Practical Activity. “The Great Depression.”

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Franklin Delano Roosevelt

FRANKLIN DELANO ROOSEVELT Franklin D.Roosevelt was born on january 30th 1882, in Hyde Park(in new york state) and died on april 12th 1945 in Warm Spring(in Georgia). He was the president of the united states on november 8th 1932 and he was reelected four times: -he was elected in novenber 8th 1932; -in november 3th 1936; -in november 5th 1940; -in november 7th 1944. Franklin D. Roosevelt signed the declaration war versus the japonese and the nazi(who occupated France) in 1941. Franklin D. Roosevelt was ill in the campobello island. Roosevelt was paralysed and he was in a wheelchair or he walked with a canne. He signed a program to relaunch the economic system of America named the"new deal" HIS LIFE BEFORE HE WAS A PRESIDENT: Before being presidents he was: -gouverner of new york states -adjoint secretarie of the marine -he founding the United States Navy Reserve -Vice president of United States -Vice president of sell society -Director of avocates cabinet affaires Franklin D. Roosevelt was married with eleanore Roosevelt the march 17,1905 and they had five children: -Anna Eleanor (1906 – 1975) -James (1907 – 1991) -Franklin Delano Jr. (3 mars 1909 – 7 novembre 1909) -Elliott (1910 – 1990) -Franklin Delano, Jr. (1914 – 1988) -John Aspinwall (1916 – 1981) When Franklin D. Roosevelt became president: -He signed, in march 9, 1933, the Emergency Banking Act -he signed, in april 5 1933 the Order presidentiel executate 6102 -he signed a seconde New Deal and the welfare state in objective to drop the unenployement in America. -he created the National Foundation for Infantile Paralysis for the children paralyzed members. -

Free to Choose Video Tape Collection

http://oac.cdlib.org/findaid/ark:/13030/kt1n39r38j No online items Inventory to the Free to Choose video tape collection Finding aid prepared by Natasha Porfirenko Hoover Institution Library and Archives © 2008 434 Galvez Mall Stanford University Stanford, CA 94305-6003 [email protected] URL: http://www.hoover.org/library-and-archives Inventory to the Free to Choose 80201 1 video tape collection Title: Free to Choose video tape collection Date (inclusive): 1977-1987 Collection Number: 80201 Contributing Institution: Hoover Institution Library and Archives Language of Material: English Physical Description: 10 manuscript boxes, 10 motion picture film reels, 42 videoreels(26.6 Linear Feet) Abstract: Motion picture film, video tapes, and film strips of the television series Free to Choose, featuring Milton Friedman and relating to laissez-faire economics, produced in 1980 by Penn Communications and television station WQLN in Erie, Pennsylvania. Includes commercial and master film copies, unedited film, and correspondence, memoranda, and legal agreements dated from 1977 to 1987 relating to production of the series. Digitized copies of many of the sound and video recordings in this collection, as well as some of Friedman's writings, are available at http://miltonfriedman.hoover.org . Creator: Friedman, Milton, 1912-2006 Creator: Penn Communications Creator: WQLN (Television station : Erie, Pa.) Hoover Institution Library & Archives Access The collection is open for research; materials must be requested at least two business days in advance of intended use. Publication Rights For copyright status, please contact the Hoover Institution Library & Archives. Acquisition Information Acquired by the Hoover Institution Library & Archives in 1980, with increments received in 1988 and 1989. -

Some Unpleasant Monetarist Arithmetic Thomas Sargent, ,, ^ Neil Wallace (P

Federal Reserve Bank of Minneapolis Quarterly Review Some Unpleasant Monetarist Arithmetic Thomas Sargent, ,, ^ Neil Wallace (p. 1) District Conditions (p.18) Federal Reserve Bank of Minneapolis Quarterly Review vol. 5, no 3 This publication primarily presents economic research aimed at improving policymaking by the Federal Reserve System and other governmental authorities. Produced in the Research Department. Edited by Arthur J. Rolnick, Richard M. Todd, Kathleen S. Rolfe, and Alan Struthers, Jr. Graphic design and charts drawn by Phil Swenson, Graphic Services Department. Address requests for additional copies to the Research Department. Federal Reserve Bank, Minneapolis, Minnesota 55480. Articles may be reprinted if the source is credited and the Research Department is provided with copies of reprints. The views expressed herein are those of the authors and not necessarily those of the Federal Reserve Bank of Minneapolis or the Federal Reserve System. Federal Reserve Bank of Minneapolis Quarterly Review/Fall 1981 Some Unpleasant Monetarist Arithmetic Thomas J. Sargent Neil Wallace Advisers Research Department Federal Reserve Bank of Minneapolis and Professors of Economics University of Minnesota In his presidential address to the American Economic in at least two ways. (For simplicity, we will refer to Association (AEA), Milton Friedman (1968) warned publicly held interest-bearing government debt as govern- not to expect too much from monetary policy. In ment bonds.) One way the public's demand for bonds particular, Friedman argued that monetary policy could constrains the government is by setting an upper limit on not permanently influence the levels of real output, the real stock of government bonds relative to the size of unemployment, or real rates of return on securities. -

Forms of Government

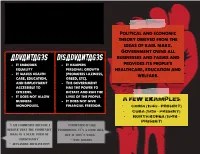

communism An economic ideology Political and economic theory derived from the ideas of karl marx. Government owns all Advantages DISAdvantages businesses and farms and - It embodies - It hampers provides its people's equality personal growth healthcare, education and - It makes health (promotes laziness, welfare. care, education, greed, etc). and employment - The government accessible to has the power to citizens. dictate and run the - It does not allow lives of the people. business - It does not give A Few Examples: monopolies. financial freedom. - China (1949 – Present) - Cuba (1959 – Present) - North Korea (1948 – Present) “I am communist because I “Communism is like believe that the comMunist prohibition. It’s a good idea, ideal is a state form of but it won’t work.” christianity” - will Rogers - Alexander Zhuravlyovv Socialism Government owns many of An Economic Ideology the larger industries and provide education, health and welfare services while Advantages DISAdvantages allowing citizens some - There is a balance - Bureaucracy hampers economic choices between wealth and the delivery of earnings services. - There is equal access - People are to health care and unmotivated to A Few Examples: education develop Vietnam - It breaks down social entrepreneurial skills. Laos barriers - The government has Denmark too much control Finland “The meaning of peace is “Socialism is workable only the absence of opposition to in heaven where it isn’t need socialism” and in where they’ve got it.” - Karl Marx - Cecil Palmer Capitalism Free-market -

History of Federal Reserve Free Edition

Free Digital Edition A Visual History of the Federal Reserve System 1914 - 2009 This is a free digital edition of a chart created by John Paul Koning. It has been designed to be ap- chase. Alternatively, if you have found this chart useful but don’t want to buy a paper edition, con- preciated on paper as a 24x36 inch display. If you enjoy this chart please consider buying the paper sider donating to me at www.financialgraphart.com/donate. It took me many months to compile the version at www.financialgraphart.com. Buyers of the chart will recieve a bonus chart “reimagin- data and design it, any support would be much appreciated. ing” the history of the Fed’s balance sheet. The updated 2010 edition is also now available for pur- John Paul Koning, 2010 FOR BETTER OR FOR WORSE, the Federal Reserve has Multiple data series including the Fed’s balance sheet, This image is published under a Creative Commons been governing the monetary system of the United States interest rates and spreads, reserve requirements, chairmen, How to read this chart: Attribution-Noncommercial-No Derivative Works 2.5 License since 1914. This chart maps the rise of the Fed from its inflation, recessions, and more help chronicle this rise. While Start origins as a relatively minor institution, often controlled by this chart can only tell part of the complex story of the Fed, 1914-1936 Willliam P. Harding $16 Presidents and the United States Department of the we trust it will be a valuable reference tool to anyone Member, Federal Reserve Board 13b Treasury, into an independent and powerful body that rivals curious about the evolution of this very influential yet Adviser to the Cuban government Benjamin Strong Jr. -

Liberty, Property and Rationality

Liberty, Property and Rationality Concept of Freedom in Murray Rothbard’s Anarcho-capitalism Master’s Thesis Hannu Hästbacka 13.11.2018 University of Helsinki Faculty of Arts General History Tiedekunta/Osasto – Fakultet/Sektion – Faculty Laitos – Institution – Department Humanistinen tiedekunta Filosofian, historian, kulttuurin ja taiteiden tutkimuksen laitos Tekijä – Författare – Author Hannu Hästbacka Työn nimi – Arbetets titel – Title Liberty, Property and Rationality. Concept of Freedom in Murray Rothbard’s Anarcho-capitalism Oppiaine – Läroämne – Subject Yleinen historia Työn laji – Arbetets art – Level Aika – Datum – Month and Sivumäärä– Sidoantal – Number of pages Pro gradu -tutkielma year 100 13.11.2018 Tiivistelmä – Referat – Abstract Murray Rothbard (1926–1995) on yksi keskeisimmistä modernin libertarismin taustalla olevista ajattelijoista. Rothbard pitää yksilöllistä vapautta keskeisimpänä periaatteenaan, ja yhdistää filosofiassaan klassisen liberalismin perinnettä itävaltalaiseen taloustieteeseen, teleologiseen luonnonoikeusajatteluun sekä individualistiseen anarkismiin. Hänen tavoitteenaan on kehittää puhtaaseen järkeen pohjautuva oikeusoppi, jonka pohjalta voidaan perustaa vapaiden markkinoiden ihanneyhteiskunta. Valtiota ei täten Rothbardin ihanneyhteiskunnassa ole, vaan vastuu yksilöllisten luonnonoikeuksien toteutumisesta on kokonaan yksilöllä itsellään. Tutkin työssäni vapauden käsitettä Rothbardin anarko-kapitalistisessa filosofiassa. Selvitän ja analysoin Rothbardin ajattelun keskeisimpiä elementtejä niiden filosofisissa, -

Insights from the Federal Reserve's Weekly Balance Sheet, 1914-1941

SAE./No.73/January 2017 Studies in Applied Economics INSIGHTS FROM THE FEDERAL RESERVE'S WEEKLY BALANCE SHEET, 1914-1941 Justin Chen and Andrew Gibson Johns Hopkins Institute for Applied Economics, Global Health, and Study of Business Enterprise Insights from the Federal Reserve’s Weekly Balance Sheet, 1914-1941 By Justin Chen and Andrew Gibson Copyright 2017 by Justin Chen and Andrew Gibson. This work may be reproduced or adapted provided that no fee is charged and the original source is properly credited. About the Series The Studies in Applied Economics series is under the general direction of Professor Steve H. Hanke, co-director of the Johns Hopkins institute for Applied Economics, Global Health, and the Study of Business Enterprise ([email protected]). The authors are mainly students at The Johns Hopkins University in Baltimore. Some performed their work as research assistants at the Institute. About the Authors Justin Chen ([email protected]) and Andrew Gibson ([email protected]) are students at The Johns Hopkins University in Baltimore, Maryland. Justin is a sophomore pursuing a degree in Computer Science, while Andrew is a junior studying Economics. Both are seeking a minor in Financial Economics. They wrote this paper as undergraduate researchers at the Institute for Applied Economics, Global Health, and the Study of Business Enterprise during Summer 2016. Andrew and Justin will graduate in May 2018 and 2019, respectively. Abstract We present digitized data of the Federal Reserve System’s weekly balance sheet from 1914- 1941 for the first time. Following a brief account of the beginning era of the central bank, we analyze the composition and trends of Federal Reserve assets and liabilities, with particular emphasis on how they were affected by significant events such as World War I and the Great Depression. -

Closed for the Holiday: the Bank Holiday of 1933

THE BANK HOLIDAY OF 1933 THE BANK HOLIDAY OF 1933 is al~lm~achin,~,, ~dten no ore" Mll lu’ Iq/t to remind us that ".~ood he,dth " mid ,1 "stead),job" arc thin.~s that ou,~ht not to be tahcnJbr y, nmted. Hqth that in mind, theJbllo~dtt.~ paXes reaq~ tin" tu,o most c~,cnts qf the Great Dq~ression: the stoch marhct or, Mr qf 1929 amt the B,mh Holida), q/ 1933. As he stood before his party’s delegates to accept the 1928 Republican presidential nomination, Herbert Hoover had every reason to be optimistic. He had no way of knowing that he would soon face the most devastating economic collapse in U.S. history. WHAT OES UP... Herbert Hoover’s adult life had been au -- automobiles, refrigerators, washing machines, unbroken striug of successes. The Stauford- radios, phonographs -- aud middle-class Amer- trained mining engiueer had amassed a fortune icans discovered tile wonders of buying on by age 40 and embarked on a secoud career in instalhnent credit. public service. As director of relief operations in the years after World War I, he was responsible There was a widely-held belief that \vealth t-or saviug countless lives in war-ravaged Europe was witbiu reach of anyone with energy, initia- and garnered international recoguition. From tive, and the willinguess to take a risk. Chicago 1921 to 1928, lie stowed as SecretaW of Com- gangster M Capone declared merce under Presidents Harding and Coolidge (perhaps with a touch of aud was perhaps the ceutral figure iu the U.S. -

Strained Relations: US Foreign-Exchange Operations and Monetary Policy in the Twentieth Century

This PDF is a selection from a published volume from the National Bureau of Economic Research Volume Title: Strained Relations: U.S. Foreign-Exchange Operations and Monetary Policy in the Twentieth Century Volume Author/Editor: Michael D. Bordo, Owen F. Humpage, and Anna J. Schwartz Volume Publisher: University of Chicago Press Volume ISBN: 0-226-05148-X, 978-0-226-05148-2 (cloth); 978-0-226-05151-2 (eISBN) Volume URL: http://www.nber.org/books/bord12-1 Conference Date: n/a Publication Date: February 2015 Chapter Title: Introducing the Exchange Stabilization Fund, 1934–1961 Chapter Author(s): Michael D. Bordo, Owen F. Humpage, Anna J. Schwartz Chapter URL: http://www.nber.org/chapters/c13539 Chapter pages in book: (p. 56 – 119) 3 Introducing the Exchange Stabilization Fund, 1934– 1961 3.1 Introduction The Wrst formal US institution designed to conduct oYcial intervention in the foreign exchange market dates from 1934. In earlier years, as the preceding chapter has shown, makeshift arrangements for intervention pre- vailed. Why the Exchange Stabilization Fund (ESF) was created and how it performed in the period ending in 1961 are the subject of this chapter. After thriving in the prewar years from 1934 to 1939, little opportunity for intervention arose thereafter through the closing years of this period, so it is a natural dividing point in ESF history. The change in the fund’s operations occurred as a result of the Federal Reserve’s decision in 1962 to become its partner in oYcial intervention. A subsequent chapter takes up the evolution of the fund thereafter. -

Free to Choose

June 9, 2005 COMMENTARY Free to Choose By MILTON FRIEDMAN June 9, 2005; Page A16 Little did I know when I published an article in 1955 on "The Role of Government in Education" that it would lead to my becoming an activist for a major reform in the organization of schooling, and indeed that my wife and I would be led to establish a foundation to promote parental choice. The original article was not a reaction to a perceived deficiency in schooling. The quality of schooling in the United States then was far better than it is now, and both my wife and I were satisfied with the public schools we had attended. My interest was in the philosophy of a free society. Education was the area that I happened to write on early. I then went on to consider other areas as well. The end result was "Capitalism and Freedom," published seven years later with the education article as one chapter. With respect to education, I pointed out that government was playing three major roles: (1) legislating compulsory schooling, (2) financing schooling, (3) administering schools. I concluded that there was some justification for compulsory schooling and the financing of schooling, but "the actual administration of educational institutions by the government, the 'nationalization,' as it were, of the bulk of the 'education industry' is much more difficult to justify on [free market] or, so far as I can see, on any other grounds." Yet finance and administration "could readily be separated. Governments could require a minimum of schooling financed by giving the parents vouchers redeemable for a given sum per child per year to be spent on purely educational services. -

Friedman's Monetary Framework

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by Research Papers in Economics Friedman’s Monetary Framework: Some Lessons Ben S. Bernanke t is an honor and a pleasure to have this opportunity, on the anniversary of Milton and Rose Friedman’s popular classic, Free to Choose, to speak on I Milton Friedman’s monetary framework and his contributions to the theory and practice of monetary policy. About a year ago, I also had the honor, at a conference at the University of Chicago in honor of Milton’s ninetieth birthday, to discuss the contribution of Friedman’s classic 1963 work with Anna Schwartz, A Monetary History of the United States.1 I mention this earlier talk not only to indicate that I am ready and willing to praise Friedman’s contributions wherever and whenever anyone will give me a venue but also because of the critical influ- ence of A Monetary History on both Friedman’s own thought and on the views of a generation of monetary policymakers. In their Monetary History, Friedman and Schwartz reviewed nearly a cen- tury of American monetary experience in painstaking detail, providing an his- torical analysis that demonstrated the importance of monetary forces in the economy far more convincingly than any purely theoretical or even economet- ric analysis could ever do. Friedman’s close attention to the lessons of history for economic policy is an aspect of his approach to economics that I greatly admire. Milton has never been a big fan of government licensing of profession- als, but maybe he would make an exception in the case of monetary policy- makers. -

Comment Letter of Federated Hermes, Inc. on Structural Reforms to Mitigate Systemic Risk and the Root Causes of the Liquidity Crisis of March 2020 (SEC File No

Fede1·ated Federated Hermes, Inc. Hermes -• June 1, 2021 United States Secmities and Exchange Commission 100 F St NE Washington, DC 20549 Board of Governors of the Federal Reserve System Constitution Ave NW &, 20th St NW Washington, DC 20551 United States Treasmy Department 1500 Pennsylvania A venue NW Washington, DC 20220 Re: Comment Letter Of Federated Hermes, Inc. On Structural Reforms To Mitigate Systemic Risk And The Root Causes Of The Liquidity Crisis Of March 2020 (SEC File No. S7-01-21) Dear Ladies and Gentlemen: I am writing on behalf of Federated He1mes, Inc. and its subsidiaries ("Federated He1mes"), to provide additional comments in response to the Repo1i of the President's Working Group on Financial Markets, Overview of Recent Events and Potential Refonn Options Repo1i on Money Market Funds (the "PWG MMF Repo1i") which was issued in December 2020. 1 Federated Hennes has ah-eady provided detailed comments that respond to the specific policy options identified in the PWG MMF Repo1i (the "First Federated He1mes Comment Letter") and are inco1porated and restated herein by reference. 2 In this comment Federated Hennes recommends stmctmal refo1ms that address the root causes of the failme of critical funding markets in March 2020 and the consequent systematic 1 President's Working Group on Financial Markets, Overview ofRecent Events and Potential Reform Options for Money Market Funds (Dec. 2020), available at https://home.treasmy.gov/system/files/136/PWG-MMF-repoit-final-Dec-2020.pdf (" PWG MMF Repo1t"). 2 See the First Federated Hermes, Comment Letter, (Apr. 12, 2021), available at https://www.sec.gov/comments/s7-0l -21/s70121-8662821-2353 l 1.pdf ("Federated He1mes First Comment Letter").