RAPPORT ABREGE ANGLAIS VANG 13 9 18 Ang 0

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Conditional Volatility of Most Active Shares of Casablanca Stock Exchange

CONDITIONAL VOLATILITY OF MOST ACTIVE SHARES OF CASABLANCA STOCK EXCHANGE ABDELHAMID EL BOUHADI* 89, rue Al Azhar, Quartier Amerchich Marrakech, Maroc email address : [email protected] Summary Volatility plays an important role in the explanation of prices of securities and their derivatives as well as risk which are relative to them. The stock exchange of Casablanca constitutes a market meadow emergent of MEA zone for which the problem of volatility should not be underestimated for the causes of lack of the making in the order book. The introduction of the electronic system in 1998 allowed continuous quotation of a number restricted by securities liquidity of which does not seem even so important. We test in this paper the conditional volatility of a certain number of securities considered as active and which to be result from the MADEX index. Results show a certain asymmetric volatility of the major securities. The use of the asymmetric GARCH allowed us better to describe rough variations of prices provoked by large quantities traded in block market. These models throw back quadratic specification of the conditional variance lauded by GARCH standard models. Indeed, with regard to these last ones, exponential model GARCH and threshold GARCH have two advantages. While standard model GARCH puts that only the amplitude of shock and not the sign of the past residuals has an impact on the conditional variance, EGARCH and TGARCH models allows an asymmetric answer to shocks. Second advantage is that not conditional variance is discrete. Keywords Volatility ; Asymmetric GARCH ; None Linearity ; MADEX ; The Stock Exchange of Casablanca. JEL Classification: G14 VOLATILITÉ CONDITIONNELLE DES VALEURS LES PLUS ACTIVES DE LA BOURSE DE CASABLANCA Résumé La volatilité joue un rôle important dans l’explication des prix des titres et leurs dérivés ainsi que le risque qui leur sont afférents. -

Energies Vertes Et Efficacité Énergétique

Chambre Française de Commerce et d’Industrie du Maroc www.cfcim.org 51e année Numéro 938 15 juin - 15 juillet 2012 Dispensé de timbrage autorisation n° 956 ConjonctureLE MENSUEL DES DÉCIDEURS L’invité de ConjonCTURE M’HaMED SAGOU Energies vertes et efficacité énergétique ECHOS MarOC Indicateurs économiques et financiers induStriE Comment optimiser ses profits ? ManagEMEnt Conseils pratiques pour réussir son recrutement L’actualité vue par le Service économique de l’Ambassade de France Le Coin des Adhérents : Nouveaux Adhérents CFCIM - Opportunités d’affaires - Emploi Editorial Conjoncture « Une nouvelle formule plus moderne et plus pratique » Joël Sibrac Président Nouvelle maquette, nouvelles rubriques, nouvelle organisation : votre revue Conjoncture a profité du printemps pour se faire « relooker » en profondeur. Un travail de fond mené par l’équipe de Conjoncture, Comité de rédaction en tête, afin de répondre au plus près à vos attentes et d’ancrer la revue dans un environnement informationnel en constante évolution. Comme vous pourrez le constater en feuilletant ce premier numéro « nouvelle formule », Conjoncture a adopté une mise en page moderne, aérée, qui facilite la lecture. Sur le fond, la revue est désormais divisée en trois parties : une première dédiée à l’actualité de votre Chambre et à la conjoncture marocaine et internationale. Elle est suivie par le « Zoom du mois », en milieu de revue, qui traite d’une problématique sectorielle ou transversale de l’économie marocaine. Enfin, la nouvelle rubrique « Regards d’experts » vous donne la parole pour faire profiter de votre expertise l’ensemble de notre communauté d’adhérents. En bref, Conjoncture se présente désormais comme une véritable « boîte à outils » à dispositionCEFOR entreprises des dirigeants qui nous font confiance. -

Keys Figures 2021

Kingdom of Morocco NATIONAL ACCOUNTS (BASE YEAR : 2007 : ) MONEY TOURISM الـسـيـاحـة الـنـقـد الـحسابـات الوطنيـة سـنـة األسـاس Gross domestic product by 2020* 2019 R 2018 R (In million of Dh) Number (in thousands) 2020* 2019 )بـمليون درهم( *2019 *2020 م م الـعـدد )بـاآلالف( Monetary Aggregate M3 1 485 118 1 370 518 3 الناجت الداخلي اإلجمالي sectors of activity مجمع النقد م حسب قطاعات األنشطة At current prices (in million of Dh) Liquid investment Guest nights registred in classified الليالي السياحية الـمنجزة مجمعات التوظيفات باألسعار الـجارية )بـمليون درهم( Primary sector 127 281 140 019 135 418 aggregates 796 454 741 517 establishments 6 968 25 244 بالـمؤسسات الـمصنفة السائلة (1) 3 Counterparts of M3 Aggregate(1) 1 485 118 1 370 518 الـقـطـاع األولـى Agriculture, forest and annexe services 116 317 128 643 124 083 including : international guest مقابالت الـمجمع م الفالحة، الغابة ومصالح ملحقة Fishing, aquaculture 10 964 11 376 11 335 منها : ليالي السياحة Lending to the economy 1 130 068 1 079 859 nights 3 470 17 406 ديون لالقتصاد Net claims on central الصيد، تربية األسماك Secondary sector 284 716 291 938 286 801 الدولية الديون الصافية لـمؤسسات الـقــطـــاع الـثــانــي Industry of mining extraction 24 721 26 337 25 455 government 240 994 212 432 Beds capacity in classified صناعـة االستـخـراج الـمـعـدنـي Industrial transformation (not including petroleum refinement)166 382 171 726 173 751 الطاقة اإليوائية بالـمؤسسات اإليداع على اإلدارة الـمركزية Net claims of deposit institutions on establishments الصناعة التحويلية )خـارج تكريـر النفط( Petroleum -

Weather Investment

Invest in the MEDA region, why, how ? Algeria Egypt / Israel / Jordan / Lebanon / Libya / Morocco / Palestinian Authority/ Syria / Tunisia / Turkey PAPERS & STUDIES n°22 April 2007 Collective work driven by Sonia Bessamra and Bénédict de Saint-Laurent Invest in the MEDA region, why how ? References This document has been produced within the context of a mission entrusted by the European Commission to the Invest in France Agency (AFII), assisted by the Istituto Nazionale per il Commercio Estero, ICE (Italy) and the Direction des Investissements, DI (Morocco), to develop a Euro‐Mediterranean Network of Mediterranean Investment Promotion Agencies (« ANIMA»). The n°of the contract is: ME8/B7‐4100/IB/99/0304. ISBN: 2‐915719‐28‐4 EAN 9782915719284 © AFII‐ANIMA 2007. Reproduction prohibited without the authorisation of the AFII. All rights reserved Authors This work is the second edition of a synopsis guide realised with contributions from various experts working under the ANIMA programme, especially for the writing of the project web site pages. The following authors have participated in the two editions: In 2006, Sonia Bessamra (free‐lance consultant) and Bénédict de Saint‐ Laurent (AFII) have fully updated the content, assisted by Pierre Henry, Amar Kaddouri, Emmanuel Noutary and Elsa Vachez (ANIMA team, translation, revisions); The former 2004 edition, which provides the guide frame, was directed by Bénédict de Saint‐Laurent (ANIMA, co‐ordination, synopsis, rewriting, data), Stéphane Jaffrin (ANIMA, on line implementation, some updates) and Christian Apothéloz (free‐lance consultant, co‐ordination), assisted by Alexandre Arditti, Delphine Bréant, Jean‐François Eyraud, Jean‐Louis Marcos, Laurent Mauron, Stéphanie Paicheler, Samar Smati, Nicolas Sridi et Jihad Yazigi (various thematic or country articles). -

Bmce Bank of Africa a N N U a L R E P O

20 17 ANNUAL REPORT BMCE BANK OF AFRICA Content Chairman’s Message ...................................................................................................................... 4 Presenting BMCE Bank Group A Member of FinanceCom Group ................................................................................6 Composition of the Board of Directors ...................................................................8 BMCE Bank Group around the World .................................................................... 10 Group Profile ............................................................................................................. 12 BMCE Bank’s Shareholders ...................................................................................... 13 BMCE Bank Group’s Strategy.................................................................................... 14 2017-2018 Highlights .............................................................................. 15 BMCE Bank in Morocco............................................................................................................. 16 Personal and Professional Banking ....................................................................... 16 Corporate Banking .................................................................................................... 18 Investment Banking ...................................................................................................20 Specialised Financial Subsidiaries ............................................................................22 -

Banque Marocaine Pour Le Commerce Et L'industrie Groupe BNP PARIBAS DOCUMENT DE RÉFÉRENCE RELATIF a L'exercice 2019

Banque Marocaine pour le Commerce et l’Industrie Groupe BNP PARIBAS DOCUMENT DE RÉFÉRENCE RELATIF A L’EXERCICE 2019 Enregistrement de l’Autorité Marocaine du Marché des Capitaux (AMMC) Conformément aux dispositions de la circulaire de l’AMMC, le présent document de référence a été enregistré par l’AMMC en date du 28 juillet 2020 sous la référence EN/EM/009/2020. Le présent document de référence ne peut servir de base pour effectuer du démarchage ou pour la collecte des ordres dans le cadre d’une opération financière que s’il fait partie d’un prospectus dument visé par l’AMMC. Mise à jour annuelle du dossier d’information relatif au programme d’émission de CD A la date d’enregistrement du présent document de référence, la mise à jour annuelle du dossier d’information relatif au programme d’émission de certificats de dépôt est composée : . du présent document de référence ; . de la note relative au programme de certificats de dépôt enregistrée par l’AMMC en date du 28 octobre 2019, sous la référence EN/EM/003/2019 et disponible sur le lien suivant : http://www.ammc.ma/sites/default/files/NOTE_CD_BMCI_003_2019.pdf Avertissement Enregistrement du Document de Référence Le présent Document de Référence a été enregistré par l’AMMC. L’enregistrement du Document de Référence n’implique pas authentification des informations présentées. Il a été effectué après examen de la pertinence et de la cohérence de l’information donnée. L’attention du public est attirée sur le fait que le présent Document de Référence ne peut servir de base pour le démarchage financier ou la collecte d’ordres de participation à une opération financière s’il ne fait pas partie d’un prospectus visé par l’AMMC. -

Rapport Annuel 2017.Pdf

RAPPORT ANNUEL 2017 COMPAGNIE D’ASSURANCES ET DE RÉASSURANCE Entreprise privée régie par la loi N°17-99 portant code des assurances 181, Bd d’Anfa - Casablanca -Maroc Tel: (212) 05 22 95 76 76 - Fax: (212) 05 22 36 98 12/14/16 www.atlanta.ma atlantamaroc atlanta_maroc 2 Compagnie d’assurances et de réassurance 3 SOMMAIRE MOT DU PRÉSIDENT IDENTITÉ & PROFIL Gouvernance & Management 1947 - 2017 : 70 ans en dates clés Nos valeurs et engagement Produits & Services Réseau de distribution ACTIVITÉS SECTEUR Marché de l’Assurance Marché Financier ACTIVITÉS ATLANTA ASSURANCES Interview avec M. Benchekroun Activités & Réalisations Atlanta Assurances ACTIVITÉS SOCIÉTALES Interview avec Mme Bensalah Labellisation RSE -CGEM Trophée Lalla Hasnaa « littoral durable » Partenaire leader du Pacte Mondial (PNUD Maroc) Activités sociétales RAPPORT FINANCIER Interview avec M. Tabine Résolutions 2017 États Comptables Rapports des commissaires aux comptes ANNEXE Réseau exclusif Atlanta Assurances 4 Compagnie d’assurances et de réassurance MOT DU PRÉSIDENT 5 Fiers de nos 70 ans d’histoire et de nos réalisations durant ces trois dernières années, le Groupe Atlanta s’inscrit dans cette même dynamique pour son plan stratégique 2018-2020. Mohamed Hassan BENSALAH Président-Directeur Général 6 Compagnie d’assurances et de réassurance L’année 2017 a été une année charnière pour Atlanta Assurances. Elle a marqué la fin de notre plan stratégique triennal Massar Attafaouk I, la préparation du plan Massar Attafaouk II, la célébration de notre 70ème anniversaire et le démarrage effectif de notre activité en Côte d’Ivoire. Ce contexte particulier impose un retour sur les réalisations de ces trois dernières années. -

RMSM-N°5.Pdf

EDITORIAL Mme Nada BIAZ Directrice Générale du Groupe ISCAE Face aux avancées technologiques changement constructif, à travers ultra-rapides et aux défis clima- les systèmes de veille, de qualité, de tiques, le maître mot est aujourd’hui pratique collaborative et d’innova- «Transition». Qu’il s’agisse de tran- tion. sition digitale, énergétique ou com- En phase avec l’intérêt particulier portementale, il est question de bri- accordé aux PME, dans la plupart ser le cercle de l’expérience, d’être des discours politiques au niveau réactif et de trouver des solutions international, le deuxième article créatives, en s’inscrivant dans la est une contribution à la réflexion tendance globale du développement sur l’entreprise familiale, son évolu- durable. Nous assistons bel et bien tion, ses principales réalisations et à des stratégies de rupture, et la re- ses perspectives d’avenir. cherche en management, qui se veut Le troisième article se présente inspirée par les préoccupations comme une étude exploratoire qui d’actualité, n’est pas en marge. combine les théories issues du Quoiqu’il faille reconnaître que domaine des systèmes d’informa- c’est la volonté politique en amont tion et celles du comportement du des forces qui influencent le monde consommateur, à travers le cas des qui confirmera ces ruptures, la ré- paiements électroniques. flexion théorique se doit d’apporter Les deux articles suivants concer- l’éclairage scientifique nécessaire nent deux tendances incontour- pour les justifier et les faire aboutir. nables, au cœur de la transition Au delà de l’exercice intellectuel, la dans le domaine de la finance, à recherche a ainsi un rôle essentiel savoir la finance islamique et la fi- à jouer dans l’avenir de l’humanité. -

Rapport Financier Annuel Exercice 2019

SOCIETE D’EQUIPEMENT DOMESTIQUE ET MENAGER « EQDOM » RAPPORT FINANCIER ANNUEL EXERCICE 2019 Rapport Financier Annuel 2019 1 SOMMAIRE I – PARTIE I: RAPPORT DE GESTION 2019…….………………………………………………………3 RAPPORT D’ACTIVITE…………………………………………………..….……………………………….4 GESTION DES RISQUES…………………………………….………………………………………………15 PROJETS DES RESOLUTIONS A SOUMETTRE A L'AGO…….……………....…………………21 PROJETS DES RESOLUTIONS A SOUMETTRE A L'AGO DES OBLIGATAIRES….…….24 COMPTES ANNUELS SOCIAUX ET CONSOLIDES…..…………………………………………….25 II– PARTIE II: RAPPORT SPECIAL DES COMMISSAIRES AUX COMPTES………………….77 RAPPORT SPECIAL DES COMMISSAIRES AUX COMPTES…………..……………….….…...78 ETAT DES HONORAIRES VERSES AUX CONTROLEURS DE COMPTES…………...........87 III-PARTIE III: COMMENTAIRE DES DIRIGEANTS ET PRESENTATION D’EQDOM…...88 COMMENTAIRE DES DIRIGEANTS……….…………….…………………………………….……….89 PRESENTATION GENERALE D’EQDOM……….……………………………..……….……………..90 IV-PARTIE IV: RAPPORT ESG……………………….…………………………………………………….....94 ELEMENTS GENEREAUX……….………………………………………………………………….………95 ELEMENTS SPECIFIQUES……………………………………………………….…………………………95 INFORMATION ENVIRONNEMENTALES……..…………………………………………………….95 INFORMATIONS SOCIALES……………………………………………………………………………….95 GOUVERNANCE..…………………………………………………………….……………………….……..…98 INFORMATIONS SUR LES PARTIES PRENANTES..….……………………………….….……..104 AUTRES..…………………………….……………………………………………………………….………….105 LISTE DES COMMUNIQUES DE PRESSE PUBLIES EN 2019..………………………..…………106 Rapport Financier Annuel 2019 2 PARTIE I : RAPPORT DE GESTION Rapport Financier Annuel 2019 3 RAPPORT D’ACTIVITE Rapport Financier Annuel -

Annual Report 2007

Annual Report 2007 WorldReginfo - 0dda50ba-2467-45d5-8e4b-97da50376e3d WorldReginfo - 0dda50ba-2467-45d5-8e4b-97da50376e3d In just a few years, Attijariwafa bank has performed the remarkable feat of meeting one challenge after another. Attijariwafa bank, which is market leader in all its business lines, is today considered as one of the key players in Morocco’s banking and financial services industry and in providing finance for the country’s keystone projects. Attijariwafa bank, with a healthy financial position and a risk management system meeting the highest international standards, has embarked on an ambitious yet well-planned international growth strategy. Given its ability to innovate and identify new niche growth opportunities, Attijariwafa bank is in the process of repeating overseas what it has achieved domestically and is fast becoming one of the most successful banks in the North and West African regions. Annual Report WorldReginfo - 0dda50ba-2467-45d5-8e4b-97da50376e3d 3 Contents WorldReginfo - 0dda50ba-2467-45d5-8e4b-97da50376e3d Chairman’s message 6 Governing bodies 8 Remarkable financial and commercial performance 2007 highlights 12 Attijariwafa bank in figures 14 An environment abounding in opportunities 16 Established leader in the domestic market Strong performance across the board Business activity indicators all positive 20 An effective commercial strategy 20 Keystone, value-creating projects 20 Contents Aggressive international strategy A watershed for Attijari bank Tunisie in North Africa 24 Encouraging acquisitions -

La Bourse De Casablanca ¥¥¥ Edito+Sommaire+Art 8/01/07 14:49 Page 1

••• Une ODB NEW 9/01/07 8:46 Page 1 Supplément au numéro du 26 janvier 2007 Ne peut être vendu séparément Directeur de la Publication : Fadel Agoumi En partenariat avec La Bourse de Casablanca ••• Edito+sommaire+art 8/01/07 14:49 Page 1 La Bourse de Casablanca souhaite la bienvenue aux entreprises qui se sont introduites en 2006 pour financer leur développement. ••• Edito+sommaire+art 8/01/07 14:49 Page 3 Le Guide de la Bourse Edito investissement en Bourse reste, hors période de spéculation, un placement à long L’ terme. Sur un horizon de placement de vingt ans, les actions n'ont jamais enregistré de rendement négatif, contrairement aux obligations et aux autres instruments de placement. Cela a été largement prouvé au point de devenir aujourd'hui une évidence. Sur des périodes plus courtes, la rentabilité de vos investissements dépendra plus de votre degré de connaissance des marchés, de votre capacité à identifier et à saisir les opportunités de placement et, enfin, du respect d'un certain nombre de règles. Pour investir en Bourse, il ne faut pas seulement avoir de l'argent : il faut également avoir du temps. Et du temps, il faut en avoir aussi pour lire ce guide que nous avons conçu, en partenariat avec la Bourse de Casablanca, dans le but de pallier le vide en matière de vulgarisation des concepts boursiers. Nous l'avons segmenté en onze chapitres que nous avons voulu aussi clairs et précis les uns que les autres. L'ambition de ce guide est de vous permettre de connaître la structure et les acteurs du marché boursier, de comprendre les valeurs mobilières et d'apprendre comment intervenir sur le marché des actions. -

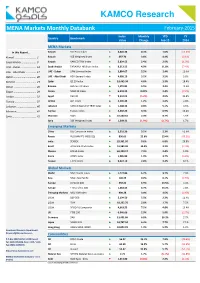

MENA Monthly Databank.Xlsx

KAMCO Research MENA Markets Monthly Databank February-2015 Index Monthly YTD FY Country Benchmark Value Change Feb-15 2014 MENA Markets In this Report… Kuwait KSE Price Index ▲ 6,601.43 0.4% 1.0% (13.4%) Kuwait ………………………………….2 Kuwait KSE Weighted Index ▲ 457.73 3.6% 4.3% (3.1%) Saudi Arabia ……………………….9 Kuwait KAMCO TRW Index ▲ 2,834.53 2.4% 2.9% (1.9%) UAE - Dubai ………………………….14 Saudi Arabia TADAWUL All Share Index ▲ 9,313.52 4.9% 11.8% (2.4%) UAE - Abu Dhabi ……………………17 UAE - Dubai DFM General Index ▲ 3,864.67 5.2% 2.4% 12.0% Qatar ……………………………………20 UAE - Abu Dhabi ADX General Index ▲ 4,686.19 5.1% 3.5% 5.6% Bahrain …………………………………23 Qatar QE 20 Index ▲ 12,445.34 4.6% 1.3% 18.4% Oman ……………………………………26 Bahrain Bahrain All Share ▲ 1,474.81 3.5% 3.4% 14.2% Egypt ………………………………….29 Oman MSM 30 Index ▲ 6,559.32 0.01% 3.4% (7.2%) Jordan …………………………………..32 Egypt EGX 30 ▼ 9,334.01 (5.2%) 4.6% 31.6% Tunisia ………………………………….37 Jordan ASE Index ▲ 2,195.46 1.2% 1.4% 4.8% Lebanon ……………………………….40 Lebanon KAMCO Beirut SE TRW Index ▲ 1,148.32 4.8% 5.1% 3.5% Morocco……………………….. 42 Tunisia Tunisia Index ▲ 5,442.26 4.3% 6.9% 16.2% Syria ……………………………… 45 Morocco MASI ▲ 10,460.62 2.3% 8.7% 5.6% Syria DSE Weighted Index ▼ 1,249.33 (1.0%) (1.7%) 1.7% Emerging Markets China SSE Composite Index ▲ 3,310.30 3.1% 2.3% 52.9% Russia RUSSIAN RTS INDEX ($) ▲ 896.63 21.6% 13.4% (45.2%) India SENSEX ▲ 29,361.50 0.6% 6.8% 29.9% Brazil BOVESPA Stock Index ▲ 51,583.09 10.0% 3.2% (2.9%) Mexico BOLSA Index ▲ 44,190.17 7.9% 2.4% 1.0% Korea KOSPI Index ▲ 1,985.80 1.9% 3.7% (4.8%) Taiwan