Efinance ENABLERS: EFFICIENTLY MOVING the BUCK

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Credit Union Guidebook

Retail Impact Investing A GUIDEBOOK FOR CANADIAN CREDIT UNIONS FOREWORD Impact investing has the potential to be a growth opportunity and differentiator for the Canadian credit union sector. Today, impact investment options exist primarily for institutional and accredited investors. The opportunities for everyday investors to generate a return, while generating positive impact, are limited – this, despite evidence of market interest led by millennials and others. Credit unions are well positioned to tap into this opportunity. A core part of their mission is to ensure the financial, social and environmental well-being of the communities they serve: a mission that is aligned with the principles of impact investing. We see this Guidebook as a tangible resource to help credit unions address a marketplace gap and empower members to make investments that will have demonstrable, positive impacts in their communities. The Guidebook offers credit unions of all sizes and at all stages of their social responsibility journey actionable ideas of how to create and deploy retail impact investment products for their members. The guide also points to recommendations that the credit union sector as a whole can undertake. The Canadian Credit Union Association (CCUA) is committed to working with credit unions to explore how these recommendations can be advanced. We welcome your ideas and feedback - contact us at www.impactinvesting.ca/contact. CCUA is proud to have partnered with Purpose Capital, Employment and Social Development Canada, as well as a number of interested credit unions, to develop and share the research in this Guidebook. We want to extend our gratitude to Affinity Credit Union, Alterna Savings and Credit Union, Assiniboine Credit Union, Conexus Credit Union, DUCA Financial Services Credit Union, Libro Credit Union, Mennonite Savings & Credit Union, Meridian Credit Union, Servus Credit Union and Vancity Credit Union for their support and contribution to the development of this Guidebook. -

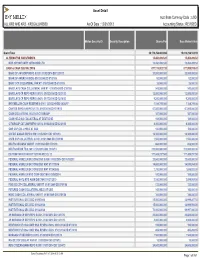

Asset Detail Acct Base Currency Code : USD ALL KR2 and KR3 - KR2GALLKRS00 As of Date : 12/31/2013 Accounting Status : REVISED

Asset Detail Acct Base Currency Code : USD ALL KR2 AND KR3 - KR2GALLKRS00 As Of Date : 12/31/2013 Accounting Status : REVISED . Mellon Security ID Security Description Shares/Par Base Market Value Grand Total 36,179,254,463.894 15,610,214,163.19 ALTERNATIVE INVESTMENTS 15,450,499.520 15,450,499.52 MKP OPPORTUNITY OFFSHORE LTD 15,450,499.520 15,450,499.52 CASH & CASH EQUIVALENTS 877,174,023.720 877,959,915.42 BANC OF AM CORP REPO 0.010% 01/02/2014 DD 12/31/13 20,000,000.000 20,000,000.00 BANK OF AMERICA (BOA) 01/01/2049 DD 07/01/08 52,000.000 52,000.00 BARC CCP COLLATERAL VAR RT 01/01/2049 DD 07/01/08 28,000.000 28,000.00 BARCLAYS CASH COLLATERAL VAR RT 01/01/2049 DD 07/01/08 543,000.000 543,000.00 BARCLAYS CP REPO REPO 0.010% 01/02/2014 DD 12/31/13 12,000,000.000 12,000,000.00 BARCLAYS CP REPO REPO 0.040% 01/17/2014 DD 12/18/13 9,200,000.000 9,200,000.00 BNY MELLON CASH RESERVE 0.010% 12/31/2049 DD 06/26/97 1,184,749.080 1,184,749.08 CANTOR REPO A REPO 0.170% 01/02/2014 DD 12/19/13 67,000,000.000 67,000,000.00 CASH COLLATERAL HELD AT CITIGROUP 387,000.000 387,000.00 CASH HELD AS COLLATERAL AT DEUTSCHE 169,000.000 169,000.00 CITIGROUP CAT 2MM REPO 0.010% 01/02/2014 DD 12/31/13 8,300,000.000 8,300,000.00 CME CCP COLL HELD AT GSC 100,000.000 100,000.00 CREDIT SUISSE REPO 0.010% 01/02/2014 DD 12/31/13 16,300,000.000 16,300,000.00 CSFB CCP COLLATERAL 0.010% 01/01/2049 DD 07/01/08 1,553,000.000 1,553,000.00 DEUTSCHE BANK VAR RT 01/01/2049 DD 07/01/08 668,000.000 668,000.00 DEUTSCHE BK TD 0.180% 01/02/2014 DD 12/18/13 270,000,000.000 270,000,000.00 -

Meewasin Annual Report 2010-2011

Annual Report Celebrating the Meewasin Valley Other significant successes in 2010-2011 include: Message from the Chair and CEO • Began major work to complete the wetland area at River Landing 1 including the river garden water Meewasin has completed 32 years of stewardship in feature to be installed this summer. the valley with successes in all areas of our mandate. • Worked on a trail in River Landing 2 including a Meewasin is unique in North America, a resource that connection from Avenue B back to the Farmers’ is considered by the people of Saskatoon and area to be Chair, Jack Vicq Market area. Completion of the backshore work in one of the single biggest contributors to our quality of this area awaits final installation of the sanitary life. We feel humbled by the responsibility. sewer. We received excellent support for special projects from Developed a new trail at the Water Treatment Plant. the public and private sector this year. With help from • We plan some more backshore work this year but all orders of government, corporate and the general completion depends on improvements to the facility public we were successful this year in raising $700,000 itself. to build the new Cameco Meewasin Skating Rink at PotashCorp Plaza, including permanent washrooms • Completed resource management work at Beaver Creek Conservation Area and the Northeast Swale. CEO, Susan Lamb and a trail connection from Spadina Crescent to the This latter work will be a focus of our resource Meewasin Trail (to be completed this summer of 2011). management plans for 2011-2012. -

6709BWOL Webstock

RIDING THE WEB-STOCK ROLLER COASTER Reprinted from the August 12, 2004 issue of BusinessWeek Online. Copyright © 2004 by The McGraw-Hill Companies. This reprint implies no endorsement, either tacit or expressed, of any company, product, service or investment opportunity. RIDING THE WEB-STOCK ROLLER COASTER Our BW Web 20 Index tracks a selection of favorite Net stocks, and this column will help interpret the ups and downs he past month has been rotten Just last week, Forrester Research christening the BW Web 20 Index Tfor Internet investors. Stocks raised its e-commerce forecast, pre- – is intended to help aggressive have been hammered since second- dicting U.S. online sales of $227 bil- investors accept the risk inherent in quarter earnings showed Web out- lion in 2007, up from earlier projec- the Web, but balance it by focusing fits growing pretty much as they had tions of $204 billion. Forrester on “real” companies with solid prod- promised – a change from their habit expects e-commerce in the U.S. to ucts, services, and profits. Every of slightly besting quarterly projec- grow 14% annually through 2010 – month, this column will do more than tions. The carnage has been just as three to four times faster than the track how stocks in our index trade – severe in the Real World Internet economy. Meanwhile, growth in it also will help investors figure out Index, a group of Web stocks we Europe is predicted to average 33% which rallies are sustainable and spot picked in 2002 to help ordinary annually through 2009. the bubblicious behavior that earned investors play the Internet without Net investing a bad rap. -

Software Industry Financial Report Contents

The Software Industry Financial Report SOFTWARE INDUSTRY FINANCIAL REPORT CONTENTS About Software Equity Group Leaders in Software M&A 4 Extensive Global Reach 5 Software Industry Macroeconomics Global GDP 8 U.S. GDP and Unemployment 9 Global IT Spending 10 E-Commerce and Digital Advertising Spend 11 SEG Indices vs. Benchmark Indices 12 Public Software Financial and Valuation Performance The SEG Software Index 14 The SEG Software Index: Financial Performance 15-17 The SEG Software Index: Market Multiples 18-19 The SEG Software Index by Product Category 20 The SEG Software Index by Product Category: Financial Performance 21 The SEG Software Index by Product Category: Market Multiples 22 Public SaaS Company Financial and Valuation Performance The SEG SaaS Index 24 The SEG SaaS Index Detail 25 The SEG SaaS Index: Financial Performance 26-28 The SEG SaaS Index: Market Multiples 29-30 The SEG SaaS Index by Product Category 31 The SEG SaaS Index by Product Category: Financial Performance 32 The SEG SaaS Index by Product Category: Market Multiples 33 Public Internet Company Financial and Valuation Performance The SEG Internet Index 35 The SEG Internet Index: Financial Performance 36-38 The SEG Internet Index: Market Multiples 39-40 The SEG Internet Index by Product Category 41 The SEG Internet Index by Product Category: Financial Performance 42 The SEG Internet Index by Product Category: Market Multiples 43 1 Q3 2013 Software Industry Financial Report Copyright © 2013 by Software Equity Group, LLC All Rights Reserved SOFTWARE INDUSTRY FINANCIAL -

Registered Political Party's Fiscal Period Return AS REVIEWED

E-521 Form BBB Registered Political Party's The Election Act, 1996 Fiscal Period Return Section 250 ,'g1ecticmsl!3J! (Form E-522) (Oct 2017) AS REVIEWED The Saskatchewan Party Name of Registered Political Party December 31, 2019 For Fiscal Year Ending ,. II VE JUN 1 2 2020 at : INDEPENDENT AUDITORS' REPORT To The Saskatchewan Party Fund Inc. Chief Official Agent for The Saskatchewan Party for submission to the Chief Electoral Officer of Saskatchewan in accordance with Section 250(4) of The Election Act, 1996 Qualified Opinion We have audited the accompanying Registered Political Party's Fiscal Period Return [the "Return"] of The Saskatchewan Party, which comprises the summary of Contributions Part I and the summary of Expenditures - Part II for the fiscal period ending December 31, 2019. In our opinion, except for the possible effects of the matter described in the Basis for Qualified Opinion section of our report, the Return for the fiscal period ending December 31, 2019 is prepared, in all material respects, in accordance with the financial reporting provisions of section 250 of The Election Act, 1996 and the accounting guidelines and prescribed form issued by Elections Saskatchewan. Basis for QualifiedOpinion Due to the inherent nature of the transactions of registered political parties, the completeness of contributions and other revenue and expenses is not susceptible of satisfactory audit verification. Accordingly, our verification of these amounts was limited to the amounts recorded in the registered political party's accounting records and we were not able to determine whether any adjustments might be necessary to contributions and other revenue and expenses. -

Annual Report Board of Directors 2016–2017

WHEN SECONDS COUNT ROYAL UNIVERSITY HOSPITAL FOUNDATION 2016–2017 ANNUAL REPORT BOARD OF DIRECTORS 2016–2017 RUH Foundation 2016–2017 Board of Directors Back row (l-r) Vice Chair Don Neufeld, Executive Chairman, J&H Builder’s Warehouse; Executive Member at Large Robert Steane, Senior VP and COO, Cameco Corporation; Tyler Pochynuk, Director of Operations, Clark Roofing (1964) Ltd.; Kaylynn Schroeder, VP Corporate Services, West Wind Aviation; Nilesh Kavia, MBA, CPA, CMA, Executive VP of Operations, Affinity Credit Union; Past Chair Bryan Leverick, President, Alliance Energy Ltd.; Doug Osborn, Partner, MLT Aikens LLP; Mike McKague, Advisor, Precedence Private Wealth Front row (l-r) Dr. Karen Chad, VP Research, University of Saskatchewan; Dr. Daphne Taras, Past Dean and Professor, Edwards School of Business; Executive Member at Large Irene Boychuk, FCPA, FCA, Partner, EY LLP; Michael Smith, CPA, CA, Partner, Deloitte LLP; Sharon McDonald, Private Banker, RBC Wealth Management; Chair Dr. Paul Babyn, Joint Department Head of Medical Imaging for the Saskatoon Health Region and RUH Foundation Board of Directors University of Saskatchewan; Arla Gustafson, CEO REPORT OF THE VOLUNTEER CHAIR AND CEO Innovation is at the heart of our community Finding a Saskatchewan family without a connection to Royal University Hospital would not be easy. RUH is a pillar of healthcare innovation for this province and beyond, and is here 24 hours a day, 365 days a year anytime you or your loved ones need care. A tremendous thank you to you our donors, who contributed so generously to the $6.823 million raised in 2016–2017. Because of your generosity, our surgeons had the most advanced technology and equipment at hand to treat patients needing neurosurgery, neurology care and spine orthopedic surgery. -

Social Purpose Credit Union Self-Assessment

SOCIAL PURPOSE CREDIT UNION SELF-ASSESSMENT 2017 Credit unions are formalizing and focusing their ‘social purpose’ to better meet member needs, play a stronger role in fostering resilient and co-operative communities and grow their businesses. This tool was developed to help them in that effort. Using the language of corporate social responsibility (CSR), it guides credit unions through a process of considering the purpose and focus of their social role – which includes the environment and extends beyond traditional banking and co-operative roles. This tool was first commissioned by Libro Credit Union, based in Ontario, Canada, to assist them in their strategic planning. Libro engaged Coro Strandberg, President of Strandberg Consulting, to draft the tool based on best practices in social purpose in financial institutions and consultation with “CSR” and values- based banking practitioners in the Canadian credit union system. It also incorporates leading corporate practices from outside the financial services sector. University Federal Credit Union, based in Texas, US, subsequently engaged Coro Strandberg to update the tool to reflect best practices in the United States and globally. The Social Purpose Credit Union Self-Assessment is designed to assist in credit union strategic planning. It is a four-stage checklist of best, leading and next practices in CSR, social purpose and values-based banking in seven areas: governance, members, employees, community, environment, suppliers and business partners and the co-operative sector. Author: Coro Strandberg is a leading sustainability and corporate responsibility consultant, with over 25 years of experience advising credit unions and other companies on the design and implementation of community investment, CSR, and social purpose business models and strategies. -

1 UNITED STATES SECURITIES and EXCHANGE COMMISSION Washington, D.C

1 UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 13F FORM 13F COVER PAGE Report for the Calendar Year or Quarter Ended: September 30, 2000 Check here if Amendment [ ]; Amendment Number: This Amendment (Check only one.): [ ] is a restatement. [ ] adds new holdings entries Institutional Investment Manager Filing this Report: Name: AMERICAN INTERNATIONAL GROUP, INC. Address: 70 Pine Street New York, New York 10270 Form 13F File Number: 28-219 The Institutional Investment Manager filing this report and the person by whom it is signed represent that the person signing the report is authorized to submit it, that all information contained herein is true, correct and complete, and that it is understood that all required items, statements, schedules, lists, and tables, are considered integral parts of this form. Person Signing this Report on Behalf of Reporting Manager: Name: Edward E. Matthews Title: Vice Chairman -- Investments and Financial Services Phone: (212) 770-7000 Signature, Place, and Date of Signing: /s/ Edward E. Matthews New York, New York November 14, 2000 - ------------------------------- ------------------------ ----------------- (Signature) (City, State) (Date) Report Type (Check only one.): [X] 13F HOLDINGS REPORT. (Check if all holdings of this reporting manager are reported in this report.) [ ] 13F NOTICE. (Check if no holdings reported are in this report, and all holdings are reported in this report and a portion are reported by other reporting manager(s).) [ ] 13F COMBINATION REPORT. (Check -

US Asian Wire Distribution Points

US Asian Wire Distribution Points NewMediaWire’s comprehensive US Asian Wire delivers your news to targeted media in the Asian American community. Reaches leading Asian−American media outlets and over 375 trades and magazines dealing with political, finance, education, community, lifestyle and legal issues impacting Asian Americans as well as Online databases and websites that feature or cover Asian−American news and issues and The Associated Press. Please note, NewMediaWire includes free distribution to trade publications and newsletters. Because these are unique to each industry, they are not included in the list below. To get your complete NewMediaWire distribution, please contact your NewMediaWire account representative at 310.492.4001. aahar Newspaper Adhra Pradesh Times Newspaper Afternoon Despatch and Courier Newspaper Agence Kampuchea Press Newspaper Akila Daily Newspaper Algorithmica Japonica Newspaper am730 Newspaper Anand Rupwate Newspaper Andhra News Newspaper Andrha Pradesh Times Newspaper ANTARA News Agency Newspaper ASAHI PASOCOM Newspaper ASAHI SHIMBUN Newspaper Asahi Shimbun Newspaper Asahi Shimbun International Satellite Ed Newspaper Asia Insurance Review Newspaper Asia Pacific Management News Newspaper Asia Source Newspaper ASIA TIMES Newspaper Asian Affairs: An American Review Newspaper Asian American Press Newspaper Asian American Times Online Newspaper Asian Enterprise Magazine Newspaper Asian Focus Newspaper Asian Fortune Newspaper Asian Herald Newspaper Asian Industrial Reporter Newspaper Asian Journal Newspaper -

BANK and BANKING E-Banking Managing Your Money And

Teach Yourself Today e-Banking Teach Yourself Today e-Banking Managing your money and transactions online Mary Dixon Brian Nixon 201 West 103rd Street, Indianapolis, Indiana 46290 Sams Teach Yourself e-Banking Acquisitions Editor Today Jeff Schultz Copyright ©2000 by Sams Publishing Development All rights reserved. No part of this book shall be reproduced, stored Editor in a retrieval system, or transmitted by any means, electronic, Alice Martina Smith mechanical, photocopying, recording, or otherwise, without written Managing Editor permission from the publisher. No patent liability is assumed with Charlotte Clapp respect to the use of the information contained herein. Although every precaution has been taken in the preparation of this book, the Project Editor publisher and author assume no responsibility for errors or omis- Andy Beaster sions. Nor is any liability assumed for damages resulting from the Copy Editor use of the information contained herein. Patricia Kinyon International Standard Book Number: 0-672-31882-2 Indexer Library of Congress Catalog Card Number: 99-69443 Greg Pearson Printed in the United States of America Proofreader First Printing: February, 2000 Candice Hightower 03 02 01 00 Team Coordinator 4 3 2 1 Amy Patton Interior Designer Trademarks Gary Adair All terms mentioned in this book that are known to be trademarks Cover Designer or service marks have been appropriately capitalized. Sams cannot Jay Corpus attest to the accuracy of this information. Use of a term in this book Copywriter should not be regarded as affecting the validity of any trademark or Eric Borgert service mark. Editorial Assistant Warning and Disclaimer Angela Boley Every effort has been made to make this book as complete and as accurate as possible, but no warranty or fitness is implied. -

August 2014 Software Business Services Internet & Digital Media

The Lighthouse August 2014 Software Business Services Internet & Digital Media A Pharus Advisors, LLC Publication | www.pharus.com August 2014 Software & Business Services Internet & Digital Media Table of Contents 1. Capital Market Trends 3 2. Public Market Valuations 4 3. Public Market Universe 13 4. M&A Transactions 15 5. Recent Transactions 23 6. Pharus Overview 24 If you would like to be included on (or removed from) the distribution list for the Software & Services version of The Lighthouse, please contact Nathan Bullock at: [email protected]. The information contained herein is obtained from sources we believe to be reliable but its accuracy and completeness, and that of the opinions based thereon, is not guaranteed. Pharus Advisors, or one or more of its partners, may have an interest in any of the securities or companies discussed herein. All rights reserved by Pharus Advisors. LLC. 2014 Copyright Pharus Advisors, LLC. Executive Contacts Telephone Email Michael E. Goodman, Co-Founder & Sr. Managing Director 212-904-0102 [email protected] Kenneth M. Harrell, Co- Founder & Sr. Managing Director 212-904-0101 [email protected] Pharus Advisors, LLC | www.pharus.com 2 August 2014 Software & Business Services Internet & Digital Media 1. Capital Market Trends Relative Performance of Major Stock Indices through August 31, 2014 (Base = 100, 7/31/2013) 140 130 120 110 100 90 Dow Jones Industrial Average (^DJI) - Index Value NASDAQ Composite Index (^COMP) - Index Value S&P 500 Index (^SPX) - Index Value Russell 2000 Index (^RUT) - Index Value As of Change % Index 31-Aug-14 1 Year 3 Months 1 Month Dow Jones 17,098.45 15.4% 2.3% 3.2% Nasdaq 4,580.27 27.6% 8.0% 4.8% S&P 500 2,003.37 22.7% 4.1% 3.8% Russell 2000 1,174.35 16.2% 3.5% 4.8% Pharus Advisors, LLC | www.pharus.com 3 August 2014 Software & Business Services Internet & Digital Media 2.