OPERA V5 OPI Installation and Reference Guide Release 20.1 F26820-01 Copyright © 2010, 2020, Oracle And/Or Its Affiliates

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Authorisation Service Sales Sheet Download

Authorisation Service OmniPay is First Data’s™ cost effective, Supported business profiles industry-leading payment processing platform. In addition to card present POS processing, the OmniPay platform Authorisation Service also supports these transaction The OmniPay platform Authorisation Service gives you types and products: 24/7 secure authorisation switching for both domestic and international merchants on behalf of merchant acquirers. • Card Present EMV offline PIN • Card Present EMV online PIN Card brand support • Card Not Present – MOTO The Authorisation Service supports a wide range of payment products including: • Dynamic Currency Conversion • Visa • eCommerce • Mastercard • Secure eCommerce –MasterCard SecureCode, Verified by Visa and SecurePlus • Maestro • Purchase with Cashback • Union Pay • SecureCode for telephone orders • JCB • MasterCard Gaming (Payment of winnings) • Diners Card International • Address Verification Service • Discover • Recurring and Installment • BCMC • Hotel Gratuity • Unattended Petrol • Aggregator • Maestro Advanced Registration Program (MARP) Supported authorisation message protocols • OmniPay ISO8583 • APACS 70 Authorisation Service Connectivity to the Card Schemes OmniPay Authorisation Server Resilience Visa – Each Data Centre has either two or four Visa EAS servers and resilient connectivity to Visa Europe, Visa US, Visa Canada, Visa CEMEA and Visa AP. Mastercard – Each Data Centre has a dedicated Mastercard MIP and resilient connectivity to the Mastercard MIP in the other Data Centre. The OmniPay platform has connections to Banknet for both European and non-European authorisations. Diners/Discover – Each Data Centre has connectivity to Diners Club International which is also used to process Discover Card authorisations. JCB – Each Data Centre has connectivity to Japan Credit Bureau which is used to process JCB authorisations. UnionPay – Each Data Centre has connectivity to UnionPay International which is used to process UnionPay authorisations. -

Payments and Market Infrastructure Two Decades After the Start of the European Central Bank Editor: Daniela Russo

Payments and market infrastructure two decades after the start of the European Central Bank Editor: Daniela Russo July 2021 Contents Foreword 6 Acknowledgements 8 Introduction 9 Prepared by Daniela Russo Tommaso Padoa-Schioppa, a 21st century renaissance man 13 Prepared by Daniela Russo and Ignacio Terol Alberto Giovannini and the European Institutions 19 Prepared by John Berrigan, Mario Nava and Daniela Russo Global cooperation 22 Prepared by Daniela Russo and Takeshi Shirakami Part 1 The Eurosystem as operator: TARGET2, T2S and collateral management systems 31 Chapter 1 – TARGET 2 and the birth of the TARGET family 32 Prepared by Jochen Metzger Chapter 2 – TARGET 37 Prepared by Dieter Reichwein Chapter 3 – TARGET2 44 Prepared by Dieter Reichwein Chapter 4 – The Eurosystem collateral management 52 Prepared by Simone Maskens, Daniela Russo and Markus Mayers Chapter 5 – T2S: building the European securities market infrastructure 60 Prepared by Marc Bayle de Jessé Chapter 6 – The governance of TARGET2-Securities 63 Prepared by Cristina Mastropasqua and Flavia Perone Chapter 7 – Instant payments and TARGET Instant Payment Settlement (TIPS) 72 Prepared by Carlos Conesa Eurosystem-operated market infrastructure: key milestones 77 Part 2 The Eurosystem as a catalyst: retail payments 79 Chapter 1 – The Single Euro Payments Area (SEPA) revolution: how the vision turned into reality 80 Prepared by Gertrude Tumpel-Gugerell Contents 1 Chapter 2 – Legal and regulatory history of EU retail payments 87 Prepared by Maria Chiara Malaguti Chapter 3 – -

Fee Schedule Effective April 2, 2021 Service Federal Credit Union Corporate Offices Stateside Offices: P.O

Fee Schedule Effective April 2, 2021 Service Federal Credit Union Corporate Offices Stateside Offices: P.O. Box 1268, Portsmouth, NH 03802 | 800.936.7730 Overseas Offices: Unit 3019, APO AE 09021-3019 | 00800.4728.2000 This Fee Schedule sets forth the conditions, fees and charges applicable to your accounts listed below. This schedule is incorporated as part of your account agreement with Service Federal Credit Union. Checking Accounts Tiers are assigned on the first of each month based on the prior month’s activity and requirements are as follows. Basic: No Requirement. Direct Deposit: Direct Deposit of your Net Pay1 into your checking account each month. Direct Deposit+: DFAS Direct Deposit (Military, military retirees and select government workers who get paid by the Defense Finance and Accounting Service) OR Direct Deposit Tier Requirements and at least 5 payments2 per month. Everyday and Dividend Checking Tier Basic Direct Deposit Direct Deposit+ Savings Transfer Overdraft Protection $5 per transfer $5 per transfer FREE Stop Payment $30 $30 $30 Courtesy Pay Up to $1,000 limit $30 $30 $30 Return Items (NSF) $30 $30 $30 ATM Surcharge and Foreign Transaction Fee None Up to $15 monthly Up to $30 monthly Rebates Out of Network ATM Fee* None None None Cashier's Check $5 $5 No Charge Check Printing Fee Variable Variable 1 free basic box annually Loan Discount** No Discount 0.50% 0.75% Monthly Maintenance Fee Tier Basic Direct Deposit Direct Deposit+ Everyday Checking None None None Dividend Checking $10 $10 $10 (Fee waived with $1,500 min daily balance) Card Fees Miscellaneous Debit Card Replacement - Standard ......................................................................... -

New Debit Card Solutions At

New Debit Card Solutions Debit Mastercard and Visa Debit are ready Swiss Banking Services Forum, 22 May 2019 Philippe Eschenmoser, Head Cards & A2A, Swisskey Ltd Maestro/V PAY Have Established Themselves As the “Key to the Account” – Schemes, However, Are Forcing Market Entry For Successor Products Response from the Maestro and V PAY are successful… …but are not future-capable products schemes # cards Maestro V PAY on Lower earnings potential millions8 for issuers as an alternative payment traffic products (e.g. 6 credit cards, TWINT) Issuer 4 V PAY will be 2 decommissioned by VISA Functional limitations: in 20211 – Visa Debit as 0 • No e-commerce the successor 2000 2018 • No preauthorizations Security and stability have End- • No virtualization proven themselves customer High acceptance in CH and Merchants with an online MasterCard is positioning abroad in Europe offer are demanding an DMC in the medium term online-capable debit as the successor to Standard product with an Merchan product Maestro integrated bank card t 2 1: As of 2021 no new V PAY may be issued TWINT (Still) No Substitute For Debit Cards – Credit Cards With Divergent Market Perception TWINT (still) not alternative for debit Credit cards a no alternative for debit Lacking a bank card Debit function Limited target group (age, ~1.1 M 1 ~10 M. creditworthiness...) Issuer ~48.5 k ~170 k1 No direct account debiting DMC/ Visa Debit Potentially high annual fee End-customer Lower customer penetration Banks and merchants DMC/ P2P demand an online- Higher costs Merchant Visa Debit -

AUTOMATED TELLER MACHINE (Athl) NETWORK EVOLUTION in AMERICAN RETAIL BANKING: WHAT DRIVES IT?

AUTOMATED TELLER MACHINE (AThl) NETWORK EVOLUTION IN AMERICAN RETAIL BANKING: WHAT DRIVES IT? Robert J. Kauffiiian Leollard N.Stern School of Busivless New 'r'osk Universit,y Re\\. %sk, Net.\' York 10003 Mary Beth Tlieisen J,eorr;~rd n'. Stcr~iSchool of B~~sincss New \'orl; University New York, NY 10006 C'e~~terfor Rcseai.clt 011 Irlfor~i~ntion Systclns lnfoornlation Systen~sI)epar%ment 1,eojrarcl K.Stelm Sclrool of' Busir~ess New York ITuiversity Working Paper Series STERN IS-91-2 Center for Digital Economy Research Stem School of Business Working Paper IS-91-02 Center for Digital Economy Research Stem School of Business IVorking Paper IS-91-02 AUTOMATED TELLER MACHINE (ATM) NETWORK EVOLUTION IN AMERICAN RETAIL BANKING: WHAT DRIVES IT? ABSTRACT The organization of automated teller machine (ATM) and electronic banking services in the United States has undergone significant structural changes in the past two or three years that raise questions about the long term prospects for the retail banking industry, the nature of network competition, ATM service pricing, and what role ATMs will play in the development of an interstate banking system. In this paper we investigate ways that banks use ATM services and membership in ATM networks as strategic marketing tools. We also examine how the changes in the size, number, and ownership of ATM networks (from banks or groups of banks to independent operators) have impacted the structure of ATM deployment in the retail banking industry. Finally, we consider how movement toward market saturation is changing how the public values electronic banking services, and what this means for bankers. -

General Terms and Conditions for Bank Cards for Individuals and for Providing Payment Services by Card As an Electronic Payment Instrument

GENERAL TERMS AND CONDITIONS FOR BANK CARDS FOR INDIVIDUALS AND FOR PROVIDING PAYMENT SERVICES BY CARD AS AN ELECTRONIC PAYMENT INSTRUMENT Section I. DEFINITIONS 1. Pursuant to these General Terms and Conditions (GTC), the terms and abbreviations listed below shall have the following meaning: Bank card (Card) - A bank card (debit/credit) for individuals, hereinafter referred to as Card, is an electronic payment instrument through which UniCredit Bulbank AD (the BANK) entitles its customers within a fixed term to make payments up to the actual amount of their available own funds on a current account as well as up to an agreed credit limit (for credit cards only) authorized by the Bank. Main debit/credit card - A card issued to the Authorized Holder (the Account Holder of a current/card account). Additional debit/ credit card - A card issued at the request of the authorized main card holder (account holder) related to the same account of the account holder and subordinated to the main debit/ credit card. Authorized Holder of the Main Card – a local or foreign legally capable individual holding the account servicing the card who assumes obligations for the payment of fees and any debt arising from using the Card/s and with whom the Bank concludes a Debit Card Agreement/ Credit Card Agreement. An authorized holder of an additional card is the person specified by the authorized holder of the main card to whom the Bank issues additional debit/credit cards according to these General Terms and Conditions. The Account is a current account maintained in the name of the Authorized Holder of the Main Card. -

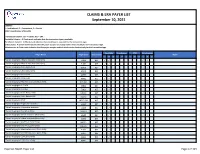

Claims and Remits Payer List

CLAIMS & ERA PAYER LIST September 10, 2021 LEGEND: I = Institutional, P = Professional, D = Dental COB = Coordination of Benefits Transaction Column: 837 = Claims, 835 = ERA Available Column: A Check-mark indicates that the transaction type is available. Enrollment Column: A Check-mark indicates that enrollment is required for the transaction type. COB Column: A Check-mark Indicates that the payer accepts secondary claims electronically for the transaction type. Attachments: A Check-mark indicates that the payer accepts medical attachments electronically for the transaction type. Available Enrollment COB Attachments Payer Name Payer Code Transaction Notes I P D I P D I P D I P D *Carisk Imaging to Allstate Insurance (Auto Only) E1069 837 ✓ ✓ ✓ ✓ *Carisk Imaging to Allstate Insurance (Auto Only) E1069 835 ✓ ✓ *Carisk Imaging to Geico (Auto Only) GEICO 837 ✓ ✓ ✓ ✓ *Carisk Imaging to Geico (Auto Only) GEICO 835 ✓ ✓ *Carisk Imaging to Nationwide A0002 837 ✓ ✓ ✓ ✓ *Carisk Imaging to Nationwide A0002 835 ✓ ✓ *Carisk Imaging to New York City Law Department NYCL001 837 ✓ ✓ ✓ ✓ *Carisk Imaging to NJ-PLIGA E3926 837 ✓ ✓ ✓ ✓ *Carisk Imaging to NJ-PLIGA E3926 835 ✓ ✓ *Carisk Imaging to North Dakota WSI NDWSI 837 ✓ ✓ ✓ ✓ *Carisk Imaging to North Dakota WSI NDWSI 835 ✓ ✓ *Carisk Imaging to NYSIF NYSIF1510 837 ✓ ✓ ✓ ✓ *Carisk Imaging to Progressive Insurance E1139 837 ✓ ✓ ✓ ✓ *Carisk Imaging to Progressive Insurance E1139 835 ✓ ✓ *Carisk Imaging to Pure (Auto Only) PURE01 837 ✓ ✓ ✓ ✓ *Carisk Imaging to Safeco Insurance (Auto Only) E0602 837 ✓ ✓ ✓ ✓ -

GBIC Approval Scheme

GBIC Approval Scheme Version 1.11 11.10.2018 GBIC Approval Scheme Content 1 Management Summary ................................................................................................... 8 2 Introduction .................................................................................................................... 11 2.1 Scope ................................................................................................................... 11 2.2 Objectives ............................................................................................................ 11 2.3 GBIC as Approval Authority .................................................................................. 12 2.4 Starting Points ...................................................................................................... 13 2.4.1 Development of the GBIC Approval Scheme ............................................. 13 2.4.2 Extension to Other Payment Schemes and Approval Bodies .................... 14 2.4.3 Necessity of a Common and Uniform Approval Scheme for Payment Schemes .................................................................................... 14 3 Approval Policy .............................................................................................................. 16 3.1 Overall Objectives ................................................................................................ 16 3.1.1 Compliance with Legal Requirements ....................................................... 16 3.1.2 Interoperability ......................................................................................... -

Moving Forward. Driving Results. Euronet Worldwide Annual Report 2004 Report Annual Worldwide Euronet

MOVING FORWARD. DRIVING RESULTS. EURONET WORLDWIDE ANNUAL REPORT 2004 REPORT ANNUAL WORLDWIDE EURONET EURONET WORLDWIDE ANNUAL REPORT 2004 The Transaction Highway At Euronet Worldwide, Inc. secure electronic financial transactions are the driving force of our business. Our mission is to bring electronic payment convenience to millions who have not had it before. Every day, our operations centers in six countries connect consumers, banks, retailers and mobile operators around the world, and we process millions of transactions a day over this transaction highway. We are the world's largest processor of prepaid transactions, supporting more than 175,000 point-of-sale (POS) terminals at small and major retailers around the world. We operate the largest pan-European automated teller machine (ATM) network across 14 countries and the largest shared ATM network in India. Our comprehensive software powers not only our own international processing centers, but it also supports more than 46 million transactions per month for integrated ATM, POS, telephone, Internet and mobile banking solutions for our customers in more than 60 countries. Glossary ATM – Automated Teller Machine EMEA - Europe, Middle East and Africa An unattended electronic machine in a public Euronet has an EMEA regional business unit in place that dispenses cash and bank account the EFT Processing Segment. information when a personal coded card is EPS - Earnings per Share used. A company's profit divided by each fully-diluted Contents EBITDA - Earnings before interest, taxes, share of common stock. depreciation and amortization 3...Letter to Our Shareholders E-top-up – Electronic top up EBITDA is the result of operating profit plus The ability to add airtime to a prepaid mobile 5...2004 Company Highlights depreciation and amortization. -

Submission to the Reserve Bank of Australia Response to EFTPOS

Submission to the Reserve Bank of Australia Response To EFTPOS Industry Working Group By The Australian Retailers Association 13 September 2002 Response To EFTPOS Industry Working Group Prepared with the assistance of TransAction Resources Pty Ltd Australian Retailers Association 2 Response To EFTPOS Industry Working Group Contents 1. Executive Summary.........................................................................................................4 2. Introduction......................................................................................................................5 2.1 The Australian Retailers Association ......................................................................5 3. Objectives .......................................................................................................................5 4. Process & Scope.............................................................................................................6 4.1 EFTPOS Industry Working Group – Composition ...................................................6 4.2 Scope Of Discussion & Analysis.............................................................................8 4.3 Methodology & Review Timeframe.........................................................................9 5. The Differences Between Debit & Credit .......................................................................10 5.1 PIN Based Transactions.......................................................................................12 5.2 Cash Back............................................................................................................12 -

In 20 Words High Performer, Inspired, Team Player, Achiever, University Education

CURRICULUM VITAE Eric de Putter 106 Pembury Road, Tonbridge, Kent TN9 2JG Mobile +44 7950 449188 [email protected] In 20 words High performer, inspired, team player, achiever, university education. 20 years experience in the banking industry, gained throughout UK/Ireland/Europe. Main skills Seeing the bigger picture & thinking outside the box Able to communicate effectively at all levels within an organisation and without Understand card business from all angles, strategic, business, IT and operational Multi-lingual (English, Dutch, basic German/French) Date of birth 13 November 1968 Marital status Married, four children Work experience: position at Payment Redesign, UK Current position: Managing partner & co-founder, Europe (January ’13 – present) Accountabilities Set-up the company as a boutique consultancy in the payment industry, associate partner selection and commercial strategy. Key achievements Discussing partnerships for POS services Consultancy assignment Work experience: position held at EVRY London, UK Current position: Director Business Development, Europe (June ’10 – December’12) Accountabilities Responsible for entry into Western Europe (shared with a fellow business development director), driving various ATM and POS bids and ensuring that export-selected products have a well-defined strategy. Manage a sales pipeline (started at zero) to € 100M+). Key achievements Doubled EVRY’s ATM footprint from 4 BAU markets to 8, gaining projects in the UK, Republic of Ireland, Netherlands and Belgium Broker a partnership with the card centre-of-excellence of a well-known European bank Develop and contribute to partnerships to complete the ATM value-chain, improving the sales channels and maturity of the European offering Eric de Putter Page 2 Work experience: positions held at VocaLink London, UK Last held position: Account Director/European card director (Sept ’08 – May ‘10) Accountabilities Responsible for European card strategy and immediate sales opportunities. -

The Transaction Network in Japan's Interbank Money Markets

The Transaction Network in Japan’s Interbank Money Markets Kei Imakubo and Yutaka Soejima Interbank payment and settlement flows have changed substantially in the last decade. This paper applies social network analysis to settlement data from the Bank of Japan Financial Network System (BOJ-NET) to examine the structure of transactions in the interbank money market. We find that interbank payment flows have changed from a star-shaped network with money brokers mediating at the hub to a decentralized network with nu- merous other channels. We note that this decentralized network includes a core network composed of several financial subsectors, in which these core nodes serve as hubs for nodes in the peripheral sub-networks. This structure connects all nodes in the network within two to three steps of links. The network has a variegated structure, with some clusters of in- stitutions on the periphery, and some institutions having strong links with the core and others having weak links. The structure of the network is a critical determinant of systemic risk, because the mechanism in which liquidity shocks are propagated to the entire interbank market, or like- wise absorbed in the process of propagation, depends greatly on network topology. Shock simulation examines the propagation process using the settlement data. Keywords: Interbank market; Real-time gross settlement; Network; Small world; Core and periphery; Systemic risk JEL Classification: E58, G14, G21, L14 Kei Imakubo: Financial Systems and Bank Examination Department, Bank of Japan (E-mail: [email protected]) Yutaka Soejima: Payment and Settlement Systems Department, Bank of Japan (E-mail: [email protected]) Empirical work in this paper was prepared for the 2006 Financial System Report (Bank of Japan [2006]), when the Bank of Japan (BOJ) ended the quantitative easing policy.