Exhibit II-39 Table of Contents

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

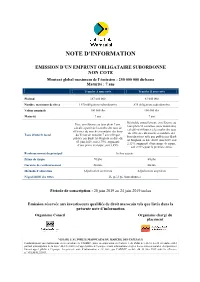

Note D'information

NOTE D’INFORMATION EMISSION D’UN EMPRUNT OBLIGATAIRE SUBORDONNE NON COTE Montant global maximum de l’émission : 250 000 000 dirhams Maturité : 7 ans Tranche A non cotée Tranche B non cotée Plafond 167 000 000 83 000 000 Nombre maximum de titres 1 670 obligations subordonnées 830 obligations subordonnées Valeur nominale 100 000 dhs 100 000 dhs Maturité 7 ans 7 ans Révisable annuellement, en référence au Fixe, en référence au taux plein 7 ans, taux plein 52 semaines (taux monétaire) calculé à partir de la courbe des taux de calculé en référence à la courbe des taux référence du marché secondaire des bons de référence du marché secondaire des Taux d’intérêt facial du Trésor de maturité 7 ans telle que bons du trésor telle que publiée par Bank publiée par Bank Al-Maghrib en date du Al-Maghrib en date du 03 juin 2019, soit 03 juin 2019, soit 2,75%, augmenté 2,31%, augmenté d’une prime de risque, d’une prime de risque, soit 3,45% soit 2,91% pour la première année Remboursement du principal In fine au pair Prime de risque 70 pbs 60 pbs Garantie de remboursement Aucune Aucune Méthode d’allocation Adjudication au prorata Adjudication au prorata Négociabilité des titres De gré à gré (hors Bourse) Période de souscription : 20 juin 2019 au 24 juin 2019 inclus Emission réservée aux investisseurs qualifiés de droit marocain tels que listés dans la présente note d’information Organisme Conseil Organisme chargé du placement VISA DE L’AUTORITE MAROCAINE DU MARCHE DES CAPITAUX Conformément aux dispositions de la circulaire de l’AMMC, prise en application de l’article 5 du Dahir n°1-12-55 du 28 décembre 2012 portant promulgation de la loi n° 44-12 relative à l’appel public à l’épargne et aux informations exigées des personnes morales et organismes faisant appel public à l’épargne, la présente note d’information a été visée par l’AMMC en date du 12 juin 2019 sous la référence n° VI/EM/012/2019. -

Al Akhawayn University in Ifrane 2013 - 2015 Catalog

Al Akhawayn University in Ifrane 2013 - 2015 Catalog www.aui.ma His Majesty King Mohammed VI at The George Washington University where he received an honorary doctorate on June 6, 2000. The university’s two founding brothers (Al Akhawayn). The late King Hassan II of Morocco and the late King Fahd Ibn Abdulaziz of Saudi Arabia. Table of Contents Message from the President. 4 Calendar . .5-6 Mission . 7 Core Values and Principles. 9 Board of Trustees. 14 University Administration . 16 Admissions and Enrollment . 19 Application Deadlines . .19 Undergraduate Admission . .20 Graduate Admission. 26 Deferred Enrollment . .31 Re-admission to the University . 32 Enrollment . .32 Financial Information . 36 Tuition, Fees, Deposits, and Refunds . .36 Financial Aid . .41 AUI Scholarships . 51 Academic Policies and Procedures. 57 Attendance . 57 Adding/Dropping Courses . .59 Withdrawing from the University . .60 Change of Degree Program . .62 Academic Integrity . .62 Final Examinations . .63 Grading Policy . 64 Undergraduate Academic Regulations . 70 Graduate Academic Regulations . .80 Student Support . 85 Student Services . 85 Academic Resources . .86 Mohammed VI Library . .86 The Writing Center . .87 Tutoring Services . .88 Student Life . 89 Degree Programs . 92 Degree Requirements. 93 Requirements for Bachelor’s Degrees . .93 University Core Curriculum . .93 Major Requirements . 98 Community Involvement Program . .101 Honors Program . 102 Language Center . 106 Al Akhawayn University in Ifrane 2013 - 2015 Catalog 1 Table of Contents School of Business Administration. 113 Undergraduate Prog rams . 113 Bachelor of Business Administration (BBA) . 113 Minors in the School of Business Administration . .120 Graduate Programs . 123 Master of Business Administration (MBA) . 123 Post-Experience Graduate Programs . 131 School of Humanities and Social Sciences . -

An N U Al R Ep O R T 2018 Annual Report

ANNUAL REPORT 2018 ANNUAL REPORT The Annual Report in English is a translation of the French Document de référence provided for information purposes. This translation is qualified in its entirety by reference to the Document de référence. The Annual Report is available on the Company’s website www.vivendi.com II –— VIVENDI –— ANNUAL REPORT 2018 –— –— VIVENDI –— ANNUAL REPORT 2018 –— 01 Content QUESTIONS FOR YANNICK BOLLORÉ AND ARNAUD DE PUYFONTAINE 02 PROFILE OF THE GROUP — STRATEGY AND VALUE CREATION — BUSINESSES, FINANCIAL COMMUNICATION, TAX POLICY AND REGULATORY ENVIRONMENT — NON-FINANCIAL PERFORMANCE 04 1. Profile of the Group 06 1 2. Strategy and Value Creation 12 3. Businesses – Financial Communication – Tax Policy and Regulatory Environment 24 4. Non-financial Performance 48 RISK FACTORS — INTERNAL CONTROL AND RISK MANAGEMENT — COMPLIANCE POLICY 96 1. Risk Factors 98 2. Internal Control and Risk Management 102 2 3. Compliance Policy 108 CORPORATE GOVERNANCE OF VIVENDI — COMPENSATION OF CORPORATE OFFICERS OF VIVENDI — GENERAL INFORMATION ABOUT THE COMPANY 112 1. Corporate Governance of Vivendi 114 2. Compensation of Corporate Officers of Vivendi 150 3 3. General Information about the Company 184 FINANCIAL REPORT — STATUTORY AUDITORS’ REPORT ON THE CONSOLIDATED FINANCIAL STATEMENTS — CONSOLIDATED FINANCIAL STATEMENTS — STATUTORY AUDITORS’ REPORT ON THE FINANCIAL STATEMENTS — STATUTORY FINANCIAL STATEMENTS 196 Key Consolidated Financial Data for the last five years 198 4 I – 2018 Financial Report 199 II – Appendix to the Financial Report 222 III – Audited Consolidated Financial Statements for the year ended December 31, 2018 223 IV – 2018 Statutory Financial Statements 319 RECENT EVENTS — OUTLOOK 358 1. Recent Events 360 5 2. Outlook 361 RESPONSIBILITY FOR AUDITING THE FINANCIAL STATEMENTS 362 1. -

Morocco: an Emerging Economic Force

Morocco: An Emerging Economic Force The kingdom is rapidly developing as a manufacturing export base, renewable energy hotspot and regional business hub OPPORTUNITIES SERIES NO.3 | DECEMBER 2019 TABLE OF CONTENTS SUMMARY 3 I. ECONOMIC FORECAST 4-10 1. An investment and export-led growth model 5-6 2. Industrial blueprint targets modernisation. 6-7 3. Reforms seek to attract foreign investment 7-9 3.1 Improvements to the business environment 8 3.2 Specific incentives 8 3.3 Infrastructure improvements 9 4. Limits to attractiveness 10 II. SECTOR OPPORTUNITIES 11-19 1. Export-orientated manufacturing 13-15 1.1 Established and emerging high-value-added industries 14 2. Renewable energy 15-16 3. Tourism 16-18 4. Logistics services 18-19 III. FOREIGN ECONOMIC RELATIONS 20-25 1. Africa strategy 20-23 1.1 Greater export opportunities on the continent 21 1.2 Securing raw material supplies 21-22 1.3 Facilitating trade between Africa and the rest of the world 22 1.4 Keeping Africa opportunities in perspective 22-23 2. China ties deepening 23-24 2.1 Potential influx of Chinese firms 23-24 2.2 Moroccan infrastructure to benefit 24 3 Qatar helping to mitigate reduction in gulf investment 24-25 IV. KEY RISKS 26-29 1. Social unrest and protest 26-28 1.1 2020 elections and risk of upsurge in protest 27-28 1.2 But risks should remain contained 28 2. Other important risks 29 2.1 Export demand disappoints 29 2.2 Exposure to bad loans in SSA 29 2.3 Upsurge in terrorism 29 SUMMARY Morocco will be a bright spot for investment in the MENA region over the next five years. -

S O N a S I D R a P P O R T a N N U

SONASID Rapport Annuel 2 0 1 0 [Rapport Annuel 2010] { S ommaire} 04 MESSAGE DU DIRECTEUR GÉNÉRAL 06 HISTORIQUE 07 PROFIL 09 CARNET DE L’ACTIONNAIRE 10 GOUVERNANCE 15 STRATÉGIE 19 ACTIVITÉ 25 RAPPORT SOCIAL 31 ÉLÉMENTS FINANCIERS 3 [Rapport Annuel 2010] Chers actionnaires, L’année 2010 a été particulièrement difficile pour l’ensemble Sonasid devrait en effet profiter d’un marché international des entreprises sidérurgiques au Maroc qui ont subi de favorable qui augure de bonnes perspectives avec la plein fouet à la fois les fluctuations d’un marché international prudence nécessaire, eu égard des événements récents Message du perturbé et la baisse locale des mises en chantier dans imprévisibles (Japon, monde arabe), mais une tendance { l’immobilier et le BTP. Une situation qui a entraîné une qui se confirme également sur le marché local qui devrait réduction de la consommation nationale du rond-à-béton bénéficier dès le second semestre 2011 de la relance des Directeur General qui est passée de 1500 kt en 2009 à 1400 kt en 2010. chantiers d’infrastructures et d’habitat social. } Un recul aggravé par la hausse des prix des matières premières, la ferraille notamment qui a représenté 70% du Nous sommes donc optimistes pour 2011 et mettrons prix de revient du rond-à-béton. Les grands consommateurs en œuvre toutes les mesures nécessaires pour y parvenir. d’acier sont responsables de cette inflation, la Chine en Nous avons déjà en 2010 effectué des progrès notables au particulier, au détriment de notre marché qui, mondialisé, a niveau de nos coûts de transformations, efforts que nous été directement affecté. -

Annual Report Annual Report

Twin Center, Tour A, Angle Boulevards Zerktouni et Al Massira Al Khadra BP 5199, Casablanca Tél : +212 5 22 59 65 65 - Email : [email protected] : /Managemgroup : @Managem_group : groupe-managem ANNUAL REPORT ANNUAL REPORT The electronic version of our report is available on http://www.managemgroup.com/Media-Center Managem Annual Report 2016 Draa Sfar Mine COMPANY OVERVIEW Managem is an integrated mining group managing a diversified portfolio of mineral resources, focusing on precious metals, base metals, Cobalt and Fluorite. Managem employs 5,660 employees across all its subsidiaries. The Group has operations in Morocco and throughout Africa in Gabon, Democratic Republic of Congo, Sudan, Guinea, Mali, Burkina Faso, Ivory Coast and Ethiopia. In addition Managem has trading activities based mainly in Switzerland and UAE. Managem is active across the entire value chain of mining activity. Managem is a leading player in the mining and hydrometallurgical industry in Morocco as well as in the African continent. The Group’s expertise and unwavering insistence on safety, ethics, performance and innovation fostered its growth and diversification, thanks to its business model developed for almost 90 years. The development of the Group’s activities was included in a responsible growth pattern through strong commitments to environment, risk management and development of neighbouring communities. 3 Diversité Managem Annual Report 2016 KEY FIGURES 2016 TURNOVERTURNOVER 5,6605,660 4,3774,377MMADMMAD CONTRIBUTORSCONTRIBUTORS +1%+1% ComparedCompared -

J Lo's Performance in Rabat Provokes Furore

22 June 12, 2015 Culture J Lo’s performance in Rabat provokes furore Saad Guerraoui said Aftati. Another PJD member, Khalid Rahmouni, expressed dis- gust at what he watched on 2M and Rabat called on Khalfi, as the one respon- sible for media policy, to resign. sexually charged per- However, PJD MP Abdeslam Bal- formance by pop diva laji told The Arab Weekly that Khalfi Jennifer Lopez at the does not have authority over public Mawazine music festival TV channels. in Rabat prompted mem- “It is the responsibility of the bersA of the ruling Islamist Justice High Authority of Audiovisual and Development Party (PJD) to call Communication (HACA) to investi- for the resignation of Communica- gate the matter following the min- tions Minister Mustapha el-Khalfi. ister’s request,” said Ballaji who Lopez, 45 and a popular Ameri- was the first MP from PJD’s parlia- can performer, opened the 14th mentary team to ask Khalfi for an Mawazine festival on May 30th, explanation for the concert. performing a nearly two-hour In a message posted on his Fa- long concert for a record crowd of cebook page, Khalfi, who is also 160,000 while millions watched on the government spokesman, an- state-owned television channel 2M. nounced that HACA and the ethics The glamorous New York-born committee of 2M would be inves- singer showcased scanty costumes tigated. Ballaji stressed that broad- and provocative poses as she casting the US singer’s suggestive donned seven different outfits, -in dance routine on a public TV chan- cluding a white leotard, during her nel was against Morocco’s constitu- performance, which was slammed tion, values and media ethics. -

CONSEIL D'administration DU 17 Mars 2021

CONSEIL D’ADMINISTRATION DU 17 Mars 2021 RAPPORT DU CONSEIL D’ADMINISTRATION SUR LES OPERATIONS DE L’EXERCICE 2020 A L’ASSEMBLEE GENERALE ORDINAIRE ANNUELLE Messieurs les Actionnaires, Nous vous avons réuni en Assemblée Générale Ordinaire Annuelle, conformément à la loi et à l’article 22 des statuts, pour entendre le rapport du Conseil d’Administration et celui des Commissaires aux Comptes sur l’exercice clos le 31 décembre 2020. Avant d’analyser l’activité de la Compagnie, nous voudrions vous rappeler brièvement l’environnement économique international et national dans lequel elle a évolué ainsi que le contexte du secteur des assurances. CONTEXTE A l’international Dans un contexte de crise inédit, l’économie mondiale a connu une sévère récession en 2020 (- 3,7% selon la Banque Mondiale), frappée de plein fouet par la pandémie du COVID-19. Confrontée à une grave crise sanitaire (plus de 28,6 millions de cas au 28/02/2021), l’économie américaine a perdu 3,6% en 2020, la pire récession depuis 1946, affectée par les effets de la pandémie. Après une forte remontée du PIB au 3ème trimestre 2020 (+33,1% en glissement annuel), la reprise s’est affaiblie au 4ème trimestre 2020 suite à la résurgence des infections au Coronavirus et la mise en place de nouvelles restrictions locales. Pour sa part, la croissance en Zone Euro accuse un repli historique de 6,8% en 2020 en raison de l’aggravation de la situation sanitaire et la multiplication des mesures de confinement dans la plupart des grandes économies de la Zone. Le recul le plus marqué est en Espagne (-11%) contre -8,8% pour l’Italie, -8,3% pour la France et -5% pour l’Allemagne. -

Morocco Market Brief

MOROCCO MARKET BRIEF www.renewablesnow.com 2 Wind & Solar project development in Morocco by 2020 “2,000 MW of wind power 2,000 MW of solar power Koudia Tanger II 150 MW by 2020” Tanger I Baida 140 MW 300 MW Khallada 120 MW Haouma Jbel Hdid 50 MW 200 MW Ain Beni Mathar Tarfaya Taza 300 MW Midelt Noor MII 150 MW Akhfenir 400 MW Tiskrad 200 MW Noor II Ouarzazate Midelt 300 MW 150-200 MW 100 MW Noor I Ouarzazate 500 MW Foum El Oued Noor III Ouarzazate 100-150 MW Boujdour Amougdoul 60 MW Sebkhat-Tah Boujdour 100 MW Laayoune 50 MW 2000 2001 MW of installed capacity MW of installed capacity 6600 4500 GWh of electricity generation GWh of electricity generation MAD 34.5 MAD 89.4 billion in investment billion in investment This report is available for download at www.renewablesnow.com/research 3 When it comes to clean energy projects in developing countries, Morocco stands out big time with a bold target of sourcing more than half of its electrical energy from renewable sources by 2030 and a firm plan to have 2,000 MW of wind and 2,000 MW of solar power plants by 2020. The North African kingdom, which hosted in Marrakesh COP 22, the UN climate change conference, already has a pretty detailed plan as to how it will transform the country’s energy mix. Noor Ouarzazate In February 2016, Morocco was all over the news with the official launch of the 160-MW first phase of its giant 580 MW Noor solar project near the trading city of Ouarzazate. -

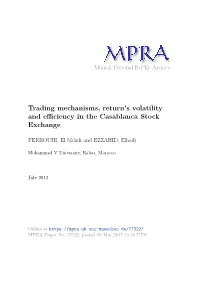

Trading Mechanisms, Return's Volatility and Efficiency in the Casablanca

Munich Personal RePEc Archive Trading mechanisms, return’s volatility and efficiency in the Casablanca Stock Exchange FERROUHI, El Mehdi and EZZAHID, Elhadj Mohammed V University, Rabat, Morocco July 2013 Online at https://mpra.ub.uni-muenchen.de/77322/ MPRA Paper No. 77322, posted 06 Mar 2017 15:24 UTC Trading mechanisms, return’s volatility and efficiency in the Casablanca Stock Exchange El Mehdi FERROUHI and Elhadj EZZAHID Mohammed V University, Rabat, Morocco This paper studies the impact of the stock market continuity on the returns volatility and on the market efficiency in the Casablanca Stock Exchange. For the most active stocks, the trading mechanism used is the continuous market which is preceded by a call market pre-opening session. Results obtained concerning return volatility and efficiency under the two trading mechanisms show that the continuous market returns are more volatile than the call market returns and 50 percent of stocks studied show independence between variations. Keywords: Trading mechanism, microstructure, call market, continuous market, efficiency, volatility 1. Introduction The microstructure of financial markets is the discipline that studies the modalities of the operational functioning of financial markets and the mechanisms that lead to the determination of prices at which stocks are exchanged. Thus, it discusses the impact of trading mechanisms on the pattern of financial markets. In this paper we will focus in the impacts of trading mechanisms, which differ from a market to other, on return’s volatility and market efficiency. Some stock markets apply the “call market” in which trading and orders executions occur at regular time intervals. All transactions are conducted at a single price determined to balance the sales and purchases orders. -

UNE RETROSPECTIVE 2014-A.Indd

Système de Management de la Qualité certifié ISO 9001 version 2008 par BUREAU VERITAS MAROC LE PREMIER QUOTIDIEN ECONOMIQUE DU MAROC Année marathon II RétRospective L’année où la diplomatie • Tournées royales d’envergure construite avec un montant de 330 mil- lions de DH. Les champs de partenariats ont également compris d’autres secteurs • Le capital immatériel fait son comme les finances, les énergies renou- velables, les infrastructures, le transport, entrée dans l’évaluation de la l’agroalimentaire, les mines, l’habitat… richesse du pays L’impact de cette tournée a été retentis- sant en termes de perception du Maroc dans le continent. En peu de temps, le • Appel à une rupture avec les Souverain a construit une image charis- matique en Afrique. La dynamique de la privilèges et l’économie de rente diplomatie royale a permis un plus grand au Sahara rapprochement avec certains Etats du Sahel, comme le Mali, qui n’étaient pas considérés traditionnellement comme des 2014 est décidément l’année bastions acquis au Maroc. Aujourd’hui, de la consécration de l’orientation afri- le renforcement du partenariat avec ces caine du Maroc. La tournée royale dans Etats se base sur une logique de com- la région, durant les premiers mois de plémentarité. Ces Etats ont demandé de cette année, a montré l’engagement du profiter de l’expertise marocaine dans Royaume en faveur du développement de plusieurs domaines, notamment dans la la coopération Sud-Sud. Le pays ne s’est promotion des ressources humaines, mais pas contenté des beaux discours, mais surtout dans l’encadrement religieux. -

Attijariwafa Bank Morocco

Attijariwafa Bank Morocco Active This profile is actively maintained Send feedback on this profile Created on: Nov 2 2020 Last update: Dec 31 2020 About Attijariwafa Bank Attijariwafa Bank is a Moroccan multinational commercial bank and financial services company, headquartered in Casablanca. It was established in 2003 after a merger between Banque Commerciale du Maroc and Wafabank. The bank's largest shareholder is king Mohammed VI's holding company Société Nationale d'Investissement (SNI). The bank maintains offices in China, France, Belgium, Spain, Italy, Milan, The Netherlands, Tunisia, Senegal, Ghana, Mauritania and Mali. Website https://www.attijariwafabank.com/en Headquarters 2 boulevard Moulay Youssef BP 11141 2000 Casablanca Morocco CEO/chair Mohamed El Kettani CEO Supervisor Bank Al-Maghrib Annual Annual report 2019 CSR report 2019 reports CSR report 2018 Annual report 2018 Ownership Atijariwafa bank's largest shareholder is SNI (also know as Al Mada) with 46.4%. The bank's complete shareholder structure can be accessed here. Complaints and grievances Sustainability Voluntary initiatives Attijariwafa Bank has committed itself to the following voluntary standards: OECD Guidelines for Multinational Enterprises United Nations Global Compact Universal Declaration of Human Rights Investment policies Atijariwafa's bank webpage on corporate social responsibility can be accessed here. CSR Approach Dec 31 2018 | Atijariwafa bank Principles of responsible purchasing Oct 4 2018 | Atijariwafa bank Good moves Related Dodgy Deals Attijariwafa Bank has been linked to the following "Dodgy Deals", e.g. as a current or past financier or through an expression of interest. Find out more about dodgy deals here. See the project or company profile for more details on the nature of the bank's link to the Dodgy Deal.