BANK and BANKING E-Banking Managing Your Money And

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

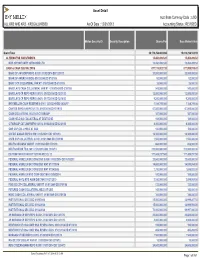

Asset Detail Acct Base Currency Code : USD ALL KR2 and KR3 - KR2GALLKRS00 As of Date : 12/31/2013 Accounting Status : REVISED

Asset Detail Acct Base Currency Code : USD ALL KR2 AND KR3 - KR2GALLKRS00 As Of Date : 12/31/2013 Accounting Status : REVISED . Mellon Security ID Security Description Shares/Par Base Market Value Grand Total 36,179,254,463.894 15,610,214,163.19 ALTERNATIVE INVESTMENTS 15,450,499.520 15,450,499.52 MKP OPPORTUNITY OFFSHORE LTD 15,450,499.520 15,450,499.52 CASH & CASH EQUIVALENTS 877,174,023.720 877,959,915.42 BANC OF AM CORP REPO 0.010% 01/02/2014 DD 12/31/13 20,000,000.000 20,000,000.00 BANK OF AMERICA (BOA) 01/01/2049 DD 07/01/08 52,000.000 52,000.00 BARC CCP COLLATERAL VAR RT 01/01/2049 DD 07/01/08 28,000.000 28,000.00 BARCLAYS CASH COLLATERAL VAR RT 01/01/2049 DD 07/01/08 543,000.000 543,000.00 BARCLAYS CP REPO REPO 0.010% 01/02/2014 DD 12/31/13 12,000,000.000 12,000,000.00 BARCLAYS CP REPO REPO 0.040% 01/17/2014 DD 12/18/13 9,200,000.000 9,200,000.00 BNY MELLON CASH RESERVE 0.010% 12/31/2049 DD 06/26/97 1,184,749.080 1,184,749.08 CANTOR REPO A REPO 0.170% 01/02/2014 DD 12/19/13 67,000,000.000 67,000,000.00 CASH COLLATERAL HELD AT CITIGROUP 387,000.000 387,000.00 CASH HELD AS COLLATERAL AT DEUTSCHE 169,000.000 169,000.00 CITIGROUP CAT 2MM REPO 0.010% 01/02/2014 DD 12/31/13 8,300,000.000 8,300,000.00 CME CCP COLL HELD AT GSC 100,000.000 100,000.00 CREDIT SUISSE REPO 0.010% 01/02/2014 DD 12/31/13 16,300,000.000 16,300,000.00 CSFB CCP COLLATERAL 0.010% 01/01/2049 DD 07/01/08 1,553,000.000 1,553,000.00 DEUTSCHE BANK VAR RT 01/01/2049 DD 07/01/08 668,000.000 668,000.00 DEUTSCHE BK TD 0.180% 01/02/2014 DD 12/18/13 270,000,000.000 270,000,000.00 -

6709BWOL Webstock

RIDING THE WEB-STOCK ROLLER COASTER Reprinted from the August 12, 2004 issue of BusinessWeek Online. Copyright © 2004 by The McGraw-Hill Companies. This reprint implies no endorsement, either tacit or expressed, of any company, product, service or investment opportunity. RIDING THE WEB-STOCK ROLLER COASTER Our BW Web 20 Index tracks a selection of favorite Net stocks, and this column will help interpret the ups and downs he past month has been rotten Just last week, Forrester Research christening the BW Web 20 Index Tfor Internet investors. Stocks raised its e-commerce forecast, pre- – is intended to help aggressive have been hammered since second- dicting U.S. online sales of $227 bil- investors accept the risk inherent in quarter earnings showed Web out- lion in 2007, up from earlier projec- the Web, but balance it by focusing fits growing pretty much as they had tions of $204 billion. Forrester on “real” companies with solid prod- promised – a change from their habit expects e-commerce in the U.S. to ucts, services, and profits. Every of slightly besting quarterly projec- grow 14% annually through 2010 – month, this column will do more than tions. The carnage has been just as three to four times faster than the track how stocks in our index trade – severe in the Real World Internet economy. Meanwhile, growth in it also will help investors figure out Index, a group of Web stocks we Europe is predicted to average 33% which rallies are sustainable and spot picked in 2002 to help ordinary annually through 2009. the bubblicious behavior that earned investors play the Internet without Net investing a bad rap. -

Software Industry Financial Report Contents

The Software Industry Financial Report SOFTWARE INDUSTRY FINANCIAL REPORT CONTENTS About Software Equity Group Leaders in Software M&A 4 Extensive Global Reach 5 Software Industry Macroeconomics Global GDP 8 U.S. GDP and Unemployment 9 Global IT Spending 10 E-Commerce and Digital Advertising Spend 11 SEG Indices vs. Benchmark Indices 12 Public Software Financial and Valuation Performance The SEG Software Index 14 The SEG Software Index: Financial Performance 15-17 The SEG Software Index: Market Multiples 18-19 The SEG Software Index by Product Category 20 The SEG Software Index by Product Category: Financial Performance 21 The SEG Software Index by Product Category: Market Multiples 22 Public SaaS Company Financial and Valuation Performance The SEG SaaS Index 24 The SEG SaaS Index Detail 25 The SEG SaaS Index: Financial Performance 26-28 The SEG SaaS Index: Market Multiples 29-30 The SEG SaaS Index by Product Category 31 The SEG SaaS Index by Product Category: Financial Performance 32 The SEG SaaS Index by Product Category: Market Multiples 33 Public Internet Company Financial and Valuation Performance The SEG Internet Index 35 The SEG Internet Index: Financial Performance 36-38 The SEG Internet Index: Market Multiples 39-40 The SEG Internet Index by Product Category 41 The SEG Internet Index by Product Category: Financial Performance 42 The SEG Internet Index by Product Category: Market Multiples 43 1 Q3 2013 Software Industry Financial Report Copyright © 2013 by Software Equity Group, LLC All Rights Reserved SOFTWARE INDUSTRY FINANCIAL -

1 UNITED STATES SECURITIES and EXCHANGE COMMISSION Washington, D.C

1 UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 13F FORM 13F COVER PAGE Report for the Calendar Year or Quarter Ended: September 30, 2000 Check here if Amendment [ ]; Amendment Number: This Amendment (Check only one.): [ ] is a restatement. [ ] adds new holdings entries Institutional Investment Manager Filing this Report: Name: AMERICAN INTERNATIONAL GROUP, INC. Address: 70 Pine Street New York, New York 10270 Form 13F File Number: 28-219 The Institutional Investment Manager filing this report and the person by whom it is signed represent that the person signing the report is authorized to submit it, that all information contained herein is true, correct and complete, and that it is understood that all required items, statements, schedules, lists, and tables, are considered integral parts of this form. Person Signing this Report on Behalf of Reporting Manager: Name: Edward E. Matthews Title: Vice Chairman -- Investments and Financial Services Phone: (212) 770-7000 Signature, Place, and Date of Signing: /s/ Edward E. Matthews New York, New York November 14, 2000 - ------------------------------- ------------------------ ----------------- (Signature) (City, State) (Date) Report Type (Check only one.): [X] 13F HOLDINGS REPORT. (Check if all holdings of this reporting manager are reported in this report.) [ ] 13F NOTICE. (Check if no holdings reported are in this report, and all holdings are reported in this report and a portion are reported by other reporting manager(s).) [ ] 13F COMBINATION REPORT. (Check -

US Asian Wire Distribution Points

US Asian Wire Distribution Points NewMediaWire’s comprehensive US Asian Wire delivers your news to targeted media in the Asian American community. Reaches leading Asian−American media outlets and over 375 trades and magazines dealing with political, finance, education, community, lifestyle and legal issues impacting Asian Americans as well as Online databases and websites that feature or cover Asian−American news and issues and The Associated Press. Please note, NewMediaWire includes free distribution to trade publications and newsletters. Because these are unique to each industry, they are not included in the list below. To get your complete NewMediaWire distribution, please contact your NewMediaWire account representative at 310.492.4001. aahar Newspaper Adhra Pradesh Times Newspaper Afternoon Despatch and Courier Newspaper Agence Kampuchea Press Newspaper Akila Daily Newspaper Algorithmica Japonica Newspaper am730 Newspaper Anand Rupwate Newspaper Andhra News Newspaper Andrha Pradesh Times Newspaper ANTARA News Agency Newspaper ASAHI PASOCOM Newspaper ASAHI SHIMBUN Newspaper Asahi Shimbun Newspaper Asahi Shimbun International Satellite Ed Newspaper Asia Insurance Review Newspaper Asia Pacific Management News Newspaper Asia Source Newspaper ASIA TIMES Newspaper Asian Affairs: An American Review Newspaper Asian American Press Newspaper Asian American Times Online Newspaper Asian Enterprise Magazine Newspaper Asian Focus Newspaper Asian Fortune Newspaper Asian Herald Newspaper Asian Industrial Reporter Newspaper Asian Journal Newspaper -

August 2014 Software Business Services Internet & Digital Media

The Lighthouse August 2014 Software Business Services Internet & Digital Media A Pharus Advisors, LLC Publication | www.pharus.com August 2014 Software & Business Services Internet & Digital Media Table of Contents 1. Capital Market Trends 3 2. Public Market Valuations 4 3. Public Market Universe 13 4. M&A Transactions 15 5. Recent Transactions 23 6. Pharus Overview 24 If you would like to be included on (or removed from) the distribution list for the Software & Services version of The Lighthouse, please contact Nathan Bullock at: [email protected]. The information contained herein is obtained from sources we believe to be reliable but its accuracy and completeness, and that of the opinions based thereon, is not guaranteed. Pharus Advisors, or one or more of its partners, may have an interest in any of the securities or companies discussed herein. All rights reserved by Pharus Advisors. LLC. 2014 Copyright Pharus Advisors, LLC. Executive Contacts Telephone Email Michael E. Goodman, Co-Founder & Sr. Managing Director 212-904-0102 [email protected] Kenneth M. Harrell, Co- Founder & Sr. Managing Director 212-904-0101 [email protected] Pharus Advisors, LLC | www.pharus.com 2 August 2014 Software & Business Services Internet & Digital Media 1. Capital Market Trends Relative Performance of Major Stock Indices through August 31, 2014 (Base = 100, 7/31/2013) 140 130 120 110 100 90 Dow Jones Industrial Average (^DJI) - Index Value NASDAQ Composite Index (^COMP) - Index Value S&P 500 Index (^SPX) - Index Value Russell 2000 Index (^RUT) - Index Value As of Change % Index 31-Aug-14 1 Year 3 Months 1 Month Dow Jones 17,098.45 15.4% 2.3% 3.2% Nasdaq 4,580.27 27.6% 8.0% 4.8% S&P 500 2,003.37 22.7% 4.1% 3.8% Russell 2000 1,174.35 16.2% 3.5% 4.8% Pharus Advisors, LLC | www.pharus.com 3 August 2014 Software & Business Services Internet & Digital Media 2. -

Merrill Lynch Security Risk Evaluation 1-07

Security Risk Evaluation ALPHA January 2007 Price As of December 2006 Month End COPYRIGHT 1998 MERRILL LYNCH, PIERCE, FENNER & SMITH INCORPORATED (MLPF&S). APPROVED FOR PUBLICATION IN THE UNITED KINGDOM BY MERRILL LYNCH, PIERCE, FENNER & SMITH LIMITED, AN AFFILIATED COMPANY AND REGULATED BY THE SECURITIES AND FUTURES AUTHORITY LIMITED. THE INFORMATION HEREIN WAS OBTAINED FROM VARIOUS SOURCES; WE DO NOT GUARANTEE ITS ACCURACY. ADDITIONAL INFORMATION AVAILABLE. GLOBAL SECURITIES RESEARCH & ECONOMICS RESEARCH TECHNOLOGY ALPHA (1) 800 255-9107 CONTINENTAL UNITED STATES January 2007 (1) 212 449-1072 WORLD WIDE PRICE AS OF December 2006 MONTH END Merrill Lynch, Pierce, Fenner & Smith, Inc. Market Sensitivity Statistics 2006/ 12 Resid Number Ticker Close Std --Std Error-- Adjusted Of Symbol Security Name Price Beta Alpha R-Sqr Dev-n Beta Alpha Beta Observ DOWI DOW JONES & CO 30 INDUSTRIALS 12463.150 0.96 0.03 0.91 1.09 0.04 0.14 0.98 60 DJ 20 DOW JONES & CO 20 TRANS ACTUAL 4560.200 0.94 0.65 0.42 3.86 0.14 0.50 0.96 60 DJ 15 DOW JONES & CO 15 UTIL ACTUAL 456.770 0.57 0.60 0.19 4.12 0.15 0.54 0.72 60 DJ 65 DOW JONES & CO 65 STOCK COMPOSITE 4120.960 0.89 0.28 0.86 1.29 0.05 0.17 0.93 60 SPALNS S&P 500 500 STOCKS 1418.300 1.00 0.00 1.00 0.00 0.00 0.00 1.00 60 Based on S&P 500 Index Using Straight Regression Merrill Lynch, Pierce, Fenner & Smith, Inc. -

Efinance ENABLERS: EFFICIENTLY MOVING the BUCK

REVISED 10-19-00 eFINANCE ENABLERS: EFFICIENTLY MOVING THE BUCK Jeffery B. Baker [email protected] 415.551.8600 Stephen A. Laws [email protected] REVISED 10-19-00 eFinance Enablers: Efficiently Moving the Buck TABLE OF CONTENTS Executive Summary....................................................................................... 3 Industry Report.............................................................................................. 6 Initiating Coverage ...................................................................................... 36 CheckFree Holdings (CKFR)....................................................................................... 37 The InterCept Group (ICPT) ....................................................................................... 48 S1 Corp. (SONE)......................................................................................................... 58 Company Profiles ....................................................................................... 72 Financial Enterprise Enablers ...................................................................................... 73 Electronic Bill Presentment and Payment..................................................................... 91 Data Processors ......................................................................................................... 111 Payment Processors ................................................................................................... 118 Payment Enablers ..................................................................................................... -

List of Section 13F Securities, Third Quarter 2001

OFFICIAL LIST OF SECTION 13(F) SECURITIES USER INFORMATION SHEET General This list of "Section 13(f) securities" as defined by Rule 13f-I(c) [I7 CFR 240.13f-I (c)] is made available to the public pursuant to Section13 (f) (3) of the Securities Exchange Act of 1934 [I5 USC 78m(f) (3)]. It is made available for use in the preparation of reports filed with the Securities and Exhange Commission pursuant to Rule 13f-1 117 CFR 240.1 3f-I] under Section 13(f) of the Securities Exchange Act of 1934. An updated list is published on a quarterly basis. This list is current as of September, 15, 2001 ,and may be relied on by institutional investment managers filing Form 13F reports for the calendar quarter ending September 30, 2001 . Institutional investment managers should report holdings--number of shares and fair market value--as of the last day of the calendar quarter as required by [ Section 13(f)(l) and Rule 13f-I] thereunder. Features (1 ) Additions and Deletions: Revisions made to the list of Section 13(f) securities are indicated in a column titled "STATUS." The word "ADDED" in the status column opposite the name of a security indicates that the security has become a Section 13(f) security. The word "DELE-TED" in the status colurr~nopposite the name of a security indicates that the security ceases to be a 13(f) security since the date of the last list. (2) List of options: An asterisk is placed next to the name of any security having a listed option and each option is individually listed with its own CUSlP nurr~berimmediately below the name of the security having the option. -

African American Newsline Distribution Points

African American Newsline Distribution Points Deliver your targeted news efficiently and effectively through NewMediaWire’s African−American Newsline. Reach 700 leading trades and journalists dealing with political, finance, education, community, lifestyle and legal issues impacting African Americans as well as The Associated Press and Online databases and websites that feature or cover African−American news and issues. Please note, NewMediaWire includes free distribution to trade publications and newsletters. Because these are unique to each industry, they are not included in the list below. To get your complete NewMediaWire distribution, please contact your NewMediaWire account representative at 310.492.4001. A.C.C. News Weekly Newspaper African American AIDS Policy &Training Newsletter African American News &Issues Newspaper African American Observer Newspaper African American Times Weekly Newspaper AIM Community News Weekly Newspaper Albany−Southwest Georgian Newspaper Alexandria News Weekly Weekly Newspaper Amen Outreach Newsletter Newsletter Annapolis Times Newspaper Arizona Informant Weekly Newspaper Around Montgomery County Newspaper Atlanta Daily World Weekly Newspaper Atlanta Journal Constitution Newspaper Atlanta News Leader Newspaper Atlanta Voice Weekly Newspaper AUC Digest Newspaper Austin Villager Newspaper Austin Weekly News Newspaper Bakersfield News Observer Weekly Newspaper Baton Rouge Weekly Press Weekly Newspaper Bay State Banner Newspaper Belgrave News Newspaper Berkeley Tri−City Post Newspaper Berkley Tri−City Post -

SECURITIES and EXCHANGE COMMISSION Washington D.C

SECURITIES AND EXCHANGE COMMISSION Washington D.C. 20549 FORM 11-K FOR ANNUAL REPORTS OF EMPLOYEE STOCK PURCHASE, SAVINGS AND SIMILAR PLANS PURSUANT TO SECTION 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 (Mark One) [ x ] ANNUAL REPORT PURSUANT TO SECTION 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the month ended December 31, 2001 OR [ ] TRANSITION REPORT PURSUANT TO SECTION 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from ___ to ___ Commission File No. 1 - 6033 A. United Air Lines, Inc. Pilots' Directed Account Retirement Income Plan (Full title of the Plan) United Air Lines, Inc. (Employer sponsoring the Plan) B. UAL Corporation (Issuer of the shares held pursuant to the Plan) 1200 Algonquin Road, Elk Grove Township, Illinois Mailing Address: P.O. Box 66100, Chicago, Illinois 60666 (Address of principal executive offices) REPORT OF INDEPENDENT PUBLIC ACCOUNTANTS To the Board of Directors of United Air Lines, Inc. Pilots' Directed Account Retirement Income Plan: We have audited the accompanying statements of net assets available for plan benefits of the United Air Lines, Inc. Pilots' Directed Account Retirement Income Plan as of December 31, 2001 and November 30, 2001, and the related statements of changes in net assets available for plan benefits for the month ended December 31, 2001. These financial statements are the responsibility of the Plan's management. Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits in accordance with auditing standards generally accepted in the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. -

GAO-03-395R Financial Statement Restatement Database

United States General Accounting Office Washington, DC 20548 January 17, 2003 The Honorable Paul S. Sarbanes Ranking Minority Member Committee on Banking, Housing, and Urban Affairs United States Senate Subject: Financial Statement Restatement Database On October 4, 2002, we issued a report to you entitled Financial Statement Restatements: Trends, Market Impacts, Regulatory Responses, and Remaining Challenges (Washington, D.C.: GAO-03-138). That report included a listing of 919 restatements we identified as having been made because of accounting irregularities between January 1, 1997, and June 30, 2002. Since its release, the report has drawn considerable attention from academics and other researchers, and we have received numerous requests for additional data about these restatements. As a result, and with the agreement of your office, we are releasing our database of information collected from public sources on the 919 restatements. We encourage researchers and the public to consider our objectives, scope, and methodology (enclosure I) and engage in their own analyses of the data contained in our restatements database (enclosure II). In addition to providing the name of each company associated with a restatement announcement, we are including the company’s stock ticker symbol, the market on which the stock was trading at the time of the announcement, the date of the announcement, the entity that prompted the restatement, and the reason(s) for the restatement. We are not releasing stock price or market capitalization data, since we obtained this information from proprietary sources, but we are including the number of shares outstanding for each company. As we stated in our October report, certain of these items, such as the entity that prompted the restatement and the reason for the restatement, are subject to interpretation, and other researchers may categorize certain restatements differently.