the loss of overall confidence in the economy. -

Liberty, Property and Rationality

Liberty, Property and Rationality Concept of Freedom in Murray Rothbard’s Anarcho-capitalism Master’s Thesis Hannu Hästbacka 13.11.2018 University of Helsinki Faculty of Arts General History Tiedekunta/Osasto – Fakultet/Sektion – Faculty Laitos – Institution – Department Humanistinen tiedekunta Filosofian, historian, kulttuurin ja taiteiden tutkimuksen laitos Tekijä – Författare – Author Hannu Hästbacka Työn nimi – Arbetets titel – Title Liberty, Property and Rationality. Concept of Freedom in Murray Rothbard’s Anarcho-capitalism Oppiaine – Läroämne – Subject Yleinen historia Työn laji – Arbetets art – Level Aika – Datum – Month and Sivumäärä– Sidoantal – Number of pages Pro gradu -tutkielma year 100 13.11.2018 Tiivistelmä – Referat – Abstract Murray Rothbard (1926–1995) on yksi keskeisimmistä modernin libertarismin taustalla olevista ajattelijoista. Rothbard pitää yksilöllistä vapautta keskeisimpänä periaatteenaan, ja yhdistää filosofiassaan klassisen liberalismin perinnettä itävaltalaiseen taloustieteeseen, teleologiseen luonnonoikeusajatteluun sekä individualistiseen anarkismiin. Hänen tavoitteenaan on kehittää puhtaaseen järkeen pohjautuva oikeusoppi, jonka pohjalta voidaan perustaa vapaiden markkinoiden ihanneyhteiskunta. Valtiota ei täten Rothbardin ihanneyhteiskunnassa ole, vaan vastuu yksilöllisten luonnonoikeuksien toteutumisesta on kokonaan yksilöllä itsellään. Tutkin työssäni vapauden käsitettä Rothbardin anarko-kapitalistisessa filosofiassa. Selvitän ja analysoin Rothbardin ajattelun keskeisimpiä elementtejä niiden filosofisissa, -

Inter-Relationship Between Economic Growth, Savings and Inflation in Asia

Inter-Relationship between Economic Growth, Savings and Inflation in Asia 著者 Chaturvedi Vaibhav, Kumar Brajesh, Dholakia Ravindra H. 出版者 Institute of Comparative Economic Studies, Hosei University journal or Journal of International Economic Studies publication title volume 23 page range 1-22 year 2009-03 URL http://hdl.handle.net/10114/3628 Journal of International Economic Studies (2009), No.23, 1–22 ©2009 The Institute of Comparative Economic Studies, Hosei University INTER-RELATIONSHIP BETWEEN ECONOMIC GROWTH, SAVINGS AND INFLATION IN ASIA Vaibhav Chaturvedi 1 Brajesh Kumar 2 Ravindra H. Dholakia 3 Abstract The present study examines the inter- relationship between economic growth, saving rate and inflation for south-east and south Asia in a simultaneous equation framework using two stage least squares with panel data. The relationship between saving rate and growth has been found to be bi-directional and positive. Inflation has a highly significant negative effect on growth but positive effect on saving rate. Inflation is not affected by growth but is largely determined by its past values, and saving rate is not affected by interest rate. These findings for countries in Asia with widely divergent values of aggregates are very relevant for develop- ment policies and strategies4. JEL classification: C33; E21; E31; E60; O57 Keywords: Growth; Savings; Inflation; Asia; Simultaneity; Fixed-Effect 1. Introduction Growth experience in south-east and south Asia has generated keen interest among econ- omists and policy makers for the last two decades. Numerous macroeconomic factors affect- ing economic growth like inflation, savings, foreign exchange rate, etc. have widely varying values across these nations and so also their economic growth.