Latin America's Top Acquirers Transactions (Bil.) in 2017

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Payments Insights. Opinions. Volume 24

#payments insights. opinions. Tap. Touch. Speak. Grab and Seven themes impacting the future of payments go. The way we make payments is changing faster than any Winners in the future payments ecosystem will be those that make the right decisions other area of financial services. today. Understanding these seven key themes reshaping payments will help leaders make those decisions and determine how best to differentiate themselves in this New technology and changing fast-changing landscape. customer expectations are shattering the status quo and ushering in a growing number Continued on page 3 of new players that are challenging the traditional role of banks. Volume 24 03 Seven themes impacting the future of payments Understanding the themes transforming payments can help banks make strategic investment decisions and emerge as winners. 07 Why real-time payments are the new normal — and how payments providers can adapt As RTP schemes expand, providers will need to assess readiness and define a clear strategy for platforms, operations, risk and customer experience. Editorial 10 How the mPOS business model expands This newsletter comes to you as many of us prepare to meet again at beyond payments acceptance Sibos – the world’s premier financial services event, held this year in London, 23 to 26 September 2019. EY is a proud sponsor of Sibos, and commends As pure payments acceptance becomes a their efforts to bring together the global financial services and payments commodity for smaller merchants and fees from transaction processing come under community. pressure, mPOS providers are putting a This year’s theme is an exciting one that touches on many of the issues we strategic focus on value-added services to are covering in this #payments issue: “Thriving in a hyperconnected world” continue their high growth. -

Authorisation Service Sales Sheet Download

Authorisation Service OmniPay is First Data’s™ cost effective, Supported business profiles industry-leading payment processing platform. In addition to card present POS processing, the OmniPay platform Authorisation Service also supports these transaction The OmniPay platform Authorisation Service gives you types and products: 24/7 secure authorisation switching for both domestic and international merchants on behalf of merchant acquirers. • Card Present EMV offline PIN • Card Present EMV online PIN Card brand support • Card Not Present – MOTO The Authorisation Service supports a wide range of payment products including: • Dynamic Currency Conversion • Visa • eCommerce • Mastercard • Secure eCommerce –MasterCard SecureCode, Verified by Visa and SecurePlus • Maestro • Purchase with Cashback • Union Pay • SecureCode for telephone orders • JCB • MasterCard Gaming (Payment of winnings) • Diners Card International • Address Verification Service • Discover • Recurring and Installment • BCMC • Hotel Gratuity • Unattended Petrol • Aggregator • Maestro Advanced Registration Program (MARP) Supported authorisation message protocols • OmniPay ISO8583 • APACS 70 Authorisation Service Connectivity to the Card Schemes OmniPay Authorisation Server Resilience Visa – Each Data Centre has either two or four Visa EAS servers and resilient connectivity to Visa Europe, Visa US, Visa Canada, Visa CEMEA and Visa AP. Mastercard – Each Data Centre has a dedicated Mastercard MIP and resilient connectivity to the Mastercard MIP in the other Data Centre. The OmniPay platform has connections to Banknet for both European and non-European authorisations. Diners/Discover – Each Data Centre has connectivity to Diners Club International which is also used to process Discover Card authorisations. JCB – Each Data Centre has connectivity to Japan Credit Bureau which is used to process JCB authorisations. UnionPay – Each Data Centre has connectivity to UnionPay International which is used to process UnionPay authorisations. -

New Debit Card Solutions At

New Debit Card Solutions Debit Mastercard and Visa Debit are ready Swiss Banking Services Forum, 22 May 2019 Philippe Eschenmoser, Head Cards & A2A, Swisskey Ltd Maestro/V PAY Have Established Themselves As the “Key to the Account” – Schemes, However, Are Forcing Market Entry For Successor Products Response from the Maestro and V PAY are successful… …but are not future-capable products schemes # cards Maestro V PAY on Lower earnings potential millions8 for issuers as an alternative payment traffic products (e.g. 6 credit cards, TWINT) Issuer 4 V PAY will be 2 decommissioned by VISA Functional limitations: in 20211 – Visa Debit as 0 • No e-commerce the successor 2000 2018 • No preauthorizations Security and stability have End- • No virtualization proven themselves customer High acceptance in CH and Merchants with an online MasterCard is positioning abroad in Europe offer are demanding an DMC in the medium term online-capable debit as the successor to Standard product with an Merchan product Maestro integrated bank card t 2 1: As of 2021 no new V PAY may be issued TWINT (Still) No Substitute For Debit Cards – Credit Cards With Divergent Market Perception TWINT (still) not alternative for debit Credit cards a no alternative for debit Lacking a bank card Debit function Limited target group (age, ~1.1 M 1 ~10 M. creditworthiness...) Issuer ~48.5 k ~170 k1 No direct account debiting DMC/ Visa Debit Potentially high annual fee End-customer Lower customer penetration Banks and merchants DMC/ P2P demand an online- Higher costs Merchant Visa Debit -

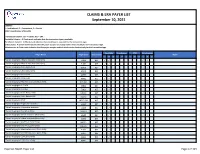

Claims and Remits Payer List

CLAIMS & ERA PAYER LIST September 10, 2021 LEGEND: I = Institutional, P = Professional, D = Dental COB = Coordination of Benefits Transaction Column: 837 = Claims, 835 = ERA Available Column: A Check-mark indicates that the transaction type is available. Enrollment Column: A Check-mark indicates that enrollment is required for the transaction type. COB Column: A Check-mark Indicates that the payer accepts secondary claims electronically for the transaction type. Attachments: A Check-mark indicates that the payer accepts medical attachments electronically for the transaction type. Available Enrollment COB Attachments Payer Name Payer Code Transaction Notes I P D I P D I P D I P D *Carisk Imaging to Allstate Insurance (Auto Only) E1069 837 ✓ ✓ ✓ ✓ *Carisk Imaging to Allstate Insurance (Auto Only) E1069 835 ✓ ✓ *Carisk Imaging to Geico (Auto Only) GEICO 837 ✓ ✓ ✓ ✓ *Carisk Imaging to Geico (Auto Only) GEICO 835 ✓ ✓ *Carisk Imaging to Nationwide A0002 837 ✓ ✓ ✓ ✓ *Carisk Imaging to Nationwide A0002 835 ✓ ✓ *Carisk Imaging to New York City Law Department NYCL001 837 ✓ ✓ ✓ ✓ *Carisk Imaging to NJ-PLIGA E3926 837 ✓ ✓ ✓ ✓ *Carisk Imaging to NJ-PLIGA E3926 835 ✓ ✓ *Carisk Imaging to North Dakota WSI NDWSI 837 ✓ ✓ ✓ ✓ *Carisk Imaging to North Dakota WSI NDWSI 835 ✓ ✓ *Carisk Imaging to NYSIF NYSIF1510 837 ✓ ✓ ✓ ✓ *Carisk Imaging to Progressive Insurance E1139 837 ✓ ✓ ✓ ✓ *Carisk Imaging to Progressive Insurance E1139 835 ✓ ✓ *Carisk Imaging to Pure (Auto Only) PURE01 837 ✓ ✓ ✓ ✓ *Carisk Imaging to Safeco Insurance (Auto Only) E0602 837 ✓ ✓ ✓ ✓ -

Interim Report-The Committee for Promoting Use of Advanced Means

Interim Report The Committee for Promoting November Use of Advanced Means of 2015 Payment in Israel Interim Report of the Committee for Promoting Use of Advanced Means of Payment in Israel Table of Contents 1. Introduction .................................................................................................................... 2 2. Executive summary ........................................................................................................ 3 3. Introduction .................................................................................................................... 6 4. Overview of advanced means of payment world-wide .................................................. 8 5. Overview of advanced means of payment in Israel ..................................................... 10 6. Advantages of using advanced means of payment ....................................................... 17 7. Alternatives for conducting transactions using advanced means of payment in the current payment systems .......................................................................................................... 19 8. Barriers to using advanced means of payment ............................................................. 23 9. Risk associated with use of advanced means of payment ............................................ 26 10. Legal aspects related to promoting use of advanced means of payment...................... 31 11. Summary and recommendations ................................................................................. -

Submission to the Reserve Bank of Australia Response to EFTPOS

Submission to the Reserve Bank of Australia Response To EFTPOS Industry Working Group By The Australian Retailers Association 13 September 2002 Response To EFTPOS Industry Working Group Prepared with the assistance of TransAction Resources Pty Ltd Australian Retailers Association 2 Response To EFTPOS Industry Working Group Contents 1. Executive Summary.........................................................................................................4 2. Introduction......................................................................................................................5 2.1 The Australian Retailers Association ......................................................................5 3. Objectives .......................................................................................................................5 4. Process & Scope.............................................................................................................6 4.1 EFTPOS Industry Working Group – Composition ...................................................6 4.2 Scope Of Discussion & Analysis.............................................................................8 4.3 Methodology & Review Timeframe.........................................................................9 5. The Differences Between Debit & Credit .......................................................................10 5.1 PIN Based Transactions.......................................................................................12 5.2 Cash Back............................................................................................................12 -

The Credit Card Industry in Israel

The credit card industry in Israel David Gilo, Faculty of Law, Tel-Aviv University Yossi Spiegel, Faculty of Management, Tel Aviv University, September 2005 2 Major Israeli banks and their credit card companies Banks and market shares in 2004 1998 – 2000 2000 – 2005 in terms of deposits by the public Bank Hapoalim - 29.8% Isracard (100% owned): Isracard (100% owned): • Isracard (100%) • Isracard (100%) • Mastercard (100%) • Mastercard (≈ 100%) • American Express (100%) • American Express (100%) • Visa (N/A) Bank Leumi - 25.6% CAL (65% owned): Leumi Card (100% owned): • Visa (84%) • Visa Leumi (≈ 50%) • Mastercard (N/A) Israel Discount Bank - 17.6% CAL (35% owned) CAL (51% owned): • Visa (≈ 50%) • Mastercard (N/A) Bank Hamizrachi - 10.7% First Int'l Bank - 8.5% Alpha Card (67% owned): CAL (20% owned) • Visa (16%) 3 Credit cards and market shares in acquisition (most of the data is from 2001) Credit card Cards Number of cards Market share in company (in millions) acquiring Isracard Isracard 1.1 47% Mastercard 0.3 American Express 0.15 Visa N/A Cal Visa Cal 1.1 31.8% Mastercard N/A Diners card 0.16 Leumi Card Visa Leumi 1.2 15.3% (2004) Mastercard N/A Others 5.9% Total active cards 3.8 (2004) Number of active cards grew at an annual rate of 9.1% since 1982 (from 0.55 million) 4 Main features of Israeli credit cards !"Deferred debit cards; virtually no credit cards and no debit cards !"Credit cards are also ATM cards and in effect are tied with bank accounts (Bank Leumi's clients were unilaterally transferred from CAL). -

DEBIT CARD POLICY 1. Debit Card a Debit Card Is a Plastic Card That

DEBIT CARD POLICY 1. Debit Card A debit card is a plastic card that provides the cardholder electronic access to his/her bank account(s). It is an instrument that can be used to: Avail of banking services such as cash withdrawal, balance enquiry etc., from any ATM and Micro ATM. Make payments to merchants against purchase, withdrawal of cash at POS or both within the prescribed limit by RBI at merchant outlets. e-Commerce transactions. 2. Understanding a Debit Card. a) Card Number: It is a 16 or 19 digit number linked to customer’s bank account. First 6 digits represent Bank’s identification no., next 4 digits represent Branch Sol ID. Remaining digits indicates serial number of the cards issued by that particular branch. Currently Bank issue debit cards with 16 digit length. b) Name of the Person: Person authorized to use the card. This field is present only on personalized card. c) Valid Date: It is in mm/yy format. The card is valid till the last day of the month. d) Card Verification Value (CVV) /CVV2: A 03 (Three) digit number printed on the back side of every debit card. This is used for validation of online transactions. e) Magnetic Strip: Important information regarding the debit card is stored in electronic format here and hence any kind of scratches or exposure to magnetic fields will cause damage to the card. f) EMV Chip Card: EMV stands for Europay, MasterCard and Visa. EMV is a global standard for credit and debit payment cards based on chip card technology. -

Multi-Lateral Mechanism of Cash Machines: Virtue Or Hassel

International Journal of Engineering Technology Science and Research IJETSR www.ijetsr.com ISSN 2394 – 3386 Volume 4, Issue 10 October 2017 Multi-Lateral Mechanism of Cash Machines: Virtue or Hassel Peeush Ranjan Agrawal1 and Sakshi Misra Shukla2 1 Professor, School of Management studies, MNNIT, Allahabad, Uttar Pradesh,India 2Assistant Professor, Department of MBA, S.P. Memorial Institute of Technology, Allahabad, India ABSTRACT Automated Teller Machines or Cash Machines became an organic constituent of the banking sector. The paper envisionsthe voyage that these cash machines have gone through since their initiation in the foreign banks operating in India. The study revolves around the indispensible factors in the foreign banking environment like availability, connectivity customer base, security, network gateways and clearing houses which were thoroughly reviewed and analyzed in the research paper. The methodology of the research paper includes literature review, derivation of variables, questionnaire formulation, pilot testing, data collectionand application of statistical tools with the help of SPSS software. The paper draws out findings related to the usage, congregation, multi-lateral functioning, security and growth of ATMs in the foreign banks operating in the country. The paper concludes by rendering recommendations to theforeign bankers to vanquish the stumbling blocks of the cash machines functioning. Keywords: ATMs, Cash Machines, Anywhere Banking, Foreign Banking, Online Banking 1. INTRODUCTION The Automated Teller Machine (ATM) has become an integral part of banking operations. Initially perceived as ‘cash machines’, which dispenses cash to depositors, ATMs can accept deposits, sell postage stamps, print statements and be used at institutions where the depositor does not have an account. -

Assessing Payments Systems in Latin America

Assessing payments systems in Latin America An Economist Intelligence Unit white paper sponsored by Visa International Assessing payments systems in Latin America Preface Assessing payments systems in Latin America is an Economist Intelligence Unit white paper, sponsored by Visa International. ● The Economist Intelligence Unit bears sole responsibility for the content of this report. The Economist Intelligence Unit’s editorial team gathered the data, conducted the interviews and wrote the report. The author of the report is Ken Waldie. The findings and views expressed in this report do not necessarily reflect the views of the sponsor. ● Our research drew on a wide range of published sources, both government and private sector. In addition, we conducted in-depth interviews with government officials and senior executives at a number of financial services companies in Latin America. Our thanks are due to all the interviewees for their time and insights. May 2005 © The Economist Intelligence Unit 2005 1 Assessing payments systems in Latin America Contents Executive summary 4 Brazil 17 The financial sector 17 Electronic payments systems 7 Governing institutions 17 Electronic payment products 7 Banks 17 Conventional payment cards 8 Clearinghouse systems 18 Smart cards 8 Electronic payment products 18 Stored value cards 9 Credit cards 18 Internet-based Payments 9 Debit cards 18 Payment systems infrastructure 9 Smart cards and pre-paid cards 19 Clearinghouse systems 9 Direct credits and debits 19 Card networks 10 Strengths and opportunities 19 -

The Credit Card Industry in Israel

Preliminary and incomplete The credit card industry in Israel David Gilo* and Yossi Spiegel** September 2005 Abstract: Since 1998, the Israeli credit card industry was transformed from a duopoly with two credit card companies which offer proprietary cards to a triopoly with two large open systems, Visa and Mastercard, which are issued and acquired by each of the three credit card companies. Regulatory intervention by the Israeli Antitrust Authority (IAA) played a key role in bringing about this structural change. In this paper we first review the Israeli credit card industry and then discuss in detail the regulatory intervention by the IAA. * The Buchmann Faculty of Law, Tel-Aviv University, Ramat Aviv, Tel Aviv, 69978, Israel, email: [email protected]. ** Faculty of Management, Tel Aviv University, Ramat Aviv, Tel Aviv, 69978, Israel. Email: [email protected], http://www.tau.ac.il/~spiegel Both authors were economic experts for Supersol (the largest supermarket chain in Israel) in the Israeli credit card case. 1 1. A brief history of the credit card industry in Israel Until 1998, there were two main players in the Israeli credit cards industry: Isracard, which was established in 1975 and is 100% owned by the largest bank in Israel, Bank Hapoalim, and CAL which was established in 1978 and was jointly owned at the time by the second largest bank in Israel, Bank Leumi (65%), and the third largest bank, Israel Discount Bank (35%). Isracard issued its own brand of credit card, called Isracard, for domestic use in Israel, and Mastercard and American express card for use in Israel and abroad, while CAL issued both Visa cards, under the brand name Visa CAL, and Diners Club cards. -

Application for a Maestro Card

CREDIT SUISSE (Switzerland) Ltd. Application for a Maestro Card Surname, First name / Company Date of birth This application refers to the following account no. IBAN (International Bank Account Number) (hereinafter referred to as the Client) 1. Application for a Maestro Card The Client hereby applies for a Maestro card from Credit Suisse (Switzerland) Ltd. (hereinafter referred to as the Bank). For him/herself, or For the following person (hereinafter referred to as the Authorized Cardholder): Mr. Ms. Surname First name Street/no. Postcode/town Domicile Date of birth Nationality Language of correspondence Card imprint 1st line 2nd line (automatic: cardholder; poss. manual entry of max. 24 characters) (poss. the account holder) The Authorized Cardholder is granted limited account The following services are available with the Maestro card: access rights for this card (Corporate Clients: not Cash withdrawals at ATMs in Switzerland and abroad possible for joint signatory authority). Cashless payment for goods and services in Switzerland Account access rights enable the Authorized Cardholder and abroad to: The Maestro card has a Maestro PIN (Personal query and print out account information at Credit Identification Number) for the use of ATMs and Maestro Suisse ATMs (current account balance, last five terminals at points of sale. transactions) make cash deposits at Credit Suisse ATMs equipped for that purpose. To be completed by the Bank Client no. (CIF) Client no. (CIF) Account holder ________________________________________ Authorized