Tax Administration Compiled and Ordered Notes from Interviews Including Cross-Checks with Publicly Accessible Material, Prepared for Future Use

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Stadtplan Mit Umgebungskarte

nach Allersberg nach Freystadt Schloss nach Freystadt TSV Meckenhausen – M hilpoltstein_de Instagram: – Sport- C – A BCDEF facebook.com/stadt.hilpoltstein – – Haimpfarrich boot- L Roth hafen – K – leine – – K Rothsee St. Hippolyt M – – F – – ,Mörlach Seezentrum – www.hilpoltstein.de 428 m C – A – A – Umwelt- – – L D nach Pierheim RH 28 Heuberg W eidac h – – – station [email protected] – – e – I – N – e ich F – Schleuse s – E – I – h – t – Eckersmühlen o A 978-505 09174 Telefon – R – – H Flussmeister- F – Hilpoltstein 91161 stelle m – 1 A 1 St. Martin – Minigolf St 2220 – Mörlach – A – – H – 1 Kirchenstraße nach Forchheim B B F – – – – nach Hilpoltstein – – nach Roth Pfarramt SV 1969 Heuberg C E – G Tourismus und Kultur für Amt – – RH 32 B – – St 2238 – Hilpoltstein Stadt Auholz – G – - – E – - - B – H C – B – - - – Meckenhausen A - RH 28 – St 2225 Grund- – D - – B – B - Heuberg schule - - A - - K Bischofsholz – B – R – i – D ed Egelsee - 9 – g Weiherhaus C - - A ra G b - D - - - – en Gef äll E - „sattelfest“ - F - St. Walburga nach Pierheim, Meckenhausen nach Sindersdorf nach Karm Lach Am M ain -D on Lochmühle au vorbehalten! Änderungen - - K b. Heuberg a C Sindersdorf n Hög lac h al Schafbühl - Wasser- und 38 nach Meckenhausen 2020 September Stand: t 22 nach Mörlach, 2 Schifffahrtsamt 410 m 2 S GmbH Art Druck D.i.e. Druck: Bauhof A - Freystadt - - St. Walburga Baumgärtner Heike Hochweiss Büro Spachmüller, B - D - M - Ganzenhof a Bernhard Kartographie für Ingenieurbüro Gestaltung: in SF Jahrsdorf St 2220 -D Spachmüller Bernhard Kartographie für Ingenieurbüro Karten: o n Tourismus und Kultur für Amt Hilpoltstein, Stadt Herausgeber: a - u E Jahrsdorf -K St 2220 - a - 56 HILPOLTSTEIN IMPRESSUM na - G - - F - B - l - - F A - – O - – - Autohof Altenhofen A – h l g – N – - e Hilpoltstein ü E - - L - K W - – b (Hilpodrom) - G - - r nach Hilpoltstein n Mariä Geburt – L e . -

The Death of the Income Tax (Or, the Rise of America's Universal Wage

Indiana Law Journal Volume 95 Issue 4 Article 5 Fall 2000 The Death of the Income Tax (or, The Rise of America’s Universal Wage Tax) Edward J. McCaffery University of Southern California;California Institute of Tecnology, [email protected] Follow this and additional works at: https://www.repository.law.indiana.edu/ilj Part of the Estates and Trusts Commons, Law and Economics Commons, Taxation-Federal Commons, Taxation-Federal Estate and Gift Commons, Taxation-State and Local Commons, and the Tax Law Commons Recommended Citation McCaffery, Edward J. (2000) "The Death of the Income Tax (or, The Rise of America’s Universal Wage Tax)," Indiana Law Journal: Vol. 95 : Iss. 4 , Article 5. Available at: https://www.repository.law.indiana.edu/ilj/vol95/iss4/5 This Article is brought to you for free and open access by the Law School Journals at Digital Repository @ Maurer Law. It has been accepted for inclusion in Indiana Law Journal by an authorized editor of Digital Repository @ Maurer Law. For more information, please contact [email protected]. The Death of the Income Tax (or, The Rise of America’s Universal Wage Tax) EDWARD J. MCCAFFERY* I. LOOMINGS When Representative Alexandria Ocasio-Cortez, just weeks into her tenure as America’s youngest member of Congress, floated the idea of a sixty or seventy percent top marginal tax rate on incomes over ten million dollars, she was met with a predictable mixture of shock, scorn, and support.1 Yet there was nothing new in the idea. AOC, as Representative Ocasio-Cortez is popularly known, was making a suggestion with sound historical precedent: the top marginal income tax rate in America had exceeded ninety percent during World War II, and stayed at least as high as seventy percent until Ronald Reagan took office in 1981.2 And there is an even deeper sense in which AOC’s proposal was not as radical as it may have seemed at first. -

2605 Karte Vorne 16.10.17

HILPOLTSTEIN HEIDECK THALMÄSSING Drachenfest im September Laibstädter Geschichtsweg Freibad Thalmässing Sommer-End-Party Premiumwanderweg, Infotafeln am Weg, von Mai bis September, tägl. von Mittelalterlicher Stadtkern mit Historische Altstadt mit schönen Archäologisches Museum Bauernmarkt jeden (ca. 7,5 km, mit Stichwegen zu 9.00-20.00 Uhr geöffnet. Fachwerkhäusern Fachwerkhäusern „Fundreich Thalmässing“ Freitagvormittag Strohbrunnen und Grenzstein 12,5 km) Burg Hilpoltstein (Aussichtsturm) Frauenkapelle, erbaut 1419 von Exponate von der Steinzeit über die Weihnachtsmarkt mit Bergfried geöffnet von April bis Okt., Friedrich II. von Heideck, Fresken vor Bronze- und Eisenzeit bis zur Zeit der Adventskonzert am ersten Ostermarkt zwei Sonntage vor Ostern jeden Samstag, Sonntag sowie an 1420, 3 Epitaphe 15. Jh. Völkerwanderung. April bis Oktober Adventswochenende Maikirchweih Steindl Sonntag vor Feiertagen von 10.30 --17.00 Uhr Stadtpfarrkirche St. Johannes der Stadtführung für Gruppen nach Di. - So. und Feiertage Stadt-, Burg- oder Christi Himmelfahrt Eintrittspreise: Erwachsene 1,50 Euro Täufer, gotischer Chor, Madonna um 1500 Vereinbarung (ab 10 Pers.) November bis März Kellerführungen, geführte Pfingstmarkt Thalmässing Jugendliche ab 12 Jahre 1,00 Euro Rathaus, erbaut 1479 bis 1481. Verein "Heimatkundliche Sammlung", Fr. --So. und Feiertage Wanderungen und Radtouren am Pfingstmontag Ehemalige Residenz Sandsteinbau mit Stufengiebel Tel.: 09177/4940-0 jeweils 10 – 12 Uhr und 13 – 16 Uhr Heimatfest am Wochenende um den Kirchweih Eckmannshofen Traidkasten (Haus des Gastes) Schloßberg (607 m), Ab Ende des Gruppen nach Voranmeldung auch letztes Wochenende im Juli Haus des Gastes (ehem. Kornspeicher) 13. Jhs. Sitz der Herren von Heideck. dritten Sonntag im Juli außerhalb der Öffnungszeiten Fahrradverleih und -reparatur Weihnachtsmarkt Thalmässing Barocke Stadtpfarrkirche Burgstall mit herrlicher Aussicht sowie Weihnachtsmarkt am Samstag vor dem Eintritt Erwachsene: 3 €, Kind 1 €, Zweirad Häckl Samstag vor dem 1.Advent Museum “Schwarzes Roß” Info- und Panoramatafel 1. -

„Das Vielleicht Beste Radgeschäft Der Welt“

28 - Dienstag, 12. Juli 2016 Datev Challenge Roth Wo sich Triathleten ihre Ausrüstung in der Region kaufen „Das vielleicht beste Radgeschäft der Welt“ Von Markus Kaiser Schwerdt unterstützt wird: „Er hat viel für mich getan.“ Gerade während NÜRNBERG/HILPOLTSTEIN – der Triathlon-Saison herrscht im Natürlich der Fritz. „Das vielleicht Laden am Westtorgraben Hochkon- beste Radgeschäft der Welt“ nennt junktur. Ständig klingelt das Telefon. Timo Bracht, Sieger des Datev Challen- Schwerdttelefoniert in der Werkstatt, ge Roth des Jahres 2014, den Laden am während er ein Rad richtet. Ortseingang von Hilpoltstein. Seit fast Seit 2014 gibt es den triathlon.de- 25 Jahren verkauft und vermisst Fritz Shop, ein Franchise-Modell wie bei Buchstaller Triathleten. Seine Kunden Schnellrestaurants, im Nürnberger kommen aus dem ganzen Bundes- Westen. Ausgelagert ist hier unter gebiet. Erst neulich war wieder ein anderem die Rennradabteilung von Athlet aus Österreich in den mittel- Radsport Duschel aus Langwasser, fränkischen Landkreis gekommen. die beide zusammengehören. Ur- Vor kurzem fuhr einer extra aus Ham- sprünglich hatte er überlegt, auch den burg in die Burgenstadt, um sein Rad Laden beim Plärrer so zu nennen,sich nach dem Vermessen per Paketpost dann aber dagegen entschieden, weil nachschicken zu lassen. „Hm, ich ken- das Sortiment viel breiter ist. „Trotz- ne den Fritz, sonst fällt mir erst mal dem kommen zu uns natürlich auch gar niemand ein“, meint Kunden, die nur nach auch Challenge-Veran- einem Rad schauen“, stalter Felix Walchshöfer, meint Schwerdt. der selbst schon an seiner Der „Radsport Burk- eigenen Veranstaltung als hardt“ in der Danziger Athlet teilgenommen hat. Straße in Nürnberg kon- Während Fritz Buch- zentriert sich dagegen staller viele langjährige komplett auf Radsport- Kunden hat, gibt es in der ler. -

Rebuilding the Soul: Churches and Religion in Bavaria, 1945-1960

REBUILDING THE SOUL: CHURCHES AND RELIGION IN BAVARIA, 1945-1960 _________________________________________________ A Dissertation presented to the Faculty of the Graduate School at the University of Missouri-Columbia _________________________________________________ In Partial Fulfillment of the Requirements for the Degree Doctor of Philosophy _________________________________________________ by JOEL DAVIS Dr. Jonathan Sperber, Dissertation Supervisor MAY 2007 © Copyright by Joel Davis 2007 All Rights Reserved The undersigned, appointed by the dean of the Graduate School, have examined the dissertation entitled REBUILDING THE SOUL: CHURCHES AND RELIGION IN BAVARIA, 1945-1960 presented by Joel Davis, a candidate for the degree of Doctor of Philosophy, and hereby certify that, in their opinion, it is worthy of acceptance. __________________________________ Prof. Jonathan Sperber __________________________________ Prof. John Frymire __________________________________ Prof. Richard Bienvenu __________________________________ Prof. John Wigger __________________________________ Prof. Roger Cook ACKNOWLEDGEMENTS I owe thanks to a number of individuals and institutions whose help, guidance, support, and friendship made the research and writing of this dissertation possible. Two grants from the German Academic Exchange Service allowed me to spend considerable time in Germany. The first enabled me to attend a summer seminar at the Universität Regensburg. This experience greatly improved my German language skills and kindled my deep love of Bavaria. The second allowed me to spend a year in various archives throughout Bavaria collecting the raw material that serves as the basis for this dissertation. For this support, I am eternally grateful. The generosity of the German Academic Exchange Service is matched only by that of the German Historical Institute. The GHI funded two short-term trips to Germany that proved critically important. -

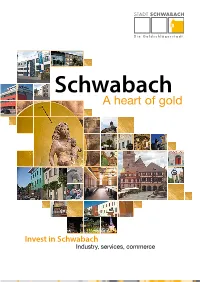

A Heart of Gold

Schwabach A heart of gold Invest in Schwabach Industry, services, commerce Schwabach, centrally located At important transport route intersections Innovative products, marketable services and lively trade shape the eco- nomic life in an attractive, centuries-old city centre. As part of the overall regional development plan’s forward projection, Schwabach is planned as a regional centre together with the cities Nuremberg, Fürth and Erlangen (so-called multi-centres). The city is integrated into the European met- ropolitan region network. Schwabach is located on the most important west-east and north-south transport routes, which were important for business dealings and decisions in earlier times. The central location also plays an important part today with its superb transport links. Schwabach is a modern, small but also a large city in some areas, which provides the best development prospects for the future. Latitude 49° 19’ 45” Height: 339 m above sea level* 39,112 inhabitants Area: 40.82 km2 Longitude 11° 1’ 32” A city of short distances and quick decisions It’s not only the distances that are short in Schwabach. The municipal Facts about the metropolitan administration also works according to the principle of short communica- region: tion channels. With a gross domestic product Quick decisions: building applications are always urgent for companies, (GDP) of over EUR 106 billion and they need planning security. If required round table discussion are set up 3.5 inhabitants, the metropolitan region of Nuremberg is one of the by the city of Schwabach, in which all of those involved take part so that strongest economic regions in Ger- the project’s expectations and current time frame are known as soon as many and Europe. -

The Kpd and the Nsdap: a Sttjdy of the Relationship Between Political Extremes in Weimar Germany, 1923-1933 by Davis William

THE KPD AND THE NSDAP: A STTJDY OF THE RELATIONSHIP BETWEEN POLITICAL EXTREMES IN WEIMAR GERMANY, 1923-1933 BY DAVIS WILLIAM DAYCOCK A thesis submitted for the degree of Ph.D. The London School of Economics and Political Science, University of London 1980 1 ABSTRACT The German Communist Party's response to the rise of the Nazis was conditioned by its complicated political environment which included the influence of Soviet foreign policy requirements, the party's Marxist-Leninist outlook, its organizational structure and the democratic society of Weimar. Relying on the Communist press and theoretical journals, documentary collections drawn from several German archives, as well as interview material, and Nazi, Communist opposition and Social Democratic sources, this study traces the development of the KPD's tactical orientation towards the Nazis for the period 1923-1933. In so doing it complements the existing literature both by its extension of the chronological scope of enquiry and by its attention to the tactical requirements of the relationship as viewed from the perspective of the KPD. It concludes that for the whole of the period, KPD tactics were ambiguous and reflected the tensions between the various competing factors which shaped the party's policies. 3 TABLE OF CONTENTS PAGE abbreviations 4 INTRODUCTION 7 CHAPTER I THE CONSTRAINTS ON CONFLICT 24 CHAPTER II 1923: THE FORMATIVE YEAR 67 CHAPTER III VARIATIONS ON THE SCHLAGETER THEME: THE CONTINUITIES IN COMMUNIST POLICY 1924-1928 124 CHAPTER IV COMMUNIST TACTICS AND THE NAZI ADVANCE, 1928-1932: THE RESPONSE TO NEW THREATS 166 CHAPTER V COMMUNIST TACTICS, 1928-1932: THE RESPONSE TO NEW OPPORTUNITIES 223 CHAPTER VI FLUCTUATIONS IN COMMUNIST TACTICS DURING 1932: DOUBTS IN THE ELEVENTH HOUR 273 CONCLUSIONS 307 APPENDIX I VOTING ALIGNMENTS IN THE REICHSTAG 1924-1932 333 APPENDIX II INTERVIEWS 335 BIBLIOGRAPHY 341 4 ABBREVIATIONS 1. -

LR Wanderfr 10 05 INT.Pdf

Erleben Sie den Landkreis Roth diesmal aber auch mit dem Rad. Erstmalig wurde eine Radltour in den „Wander - frühling“ mit auf genommen. Auf der ehemaligen Bahntrasse der Lokalbahn „Gredl“ radln wir von Hilpoltstein über Seiboldsmühle, Alfershausen und Thalmässing in Richtung Greding. An der Strecke war- die kalte Jahreszeit hat sich verabschiedet, der Früh - tet so manche Attraktion und Aktion auf Sie. Lassen ling steht vor der Tür! Mit dem „Wanderfrühling 2010“ Sie sich das Mahlen von Mehl in der Schweizermüh - haben wir Ihnen auch dieses Jahr wieder einen bunten le bei Hilpoltstein erklären oder besichtigen Sie das Strauß an Themenwanderungen zusammengestellt. Michael-Kirschner-Museum in Stauf. Am Sportug - platz in Schutzendorf bietet sich die Möglichkeit, den Nördlich des Marktes Allersberg tauchen wir ein in Landkreis auch von der Luft aus zu entdecken. Und die vergangene Zeit der Drahtbarone Allersbergs. wem danach nach einer Stärkung ist, kann sich im Ein Besuch im Gilardihaus führt Ihnen deutlich den Milchhof Walter auf Yoghurt und frische Milch aus damaligen Lebensstil vor Augen. Lassen Sie Ihren Tag der Region freuen. anschließend in den Gaststätten und Cafés um den Allersberger Marktplatz ausklingen. Sie werden sehen, es ist für jeden Geschmack etwas Auf einem Teilstück des Jakobsweges von Nürnberg dabei! nach Ulm pilgern Sie dann an Pngsten von Schwabach über Kammerstein nach Abenberg und lassen sich bei Wir freuen uns auf Sie! meditativen Gedanken vom Alltag entrücken. Im Juni lockt schließlich eine besondere Dämmerungs - wanderung am Teufelsknopf! Fantasie und Wahrheit zahlreicher Sagen und Legenden treen sich hier im Waldgebiet um die Ruine Wartstein nahe dem Ort Herbert Eckstein Eichelburg am Rothsee. -

Characteristics of Plastic Bag Fee and the Evaluation of This Fee by Means of Fiscal and Environmental Policy

34.International Public Finance Conference / Turkey April 24-27, 2019, Antalya – Turkey 54 DOI: 10.26650/PB/SS10.2019.001.008 CHARACTERISTICS OF PLASTIC BAG FEE AND THE EVALUATION OF THIS FEE BY MEANS OF FISCAL AND ENVIRONMENTAL POLICY Erdem ERCAN1 Abstract In many countries of the world and mainly in European countries, implementations in order to reduce the use of plastic, by means of academic, administrative and political efforts, have resulted in the form of scientific reports, conventions, directives and legal regulations at national and international level. The implementations are rapidly spreading. In parallel to these developments in Turkey, a new and integrated environmental policy began with the “Zero Waste Project” in order to implement waste segregation at source, reduce and recycle waste. In this context, the first legal step was taken to reduce the use of plastic by a series of legal regulations known as “plastic bag fee regulation”. The goal was determined as reducing the amount of annual average plastic bag usage by 90%, from 440 to 40 per capita. After that, it is foreseen to establish a recycling infrastructure which will be financed by the revenues, to be obtained from the plastic bags. This development, of course, necessitates the pursuit of an environmentally motivated fiscal policy that supports the new environmental policy. In this study, first of all the characteristics and elements of the plastic bag fees will be emphasized, and after determining the type of income of this fee, the issue will be evaluated by means of fiscal and environmental policies. Afterwards, some countries which have realized the same issue will be evaluated and it will be comparisoned with the situation in Turkey. -

NEU Im Heft: STELLENANZEIGEN

BürgerInfo Offizielles Mitteilungsblatt der Marktgemeinde Schwanstetten WIR IN TETTEN ANS SCHW WILLKOMMEN SOMMER! NEU im Heft: STELLENANZEIGENwww.schwanstetten.de | JULI 2021! ab Seite 14 Rathaus - Informationen Wichtige Rufnummern Öffnungszeiten Polizei: 110 Wir bitten um telefonische Terminvereinbarung Feuerwehr: 112 Telefon 09170 289 -0 Rettungsdienst, Notarzt: 112 Fax 09170 289 - 40, -35 Mail [email protected] Ärztlicher Internet www.schwanstetten.de Bereitschaftsdienst: 116 117 Zahnärztlicher Erledigen Sie Ihre Amtsgänge online: Notdienst: www.notdienst-zahn.de www.buergerserviceportal.de/bayern/schwanstetten Zentraler Notruf zum Kartensperren: 116 116 Bitte benutzen Sie im Telefonverkehr Telefonseelsorge: 0800 / 111 0 111 (evang.) die Rufnummer 289 + Durchwahl 0800 / 111 0 222 (kath.) Kinder- und Jugendtelefon: 116 111 Zi. Amt Durchwahl Hilfe für Frauen in Not 01 Meldeamt, Passamt: Sabine Döring-Huber -10 Roth/Schwabach: 09122 / 98 20 80 Vanessa Bogatscher -12 Hilfetelefon Sexueller 0800 / 22 55 530 02 Ordnungsamt: Dominic Nowak -11 Missbrauch: (kostenfrei & anonym) 03 Standesamt, Versicherungsamt: Stefanie Dößel -27 Giftnotruf: 0911 / 39 82 451 Apothekennotdienst: 0800 / 00 22 833 04 Steueramt: Elke Jakob -26 Katharina Wagner -23 N-ERGIE/Stromnotruf: 01802 / 71 35 38 05 Kasse: Sabine Zachmann -13 (kostenlos) Telekom Service Hotline: 0800 / 330 10 00 09 Vorzimmer Bürgermeister: Michaela Braun -16 (Störungen Festnetz) Ehrungen: Marion Reuß -28 Geschäftsleiter: Frank Städler -17 0800 / 320 22 02 Bürgermeister: Robert Pfann -15 (Störungen Mobilfunk) Fahrplanberater VGN: 0911 / 270 75 99 8 10 Volkshochschule, Birgit Jansen -24 (24 Std. täglich) Schulwesen, Sport: 11 Kulturamtsleitung: Stefanie Weidner -25 15 Kämmerei: Peter Lösch -22 BÜRGERINFO SCHWANSTETTEN 16 Bauanfragen und Bauanträge, Erschließungsbeiträge: USGABE UGUST Mario Knorr -20 A A Manuela Städler-Ohnesorge -21 Abgabeschluss für Anzeigen und Berichte 17 Gemeindliche Bauvorhaben, ist der 08. -

Conference Binder

Mövenpick Hotel Nuremberg Airport Hotel Description The Green Globe certified Mövenpick Hotel Nuremberg-Airport, located directly at the airport, is the ideal starting point for your business trips, visiting trade fairs or any private ventures. Because of the successful tradition of our company we have evolved a fine sense for counting details. Enjoy Swiss hospitality at its best. Distinguished service and utmost motivated staff is living our corporate policy to pamper each guest with a personal nice touch. For a brief overview we would like to invite you for a visit on our homepage at www.movenpick.com/nuernberg. Hotel Rooms Whether you are travelling for business or leisure, our 150 comfortable rooms will meet all your needs. All our rooms are equipped with air conditioning, high class noise protection windows, Full HD TV with international program, free Wi-Fi, telephone with voicemail, hairdryer, minibar, safe and a station for coffee and tea-making. Our Superior Rooms provide additional comfort with free usage of the minibar, high speed Wi-Fi and access to daily newspapers at our reading corner. Mövenpick Restaurant The Mövenpick Restaurant is located in the airport terminal opposite to the hotel. Alongside the classic menus, there is a large selection of regional and international dishes. Take a glance at the airplanes starting and landing silently while enjoying the flair and the delicacies of our kitchen and wine cellars. Opening times: Monday – Thursday 12 a.m. - 8 p.m. Friday 12 a.m. - 10 p.m. Saturday closed Sunday 10 a.m. - 8 p.m. Premium Breakfast at the Hotel Our regional and Swiss specialties together with the laid-back atmosphere at our famous breakfast buffet will provide you the basis for a perfect start of your day. -

März 2020 (PDF-Datei)

BürgerInfo Offizielles Mitteilungsblatt der Marktgemeinde Schwanstetten IN WIR SCHWANSTETTEN FRÜHLINGSERWACHEN DIE MÄRZENBECHER IN DER SOOS BLÜHEN AUF www.schwanstett en.de | MÄRZ 2020 Rathaus - Informationen Wichtige Rufnummern Öffnungszeiten Polizei: 110 Mo 08.00 – 12.00 Uhr Feuerwehr: 112 Di 08.00 – 12.00 Uhr Rettungsdienst, Notarzt: 112 Mi 08.00 – 12.00 Uhr Do 14.00 – 18.00 Uhr Ärztlicher Fr 08.00 – 12.00 Uhr Bereitschaftsdienst: 116 117 Terminvereinbarungen sind auch außerhalb der Öffnungszeiten möglich. Zahnärztlicher Telefon 09170 289 -0 Notdienst: www.notdienst-zahn.de Fax 09170 289 - 40, -35 Zentraler Notruf Mail [email protected] Internet www.schwanstetten.de zum Kartensperren: 116 116 Telefonseelsorge: 0800 / 111 0 111 (evang.) Erledigen Sie Ihre Amtsgänge online: 0800 / 111 0 222 (kath.) www.buergerserviceportal.de/bayern/schwanstetten Kinder- und Jugendtelefon: 116 111 Bitte benutzen Sie im Telefonverkehr Hilfe für Frauen in Not die Rufnummer 289 + Durchwahl Roth/Schwabach: 09122 / 8 19 19 Hilfetelefon Sexueller 0800 / 22 55 530 Zi. Amt Durchwahl Missbrauch: (kostenfrei & anonym) Giftnotruf: 0911 / 39 82 451 01 Meldeamt, Passamt: Sabine Döring-Huber -10 Vanessa Bogatscher -91 Apothekennotdienst: 0800 / 00 22 833 02 Ordnungsamt: Dominic Nowak -11 N-ERGIE/Stromnotruf: 01802 / 71 35 38 03 Standesamt, Versicherungsamt: (kostenlos) Stefanie Dößel -27 Telekom Service Hotline: 0800 / 330 10 00 04 Steueramt: Elke Jakob -26 (Störungen Festnetz) Katharina Wagner -23 0800 / 320 22 02 05 Kasse: Sabine Zachmann -13 (Störungen Mobilfunk) 09 Vorzimmer Bürgermeister: Michaela Braun -16 Fahrplanberater VGN: 0911 / 270 75 99 8 Ehrungen: Marion Reuß -28 (24 Std. täglich) Geschäftsleiter: Frank Städler -17 Bürgermeister: Robert Pfann -15 10 Volkshochschule, Birgit Jansen -24 Schulwesen, Sport: BÜRGERINFO SCHWANSTETTEN 11 Kulturamtsleitung: Stefanie Weidner -25 AUSGABE APRIL A bgabesch uss ü r n eigen und erichte 12 Kämmerei: Peter Lösch -22 ist der 10.