Merrill Lynch Security Risk Evaluation 1-07

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

List of Marginable OTC Stocks

List of Marginable OTC Stocks @ENTERTAINMENT, INC. ABACAN RESOURCE CORPORATION ACE CASH EXPRESS, INC. $.01 par common No par common $.01 par common 1ST BANCORP (Indiana) ABACUS DIRECT CORPORATION ACE*COMM CORPORATION $1.00 par common $.001 par common $.01 par common 1ST BERGEN BANCORP ABAXIS, INC. ACETO CORPORATION No par common No par common $.01 par common 1ST SOURCE CORPORATION ABC BANCORP (Georgia) ACMAT CORPORATION $1.00 par common $1.00 par common Class A, no par common Fixed rate cumulative trust preferred securities of 1st Source Capital ABC DISPENSING TECHNOLOGIES, INC. ACORN PRODUCTS, INC. Floating rate cumulative trust preferred $.01 par common $.001 par common securities of 1st Source ABC RAIL PRODUCTS CORPORATION ACRES GAMING INCORPORATED 3-D GEOPHYSICAL, INC. $.01 par common $.01 par common $.01 par common ABER RESOURCES LTD. ACRODYNE COMMUNICATIONS, INC. 3-D SYSTEMS CORPORATION No par common $.01 par common $.001 par common ABIGAIL ADAMS NATIONAL BANCORP, INC. †ACSYS, INC. 3COM CORPORATION $.01 par common No par common No par common ABINGTON BANCORP, INC. (Massachusetts) ACT MANUFACTURING, INC. 3D LABS INC. LIMITED $.10 par common $.01 par common $.01 par common ABIOMED, INC. ACT NETWORKS, INC. 3DFX INTERACTIVE, INC. $.01 par common $.01 par common No par common ABLE TELCOM HOLDING CORPORATION ACT TELECONFERENCING, INC. 3DO COMPANY, THE $.001 par common No par common $.01 par common ABR INFORMATION SERVICES INC. ACTEL CORPORATION 3DX TECHNOLOGIES, INC. $.01 par common $.001 par common $.01 par common ABRAMS INDUSTRIES, INC. ACTION PERFORMANCE COMPANIES, INC. 4 KIDS ENTERTAINMENT, INC. $1.00 par common $.01 par common $.01 par common 4FRONT TECHNOLOGIES, INC. -

2016-2017 U of a Career Outcomes Report.Pdf

2016-2017 [CAREER OUTCOMES REPORT] Career Outcomes Report 2016-2017 1 2016-2017 [CAREER OUTCOMES REPORT] Table of Contents Introduction and Methodology .............................................................................. 3 Definitions ........................................................................................................................................................... 3 Class of 2017 Survey Summary .............................................................................. 4 Status of the Survey Respondents ......................................................................... 4 Class of 2017 Career Outcomes ............................................................................. 5 Placement Rates for those seeking placement....................................................... 6 Salary Statistics ...................................................................................................... 6 U of A Overall Reported Starting Salary ................................................................................................... 6 Salary Means and Medians for Selected Majors .................................................................................... 6 Continuing Education Study Fields ......................................................................... 8 Career Outcomes for Different Student Affiliations ............................................... 8 Placement Status by Undergraduate Student Groups ....................................................................... -

"Trendy" Wireless Phones Most Likely to Be Researched Online; Low-Cost Models Most Often Ordered

"Trendy" Wireless Phones Most Likely To Be Researched Online; Low-Cost Models Most Often Ordered Motorola RAZR V3C Tops the List of Most Researched Wireless Phones; Sony Ericsson Z520A Most Frequently Ordered Online, with More than Two-Thirds at No Cost to the Consumer "Trendy" Wireless Phones Most Likely To Be Researched Online; Low-Cost Models Most Often Ordered RESTON, VA. June 12, 2006 - comScore Networks, a leader in the measurement and analysis of consumer behavior and attitudes, today released an analysis of the online research and purchase behavior of consumers in the wireless phone market. comScore revealed that consumers were most likely to research newly released and "trendy" models, with the Motorola RAZR V3C topping the list during the first quarter of 2006. Other models securing spots on the most researched list include the Palm Treo 650, the Palm Treo 700W, and the Motorola Pebl. Top 10 Wireless Phones Researched Online First Quarter 2006 Source: comScore Networks Manufacturer Model Motorola Razr V3C Palm Treo 650 Motorola E815 Palm Treo 700W Motorola Razr V3 Samsung A900 Motorola Pebl Sony Ericsson Z520A Nokia 6101/6102 LG C2000 The Motorola Q is the latest phone to be released, with Verizon Wireless positioned as sole provider of this model for a limited time. As a measure of interest in the model, comScore found that the Motorola Q product page on the Verizon Wireless Web site received slightly more than 100,000 unique visitors in the second half of May, 2006. Price is a Driving Factor When Purchasing a Phone comScore also analyzed trends in ordering cell phones online, among new and existing customers, at major carrier and wireless sites in the first quarter of 2006. -

Benetton Group Spa Rating Change UNDERPERFORM

Benetton Group Spa Rating Change UNDERPERFORM Equity | Italy | Apparel 15 November 2010 Faded colours Flavio Cereda >> +44 20 7996 1455 Research Analyst MLPF&S (UK) Downgrading BEN to Underperform: PO cut 17% to €5.0 [email protected] We believe BEN has become a value trap, we thought the stock had reached a floor of sorts after H110: it does not appear so. A poor Q3 combined with deteriorating news flow has returned the stock to its previous predicament, in our Stock Data view: how do I deal with competitors that are bigger, better and more appealing Price EUR5.10 than me? BEN’s inability to generate any real growth this year in spite of the Price Objective EUR5.00 recent restructuring effort (mgmt estimate €50mn net benefits at the EBIT level as Date Established 15-Nov-2010 a result) and peer performance, flags a troubling lack of brand appeal, in our view, Investment Opinion B-3-7 Volatility Risk MEDIUM that we fear will take some time to redress given a challenging 2011-12. 52-Week Range EUR5.06-EUR6.97 Beyond cotton…between a rock and a hard place… Mrkt Val / Shares Out (mn) EUR931 / 182.7 We think BEN will be struggling with a number of very key issues in the MT: over- Average Daily Volume 297,628 reliance on a stagnant and increasingly competitive domestic market (46%), BofAML Ticker / Exchange BNTOF / MIL Bloomberg / Reuters BEN IM / BNG.MI soaring input costs (a first toll in Q4-10 and H1-11), the need to continue to run a ROE (2010E) 7.4% ‘nice price’ policy with many of its retail clients, relatively small exposure to Asia Net Dbt to Eqty (Dec-2009A) 38.4% (16%) and China in particular, and what appears to be a troubling lack of profile in Est. -

Tuesday July 30, 1996

7±30±96 Tuesday Vol. 61 No. 147 July 30, 1996 Pages 39555±39838 federal register 1 II Federal Register / Vol. 61, No. 147 / Tuesday, July 30, 1996 SUBSCRIPTIONS AND COPIES PUBLIC Subscriptions: Paper or fiche 202±512±1800 FEDERAL REGISTER Published daily, Monday through Friday, Assistance with public subscriptions 512±1806 (not published on Saturdays, Sundays, or on official holidays), by General online information 202±512±1530 the Office of the Federal Register, National Archives and Records Administration, Washington, DC 20408, under the Federal Register Single copies/back copies: Act (49 Stat. 500, as amended; 44 U.S.C. Ch. 15) and the Paper or fiche 512±1800 regulations of the Administrative Committee of the Federal Register Assistance with public single copies 512±1803 (1 CFR Ch. I). Distribution is made only by the Superintendent of Documents, U.S. Government Printing Office, Washington, DC FEDERAL AGENCIES 20402. Subscriptions: The Federal Register provides a uniform system for making Paper or fiche 523±5243 available to the public regulations and legal notices issued by Assistance with Federal agency subscriptions 523±5243 Federal agencies. These include Presidential proclamations and For other telephone numbers, see the Reader Aids section Executive Orders and Federal agency documents having general applicability and legal effect, documents required to be published at the end of this issue. by act of Congress and other Federal agency documents of public interest. Documents are on file for public inspection in the Office of the Federal Register the day before they are published, unless earlier filing is requested by the issuing agency. -

Encrypted Traffic Management for Dummies®, Blue Coat Systems Special Edition Published by John Wiley & Sons, Inc

These materials are © 2015 John Wiley & Sons, Inc. Any dissemination, distribution, or unauthorized use is strictly prohibited. Encrypted Traffic Management Blue Coat Systems Special Edition by Steve Piper, CISSP These materials are © 2015 John Wiley & Sons, Inc. Any dissemination, distribution, or unauthorized use is strictly prohibited. Encrypted Traffic Management For Dummies®, Blue Coat Systems Special Edition Published by John Wiley & Sons, Inc. 111 River St. Hoboken, NJ 07030‐5774 www.wiley.com Copyright © 2015 by John Wiley & Sons, Inc., Hoboken, New Jersey No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanical, photocopying, recording, scanning or otherwise, except as permitted under Sections 107 or 108 of the 1976 United States Copyright Act, without the prior written permission of the Publisher. Requests to the Publisher for permission should be addressed to the Permissions Department, John Wiley & Sons, Inc., 111 River Street, Hoboken, NJ 07030, (201) 748‐6011, fax (201) 748‐6008, or online at http://www.wiley.com/go/permissions. Trademarks: Wiley, For Dummies, the Dummies Man logo, The Dummies Way, Dummies.com, Making Everything Easier, and related trade dress are trademarks or registered trademarks of John Wiley & Sons, Inc. and/or its affiliates in the United States and other countries, and may not be used without written permission. Blue Coat Systems and the Blue Coat logo are trademarks or registered trade- marks of Blue Coat Systems, Inc. All other trademarks are the property of their respective owners. John Wiley & Sons, Inc., is not associated with any product or vendor mentioned in this book. -

Annual Report 2004

04 Bringing growth into focus. Annual Report 2004. 04 a successful year for Continental. 2 2 Continental Corporation in € millions 2004 2003 2002 2001 2000 Sales 12,597.4 11,534.4 11,408.3 11,233.3 10,115.0 EBITA¹ 1,096.4 855.2 694.3 32.8 533.0 Consolidated net income/loss for the year 673.8 314.0 226.0 - 257.6 204.7 Dividends 116.3² 70.4 58.6 – 64.1 Cash flow 1,443.8 985.9 919.0 666.5 866.3 Capital expenditure on property, plant, and equipment 672.4 583.5 581.2 704.9 682.8 Amortization and depreciation³ 665.7 603.1 670.3 891.3 654.7 Shareholders’ equity 2,842.3 1,983.2 1,715.2 1,546.7 1,844.1 Equity ratio in % 29.4 23.9 20.9 17.2 24.2 Employees at the end of the year 4 80,586 68,829 64,379 65,293 63,832 Share price (high) in € 47.26 30.98 19.53 19.45 20.94 Share price (low) in € 28.87 12.04 11.72 9.68 15.85 ¹ Earnings before interest, taxes and regular goodwill amortization ² Subject to the approval of the Annual Shareholders’ Meeting on May 12, 2005 ³ Excluding write-downs of investments 4 Excluding trainees Continental Divisions Sales in € millions 2004 2003 Automotive Systems 5,007.7 4,625.7 Passenger and Light Truck Tires 4,104.2 3,907.2 Commercial Vehicle Tires 1,500.7 1,261.6 ContiTech 2,063.4 1,812.2 EBIT in € millions 2004 2003 Automotive Systems 487.5 369.5 Passenger and Light Truck Tires 383.4 345.8 Commercial Vehicle Tires 100.3 82.4 ContiTech 150.4 144.0 Bringing growth into focus. -

WHITE PAPER Encrypted Traffic Management January 2016

FRAUNHOFER INSTITUTE FOR COMMUNICATION, INFORMATION PROCESSIN G AND ERGONOMICS FKI E WHITE PAPER ENCRYPTED TRAFFIC MANAGEMENT WHITE PAPER Encrypted Traffic Management January 2016 Raphael Ernst Martin Lambertz Fraunhofer Institute for Communication, Information Processing and Ergonomics FKIE in Wachtberg and Bonn. Project number: 108146 Project partner: Blue Coat Systems Inc. Fraunhofer FKIE White paper Encrypted Traffic Management 3 | 33 Contents 1 Introduction .......................................................................................... 5 2 The spread of SSL ................................................................................. 6 3 Safety issues in previous versions of SSL ............................................... 8 4 Malware and SSL ................................................................................... 9 5 Encrypted Traffic Management .............................................................. 11 5.1 Privacy ...................................................................................................................... 12 5.1.1 Requirements ............................................................................................................ 12 5.2 Compatibility ............................................................................................................ 12 5.2.1 Requirements ............................................................................................................ 12 5.3 Performance ............................................................................................................ -

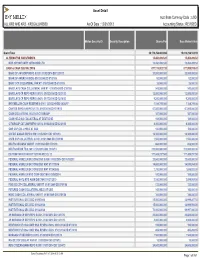

Asset Detail Acct Base Currency Code : USD ALL KR2 and KR3 - KR2GALLKRS00 As of Date : 12/31/2013 Accounting Status : REVISED

Asset Detail Acct Base Currency Code : USD ALL KR2 AND KR3 - KR2GALLKRS00 As Of Date : 12/31/2013 Accounting Status : REVISED . Mellon Security ID Security Description Shares/Par Base Market Value Grand Total 36,179,254,463.894 15,610,214,163.19 ALTERNATIVE INVESTMENTS 15,450,499.520 15,450,499.52 MKP OPPORTUNITY OFFSHORE LTD 15,450,499.520 15,450,499.52 CASH & CASH EQUIVALENTS 877,174,023.720 877,959,915.42 BANC OF AM CORP REPO 0.010% 01/02/2014 DD 12/31/13 20,000,000.000 20,000,000.00 BANK OF AMERICA (BOA) 01/01/2049 DD 07/01/08 52,000.000 52,000.00 BARC CCP COLLATERAL VAR RT 01/01/2049 DD 07/01/08 28,000.000 28,000.00 BARCLAYS CASH COLLATERAL VAR RT 01/01/2049 DD 07/01/08 543,000.000 543,000.00 BARCLAYS CP REPO REPO 0.010% 01/02/2014 DD 12/31/13 12,000,000.000 12,000,000.00 BARCLAYS CP REPO REPO 0.040% 01/17/2014 DD 12/18/13 9,200,000.000 9,200,000.00 BNY MELLON CASH RESERVE 0.010% 12/31/2049 DD 06/26/97 1,184,749.080 1,184,749.08 CANTOR REPO A REPO 0.170% 01/02/2014 DD 12/19/13 67,000,000.000 67,000,000.00 CASH COLLATERAL HELD AT CITIGROUP 387,000.000 387,000.00 CASH HELD AS COLLATERAL AT DEUTSCHE 169,000.000 169,000.00 CITIGROUP CAT 2MM REPO 0.010% 01/02/2014 DD 12/31/13 8,300,000.000 8,300,000.00 CME CCP COLL HELD AT GSC 100,000.000 100,000.00 CREDIT SUISSE REPO 0.010% 01/02/2014 DD 12/31/13 16,300,000.000 16,300,000.00 CSFB CCP COLLATERAL 0.010% 01/01/2049 DD 07/01/08 1,553,000.000 1,553,000.00 DEUTSCHE BANK VAR RT 01/01/2049 DD 07/01/08 668,000.000 668,000.00 DEUTSCHE BK TD 0.180% 01/02/2014 DD 12/18/13 270,000,000.000 270,000,000.00 -

List of Section 13F Securities

List of Section 13F Securities 1st Quarter FY 2004 Copyright (c) 2004 American Bankers Association. CUSIP Numbers and descriptions are used with permission by Standard & Poors CUSIP Service Bureau, a division of The McGraw-Hill Companies, Inc. All rights reserved. No redistribution without permission from Standard & Poors CUSIP Service Bureau. Standard & Poors CUSIP Service Bureau does not guarantee the accuracy or completeness of the CUSIP Numbers and standard descriptions included herein and neither the American Bankers Association nor Standard & Poor's CUSIP Service Bureau shall be responsible for any errors, omissions or damages arising out of the use of such information. U.S. Securities and Exchange Commission OFFICIAL LIST OF SECTION 13(f) SECURITIES USER INFORMATION SHEET General This list of “Section 13(f) securities” as defined by Rule 13f-1(c) [17 CFR 240.13f-1(c)] is made available to the public pursuant to Section13 (f) (3) of the Securities Exchange Act of 1934 [15 USC 78m(f) (3)]. It is made available for use in the preparation of reports filed with the Securities and Exhange Commission pursuant to Rule 13f-1 [17 CFR 240.13f-1] under Section 13(f) of the Securities Exchange Act of 1934. An updated list is published on a quarterly basis. This list is current as of March 15, 2004, and may be relied on by institutional investment managers filing Form 13F reports for the calendar quarter ending March 31, 2004. Institutional investment managers should report holdings--number of shares and fair market value--as of the last day of the calendar quarter as required by Section 13(f)(1) and Rule 13f-1 thereunder. -

Schedule 14A

DEFA14A 1 a06-22752_2defa14a.htm DEFINITIVE PROXY STATEMENT RELATING TO MERGER OR ACQUISITION UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 SCHEDULE 14A Proxy Statement Pursuant to Section 14(a) of the Securities Exchange Act of 1934 (Amendment No. ) Filed by the Registrant ⌧ Filed by a Party other than the Registrant Check the appropriate box: Preliminary Proxy Statement Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) Definitive Proxy Statement Definitive Additional Materials ⌧ Soliciting Material Pursuant to §240.14a-12 KANBAY INTERNATIONAL, INC. (Name of Registrant as Specified In Its Charter) (Name of Person(s) Filing Proxy Statement, if other than the Registrant) Payment of Filing Fee (Check the appropriate box): ⌧ No fee required. Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. (1) Title of each class of securities to which transaction applies: (2) Aggregate number of securities to which transaction applies: (3) Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): (4) Proposed maximum aggregate value of transaction: (5) Total fee paid: Fee paid previously with preliminary materials. Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. -

6709BWOL Webstock

RIDING THE WEB-STOCK ROLLER COASTER Reprinted from the August 12, 2004 issue of BusinessWeek Online. Copyright © 2004 by The McGraw-Hill Companies. This reprint implies no endorsement, either tacit or expressed, of any company, product, service or investment opportunity. RIDING THE WEB-STOCK ROLLER COASTER Our BW Web 20 Index tracks a selection of favorite Net stocks, and this column will help interpret the ups and downs he past month has been rotten Just last week, Forrester Research christening the BW Web 20 Index Tfor Internet investors. Stocks raised its e-commerce forecast, pre- – is intended to help aggressive have been hammered since second- dicting U.S. online sales of $227 bil- investors accept the risk inherent in quarter earnings showed Web out- lion in 2007, up from earlier projec- the Web, but balance it by focusing fits growing pretty much as they had tions of $204 billion. Forrester on “real” companies with solid prod- promised – a change from their habit expects e-commerce in the U.S. to ucts, services, and profits. Every of slightly besting quarterly projec- grow 14% annually through 2010 – month, this column will do more than tions. The carnage has been just as three to four times faster than the track how stocks in our index trade – severe in the Real World Internet economy. Meanwhile, growth in it also will help investors figure out Index, a group of Web stocks we Europe is predicted to average 33% which rallies are sustainable and spot picked in 2002 to help ordinary annually through 2009. the bubblicious behavior that earned investors play the Internet without Net investing a bad rap.