102555~[David E. Lindsey (Auth

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Econstor Wirtschaft Leibniz Information Centre Make Your Publications Visible

A Service of Leibniz-Informationszentrum econstor Wirtschaft Leibniz Information Centre Make Your Publications Visible. zbw for Economics National Bureau of Economic Research (NBER) (Ed.) Periodical Part NBER Reporter Online, Volume 2011 NBER Reporter Online Provided in Cooperation with: National Bureau of Economic Research (NBER), Cambridge, Mass. Suggested Citation: National Bureau of Economic Research (NBER) (Ed.) (2011) : NBER Reporter Online, Volume 2011, NBER Reporter Online, National Bureau of Economic Research (NBER), Cambridge, MA This Version is available at: http://hdl.handle.net/10419/61994 Standard-Nutzungsbedingungen: Terms of use: Die Dokumente auf EconStor dürfen zu eigenen wissenschaftlichen Documents in EconStor may be saved and copied for your Zwecken und zum Privatgebrauch gespeichert und kopiert werden. personal and scholarly purposes. Sie dürfen die Dokumente nicht für öffentliche oder kommerzielle You are not to copy documents for public or commercial Zwecke vervielfältigen, öffentlich ausstellen, öffentlich zugänglich purposes, to exhibit the documents publicly, to make them machen, vertreiben oder anderweitig nutzen. publicly available on the internet, or to distribute or otherwise use the documents in public. Sofern die Verfasser die Dokumente unter Open-Content-Lizenzen (insbesondere CC-Lizenzen) zur Verfügung gestellt haben sollten, If the documents have been made available under an Open gelten abweichend von diesen Nutzungsbedingungen die in der dort Content Licence (especially Creative Commons Licences), -

The Public Option in Housing Finance

The Public Option in Housing Finance Adam J. Levitin†* and Susan M. Wachter** The U.S. housing finance system presents a conundrum for the scholar of regulation because it defies description using the traditional regulatory vocabulary of command-and-control, taxation, subsidies, cap-and-trade permits, and litigation. Instead, since the New Deal, the housing finance market has been regulated primarily by government participation in the market through a panoply of institutions. The government’s participation in the market has shaped the nature of the products offered in the market. We term this form of regulation “public option” regulation. This Article presents a case study of this “public option” as a regulatory mode. It explains the public option’s rise as a governmental gap-filling response to market failures. The public option, however, took on a life of its own as the federal government undertook financial innovations that the private market had eschewed, in particular the development of the “American mortgage” — a long-term, fixed-rate fully amortizing mortgage. These innovations were trend-setting and set the tone for entire housing finance market, serving as functional regulation. The public option was never understood as a regulatory system due to its ad hoc nature. As a result, its integrity was not protected. Key parts of the system were privatized without a substitution of alternative regulatory measures. The consequence was a return to the very market failures that led to the public option in the first place, followed by another round of ad hoc public options in housing finance. This history suggests that an † Copyright © 2013 Adam J. -

Inflation Targeting

A SYMPOSIUM OF VIEWS Inflation Targeting Should the Federal Reserve in its conduct of monetary policy follow ome argue that while Fed Chairman Alan Greenspan, in office since 1987, has been an extraordinarily sub- Stle and skillful manager, his successor may not en- the European Central joy these unique skills. Thus, the system needs eventually to agree on a series of guiding benchmarks if not a target for use Bank and adopt some in the conduct of monetary policy. Globally, such an addi- tional tool might help in the convergence process and po- form of inflation target tentially create more stability for exchange rates. Others counter that it is not wise to lock the system range? TIE asked thirteen into a simplistic rule, or set of rules, particularly at a time of continued geopolitical uncertainty. Still others distinguished experts. counter that the European Central Bank established provisions that have successfully anticipated such ex- ternal shocks to the system. Is the time approaching for the U.S. central bank to adopt an inflation target or inflation target range? Or does the U.S. monetary system require a more prag- THE MAGAZINE OF INTERNATIONAL ECONOMIC POLICY matic and intuitive approach? To what extent should an 2099 Pennsylvania Avenue, N.W., Suite 950 Washington, D.C. 20006 inflation target be discretionary? Phone: 202-861-0791, Fax: 202-861-0790 www.international-economy.com 24 THE INTERNATIONAL ECONOMY WINTER 2004 I will therefore simply sketch out what has worked well for us at the ECB. We announced our monetary poli- Inflation targets are cy strategy in October 1998. -

Download (Pdf)

VOLUME 83 • NUMBER 12 • DECEMBER 1997 FEDERAL RESERVE BULLETIN BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM, WASHINGTON, D.C. PUBLICATIONS COMMITTEE Joseph R. Coyne, Chairman • S. David Frost • Griffith L. Garwood • Donald L. Kohn • J. Virgil Mattingly, Jr. • Michael J. Prell • Richard Spillenkothen • Edwin M. Truman The Federal Reserve Bulletin is issued monthly under the direction of the staff publications committee. This committee is responsible for opinions expressed except in official statements and signed articles. It is assisted by the Economic Editing Section headed by S. Ellen Dykes, the Graphics Center under the direction of Peter G. Thomas, and Publications Services supervised by Linda C. Kyles. Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis Table of Contents 947 TREASURY AND FEDERAL RESERVE OPEN formance can improve investor and counterparty MARKET OPERATIONS decisions, thus improving market discipline on banking organizations and other companies, During the third quarter of 1997, the dollar before the Subcommittee on Capital Markets, appreciated 5.0 percent against the Japanese yen Securities and Government Sponsored Enter- and 0.8 percent against the German mark. On a prises of the House Committee on Banking and trade-weighted basis against other Group of Ten Financial Services, October 1, 1997. currencies, the dollar appreciated 1.4 percent. The U.S. monetary authorities did not undertake 96\ Theodore E. Allison, Assistant to the Board of any intervention in the foreign exchange mar- Governors for Federal Reserve System Affairs, kets during the quarter. reports on the Federal Reserve's plans for deal- ing with some new-design $50 notes that 953 STAFF STUDY SUMMARY were imperfectly printed, including the Federal Reserve's view of the quality and quantity of In The Cost of Implementing Consumer Finan- $50 notes currently being produced by the cial Regulations, the authors present results for Bureau of Engraving and Printing, the options U.S. -

January 2021 Fri, Jan 1

January 2021 Fri, Jan 1 All Day Bank Holiday 1 January 2021 Mon, Jan 4 All Day 2021 AEA/ASSA Annual Meeting Virtual Event 8:30 AM – 8:55 AM Morning Checkpoint Call John to dial in 8:55 AM – 9:00 AM Blocked 9:00 AM – 9:30 AM Markets Group 9:05/9:20 Conference Call John to dial in 9:30 AM – 2:00 PM Blocked 2:00 PM ‐2:30 PM Meeting with Daleep Singh Skype 2:30 PM – 6:00 PM Blocked Tue, Jan 5 All Day 2021 AEA/ASSA Annual Meeting Virtual Event 9:00 AM – 9:30 AM Markets Group 9:05/9:20 Conference Call John to dial in 9:30 AM – 12:00 PM Blocked 12:00 PM – 12:30 PM Meeting with the Board John to dial in 12:30 PM – 1:00 PM Blocked 1:00 PM – 1:45 PM Weekly Email Discussion Skype 1:45 PM – 2:00 PM Blocked 2:00 PM – 2:30 PM Weekly Meeting with Chair Jay Powell Skype 2:30 PM – 3:30 PM Blocked 3:30 PM – 3:45 PM Tech Set‐Up for ASSA Panel: The Monetary‐Fiscal Nexus with Ultra Low Interest Rates Zoom 3:45 PM – 5:45 PM John to chair ASSA Panel: The Monetary‐Fiscal Nexus with Ultra Low Interest Rates Zoom 5:45 PM – 6:00 PM Blocked 1 January 2021 Wed, Jan 6 8:30 AM – 8:55 AM Morning Checkpoint Call John to dial in 8:55 AM – 9:00 AM Blocked 9:00 AM – 9:30 AM Markets Group 9:05/9:20 Conference Call John to dial in 9:30 AM – 10:00 AM Phone Call with Barbara Van Allen, ECNY John to initiate the call 10:00 AM – 10:15 AM Phone Call with Luiz Pereira da Silva, BIS Deputy General Manager John to initiate the call 10:15 AM – 10:30 AM Blocked 10:30 AM – 11:30 AM Government Relations Committee Meeting Skype 11:30 AM – 1:00 PM Blocked 1:00 PM – 2:00 PM FVP Interview -

Cross-Border Spillovers of Balance Sheet Normalization

For release on delivery 12:30 p.m. EDT July 11, 2017 Cross-Border Spillovers of Balance Sheet Normalization Remarks by Lael Brainard Member Board of Governors of the Federal Reserve System at “Normalizing Central Banks’ Balance Sheets: What Is the New Normal?” a conference sponsored by Columbia University’s School of International and Public Affairs and the Federal Reserve Bank of New York New York, New York July 11, 2017 When the central banks in many advanced economies embarked on unconventional monetary policy, it raised concerns that there might be differences in the cross-border transmission of unconventional relative to conventional monetary policy.1 These concerns were sufficient to warrant a special Group of Seven (G-7) statement in 2013 establishing ground rules to address possible exchange rate effects of the changing composition of monetary policy.2 Today the world confronts similar questions in reverse. In the United States, in my assessment, normalization of the federal funds rate is now well under way, and the Federal Reserve is advancing plans to allow the balance sheet to run off at a gradual and predictable pace. And for the first time in many years, the global economy is experiencing synchronous growth, and authorities in the euro area and the United Kingdom are beginning to discuss the time when the need for monetary accommodation will diminish. Unlike in previous tightening cycles, many central banks currently have two tools for removing accommodation. They can therefore pursue alternative normalization strategies--first seeking to guide policy rates higher before initiating balance sheet runoff, as in the United States, or instead starting to shrink the balance sheet before initiating a 1 I am grateful to John Ammer, Bastian von Beschwitz, Christopher Erceg, Matteo Iacoviello, and John Roberts for their assistance in preparing this text. -

Jelena Mcwilliams-FDIC

www-scannedretina.com Jelena McWilliams-FDIC Jelena McWilliams-FDIC Voice of the American Sovereign (VOAS) The lawless Municipal Government operated by the "US CONGRESS" Washington, D.C., The smoking gun; do you get it? John Murtha – Impostor committed Treason – Time to sue his estate… Trust through Transparency - Jelena McWilliams - FDIC Chair Theft through Deception - Arnie Rosner - American sovereign, a Californian — and not a US Citizen via the fraudulent 14th Amendment. Sovereignty! TRUMP – THE AMERICAN SOVEREIGNS RULE AMERICA! All rights reserved - Without recourse - 1 of 120 - [email protected] - 714-964-4056 www-scannedretina.com Jelena McWilliams-FDIC 1.1. The FDIC responds - the bank you referenced is under the direct supervision of the Consumer Financial Protection Bureau. From: FDIC NoReply <[email protected]> Subject: FDIC Reply - 01003075 Date: April 29, 2019 at 6:36:46 AM PDT To: "[email protected]" <[email protected]> Reply-To: [email protected] April 29, 2019 Ref. No.: 01003075 Re: MUFG Union Bank, National Association, San Francisco, CA Dear Arnold Beryl Rosner: Thank you for your correspondence, which was received by the Federal Deposit Insurance Corporation (FDIC). The FDIC's mission is to ensure the stability of and public confidence in the nation's financial system. To achieve this goal, the FDIC has insured deposits and promoted safe and sound banking practices since 1933. We are responsible for supervising state- chartered, FDIC-insured institutions that are not members of the Federal Reserve System. Based on our review of your correspondence, the bank you referenced is under the direct supervision of the Consumer Financial Protection Bureau. -

Is Inflation Really Transitory?

Is Inflation Really Transitory? By Eric Grover National Review August 17, 2021 Financial-market indicators point to a persistent uptick in inflation. DESPITE a few recent hints of unease, the Fed still maintains that the current surge in inflation is “transitory.” That seems optimistic: The central bank has been stoking inflation and is stubbornly blind to the danger of getting more than it bargained for, of letting loose what Nobel Prize– winning economist Friedrich Hayek described as the “tiger.” Fed chairman Paul Volcker caged inflation after it’d crested at 13.5 percent in 1980. Since then, however, the Fed, politicians, consumers, and producers have become complacent about the risk that it might escape again. The current cocktail of money-printing, massive deficit spending, pandemic- related supply-chain disruptions, and pent-up demand coming out of COVID-19 hibernation means inflation ahead — and not just for the short term. The outlook is only made worse by the hit to the supply side that will come from increased regulation and taxes, not to speak of the boost to energy costs that will flow from the administration’s hostility to fossil fuels. The Fed’s balance sheet has ballooned from $900 billion in August 2008 to a whopping $8.2 trillion in mid July 2021. However, by paying banks interest to park excess reserves held at the Fed, the central bank has managed to keep new dollars from entering the economy in the form of credit, thereby holding down inflation. Now, printed money is showing up in consumption and price data, and the longer the “transitory” surge endures, the more difficult it will be to contain. -

Data Appendix

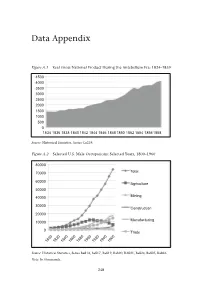

Data Appendix Figure A.1 Real Gross National Product During the Antebellum Era: 1834–1859 4500 4000 3500 3000 2500 2000 1500 1000 500 0 1834 1836 1838 1840 1842 1844 1846 1848 1850 1852 1854 18561858 Source: Historical Statistics, Series Ca219. Figure A.2 Selected U.S. Male Occupations: Selected Years, 1800–1960 80000 70000 Total 60000 Agriculture 50000 40000 Mining 30000 Construction 20000 Manufacturing 10000 0 Trade 1800 1820 1840 1860 1880 1900 1920 1940 1960 Source: Historical Statistics, Series Ba814, Ba817, Ba819, Ba820, BA821, Ba824, Ba825, Ba826. Note: In thousands. 248 Source Source Note Source Figure A.5 Figure A.4 Figure A.3 : ThisistheSchwert’sIndexofCommonStock. : HistoricalStatistics,SeriesAa36,Aa46, Aa56. : HistoricalStatistics,SeriesCh411. : HistoricalStatistics,SeriesCj979. 100000000 150000000 200000000 250000000 300000000 100000 120000 10 12 14 16 50000000 20000 40000 60000 80000 0 2 4 6 8 0 1802 0 U.S. PopulationforSelectedYears:1790–1990 Total NumberofU.S.BusinessFailures:1857–1997 1805 Stock IndexDuringtheAntebellumEra:1802–1870 1857 1790 1830 1860 1890 1920 1950 1990 1808 1863 1869 1811 1875 1814 1881 1817 1887 1820 1893 1823 1899 1826 1905 1829 1911 1832 1917 1835 1923 1838 1929 1841 1935 1941 1844 1947 1847 1953 1850 1959 1853 Total RuralPopulation Total UrbanPopulation Total Population Total 1965 1856 Data Appendix 1971 1859 1977 1862 1983 1865 1989 1995 1868 249 Note Source Note Source Figure A.8 up totheGreatDepression:1869–1929 Figure A.7 250 Source: Figure A.6 : ThisistheIndustrialsIndex. : ThisdataisfromGallman-Kuznetsestimationandin1929dollars. -

Annual Report 2014–15 © 2015 National Council of Applied Economic Research

National Council of Applied Economic Research Annual Report Annual Report 2014–15 2014–15 National Council of Applied Economic Research Annual Report 2014–15 © 2015 National Council of Applied Economic Research August 2015 Published by Dr Anil K. Sharma Secretary & Head Operations and Senior Fellow National Council of Applied Economic Research Parisila Bhawan, 11 Indraprastha Estate New Delhi 110 002 Telephone: +91-11-2337-9861 to 3 Fax: +91-11-2337-0164 Email: [email protected] www.ncaer.org Compiled by Jagbir Singh Punia Coordinator, Publications Unit ii | NCAER Annual Report 2014-15 NCAER | Quality . Relevance . Impact The National Council of Applied Economic Research, or NCAER as it is more commonly known, is India’s oldest and largest independent, non-profit, economic policy research institute. It is also one of a handful of think tanks globally that combine rigorous analysis and policy outreach with deep data collection capabilities, especially for household surveys. NCAER’s work falls into four thematic NCAER’s roots lie in Prime Minister areas: Nehru’s early vision of a newly- independent India needing independent • Growth, macroeconomics, trade, institutions as sounding boards for international finance, and economic the government and the private sector. policy; Remarkably for its time, NCAER was • The investment climate, industry, started in 1956 as a public-private domestic finance, infrastructure, labour, partnership, both catering to and funded and urban; by government and industry. NCAER’s • Agriculture, natural resource first Governing Body included the entire management, and the environment; and Cabinet of economics ministers and • Poverty, human development, equity, the leading lights of the private sector, gender, and consumer behaviour. -

The Problem of Predatory Lending: Price Lauren E

Maryland Law Review Volume 65 | Issue 3 Article 3 Decisionmaking and the Limits of Disclosure: The Problem of Predatory Lending: Price Lauren E. Willis Follow this and additional works at: http://digitalcommons.law.umaryland.edu/mlr Part of the Banking and Finance Commons, and the Property Law and Real Estate Commons Recommended Citation Lauren E. Willis, Decisionmaking and the Limits of Disclosure: The Problem of Predatory Lending: Price, 65 Md. L. Rev. 707 (2006) Available at: http://digitalcommons.law.umaryland.edu/mlr/vol65/iss3/3 This Article is brought to you for free and open access by the Academic Journals at DigitalCommons@UM Carey Law. It has been accepted for inclusion in Maryland Law Review by an authorized administrator of DigitalCommons@UM Carey Law. For more information, please contact [email protected]. MARYLAND LAW REVIEW VOLUME 65 2006 NUMBER 3 © Copyright Maryland Law Review 2006 Articles DECISIONMAKING AND THE LIMITS OF DISCLOSURE: THE PROBLEM OF PREDATORY LENDING: PRICE LAUREN E. WILLIS* INTRODUCTION ................................................. 709 I. PREDATORY LENDING AND THE HOME LOAN MARKET ...... 715 A. The Home Lending Revolution ........................ 715 1. The Twentieth Century Marketplace: Standardized Terms, Limited and Advertised Prices, and Low Risk. 715 2. The Brave New World of ProliferatingProducts, Price, and R isk ........................................ 718 3. Evidence of Predatory Home Lending ............... 729 B. A New Definition of Predatory Lending ................. 735 II. FEDERAL LAW REGULATING THE PRICING OF HOME- SECURED LOANS: DISCLOSURE AS PANACEA ................ 741 A. The Rational Actor Decisionmaker Model ............... 741 B. CurrentFederal Law .................................. 743 C. Even a Rational Actor Could Not Use the Federal Disclosures to Price Shop in Today's Marketplace ....... -

Working Paper Series Department of Economics Alfred Lerner College of Business & Economics University of Delaware

Working Paper Series Department of Economics Alfred Lerner College of Business & Economics University of Delaware Working Paper No. 2004-07 The Constitutional Creation of a Common Currency in the U.S. 1748-1811: Monetary Stabilization Versus Merchant Rent Seeking. Farley Grubb FARLEY GRUBB THE CONSTITUTIONAL CREATION OF A COMMON CURRENCY IN THE U.S., 1748-1811: MONETARY STABILIZATION VERSUS MERCHANT RENT SEEKING The value of having a single currency, the optimal size of currency unions, and the cost of forming such unions, is an unresolved debate1. An important aspect of this debate is the empirical success claimed for currency unions such as the United States. The fact that otherwise-sovereign states within the United States are not legally allowed to issue their own currency, thus creating a single cur- rency zone for the whole United States based on the U.S. dollar, is commonly used as an example for emulation and as justification for policy choices, such as the current move toward a European currency union based on the Euro2. The benefits of this constitutionally created U.S. currency union and, by analogy, the benefits for other politically manufactured currency unions are as- sumed to be obvious, namely a reduction in monetary instability and exchange- rate transactions costs within the union thereby stimulating long-run economic growth. These alleged benefits for the U.S., however, are not derived from market evidence, but from simple theoretical assertions and from a historical literature that has taken as fact the rhetoric of the winning side at the U.S. Con- stitutional Convention. Independent of theory and rhetoric, little is known about how and why the U.S.