Introduction

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Putusan Sidang Putusan No 50-PHPU-D-VIII-2010.Pdf

PUTUSAN Nomor 50/PHPU.D-VIII/2010 DEMI KEADILAN BERDASARKAN KETUHANAN YANG MAHA ESA MAHKAMAH KONSTITUSI REPUBLIK INDONESIA [1.1] Yang memeriksa, mengadili, dan memutus perkara konstitusi pada tingkat pertama dan terakhir, menjatuhkan putusan dalam perkara Perselisihan Hasil Pemilihan Umum Kepala Daerah dan Wakil Kepala Daerah Kabupaten Bima Tahun 2010, yang diajukan oleh: [1.2] 1. Nama : Drs. H. Zainul Arifin Tempat dan Tanggal Lahir : Bima, 29 Juli 1955 Agama : Islam Pekerjaan : Pensiunan PNS Alamat : Talabiu RT 001/RW 001 Desa Talabiu, Kecamatan Woha, Kabupaten Bima 2. Nama : Drs. H. Usman, AK Tempat dan Tanggal Lahir : Bima, 4 Oktober 1953 Agama : Islam Pekerjaan : Wakil Bupati Bima Alamat : Jalan Gatot Subroto Nomor 45 Kelurahan Mande, Kecamatan Mpunda, Kota Bima Adalah Pasangan Calon Bupati dan Wakil Bupati Peserta Pemilihan Umum Kepala Daerah Kabupaten Bima Tahun 2010 Nomor Urut 3; Berdasarkan Surat Kuasa Khusus bertanggal 15 Juni 2010, memberikan kuasa kepada i) Sulaiman MT, S.H.; ii) Ilham, S.H.; iii) Sutrisno, S.H., M.H.; iv) H.M. Natsir, S.H.; dan v) Kafani, S.H., semuanya adalah Advokat yang berkedudukan di Salama, Kelurahan Na’e, Kecamatan Rasana’e Barat, Kota Bima, baik secara bersama-sama maupun sendiri-sendiri bertindak untuk dan atas nama Pemohon; Selanjutnya disebut sebagai -------------------------------------------------------- Pemohon; 2 Terhadap: [1.3] Komisi Pemilihan Umum Kabupaten Bima, berkedudukan di Jalan Soekarno-Hatta Nomor 1 Kelurahan Penatoi, Kecamatan Mpunda, Kota Bima, Provinsi Nusa Tenggara Barat; Berdasarkan Surat Kuasa Khusus bertanggal 22 Juni 2010, memberikan kuasa kepada i) H. Mahsan, S.H., M.Hum.; ii) Akmaludin, S.H., M.H.; iii) Edy Gunawan, S.H.; iv) Ina Maulina, S.H.; dan v) Helmi Hidayat, S.H., semuanya adalah Advokat yang beralamat di Jalan Panca Usaha Nomor 22C Cakranegara, Kota Mataram, Provinsi Nusa Tenggara Barat, baik secara bersama-sama maupun sendiri-sendiri bertindak untuk dan atas nama Termohon; Selanjutnya disebut sebagai ------------------------------------------------------- Termohon; [1.4] 1. -

1 11103100105681 Irwadi Batubara, MM. Universitas Ibnu Chaldun M 2 11103100106543 Leonardus Subagyo, M.Sc

Hasil Laporan No. Nomor Sertifikat Nama Tempat Tugas Keterangan BKD BKD 1 11103100105681 Irwadi Batubara, MM. Universitas Ibnu Chaldun M 2 11103100106543 Leonardus Subagyo, M.Sc. Universitas Ibnu Chaldun M 3 11103100112471 Urhen Lukman, MA. Universitas Ibnu Chaldun M 4 08156103357 Ir. Mulki Siregar, MT. Universitas Islam Jakarta M 5 08156109369 Ir. Achmad Sutrisna, MT. Universitas Islam Jakarta M 6 08156110926 Muhammad Ali Yusuf, SE., M.Pd. Universitas Islam Jakarta M 7 08156110927 Farhana, SH., MH. Universitas Islam Jakarta M 8 091156100635 Edi Suhara, SE, MM. Universitas Islam Jakarta M 9 091156101331 Hamdan Azhar Siregar, SH, MH. Universitas Islam Jakarta M 10 091156102156 Ir. Untung Setiyo Purwanto, MT. Universitas Islam Jakarta M 11 091156105753 Endang Saefuddin Mubarok, SE, MM. Universitas Islam Jakarta M 12 101156100184 Siti Miskiah, SH., MH. Universitas Islam Jakarta M 13 101156100185 Mimin Mintarsih, SH,. MH. Universitas Islam Jakarta M 14 101156100186 Otom Mustomi, SH,. MH. Universitas Islam Jakarta M 15 11103100303161 Eka Sutisna, SE., MM. Universitas Islam Jakarta M 16 11103100306739 H. Lukman Achmad, SE., MM. Universitas Islam Jakarta M 17 11103100308546 Nur Aida, SH., M.Si. Universitas Islam Jakarta M 18 11103100309779 Ritawati, SH., MH. Universitas Islam Jakarta M 19 11103100315557 Bambang Sukamto, SH., MH. Universitas Islam Jakarta M 20 11103100316046 Fatimah, SH., MH. Universitas Islam Jakarta M 21 11103100318366 Yusri Ilyas, SE., MM. Universitas Islam Jakarta M 22 12103100313055 Untoro, SH., MH. Universitas Islam Jakarta M 23 08156211262 Tri Rumayanto, S.Si., M.Si. Universitas Jakarta M 24 08156210928 Jamalullail, S.IP, MM Universitas Jakarta M 25 091156200718 Dra. Dwi Murdiati, M.Hum. Universitas Jakarta M 26 091156202158 Dra. -

PT Permata Graha Nusantara (99,95%) Discussion

33 PT Perusahaan Gas Negara Tbk Annual Report 2019 Annual Report 2019 PT Perusahaan Gas Negara Tbk 34 03 COMPANY PROFILE Contributing to the Country. The Company’s footsteps, which were built from the colonial era to the role of Subholding Gas, prove that the Company can answer the challenges of the times. 33 PT PerusahaanGasNegaraTbkAnnualReport2019 Overview Performance to The Report Shareholders Profile Company Discussion and Analysis Management Governance Good Corporate Annual Report 2019 PT Perusahaan Gas Negara Tbk Annual Report2019PTPerusahaanGasNegaraTbk Responsibility Corporate Social and Environmental Financial Statements Consolidated Regulatory Cross Reference 34 35 PT Perusahaan Gas Negara Tbk Annual Report 2019 Annual Report 2019 PT Perusahaan Gas Negara Tbk 36 PT PERUSAHAAN GAS NEGARA AT A GLANCE NAME AND DOMICILE OF STOCK CODE THE COMPANY Indonesia Stock Exchange: PGAS. PT Perusahaan Gas Negara Tbk dan Berdomisili di Jakarta. Name change of PT Perusahaan Gas Negata (Persero) Tbk to PT Perusahaan Gas Negara Tbk was formally occurred on April 26th, 2018. This was occurred due to the transfer of all B Series shares owned by the Republic of Indonesia in PGN to PT Pertamina (Persero). OWNERSHIP DATE OF The Republic of Indonesia: 0%, 1 Series A ESTABLISHMENT Dwiwarna Shares. May 13, 1965. PT Pertamina (Persero): 56,96%, 13,809,038,755 Series B Shares. Public: 43,04%, 10,432,469,440 Series B Shares. 35 PT Perusahaan Gas Negara Tbk Annual Report 2019 Annual Report 2019 PT Perusahaan Gas Negara Tbk 36 Overview Performance to The Report Shareholders LEGAL BASIS OF AUTHORIZED CAPITAL ESTABLISHMENT Rp7,000,000,000,000 (seven trillion Rupiah). -

Aisteel 2016)

Proceedings of the 1st Annual International Seminar on Transformative Education and Educational Leadership (AISTEEL) e-ISSN: 2548-4613 Proceedings of The First Annual International Seminar on Transformative Education and Educational Leadership (AISTEEL 2016) “Developing Future Teachers’ Educational Model” State University of Medan, North Sumatera, Indonesia November, 19th 2016 EDITORIAL BOARD Editorial-in-Chief Dr. Juniastel Rajagukguk, M.Si (State University of Medan, Unimed) Deputy Editor Dr. Saronom Silaban, M.Pd (State University of Medan, Unimed) Associate Editors Prof. Dr. Hamzah B. Uno, M.Pd (State University of Gorontalo, UNG) Prof. Dr. Johanes Sapri, M.Pd (University of Bengkulu, UNIB) Prof. Drs. Herman Dwi Surjono, M.Sc., MT., Ph.D. (Yogyakarta State University, UNY) Dr. Rahmad Husein, M.Ed (State University of Medan, Unimed) Dr. Imron Arifin, M.Pd (State University of Malang, UM) Dr. R. Mursid, ST.,M.Pd (State University of Medan, Unimed) Dr. Anni Holila Pulungan, M.Pd (State University of Medan, Unimed) Dr. Tumiur Gultom, M.P (State University of Medan, Unimed) Dr. Mariati Simanjuntak, S.Pd.,M.Pd (State University of Medan, Unimed) Dr. Fauziyah Harahap, M.Pd (State University of Medan, Unimed) Yullita Molliq, M.Sc.,Ph.D (State University of Medan, Unimed) Dr. Siti Aisyah Ginting, M.Pd (State University of Medan, Unimed) Dra. Meisuri, M.A (State University of Medan, Unimed) Indra Hartoyo, M.Hum (State University of Medan, Unimed) Please cite the proceeding as “Proceeding of the First Annual International Seminar on Transformative -

Seminar Nasional Terapan Riset Inovatif SEMARANG, 15 – 16 Oktober 2016

Seminar Nasional Terapan Riset Inovatif SEMARANG, 15 – 16 Oktober 2016 SITUASI DAN PERMASALAHAN PARKIR ON-STREET DI KAWASAN PUSAT KOTA MALANG Imma Widyawati Agustin1 1Jurusan Perencanaan Wilayah dan Kota Fakultas Teknik Universitas Brawijaya Jalan Mayjen Haryono 167 Malang 65145 – Telp (0341) 567886 Email: [email protected] Abstract There are some problems of on-street parking, such as the use of parking lot 90 in limited use of effective road width, limited parking spaces, and high-side constraints due to the activity of non-motorized vehicles. It encourages researcher to solve the parking problems in the study area. The main purpose of the research is to arrange a model of the needs of on-street parking spaces in the study area. The research used the analysis of land use, the performance analysis of on-street parking and the street performance analysis. Multiple linear regression analysis serves as a model determining the needs of motorcycle and car parking space. The results showed that independent variables that affect the models of the need parking spaces for motorcycles: the accumulation of parking (X5) and the turnover of parking (X7), while the independent variables that affect the models of the need parking space four-wheeled vehicle that is an index parking (X8) , accumulated parking (X5), and the turnover of parking (X7). These variables became one of the considerations on on-street parking is parking control for the study area is the parking progressive control of the parking area, parking time control, and provision of centralized parking. Keywords: on-street-parking, Malang-city, multiple-linear-regression, parking-space Abstrak Ada beberapa permasalahan parkir di badan jalan, seperti penggunaan lahan parkir 90 mengakibatkan keterbatasan penggunaan lebar jalan efektif, keterbatasan ruang parkir, dan terdapat hambatan samping tinggi akibat aktivitas kendaraan tidak bermotor. -

PGAS Business Updates Mandiri Investment Forum 2020 February 6, 2020

Investor Presentation PGAS Business Updates Mandiri Investment Forum 2020 February 6, 2020 www.pgn.co.id About PGAS 1 Operation Highlight & Projection 2020 Dec 19 Operation Highlight | Operation Projection | Capex Projection Table of Company Overview 2 The Milestones | The Sub-Holding Co | Leadership | Business Portfolio | Business Structure | Gas Infrastructure Contents 6M – 2019 Highlights 9M2019 3 Operational Performance Distribution | Transmission | Other Downstream | Upstream Lifting 9M2019 4 Financial Performance Income Statement | Balance Sheet | Cashflow | Financial Ratios | Debt Maturity Profile 2 Disclaimer & This document is not, and nothing in it should be construed as, an offer, invitation or recommendation in respect of the Company’s credit facilities or any of the Company’s securities. Neither this presentation nor anything in it shall form the basis of any contract or commitment. This document is not intended to be relied Cautionary upon as advice to investors or potential investors and does not take into account the investment objectives, financial situation or needs of any investor. Statement The Company has prepared this document based on information available to it that have not been independently verified. No representation or warranty, expressed or implied, is provided in relation to the fairness, accuracy, correctness, completeness or reliability of the information, opinions or conclusions expressed herein. The information included in this presentation is preliminary, unaudited and subject to revision upon completion -

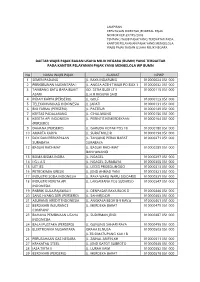

Bumn) Yang Terdaftar Pada Kantor Pelayanan Pajak Yang Mengelola Wp Bumn

LAMPIRAN KEPUTUSAN DIREKTUR JENDERAL PAJAK NOMOR KEP-397/PJ./2003 TENTANG WAJIB PAJAK YANG TERDAFTAR PADA KANTOR PELAYANAN PAJAK YANG MENGELOLA WAJIB PAJAK BADAN USAHA MILIK NEGARA DAFTAR WAJIB PAJAK BADAN USAHA MILIK NEGARA (BUMN) YANG TERDAFTAR PADA KANTOR PELAYANAN PAJAK YANG MENGELOLA WP BUMN No NAMA WAJIB PAJAK ALAMAT NPWP 1 SEMEN PADANG JL. RAYA INDARUNG 010000024 051 000 2 PERKEBUNAN NUSANTARA I JL. ANGSA ACEH TIMUR PO BOX 1 010000032 051 000 3 TAMBANG BATU BARA BUKIT GD. SETIA BUDI LT II 010000115 051 000 ASAM JL.H.R.RASUNA SAID 4 INDAH KARYA (PERSERO) JL. GOLF 010000123 051 000 5 TELEKOMUNIKASI INDONESIA JL. JAPATI 010000131 051 000 6 BIO FARMA (PERSERO) JL. PASTEUR 010000149 051 000 7 KERTAS PADALARANG JL. CIHALIWUNG 010000156 051 000 8 KERETA API INDONESIA JL. PERINTIS KEMERDEKAAN 010000164 051 000 (PERSERO) 9 DAHANA (PERSERO) JL. GARUDA KOTAK POS 18 010000180 051 000 10 AMARTA KARYA JL. SURATMO,DR 010000198 051 000 11 DOK DAN PERKAPALAN JL. TANJUNG PERAK BARAT 010000271 051 000 SURABAYA SURABAYA 12 BASUKI RACHMAT JL. BASUKI RACHMAT 010000289 051 000 BANYUWANGI 13 BOMA BISMA INDRA JL. NGAGEL 010000297 051 000 14 I G L A S JL. NGAGEL SURABAYA 010000305 051 000 15 LET JES JL. LECES PROBOLINGGO 010000313 051 000 16 PETROKIMIA GRESIK JL. JEND AHMAD YANI 010000321 051 000 17 INDUSTRI SODA INDONESIA JL. RAYA WARU WARU SIDOARJO 010000339 051 000 18 INDUSTRI KERETA API JL. LAKSAMANA YOS SUDARSO 010000347 051 000 INDONESIA 19 PABRIK GULA RAJAWALI I JL. DENPASAR RAYA BLOK D 010000446 051 000 20 SANG HYANG SERI (PERSERO) JL. -

Animation Video of Eight National Heroes from North Sumatra: Digital Learning Media to Enhance Student Nationality Character

Animation Video of Eight National Heroes from North Sumatra: Digital Learning Media to Enhance Student Nationality Character Deny Setiawan,1 Apriani Harahap,2 Rosnah Siregar,3 {[email protected], [email protected], [email protected]} 1,3Department of Citizenship Education Faculty of Social Science, Universitas Negeri Medan, Indonesia 2Department of History Education, Faculty of Social Science, Universitas Negeri Medan, Indonesia Abstract. There are eight national heroes from Sumatra namely Sisingamangaraja XII, Ferdinand Lumban Tobing, Zainul Arifin, Tengku Amir Hamzah, Adam Malik, Kiras Bangun, Teuku Mohammad Hasan, and Tahi Bonar Simatupang who have a strong national character to be encouraged and imitated by students of North Sumatra. However, the national character is only contained in a learning textbook that has not been utilized as a digital learning media. For this reason, the animated video of eight National Heroes from North Sumatra is a digital learning media that is appropriate for enhancing the national character of colleger. The research aims to develop an animated video learning media that displays eight national characters of eight national heroes from North Sumatra. This research uses research and development methods. The results showed that this animated video is very interesting to be used as a digital learning media to enhance the national character of students. Keywords: Animation, National Hero, Learning Media, National Character. 1 Introduction Menristekdikti Mohamad Nasir stressed that improving the quality of education requires equitable distribution of education through the use of information technology such as learning through digital learning which is currently developing [1]. Higher education is required to utilize digital technical technology as a medium and source of learning. -

No STORE NAME ADDRESS2 CITY STORE PHONE 1 TBS

No STORE_NAME ADDRESS2 CITY STORE_PHONE 1 TBS PONDOK INDAH MALL JKT Pondok Indah Mall Lt. 1 - JL. Metro Pondok Indah Blok IIIB Jakarta Selatan 021-7692353 2 TBS CIPUTRA SERAYA MALL PEKANBARU Mall Ciputra Seraya Lt. Dasar No.18 - Jl. Riau No. 58 Pekanbaru 0761-868618 3 TBS PARIS VAN JAVA BANDUNG RL B20 Paris Van Java - Jl. Sukajadi 137 - 139, Bandung Bandung 022-82063649 4 TBS GANDARIA MAIN STREET JKT Gandaria City - Jl. Sultan Iskandar Muda No. 57 Jakarta Selatan 021-29053091 5 TBS E-WALK BALIKPAPAN E Walk Superblok GF - Jl. Jendral Sudirman No. 71 Balikpapan 0542-7586881 6 TBS KELAPA GADING MALL JKT Kelapa Gading - Jl. Boulevard Raya Kav. 144 Jakarta Utara 021-4533422 7 TBS PLAZA SENAYAN JKT Plaza Senayan 2 ND Floor - JL. Asia Afrika No. 8 Jakarta Pusat 021-5725179 8 TBS GALAXY MALL SURABAYA Galaxy Mall G.101-102 - Jl. Dharmahusada Indah Timur No.14 Surabaya 031-5915032 9 TBS PLUIT MEGA MALL JKT Mega Mall Pluit GF - JL. Pluit Indah Raya No. 36 Jakarta Utara 021-6683878 10 TBS TAMAN ANGGREK MALL JKT Mall Taman Anggrek UG Floor - JL. Letjen S. Parman Kav. 21 No. 78 Jakarta Barat 021-5639296 11 TBS BANDUNG INDAH PLAZA BANDUNG Bandung Indah Plaza GF NO. 5 - Jl. Merdeka No. 56 Bandung 022-4233521 12 TBS BLOK M PLAZA JKT Blok M Plaza UG - 01 - 02 - Jl. Bulungan No. 76 Keb. Baru Jakarta Selatan 021-7209041 13 TBS INDONESIA PLAZA JKT Plaza Indonesia LB# B-08 FLOOR - Jl. MH Thamrin Kav.28-30 Jakarta Pusat 021-29923853 14 TBS TRANS STUDIO MALL BANDUNG Bandung Supermall 1ST Floor - Jl. -

Kata Pengantar

KATA PENGANTAR Undang-Undang No. 43 Tahun 2009 tentang Kearsipan mengamanatkan Arsip Nasional Republik Indonesia (ANRI) untuk melaksanakan pengelolaan arsip statis berskala nasional yang diterima dari lembaga negara, perusahaan, organisasi politik, kemasyarakatan dan perseorangan. Pengelolaan arsip statis bertujuan menjamin keselamatan dan keamanan arsip sebagai bukti pertanggungjawaban nasional dalam kehidupan bermasyarakat, berbangsa dan bernegara. Arsip statis yang dikelola oleh ANRI merupakan memori kolektif, identitas bangsa, bahan pengembangan ilmu pengetahuan, dan sumber informasi publik. Oleh karena itu, untuk meningkatkan mutu pengolahan arsip statis, maka khazanah arsip statis yang tersimpan di ANRI harus diolah dengan benar berdasarkan kaidah-kaidah kearsipan sehingga arsip statis dapat ditemukan dengan cepat, tepat dan lengkap. Pada tahun anggaran 2016 ini, salah satu program kerja Sub Bidang Pengolahan Arsip Pengolahan I yang berada di bawah Direktorat Pengolahan adalah menyusun Guide Arsip Presiden RI: Sukarno 1945-1967. Guide arsip ini merupakan sarana bantu penemuan kembali arsip statis bertema Sukarno sebagai Presiden dengan kurun waktu 1945-1967 yang arsipnya tersimpan dan dapat diakses di ANRI. Seperti kata pepatah, “tiada gading yang tak retak”, maka guide arsip ini tentunya belum sempurna dan masih ada kekurangan. Namun demikian guide arsip ini sudah dapat digunakan sebagai finding aid untuk mengakses dan menemukan arsip statis mengenai Presiden Sukarno yang tersimpan di ANRI dalam rangka pelayanan arsip statis kepada pengguna arsip (user). Akhirnya, kami mengucapkan banyak terima kasih kepada pimpinan ANRI, anggota tim, Museum Kepresidenan, Yayasan Bung Karno dan semua pihak yang telah membantu penyusunan guide arsip ini hingga selesai. Semoga Allah SWT, Tuhan Yang Maha Esa membalas amal baik yang telah Bapak/Ibu/Saudara berikan. -

Gasnet.Id 01 Our Tagline

COMPANY PROFILE FAST & RELIABLE INTERNET WITH A GUARANTEE RATIO ORGANIZATIONAL STRUCTURE PT PGAS Telekomunikasi Nusantara License: Jartaptup, Jartaplok & NAP Service: Managed ICT PGN Group & External Customer Segment: Operator, NAP, ISP, Corporate PT PGAS PT Telemedia Telecomunications Dinamika Sarana International License: ISP (Internet License: SBO Service Provider) (Service Based Service: Internet, Operator) Additional Services, Service: International Managed Services Connectivity dan Cloud Services. Customer Segment: Customer Segment: Multinational Corporate & SOHO Corporation WWW.GASNET.ID 01 OUR TAGLINE HONEST INTERNET We are committed to always offering solution & technology service based on honesty values. We deliver our promise to suit your business require- ments. RATIO GUARANTEE We are the only ISP that provides ration guarantee bandwidth to internet service, both dedicated and broadband internet. If your business needs internet service that guaran- tees stable, reliable, and high-quality access speed, TRY US! 02 WWW.GASNET.ID RELIABILITY OUR OWN BACKBONE NETWORK CABLE INTERNATIONAL DIRECT CONNECTION VIA WEST PATH (via Jurong to Equinix) BATAM SINGAPORE TWO MAIN INTERNET PATHS BATAM JAKARTA CHANGI JAKARTA BACKUP UPSTREAM PATHS WWW.GASNET.ID 03 CAPACITY HIGH-CAPACITY RELIABLE FIBRE OPTIC Our own fibre optic connecting Singapore – Jakarta is of high-capacity bandwidth up to 1 TB and in an exclusive gas pipeline network SECURE INFRASTRUCTURE ROCK DUMPING (SUBMARINE CABLE PROTECTION) Our fibre optic cable path is protected by PGN’s dumping of 5m high and 15m wide, located side by side with our gas pipeline network. This rock dumping is pressure-resistant to a 22,000-ton anchor and it’s proven that our fibre optic cable network has been problem-free since it was built in 2003. -

Daftar Faskes/Dinkes/Klinik/Laboratorium Yang Menginput Pada Aplikasi Nar Antigen Periode Waktu 22 - 28 Agustus 2021

DAFTAR FASKES/DINKES/KLINIK/LABORATORIUM YANG MENGINPUT PADA APLIKASI NAR ANTIGEN PERIODE WAKTU 22 - 28 AGUSTUS 2021 No Asal Provinsi Faskes Asal Kabupaten/Kota Faskes Jenis Faskes Nama Faskes 1 ACEH ACEH BARAT Lainnya KLINIK ANANDA FAMILY 2 ACEH ACEH BARAT Lainnya Klinik Cempaka Lima Meulaboh 3 ACEH ACEH BARAT Puskesmas COT SEUMEREUNG 4 ACEH ACEH BARAT Puskesmas DRIEN RAMPAK 5 ACEH ACEH BARAT Puskesmas KUALA BHEE 6 ACEH ACEH BARAT Puskesmas MENTULANG 7 ACEH ACEH BARAT Puskesmas MEUREUBO 8 ACEH ACEH BARAT Puskesmas PANTE CEUREUMEN 9 ACEH ACEH BARAT Puskesmas PASIE MALI (WOYLA BARAT) 10 ACEH ACEH BARAT Puskesmas PEUREUMEU 11 ACEH ACEH BARAT RS RSUD CUT NYAK DHIEN MEULABOH 12 ACEH ACEH BARAT DAYA Klinik Dinkes Aceh Barat Daya 13 ACEH ACEH BESAR Lainnya Klinik Utama Kasehat Walafiat 14 ACEH ACEH BESAR Lainnya Tirtana Medikal Klinik 15 ACEH ACEH BESAR Puskesmas BLANG BINTANG 16 ACEH ACEH BESAR Puskesmas LAMPISANG 17 ACEH ACEH BESAR Puskesmas LHOKNGA 18 ACEH ACEH BESAR Puskesmas MESJID RAYA 19 ACEH ACEH BESAR Puskesmas MONTASIK 20 ACEH ACEH BESAR Puskesmas Puskesmas Krueng Barona Jaya 21 ACEH ACEH JAYA Klinik dinkesacehjaya 22 ACEH ACEH SELATAN Klinik Dinas kesehatan 23 ACEH ACEH SELATAN Puskesmas BAKONGAN 24 ACEH ACEH SELATAN Puskesmas BLANGKEJEREN 25 ACEH ACEH SELATAN Puskesmas BUKIT GADENG 26 ACEH ACEH SELATAN Puskesmas DURIAN KAWAN 27 ACEH ACEH SELATAN Puskesmas KAMPONG PAYA 28 ACEH ACEH SELATAN Puskesmas KLUET TIMUR 29 ACEH ACEH SELATAN Puskesmas KRUENG LUAS 30 ACEH ACEH SELATAN Puskesmas KUALA BA'U 31 ACEH ACEH SELATAN Puskesmas LADANG