Overview of Advanced Technology Transportation, 2004 Update. Advanced Vehicle Testing Activity

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Multiple Year Bus Procurement Program

Customer Services, Operations, and Safety Committee Board Action/Action Item III-A September 13, 2007 Multiple Year Bus Procurement Program Washington Metropolitan Area Transportation Authority Board Action/Information Summary Action MEAD Number: Resolution: Information 99828 Yes No PURPOSE Obtain Board approval to award a one-year base with four one-year options competitive procurement of hybrid electric buses and a procurement of 22 articulated Compressed Natural Gas (CNG) buses utilizing piggy-back options available from Los Angeles County Metropolitan Transportation Authority. DESCRIPTION On May 4, 2006, staff presented to the Planning and Development Committee the Bus Technology selection for FY08-12 and requested approval to initiate and award a one-year base with four one-year options competitive procurement of hybrid electric buses. This contract includes 100 buses a year for five years with options for an additional 100 buses each year assignable to other agencies. The Committee requested staff return to the Committee for final approval of the selected vendor. On June 19, 2006, the Board approved funding and authority to initiate the contracting action. Additionally, staff is requesting Board approval to purchase 22 articulated CNG buses as replacement buses. These 22 articulated CNG buses will be procured in accordance with Federal Transit Administration (FTA) Circular 4220 1.E “Assignabilty” options available from Los Angeles County Metropolitan Transportation Authority for CNG Bus Rapid Transit (BRT) style buses. FUNDING IMPACT There is no further impact on funding. Funding approved June 2006. RECOMMENDATION Board approval to award a one-year base with four one-year options competitive procurement of hybrid electric buses and procure 22 articulated CNG buses utilizing piggy-back options available from Los Angeles County Metropolitan Transportation Authority for CNG Bus Rapid Transit (BRT) style buses. -

Surplus Property Inventory

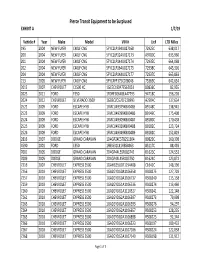

Pierce Transit Equipment to be Surplused EXHIBIT A 1/7/19 Vehicle # Year Make Model VIN # Lic# LTD Miles 195 2004 NEW FLYER C40LF CNG 5FYC2LP194U027168 72925C 638,017 200 2004 NEW FLYER C40LF CNG 5FYC2LP124U027173 A9780C 633,960 201 2004 NEW FLYER C40LF CNG 5FYC2LP144U027174 72935C 664,068 202 2004 NEW FLYER C40LF CNG 5FYC2LP164U027175 72938C 645,301 204 2004 NEW FLYER C40LF CNG 5FYC2LP1X4U027177 72937C 665,863 213 2005 NEW FLYER C40LF CNG 5FYC4FP175C028046 75369C 642,634 2012 2007 CHEVROLET C1500 XC 1GCEC19047E562051 80836C 82,955 2023 2011 FORD F350 1FDRF3G64BEA47793 94718C 156,201 2024 2012 CHEVROLET SILVERADO 3500 1GB3CZCG2CF228993 A2904C 137,634 2522 2009 FORD ESCAPE HYB 1FMCU49379KB00485 89148C 138,941 2523 2009 FORD ESCAPE HYB 1FMCU49399KB00486 89149C 175,408 2524 2009 FORD ESCAPE HYB 1FMCU49309KB00487 89180C 170,458 2525 2009 FORD ESCAPE HYB 1FMCU49329KB00488 89182C 123,724 2526 2009 FORD ESCAPE HYB 1FMCU49349KB00489 89181C 152,819 2816 2007 DODGE GRAND CARAVAN 1D4GP24E57B251304 80829C 160,398 4590 2001 FORD E350 1FBSS31L81HB58963 85117C 88,493 7001 2005 DODGE GRAND CARAVAN 2D4GP44L55R183742 B1623C 124,553 7009 2005 DODGE GRAND CARAVAN 2D4GP44L45R183750 B1624C 123,872 7216 2007 CHEVROLET EXPRESS 3500 1GAHG35U071194408 C1642C 148,396 7256 2010 CHEVROLET EXPRESS 3500 1GA2GYDG0A1106558 RS08275 127,703 7257 2010 CHEVROLET EXPRESS 3500 1GA2GYDG0A1106737 RS08240 115,158 7259 2010 CHEVROLET EXPRESS 3500 1GA2GYDG1A1106536 RS08274 113,460 7260 2010 CHEVROLET EXPRESS 3500 1GA2GYDG1A1110327 RS08241 122,148 7261 2010 CHEVROLET EXPRESS 3500 -

Financial Analysis of Battery Electric Transit Buses (PDF)

Financial Analysis of Battery Electric Transit Buses Caley Johnson, Erin Nobler, Leslie Eudy, and Matthew Jeffers National Renewable Energy Laboratory NREL is a national laboratory of the U.S. Department of Energy Technical Report Office of Energy Efficiency & Renewable Energy NREL/TP-5400-74832 Operated by the Alliance for Sustainable Energy, LLC June 2020 This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications. Contract No. DE-AC36-08GO28308 Financial Analysis of Battery Electric Transit Buses Caley Johnson, Erin Nobler, Leslie Eudy, and Matthew Jeffers National Renewable Energy Laboratory Suggested Citation Johnson, Caley, Erin Nobler, Leslie Eudy, and Matthew Jeffers. 2020. Financial Analysis of Battery Electric Transit Buses. Golden, CO: National Renewable Energy Laboratory. NREL/TP-5400-74832. https://www.nrel.gov/docs/fy20osti/74832.pdf NREL is a national laboratory of the U.S. Department of Energy Technical Report Office of Energy Efficiency & Renewable Energy NREL/TP-5400-74832 Operated by the Alliance for Sustainable Energy, LLC June 2020 This report is available at no cost from the National Renewable Energy National Renewable Energy Laboratory Laboratory (NREL) at www.nrel.gov/publications. 15013 Denver West Parkway Golden, CO 80401 Contract No. DE-AC36-08GO28308 303-275-3000 • www.nrel.gov NOTICE This work was authored by the National Renewable Energy Laboratory, operated by Alliance for Sustainable Energy, LLC, for the U.S. Department of Energy (DOE) under Contract No. DE-AC36-08GO28308. Funding provided by the U.S. Department of Energy Office of Energy Efficiency and Renewable Energy Vehicle Technologies Office. -

Page 1 of 32 VEHICLE RECALLS by MANUFACTURER, 2000 Report Prepared 1/16/2008

Page 1 of 32 VEHICLE RECALLS BY MANUFACTURER, 2000 Report Prepared 1/16/2008 MANUFACTURER RECALLS VEHICLES ACCUBUIL T, INC 1 8 AM GENERAL CORPORATION 1 980 AMERICAN EAGLE MOTORCYCLE CO 1 14 AMERICAN HONDA MOTOR CO 8 212,212 AMERICAN SUNDIRO MOTORCYCLE 1 2,183 AMERICAN SUZUKI MOTOR CORP. 4 25,023 AMERICAN TRANSPORTATION CORP. 5 1,441 APRILIA USA INC. 2 409 ASTON MARTIN 2 666 ATHEY PRODUCTS CORP. 3 304 B. FOSTER & COMPANY, INC. 1 422 BAYERISCHE MOTOREN WERKE 11 28,738 BLUE BIRD BODY COMPANY 12 62,692 BUELL MOTORCYCLE CO 4 12,230 CABOT COACH BUILDERS, INC. 1 818 CARPENTER INDUSTRIES, INC. 2 6,838 CLASSIC LIMOUSINE 1 492 CLASSIC MANUFACTURING, INC. 1 8 COACHMEN INDUSTRIES, INC. 8 5,271 COACHMEN RV COMPANY 1 576 COLLINS BUS CORPORATION 1 286 COUNTRY COACH INC 6 519 CRANE CARRIER COMPANY 1 138 DABRYAN COACH BUILDERS 1 723 DAIMLERCHRYSLER CORPORATION 30 6,700,752 DAMON CORPORATION 3 824 DAVINCI COACHWORKS, INC 1 144 D'ELEGANT CONVERSIONS, INC. 1 34 DORSEY TRAILERS, INC. 1 210 DUTCHMEN MANUFACTURING, INC 1 105 ELDORADO NATIONAL 1 173 ELECTRIC TRANSIT, INC. 1 54 ELGIN SWEEPER COMPANY 1 40 E-ONE, INC. 1 3 EUROPA INTERNATIONAL, INC. 2 242 EXECUTIVE COACH BUILDERS 1 702 FEATHERLITE LUXURY COACHES 1 83 FEATHERLITE, INC. 2 3,235 FEDERAL COACH, LLC 1 230 FERRARI NORTH AMERICA 8 1,601 FLEETWOOD ENT., INC. 5 12, 119 FORD MOTOR COMPANY 60 7,485,466 FOREST RIVER, INC. 1 115 FORETRAVEL, INC. 3 478 FOURWINNS 2 2,276 FREIGHTLINER CORPORATION 27 233,032 FREIGHTLINER LLC 1 803 GENERAL MOTORS CORP. -

Richard Ferguson Is a Fortune 50 Business Leader with a Unique Blend of Sales and Financial Management Experience. He Has Extens

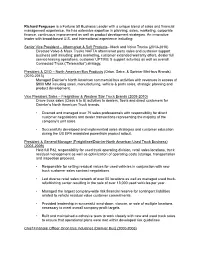

Richard Ferguson is a Fortune 50 Business Leader with a unique blend of sales and financial management experience. He has extensive expertise in planning, sales, marketing, corporate finance, continuous improvement as well as product development strategies. An innovative leader with broad-based U.S. and international experience including: Senior Vice President – Aftermarket & Soft Products– Mack and Volvo Trucks (2013-2016) Directed Volvo & Mack Trucks NAFTA aftermarket parts sales and customer support business unit including: parts marketing, customer extended warranty offers, dealer full service leasing operations, customer UPTIME & support activities as well as overall Connected Truck (“Telematics”) strategy. President & CEO – North American Bus Products (Orion, Setra, & Sprinter Mini-bus Brands) (2010-2013) Managed Daimler’s North American commercial bus activities with revenues in excess of $900 MM including sales, manufacturing, vehicle & parts sales, strategic planning and product development. Vice President Sales – Freightliner & Western Star Truck Brands (2009-2010) Drove truck sales (Class 6 to 8) activities to dealers, fleets and direct customers for Daimler’s North American Truck brands. • Directed and managed over 75 sales professionals with responsibility for direct customer negotiations and dealer transactions representing the majority of the company’s unit sales. • Successfully developed and implemented sales strategies and customer education during the US EPA mandated powertrain product rollout. President & General Manager (Freightliner/Daimler North American Used Truck Business) (2003-2009) Held full P&L responsibility for used truck operating division, retail sales locations, truck residual management as well as optimization of operating costs (storage, transportation and inspection process). • Responsible for setting residual values for used vehicles in conjunction with new truck customer sales contract negotiations. -

Field Operations Program -- Overview Of

July 2000 • NREL/MP-540-27962 Field Operations Program― Overview of Advanced Technology Transportation CY2000 K. Kelly L. Eudy National Renewable Energy Laboratory 1617 Cole Boulevard Golden, Colorado 80401-3393 NREL is a U.S. Department of Energy Laboratory Operated by Midwest Research Institute • Battelle • Bechtel Contract No. DE-AC36-99-GO10337 NOTICE This report was prepared as an account of work sponsored by an agency of the United States government. Neither the United States government nor any agency thereof, nor any of their employees, makes any warranty, express or implied, or assumes any legal liability or responsibility for the accuracy, completeness, or usefulness of any information, apparatus, product, or process disclosed, or represents that its use would not infringe privately owned rights. Reference herein to any specific commercial product, process, or service by trade name, trademark, manufacturer, or otherwise does not necessarily constitute or imply its endorsement, recommendation, or favoring by the United States government or any agency thereof. The views and opinions of authors expressed herein do not necessarily state or reflect those of the United States government or any agency thereof. Printed on paper containing at least 50% wastepaper, including 20% postconsumer waste Field Operations Program—Overview of Advanced Technology Transportation, CY 2000 The transportation industry’s private sector is adept at understanding and meeting the demands of its customers; the federal government has a role in encouraging the development of products that are in the long-term interest of the greater public good. It is up to the government to understand issues that affect public health, well-being, and security. -

Financial Results Fiscal 2020

Financial Results Fiscal 2020 March 4, 2021 NFI continues changing the game. 2 NFI GROUP INC. 2020 REPORT www.nfigroup.com We continue to innovate and drive forward. 3 NFI GROUP INC. 2020 REPORT www.nfigroup.com We provide comprehensive mobility solutions. 4 NFI GROUP INC. 2020 REPORT www.nfigroup.com We have more than 105,000 buses in service in 11 countries around the world. 5 NFI GROUP INC. 2020 REPORT www.nfigroup.com We are leading the evolution to a zero-emission future. 6 NFI GROUP INC. 2020 REPORT www.nfigroup.com NOTES TO READERS MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS FOR THE 13-WEEKS AND 52-WEEKS ENDED DECEMBER 27, 2020 Information in this Management’s Discussion and Analysis (“MD&A”) relating to the financial condition and results of operations of NFI Group Inc. (“NFI” or the "Company") is supplemental to, and should be read in conjunction with, NFI’s audited consolidated financial statements (including notes) (the “Financial Statements”) for the 52-week period ended December 27, 2020. This MD&A contains forward-looking statements, which are subject to a variety of factors that could cause actual results to differ materially from those contemplated by such forward-looking statements, including, but not limited to, the factors described in the Company's public filings available on SEDAR at www.sedar.com. See “Forward-Looking Statements” in Appendix A. The Financial Statements have been prepared in accordance with International Financial Reporting Standards (“IFRS”) and, except where otherwise indicated, are presented in U.S. -

INVESTOR PRESENTATION August 2019

INVESTOR PRESENTATION August 2019 NFI:TSX Who is NFI? Bus Design & Manufacture Part Fabrication Parts and Service North America’s largest bus and North America’s largest heavy-duty Captive fiberglass reinforced plastic motor coach parts distributor public transit bus manufacturer fabricator for MCI, New Flyer and ADL and the leader in Zero-Emission Bus (ZEB) transit Captive parts fabricator for New Flyer, UK’s leading bus parts distributor North American market leader in ARBOC and NFI Parts. Plans to and aftermarket service support motor coaches for both Public and KMG fabricate for MCI and ADL beyond network Private operators 2020 U.K.’s largest bus and motor coach Supports eMobility projects from manufacturer with leading share in start to finish Hong Kong and New Zealand and a growing global presence. North America’s first innovation North America’s disruptive low-floor lab dedicated to the exploration cutaway and medium-duty transit and advancement of bus and bus leader coach technology 2 Why Invest In NFI? Track Record Our Differentiators • Trusted business partner with over 300 years of combined bus • Market leading positions in US, Canada, UK, Hong Kong and and motor coach design and manufacturing experience New Zealand with strong portfolios in Singapore, Malaysia and Mexico • 5 year Q2 2019 LTM Revenue CAGR of 13.1% and Adj. EBITDA CAGR of 21.5% • Growing presence in Switzerland and Germany (gateway into continental Europe) • Peer Leading(1) 11.6% Q2 2019 LTM Adj. EBITDA margin • ~80% of revenue driven by public (i.e. government -

Reg Makes Sorted by Company Name

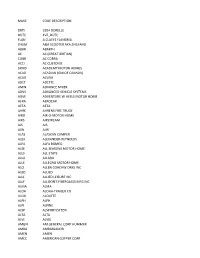

MAKE CODE DESCRIPTION DRTI 1954 DORELLE DUTC 4VZ_DUTC FLAN A CLAEYS FLANDRIA ZHUM A&A SCOOTER AKA ZHEJIANG ABAR ABARTH AC AC (GREAT BRITIAN) COBR AC COBRA ACCI AC CUSTOMS SKMD ACADEMY MOTOR HOMES ACAD ACADIAN (GM OF CANADA) ACUR ACURA ADET ADETTE AMIN ADVANCE MIXER ADVS ADVANCED VEHICLE SYSTEMS ADVE ADVENTURE W HEELS MOTOR HOME AERA AEROCAR AETA AETA AHRE AHRENS FIRE TRUCK AIRO AIR-O-MOTOR HOME AIRS AIRSTREAM AJS AJS AJW AJW ALAS ALASKAN CAMPER ALEX ALEXANDER-REYNOLDS ALFA ALFA ROMEO ALSE ALL SEASONS MOTOR HOME ALLS ALL STATE ALLA ALLARD ALLE ALLEGRO MOTOR HOME ALCI ALLEN COACHW ORKS INC ALED ALLIED ALLL ALLIED LEISURE INC ALLF ALLISON'S FIBERGLASS MFG INC ALMA ALMA ALOH ALOHA-TRAILER CO ALOU ALOUTTE ALPH ALPH ALPI ALPINE ALSP ALSPORT/STEEN ALTA ALTA ALVI ALVIS AMGN AM GENERAL CORP HUMMER AMBA AMBASSADOR AMEN AMEN AMCC AMERICAN CLIPPER CORP AMCR AMERICAN CRUISER INC AEAG AMERICAN EAGLE AMEL AMERICAN ECONOMOBILE HILIF AIH AMERICAN IRONHORSE MOTORCYCLE LAFR AMERICAN LA FRANCE AMLF AMERICAN LIFAN IND INC AMI AMERICAN MICROCAR INC AMER AMERICAN MOTORS AMPF AMERICAN PERFORMANCE AMQT AMERICAN QUANTUM AMF AMF AMME AMMEX AMPH AMPHICAR AMPT AMPHICAT AMTC AMTRAN CORP ANGL ANGEL APOL APOLLO HOMES APRI APRILIA USA,INC. ARCA ARCTIC CAT ARGO ARGONAUT STATE LIMOUSINE ARGS ARGOSY TRAVEL TRAILER AGYL ARGYLE ARIE ARIEL (BRITISH) ARIT ARISTA ARIS ARISTOCRAT MOTOR HOME ARMS ARMSTRONG SIDDELEY ARNO ARNOLT-BRISTOL ARO ARO OF N.A. ARRO ARROW ARTI ARTIE ASA ASA ARSC ASCORT ASHL ASHLEY ASPS ASPES ASVE ASSEMBLED VEHICLE (NO MFR VIN) ASTO ASTON-MARTIN ASUN ASUNA -

CNG As a Transit Bus Fuel

TheThe TransitTransit BusBus NicheNiche MarketMarket ForFor AlternativeAlternative Fuels:Fuels: ModuleModule 3:3: OverviewOverview ofof CompressedCompressed NaturalNatural GasGas asas aa TransitTransit BusBus FuelFuel CleanClean CitiesCities CoordinatorCoordinator ToolkitToolkit PreparedPrepared byby TIAXTIAX LLC,LLC, IrvineIrvine OfficeOffice DecemberDecember 20032003 TIAX LLC One Park Plaza, 6th Floor Irvine, California 92614 949-833-7131 / [email protected] Options for Natural Gas Fueling in Transit • Compressed Natural Gas (CNG) – Pipeline natural gas: methane with other hydrocarbons – Pressurized to 3,600 psi – Fueling accomplished by pressure transfer to vehicle – About 12% of transit buses in the U.S. now use conventional CNG – Largest users include LACMTA, MARTA, NY DOT, Pierce Transit, Washington D.C. (WMATA), Cleveland, Sacramento • Liquefied Natural Gas (LNG) – Nearly pure methane (~98%) liquefied at very low temperatures – Liquid transfer to vehicle – Largest users are Phoenix, Orange County (CA), Dallas, and Tempe – Newer users include Santa Monica, Long Beach • LNG to CNG (“LCNG”) – Vaporized LNG (also nearly pure methane) – Liquid to gas conversion, then pressure transfer to vehicle – Sun Metro, OmniTrans, others use this approach Document Code 1 Methane Content in Pipeline Natural Gas Varies Regionally Methane Molecule Typical Composition of Pipeline Natural Gas What are the Implications of the Resulting CNG Fuel Quality Variations? • CNG with lower methane content (higher levels of ethane, propane, or butane) has resulted in some adverse affects on heavy-duty NG engine performance (e.g., misfire, stumble and underrated operation, engine knock, overheating) • However, today’s lean-burn closed-loop NG engines for transit (e.g., C Gas Plus and DDC S50G) are better able to tolerate and compensate for variations • Compromises in emissions performance have been found to be modest Document Code 2 Numerous OEMs Offer Natural Gas Transit Buses and Paratransit Vehicles Natural Gas Bus Manufacturer Models Available Champion Bus, Inc. -

Optimization Tool for Transit Bus Fleet Management

Graduate Theses, Dissertations, and Problem Reports 2012 Optimization tool for transit bus fleet management Feng Zhen West Virginia University Follow this and additional works at: https://researchrepository.wvu.edu/etd Recommended Citation Zhen, Feng, "Optimization tool for transit bus fleet management" (2012). Graduate Theses, Dissertations, and Problem Reports. 600. https://researchrepository.wvu.edu/etd/600 This Dissertation is protected by copyright and/or related rights. It has been brought to you by the The Research Repository @ WVU with permission from the rights-holder(s). You are free to use this Dissertation in any way that is permitted by the copyright and related rights legislation that applies to your use. For other uses you must obtain permission from the rights-holder(s) directly, unless additional rights are indicated by a Creative Commons license in the record and/ or on the work itself. This Dissertation has been accepted for inclusion in WVU Graduate Theses, Dissertations, and Problem Reports collection by an authorized administrator of The Research Repository @ WVU. For more information, please contact [email protected]. OPTIMIZATION TOOL FOR TRANSIT BUS FLEET MANAGEMENT by Feng Zhen Dissertation submitted to the College of Engineering and Mineral Resources at West Virginia University in partial fulfillment of the requirements for the degree of Doctor of Philosophy in Mechanical Engineering Approved by Nigel N. Clark, Ph.D., Committee Chairperson W. Scott Wayne, Ph.D. Hailin Li, Ph.D. Benjamin C. Shade, Ph.D. Roy S. Nutter, Jr., Ph.D. Department of Mechanical and Aerospace Engineering Morgantown, West Virginia 2012 Keywords: Transit Bus Operation, Cost Evaluation, Greenhouse Gas Emissions, Operation Optimization, Genetic Algorithm Copyright 2012 Feng Zhen ABSTRACT OPTIMIZATION TOOL FOR TRANSIT BUS FLEET Management By Feng Zhen Transit agencies face the challenge of being environmentally-friendly, while maintaining cost-effective operation. -

Download the Roadeo Program

August 2 - 5, 2019 BUILDING AMERICA’S ZERO EMISSIONS FUTURE Now Available! GILLIG’s new Battery Electric offering, powered by Cummins’ electrified powertrain. Partners you can trust. www.GILLIG.com Jerry Sheehan 510-329-0320 | [email protected] Summer Meeting & Roadeo Sponsor Sunday Bocce & Dinner Sponsor Passenger Assistance & Wheelchair Securement Sponsor Sunday Roadeo Awards Lunch Sponsor Roadeo & Summer Meeting Lanyard Sponsor Monday Membership Breakfast Sponsor Showcase Sponsors Roadeo Water & Snack Sponsors Key Locations Shuttles to Roadeo events on Saturday and Sunday will stop at both the Residence Inn (wait near the hotel’s rear entrance on Third Street) and Towneplace Suites (wait near the hotel’s main entrance on Church Street). Departure times are noted throughout the schedule. Residence Inn Williamsport 150 W Church Street, Williamsport, PA 17701 One of two host hotels for PPTA’s 2019 Roadeo & Summer Meeting. The rear entrance on Third Street is located directly across the street from the Michael Ross Event Center. Towneplace Suites Williamsport 10 W Church Street, Williamsport, PA 17701 The second of two host hotels for PPTA’s 2019 Roadeo & Summer Meeting. Located about two blocks from the Residence Inn & Michael Ross Event Center Michael Ross Event Center 3rd Floor, 144 W Third Street, Williamsport, PA 17701 The hub of all Roadeo & Summer Meeting Events. Registration, drivers’ and judges’ meetings, and Monday morning programs will be held here. Transit Drive 100 W Third Street, Williamsport, PA 17701 Location of Saturday events for drivers competing in the Roadeo. Located next door to the Michael Ross Event Center, Transit Drive sits behind RVT’s Trade & Transit Centre I.