Callidus Software Inc

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Research Hype Cycle for Human Capital Management Software, 2011

Research Publication Date: 2 August 2011 ID Number: G00215655 Hype Cycle for Human Capital Management Software, 2011, Thomas Otter, James Holincheck, Jeff Freyermuth The Hype Cycle for HCM software helps organizations with their HCM technology investments by providing insight into the maturity of key applications and technologies. © 2011 Gartner, Inc. and/or its affiliates. All rights reserved. Gartner is a registered trademark of Gartner, Inc. or its affiliates. This publication may not be reproduced or distributed in any form without Gartner's prior written permission. The information contained in this publication has been obtained from sources believed to be reliable. Gartner disclaims all warranties as to the accuracy, completeness or adequacy of such information and shall have no liability for errors, omissions or inadequacies in such information. This publication consists of the opinions of Gartner's research organization and should not be construed as statements of fact. The opinions expressed herein are subject to change without notice. Although Gartner research may include a discussion of related legal issues, Gartner does not provide legal advice or services and its research should not be construed or used as such. Gartner is a public company, and its shareholders may include firms and funds that have financial interests in entities covered in Gartner research. Gartner's Board of Directors may include senior managers of these firms or funds. Gartner research is produced independently by its research organization without input or influence from these firms, funds or their managers. For further information on the independence and integrity of Gartner research, see "Guiding Principles on Independence and Objectivity" on its website, http://www.gartner.com/technology/about/ombudsman/omb_guide2.jsp TABLE OF CONTENTS Analysis ...................................................................................................................................... -

Und Dergrad Scho Duate Ca Ool of E Areer P Univ Enginee Plans Su

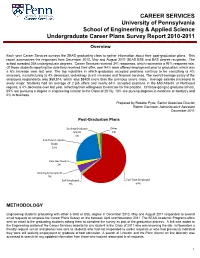

CAREER SERVICES University of Pennsylvania School of Engineering & Applied Science Undergraduate Career Plans Survey Report 2010-2011 Overview Each year Career Services surveys the SEAS graduating class to gather information about their post-graduation plans. This report summarizes the responses from December 2010, May and Auguust 2011 SEAAS BSE and BAS degree recipients. The school awarded 358 undergraduate degrees. Career Services received 341 responses, which represents a 95% response rate. Of those students reporting the date they received their offer, over 94% were offered employment prior to graduation, which was a 6% increase over last year. The top industries in which graduates accepted positions continue to be consulting (a 4% increase)), manufacturing (a 4% decrease), technology (a 6% increase) and financial services. The overall average salary of the employed respondents was $68,814, which was $6400 more than the previous year’s class. Average salaries increased in every major. Students had an average of 2 job offers and nearly 64% accepted positions in the Mid-Atlantic or Northeast regions, a 4% decrease over last year, reflecting their willingness to relocate for the position. Of those going to graduate school, 65% are pursuing a degree in engineering (similar to the Class of 2010), 13% are pursing degrees in medicine or dentistry and 6% in business. Prepared by Rosette Pyne, Senior Associate Director Robert Gannone, Administrative Assistant December 2011 Post-Graduation Pllans Seeking Graduate Other School 1% 1% Full‐Time Graduate Study 25% Post‐Bac Studies 2% Seeking Employment 5% Self‐Employed Full‐Time Employed 2% 64% METHODOLOGY Engineering students graduating with either a BAS or BSE degree in December 2010, May and August 2011 responded to several email requests to complete the Career Plans Survey on line between April and November 2011. -

158877363.Pdf

Company Name NASSCOM Contact Salutation NASSCOM Contact First Name 3D PLM Software Solutions Ltd Mr. Sudarshan 3Five8 Technologies Pvt Ltd Ms. Sangeeta 3Forz Innovations Software Pvt Ltd Mr. Janakiram 3i Infotech Ltd Mr. Prathmesh 4C-Learning Solutions Pvt Ltd Mr. Vivek 4i Apps Solutions Pvt Ltd Mr. Kathiresh Kumar 7Seas Entertainment Ltd Mr. Maruti Sanker A G Technologies Pvt Ltd Mr. Anup A N Buildwell Pvt Ltd Mr. Rohit A T Kearney Ltd Ms. Shilpi A1 Future Technologies Mr. Srish Kumar Aabasoft Mr. Sujas AABSyS Information Technology Pvt Ltd Mr. Ravi Aaric Technologies Pvt Ltd Mr. Vipin Aarupadai Veedu Institute of Technology (VinayakaMr. Missions University) C Thara Abiba Systems Pvt Ltd Mr. Senthil ABM Knowledgeware Ltd Mr. Govind Abra Technologies Pvt Ltd Mr. Yogeshnath AbsolutData Research & Analytics SolutionsMr. Pvt Ltd Suhale Accel Frontline Ltd Mr. Ravi Sankar AccelTree Software Pvt Ltd Mr. Sasikumar Accelya Kale Solutions Ltd Mr. Mitul Accenture Services Pvt Ltd Mr. Rajesh Acclaris Business Solutions Pvt Ltd Mr. Subrata Accretive Health Pvt Ltd Mr. Shailendra Pratap Acidaes Solutions Pvt Ltd Mr. Rahul Ackcezione Technologies Pvt Ltd Mr. Kishore ACL Mobile Ltd Ms. Gunjan Acliv Technologies Pvt Ltd Mr. Achutha ACN Infotech (India) Pvt Ltd Mr. Chaman Acteva Solutions Management Pvt Ltd Ms. Sreeparna ActWitty Software Systems Pvt Ltd Mr. Samarth Adaptive Processes Consulting Pvt Ltd Ms. Ananya ADCC Infocad Pvt Ltd Mr. Amit Add Technologies (India) Ltd Mr. William Adhi Software Pvt Ltd Mr. K Aditya Birla Minacs Worldwide Ltd Ms. Pooja Adobe Systems India Pvt Ltd Mr. Naresh Chand ADP India Ltd Mr. S ADP Pvt Ltd Mr. -

The 2012 Global Outsourcing 100® Sub-Lists • Best 10 Overall • by Industry Focus • by Service Area • by Region Served • Honors and Highlights

The 2012 Global Outsourcing 100® Sub-Lists • Best 10 Overall • By Industry Focus • By Service Area • By Region Served • Honors and Highlights Best 10 Leaders in Overall Revenue Rising Stars in Overall Revenue Leaders in Revenue Growth Accenture Emerio GlobeSoft Aegis ADP Endava Altisource Compass Group Freeborders China Talent Group CSC GeBBS Healthcare Solutions Ci&T Getronics Workspace Alliance NETAS EPAM Systems HP Enterprise Services Scicom Grupo ASSA Infosys SoftServe Integreon Managed Solutions ISS Symphony House Berhad Long View Systems Sodexo Synygy VanceInfo Wipro Technologies Xceed Wicresoft Rising Stars in Number of Rising Stars in Revenue Growth Leaders in Number of Employees Employees Bleum Accenture Azure Knowledge Corporation Cross-Tab Marketing Services Aegis Emerio GlobeSoft eMids Technologies Compass Group Freeborders First Line Software Convergys GeBBS Healthcare Solutions GeBBS Healthcare Solutions CSC Nagarro Island Logic HCL Technologies Scicom National Medical Billing Services Infosys SoftServe ReSource Pro ISS Symphony House Berhad SoftServe Sodexo Ugam Solutions Systems In Motion Wipro Technologies Xceed Leaders in No. of Centers Leaders in Employee Growth Rising Stars in Employee Growth Worldwide Altisource AbsolutData CBRE Colliers Global Corporate Cassidy Turley Cross-Tab Marketing Services Solutions ChinaSoft International CrysTelCall Compass Group Ci&T eMids Technologies Diebold Integrated Services Diebold Integrated Services First Line Software EMCOR Group Globant Freeborders ISS TeleTech GeBBS Healthcare -

COMPETITIVE ANALYSIS Worldwide Sales Incentive

COMPETITIVE ANALYSIS Worldwide Sales Incentive Compensation Management Applications 2007 Vendor Profiles: State-of-the-Market Viewpoint and Future Market Predictions Mary Wardley Judy Hodges Albert Pang IDC OPINION Sales compensation has become more complex and critical to an organization's growth and success. Automating sales compensation not only increases accuracy and consistency but also enables companies to create and manage change within their incentive compensation management process. IDC believes: The market for automated sales incentive compensation management applications has rebounded and will continue to increase its profile and growth. Paper-based and homegrown systems are being replaced by sales incentive compensation management solutions as organizations are realizing the measurable value of implementing these flexible and strategic solutions. On-demand software as a service (SaaS) offerings for sales compensation management will be extremely appealing for companies, particularly those in the small and medium-sized business (SMB) segment, which are seeking value and the time-to-market advantage over on-premise models. Sarbanes-Oxley (SOX) compliance is a key market driver for the adoption of these sales transaction solutions, as companies seek to comply with government regulations for the protection of their brand and value in the marketplace. Established sales incentive compensation vendors will need to fend off encroaching new market entrants by developing new products or product enhancements, expanding their services offerings, and forging new partnerships. Mobile-enabled sales compensation solutions will become more prevalent in the market as companies seek to give their sales managers, salespeople, and senior executives access to critical information about their business performance, from any location. -

Global Outsourcing

SPECIAL ADVERTISING SECTION “My job is to make sure that risk is not a trade-off in here” Robert Marley, ISS Technical Specialist in THE 2013 Critical Infrastructures, worldwide GLOBAL OUTSOURCING IN Banks around the world turn to Bob and ISS for deep insights into partners HIP minimising risk and maximising uptime. Bob works closely with WitH clients to manage and limit the operational risk of a property’s critical systems and infrastructure. And, thanks to Bob’s commitment, they can rest assured. Risk management is an integral part of what ISS can do for you. We are half a million committed people, serving your people with tailored solutions and a human touch. All so you can grow your business. FACILITY MANAGEMENT | CLEANING | SUPPORT | PROPERTY | CATERING | SECURITY | issworld.com/fm ISS ADvert 203x267mm_Fortune_Bob-risk_010413.indd 1 04-04-2013 13:30:00 “My job is to make sure that risk is not a trade-off in here” Robert Marley, ISS Technical Specialist in 2013 Critical Infrastructures, worldwide Banks around the world turn to Bob and ISS for deep insights into minimising risk and maximising uptime. Bob works closely with clients to manage and limit the operational risk of a property’s critical systems and infrastructure. And, thanks to Bob’s commitment, they can rest assured. Risk management is an integral part of what ISS can do for you. We are half a million committed people, serving your people with tailored solutions and a human touch. All so you can grow your business. FACILITY MANAGEMENT | CLEANING | SUPPORT | PROPERTY | CATERING | SECURITY | issworld.com/fm ISS ADvert 203x267mm_Fortune_Bob-risk_010413.indd 1 04-04-2013 13:30:00 SPECIAL ADVERTISING SECTION THE BUilding 2013 ProdUctivitY, GLOBAL OUTSOURCING STEP When they go shopping for outsourcing partners, more and more companies are looking to establish strategic, collaborative BY relationships with advisers they can trust. -

The 2011 Global Outsourcing 100® Sub-Lists • Best 10 Overall • by Industry Focus • by Service Area • by Region Served • Honors and Highlights

The 2011 Global Outsourcing 100® Sub-Lists • Best 10 Overall • By Industry Focus • By Service Area • By Region Served • Honors and Highlights Best 10 Leaders in Overall Revenue Rising Stars in Overall Revenue Leaders in Revenue Growth Accenture BRQ IT Services Ci&T ARAMARK China Talent Group Hewlett-Packard Capgemini CIeNET International hiSoft Technology International CSC Emerio GlobeSoft Integreon Hewlett-Packard Ericpol Telecom iSoftStone Infosys Technologies Freeborders PCCW Solutions ISS Globant SourceRight Solutions Johnson Controls Grupo ASSA Stefanini IT Solutions Sodexo Scicom TCI Wipro Technologies SoftServe Wicresoft Rising Stars in Number of Rising Stars in Revenue Growth Leaders in Number of Employees Employees Auriga Accenture Azure Knowledge Corporation Azure Knowledge Corporation ARAMARK China Talent Group China Talent Group Convergys CIeNET International Extensya CSC Emerio GlobeSoft GeBBS Healthcare Solutions HCL Technologies GeBBS Healthcare Solutions Global eProcure Infosys Technologies Globant Grupo ASSA ISS M&Y Global Services ReSource Pro Sitel Scicom SoftServe Sodexo SoftServe UnitedLex Wipro Technologies Xceed Leaders in Employee Growth Rising Stars in Employee Growth Leaders in No. of Centers Worldwide Ci&T Auriga ARAMARK Hewlett-Packard Azure Knowledge Corporation CB Richard Ellis hiSoft Technology International China Talent Group Colliers International Integreon Extensya Cushman & Wakefield iSoftStone GeBBS Healthcare Solutions Diebold PCCW Solutions Global eProcure EMCOR Group SourceRight Solutions Grupo ASSA -

Dennis M. Spahr Vita

DENNIS M. SPAHR Kelley School of Business, Indiana University; 1309 E. 10th St.; Bloomington, IN 47405 812.855.7364 847.372.6748 (mobile) [email protected] EDUCATION MBA Stephen M. Ross School of Business; University of Michigan, Ann Arbor 1993 Marketing and General Management BA Indiana University, Bloomington 1986 Chemistry ACADEMIC AND RELATED TEACHING EXPERIENCE Kelley School of Business, Indiana University, Bloomington 2018 - Present Lecturer, Department of Marketing and Center for Global Sales Leadership Courses Taught: M330 Consultative Selling, M355 Personal Selling and Sales Management, M360 Sales for Social Impact, M405 Consumer Behavior, M426 Sales Management Driehaus College of Business and Kellstadt Graduate School of Business, DePaul University 2017 Adjunct Professor – Center for Sales Leadership Courses Taught: MKT 383 Analytical Sales (undergraduate), MKT 583 Monetizing Marketing Strategy (graduate) Carlson School of Management at the University of Minnesota 2014 and 2016 Guest Teacher – Sales Executive Leadership Program Sessions Taught: “Motivating and Enabling the Sales Effort” (May 2016) and “Best Practices for Hiring High Performing Salespeople” (May 2014) Quinlan School of Business at Loyola University of Chicago 2002, 2003 and 2009 Guest Teacher – Human Resources & Industrial Relations Sessions Taught: “Sales Incentive Compensation” (Nov 2009), “Sales Incentive Programs” (March 2003), “Market Pricing” (September 2002) Ralph and Lucy Schey Centre at Ohio University 2008 Speaker – 11th Annual Sales Symposium Sessions Taught: -

BSBA Class of 2020 Full-Time Employment Statistics

BSBA Class of 2020 Full-Time Employment Statistics Compensation Summary Salary Data by Industry Average Base $76,200 Percent Average Median High Low Median Base $75,000 Financial/Insurance 37% $81,700 $85,000 $150,000 $53,000 High-Low Range $150,000-44,000 Consulting 22% $78,000 $80,000 $90,000 $60,000 Average Signing Bonus $10,000 Technology 9% $70,700 $61,500 $118,000 $44,000 All salaries in this report are rounded to the nearest hundred. Consumer 7% $66,000 $67,500 $72,000 $57,000 Packaged Goods Class Profiles (upon enrollment) Retail 6% $64,800 $62,500 $75,000 $57,000 Class of 2022 Class of 2021 Class of 2020 Media/Entertainment 5% * * * * # of Students 163 225 161 Accounting 4% $64,100 $63,000 $72,500 $60,000 % Women 47% 43% 48% Healthcare 3% * * * * % Underrepresented 19% 40% 24% Other 7% * * * * Minority Grand Total 100% $76,200 $75,000 $150,000 $44,000 Average SAT Score 1510 1507 1511 Percentages are calculated as a percentage of domestic population. *Salary not displayed when fewer than three data points. Other industries: Nonprofit, Government, Manufacturing, Energy and Real Estate Salary Data by Function Employment by Industry Percent Average Median High Low Finance 34% $81,200 $85,000 $150,000 $60,000 Investment Banking 14% $87,700 $85,000 $150,000 $70,000 Other 7% Financial Analysis 8% $82,800 $84,000 $88,000 $75,000 Healthcare 3% Venture Cap/Pr. Accounting 4% Equity/Pr. Wealth 7% $71,900 $72,500 $85,000 $60,000 Financial/ Asset Mgmt. Media/Entertainment 5% Insurance 37% Other Finance 5% $76,900 $80,000 $88,000 $62,500 Retail -

The Media's Watching Vault! Here's a Sampling of Our Coverage

The media’s watching Vault! Here’s a sampling of our coverage. “Unflinching, fly-on-the-wall reports... No one gets past company propaganda to the nitty-gritty inside dope better than these guys.” — Knight-Ridder newspapers “Best way to scope out potential employers...Vault has sharp insight into corporate culture and hiring practices.” — Yahoo! Internet Life “Vault has become a de facto Internet outsourcer of the corporate grapevine.” — Fortune “For those hoping to climb the ladder of success, [Vault’s] insights are priceless.” — Money.com “Another killer app for the Internet.” — New York Times “If only the company profiles on the top sites would list the ‘real’ information... Sites such as Vault do this, featuring insights and commentary from employees and industry analysts.” — The Washington Post “A rich repository of information about the world of work.” — Houston Chronicle TOP50VAULT GUIDE TO THE TOP 50 CONSULTING CONSFIRMS FIRMS © 2002 Vault Inc. TOP50VAULT GUIDE TO THE TOP 50 CONSULTING CONSFIRMS FIRMSDOUGLAS CANTOR AND CLAY RISEN © 2002 Vault Inc. Copyright © 2002 by Vault Inc. All rights reserved. All information in this book is subject to change without notice. Vault makes no claims as to the accuracy and reliability of the information contained within and disclaims all warranties. No part of this book may be reproduced or transmitted in any form or by any means, electronic or mechanical, for any purpose, without the express written permission of Vault Inc. Vault, the Vault logo, and “the insider career networkTM” are trademarks of Vault Inc. For information about permission to reproduce selections from this book, contact Vault Inc., P.O. -

The 2012 Global Outsourcing

SPECIAL ADVERTISING SECTION the 2012 global outsourCing 100 Collaborative outsourCing—where customers and service providers work together to innovate new processes and leverage new technologies—is on the rise among leaders in the industry. utsourcing has always been still important, forward-looking businesses have regarded as a simple but powerful value embraced a more strategic version of outsourcing. proposition. It wasn’t intended to change They are now using it not just to trim expenses but the world or even change the way a com- also to add value in a variety of other ways, and in pany grew its business. The goal was to the process they’re acquiring the agility they need save money, and it was achieved in three to build markets and introduce new products and key ways: by assigning work to regions services. In the IAOP’s 2011 State of the Industry where labor costs were lower; by leverag- Survey, 56% of respondents said they wanted to ing the efficiencies of shared services; and use outsourcing to increase their flexibility and by harnessing the expertise of third-party help meet corporate business goals. providers that could do a specific task faster—and Ooften, better—than a company could on its own. Clouds on the Horizon Here’s the good news: It works. According to the One need only look at current trends throughout International Association of Outsourcing Profes- industry—the big one being cloud computing—to in sionals (IAOP), the industry’s standard-setting and see how this newer, more expansive iteration of out- partnership advocacy organization, outsourcing has proved so sourcing is taking hold. -

Co Unde Car Ollege Ergra Reer P E of a Aduate Plans Arts & E Clas Surv & Scie Ss of Vey Re Nces 2011 Eport

College of Arts & Sciences Undergraduate Class of 2011 Career Plans Survey Report Each year Career Services surveys the College of Arts and Sciences graduating class to gather information about their post-graduation plans. This report summarizes the responses from Deceember 2010, May and August 2011 Bachelor of Arts degree recipients. CONTENTS Section Page Summary 2 Salary Overview 3 Interviews, Offers, and Geographic Locations 4 Top Employers & Graduate Schools 4 Undergraduate Salaries by Industry 5 Undergraduate Salaries by Job Type 6 Graduate Study and Full-Time Employment by Major 8 Full-time Employment by Employer Organization and Major 35 Methodology Students were asked via several e-mail requests during Spring 2011 to compllete an online version of the Career Plans Survey. Follow-up emails/surveys were sent between June and Novembber 2011 to those students who had not responded or had previously indicated they were “still seeking.” A total of 1,201 surveys were returned, resulting in a 74% response rate. Prepared in December 2011 by: Kelly Cleary, Senior Associate Director Kamila DeAngelis, Administrative Assistant 1 CAREER PLANS SURVEY College of Arts and Sciences - Class of 2011 PRIMARY POST-GRAD PLANS, 2011 Seeking Seeking Other Primary Post-Grad Plans, Graduate Employment 1% 2011 School 7% College of Arts & Sciences 2% Full-Time Employed 56% 671 Intern/ Short-Term 6% 70 Other Education Part-Time Employment 2% 20 2% Graduate School 24% 288 Other Education 2% 30 Graduate Seeking Graduate School 2% 26 School 24% Full‐time Seeking