New Debit Card Solutions At

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Word Files Coverted

About MasterCard International: MasterCard International is a leading global payments solutions company that provides a broad variety of innovative services in support of their global members' credit, deposit access, electronic cash, business-to-business and related payment programs. MasterCard international manages a family of well-known, widely accepted payment cards brands including MasterCard®, Maestro®, and Cirrus® and serves financial institutions, consumers and businesses in over 210 countries and territories. What is a Debit Card: Maestro® is the Global Debit Card cum ATM Card product of MasterCard International. This card can be used to make on-line bill payments through 49,000 Point of Sale (POS) terminals in India and 70,00,000 merchant establishments worldwide exhibiting “MAESTRO” logo. In other words the Debit Card holder can pay their bills, at shops exhibiting “Maestro” Logo, using this card instead by cash or cheque. The card holder need not carry cash in future when all the shops provide this facility. SIB's Debit Card can also be used as an ATM card within the ATM network of the Bank. People around the world prefer debit card over credit card since the spending can be restricted to what they have in their account. Since payment is effected only if there is available balance in the customer's account, it is absolutely risk-free for the banks. SIB plans to issue debit cards liberally as an added convenience to its customers which in turn reduces the pressure on cash transactions at the counters. How is CIRRUS relevant to other bank's Maestro Card holders: SIB has acquired “CIRRUS”, the product of MasterCard International. -

Public Bank Unionpay Lifestyle Debit Card Product Disclosure Sheet

PRODUCT DISCLOSURE SHEET Public Bank Berhad (6463-H) Read this Product Disclosure Sheet before you PB Visa/MasterCard Lifestyle Debit – Generic decide to take up the PB Visa/MasterCard/Union Pay Lifestyle Debit. Be sure to also read the PB Visa/MasterCard Lifestyle Debit – Basic general terms and conditions. Savings Account/Basic Current Account PB UnionPay Lifestyle Debit – PB UnionPay Savings Account Date: 1. What is this product about? PB Visa/MasterCard/UnionPay Lifestyle Debit is a two-in-one card combining Visa/MasterCard/ UnionPay debit card and ATM functions. The card is linked to the Savings Account/Current Account/Basic Savings Account/Basic Current Account/PB UnionPay Savings Account (“Banking Account”) of the individual and any expenditure will be deducted directly from the Banking Account. This is a PB Visa/MasterCard/UnionPay Lifestyle Debit, a payment instrument which allows you to pay via a direct deduction of the cost for goods and services from your Banking Account at participating retail and service outlets. You are required to maintain a Banking Account with us, to be linked to your PB Visa/MasterCard/UnionPay Lifestyle Debit. If you close your Banking Account maintained with us, your PB Visa/MasterCard/UnionPay Lifestyle Debit will be automatically cancelled. 2. What are the fees and charges I have to pay? (i) Annual Fee x Generic/PB UnionPay Savings Account: RM8.00 x Basic Savings Account/Basic Current Account: Waived (subject to eight (8) ATM cash withdrawals and six (6) over-the-counter withdrawals per month*) *Note: Fee for exceeding the threshold will be RM1.00 per transaction. -

Authorisation Service Sales Sheet Download

Authorisation Service OmniPay is First Data’s™ cost effective, Supported business profiles industry-leading payment processing platform. In addition to card present POS processing, the OmniPay platform Authorisation Service also supports these transaction The OmniPay platform Authorisation Service gives you types and products: 24/7 secure authorisation switching for both domestic and international merchants on behalf of merchant acquirers. • Card Present EMV offline PIN • Card Present EMV online PIN Card brand support • Card Not Present – MOTO The Authorisation Service supports a wide range of payment products including: • Dynamic Currency Conversion • Visa • eCommerce • Mastercard • Secure eCommerce –MasterCard SecureCode, Verified by Visa and SecurePlus • Maestro • Purchase with Cashback • Union Pay • SecureCode for telephone orders • JCB • MasterCard Gaming (Payment of winnings) • Diners Card International • Address Verification Service • Discover • Recurring and Installment • BCMC • Hotel Gratuity • Unattended Petrol • Aggregator • Maestro Advanced Registration Program (MARP) Supported authorisation message protocols • OmniPay ISO8583 • APACS 70 Authorisation Service Connectivity to the Card Schemes OmniPay Authorisation Server Resilience Visa – Each Data Centre has either two or four Visa EAS servers and resilient connectivity to Visa Europe, Visa US, Visa Canada, Visa CEMEA and Visa AP. Mastercard – Each Data Centre has a dedicated Mastercard MIP and resilient connectivity to the Mastercard MIP in the other Data Centre. The OmniPay platform has connections to Banknet for both European and non-European authorisations. Diners/Discover – Each Data Centre has connectivity to Diners Club International which is also used to process Discover Card authorisations. JCB – Each Data Centre has connectivity to Japan Credit Bureau which is used to process JCB authorisations. UnionPay – Each Data Centre has connectivity to UnionPay International which is used to process UnionPay authorisations. -

(Automated Teller Machine) and Debit Cards Is Rising. ATM Cards Have A

Consumer Decision Making Contest 2001-2002 Study Guide ATM/Debit Cards The popularity of ATM (automated teller machine) and debit cards is rising. ATM cards have a longer history than debit cards, but the National Consumers League estimates that two-thirds of American households are likely to have debit cards by the end of 2000. It is expected that debit cards will rival cash and checks as a form of payment. In the future, “smart cards” with embedded computer chips may replace ATM, debit and credit cards. Single-purpose smart cards can be used for one purpose, like making a phone call, or riding mass transit. The smart card keeps track of how much value is left on your card. Other smart cards have multiple functions - serve as an ATM card, a debit card, a credit card and an electronic cash card. While this Study Guide will not discuss smart cards, they are on the horizon. Future consumers who understand how to select and use ATM and debit cards will know how to evaluate the features and costs of smart cards. ATM and Debit Cards and How They Work Electronic banking transactions are now a part of the American landscape. ATM cards and debit cards play a major role in these transactions. While ATM cards allow us to withdraw cash to meet our needs, debit cards allow us to by-pass the use of cash in point-of-sale (POS) purchases. Debit cards can also be used to withdraw cash from ATM machines. Both types of plastic cards are tied to a basic transaction account, either a checking account or a savings account. -

Fee Schedule Effective April 2, 2021 Service Federal Credit Union Corporate Offices Stateside Offices: P.O

Fee Schedule Effective April 2, 2021 Service Federal Credit Union Corporate Offices Stateside Offices: P.O. Box 1268, Portsmouth, NH 03802 | 800.936.7730 Overseas Offices: Unit 3019, APO AE 09021-3019 | 00800.4728.2000 This Fee Schedule sets forth the conditions, fees and charges applicable to your accounts listed below. This schedule is incorporated as part of your account agreement with Service Federal Credit Union. Checking Accounts Tiers are assigned on the first of each month based on the prior month’s activity and requirements are as follows. Basic: No Requirement. Direct Deposit: Direct Deposit of your Net Pay1 into your checking account each month. Direct Deposit+: DFAS Direct Deposit (Military, military retirees and select government workers who get paid by the Defense Finance and Accounting Service) OR Direct Deposit Tier Requirements and at least 5 payments2 per month. Everyday and Dividend Checking Tier Basic Direct Deposit Direct Deposit+ Savings Transfer Overdraft Protection $5 per transfer $5 per transfer FREE Stop Payment $30 $30 $30 Courtesy Pay Up to $1,000 limit $30 $30 $30 Return Items (NSF) $30 $30 $30 ATM Surcharge and Foreign Transaction Fee None Up to $15 monthly Up to $30 monthly Rebates Out of Network ATM Fee* None None None Cashier's Check $5 $5 No Charge Check Printing Fee Variable Variable 1 free basic box annually Loan Discount** No Discount 0.50% 0.75% Monthly Maintenance Fee Tier Basic Direct Deposit Direct Deposit+ Everyday Checking None None None Dividend Checking $10 $10 $10 (Fee waived with $1,500 min daily balance) Card Fees Miscellaneous Debit Card Replacement - Standard ......................................................................... -

ATM and Debit Card Safety Tips P1

ATM DEBIT CARD SAFETY TIPS Sensible Steps for: Personal Safety Account Security Identity Theft Protection ATM and Debit Card Safety and Security ith the banking convenience made possible with Automated Teller Machines WW (ATMs) and other Point of Sale terminals comes an increased need for security and personal caution. This includes protecting your ATM card number, Debit Card number, Personal Identication Number (PIN), and cash, and being aware of the condition of the machine and your surroundings. It’s no longer enough to take measures to protect your physical safety and your cash after a transaction at the ATM – now you must be aware of cameras and skimming devices that secretly record (steal) your bank account numbers and PIN numbers. Here are some other tips for safer transactions both Electronic and Personal: Electronic Safety Tips PROTECT YOUR CARD AND PIN Protect your ATM and debit cards as if they were cash. Report lost or stolen cards immediately. Don’t write your Personal Identication Number (PIN) on your card or give the number out to anyone, including friends and family, and do not reveal it to anyone over the phone. Avoid using numbers that are easily identied (birth date, phone number, etc.) with your personal identity. CONDUCT YOUR TRANSACTIONS PRIVATELY Use common courtesy at the ATM. Give people ahead of you space to conduct their transactions. When you use the ATM conduct your business quickly and eciently, make sure no one watches you key in your PIN number. Use your body and free hand to shield the ATM keypad during the transaction. -

CONSUMER DEBIT CARD ATM CARD Look for These Logos at ATM

CONSUMER DEBIT CARD ATM CARD Make purchases plus get cash fast at ATMs Get cash fast at ATMs Applicant Name: New Student _____________________________________________________________ Card Type: Sunset Eagle Your card and PIN will be sent to the address on your account statement. Please speak to an Account Representative for special mailing __________________________________ CHECKING ACCOUNT NUMBER accommodations. (Required for Debit Card __________________________________ Last 4 digits of Applicant’s Social Security Number: ___________________ SECONDARY CHECKING ACCOUNT NUMBER __________________________________ Daytime Phone: Evening or Message Phone: SAVINGS ACCOUNT NUMBER __________________________ __________________________ __________________________________ Reason for new card (lost, damage, etc.) I hereby request that I be issued a First Bank Consumer Debit card or a ATM card and Personal Identification Number for use at merchant locations, point-of-sale terminals (Consumer Debit Card only) and automated teller machines (ATMs) to access my account(s) at First Bank. I understand that I may use my card to access my savings account through an ATM only. I also acknowledge receipt of an Electronic Funds Transfer Disclosure and a Cardholder Agreement, and understand that use of my Consumer Debit Card or ATM card shall governed by the terms and conditions applicable to my account(s), to the terms of the Cardholder Agreement, by laws, rules, regulations or applicable law, and such terms, conditions, and/or amendments as may be established from time to time and communicated to me in writing. ________ As the parent/guardian on this account, I understand that I am responsible for the Please Initial transactions conducted by the minor owner. Applicant’s Signature Date If applicable, Parent Signature Date In order to expedite the processing of your application form, please remember: 1. -

General Terms and Conditions for Bank Cards for Individuals and for Providing Payment Services by Card As an Electronic Payment Instrument

GENERAL TERMS AND CONDITIONS FOR BANK CARDS FOR INDIVIDUALS AND FOR PROVIDING PAYMENT SERVICES BY CARD AS AN ELECTRONIC PAYMENT INSTRUMENT Section I. DEFINITIONS 1. Pursuant to these General Terms and Conditions (GTC), the terms and abbreviations listed below shall have the following meaning: Bank card (Card) - A bank card (debit/credit) for individuals, hereinafter referred to as Card, is an electronic payment instrument through which UniCredit Bulbank AD (the BANK) entitles its customers within a fixed term to make payments up to the actual amount of their available own funds on a current account as well as up to an agreed credit limit (for credit cards only) authorized by the Bank. Main debit/credit card - A card issued to the Authorized Holder (the Account Holder of a current/card account). Additional debit/ credit card - A card issued at the request of the authorized main card holder (account holder) related to the same account of the account holder and subordinated to the main debit/ credit card. Authorized Holder of the Main Card – a local or foreign legally capable individual holding the account servicing the card who assumes obligations for the payment of fees and any debt arising from using the Card/s and with whom the Bank concludes a Debit Card Agreement/ Credit Card Agreement. An authorized holder of an additional card is the person specified by the authorized holder of the main card to whom the Bank issues additional debit/credit cards according to these General Terms and Conditions. The Account is a current account maintained in the name of the Authorized Holder of the Main Card. -

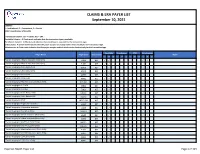

Claims and Remits Payer List

CLAIMS & ERA PAYER LIST September 10, 2021 LEGEND: I = Institutional, P = Professional, D = Dental COB = Coordination of Benefits Transaction Column: 837 = Claims, 835 = ERA Available Column: A Check-mark indicates that the transaction type is available. Enrollment Column: A Check-mark indicates that enrollment is required for the transaction type. COB Column: A Check-mark Indicates that the payer accepts secondary claims electronically for the transaction type. Attachments: A Check-mark indicates that the payer accepts medical attachments electronically for the transaction type. Available Enrollment COB Attachments Payer Name Payer Code Transaction Notes I P D I P D I P D I P D *Carisk Imaging to Allstate Insurance (Auto Only) E1069 837 ✓ ✓ ✓ ✓ *Carisk Imaging to Allstate Insurance (Auto Only) E1069 835 ✓ ✓ *Carisk Imaging to Geico (Auto Only) GEICO 837 ✓ ✓ ✓ ✓ *Carisk Imaging to Geico (Auto Only) GEICO 835 ✓ ✓ *Carisk Imaging to Nationwide A0002 837 ✓ ✓ ✓ ✓ *Carisk Imaging to Nationwide A0002 835 ✓ ✓ *Carisk Imaging to New York City Law Department NYCL001 837 ✓ ✓ ✓ ✓ *Carisk Imaging to NJ-PLIGA E3926 837 ✓ ✓ ✓ ✓ *Carisk Imaging to NJ-PLIGA E3926 835 ✓ ✓ *Carisk Imaging to North Dakota WSI NDWSI 837 ✓ ✓ ✓ ✓ *Carisk Imaging to North Dakota WSI NDWSI 835 ✓ ✓ *Carisk Imaging to NYSIF NYSIF1510 837 ✓ ✓ ✓ ✓ *Carisk Imaging to Progressive Insurance E1139 837 ✓ ✓ ✓ ✓ *Carisk Imaging to Progressive Insurance E1139 835 ✓ ✓ *Carisk Imaging to Pure (Auto Only) PURE01 837 ✓ ✓ ✓ ✓ *Carisk Imaging to Safeco Insurance (Auto Only) E0602 837 ✓ ✓ ✓ ✓ -

TD Generation Union Pay Guide

TD Generation UnionPay Guide For the TD Generation • All-in-One, HSPA, WiFi • Portal with PINpad • Portal 2 with PINpad COPYRIGHT © 2016 by The Toronto-Dominion Bank This publication is confidential and proprietary to The Toronto-Dominion Bank and is intended solely for the use of Merchant customers of TD Merchant Solutions. This publication may not be reproduced or distributed, in whole or in part, for any other purpose without the written permission of an authorized representative of The Toronto-Dominion Bank. NOTICE The Toronto-Dominion Bank reserves the right to make changes to specifications at any time and without notice. The Toronto-Dominion Bank assumes no responsibility for the use by the Merchant customers of the information furnished in this publication, including without limitation for infringements of intellectual property rights or other rights of third parties resulting from its use. Contents Who should use this guide? .....................................................1 What is UnionPay? .................................................................................. 1 How do I identify a UnionPay card? ....................................................... 1 UnionPay card types ............................................................................... 1 Financial Transactions ............................................................2 Transaction requirements ......................................................................2 PIN entry ............................................................................................................2 -

Credit Cards American Express Company 24-Hour Number: (800) 528-2121 (U.S

Credit Cards American Express Company 24-Hour Number: (800) 528-2121 (U.S. and Canada) American Express Cards include: Personal Green (pictured), Gold, Platinum, Corporate Green (pic - tured), Corporate Gold, Corporate Platinum, Corpo - rate Optima, Optima, Optima Gold, Purchasing Card, American Express Blue (pictured), Green and Gold Rewards, and more. American Express also issues co-branded cards, including Hilton, Delta SkyMiles (pictured), ITT Sheraton Club Miles, and more. American Express issues multiple styles of prepaid cards. Gift Cards (4 are pictured) can be variable load or pre-denominated ranging from $25 to $3,000. Gift Cards are not reloadable and can be personalized or issued anonymously. Reloadable prepaid cards are also available in various styles and offer different functionality. Serve and Bluebird prepaid cards are multifunction cards with many new features such as bill pay, check writing, and funds transfer. All prepaid cards have the word “PREPAID” printed on either the front or back of the card. Account numbers are 15 digits, begin with 37 or 34, and are sequenced 4-6-5. UV light reveals large “AMEX” and phosphorescence on the face of each card, excluding the Gift Card. The Centurion or the American Express Blue Box appears on most Amer - ican Express cards. To establish the validity of a card, or determine its status, please call (866) 375-3684. 98 Credit Cards Diners Club International ® 2500 Lake Cook Rd. Riverwoods, IL 60015 Security Contacts: Law Enforcement Phone Line: 1-800-347-3083 for law enforcement officers Merchant Code 10 Authorization: 1-800-347-1111 for suspicious transactions Diners Club ® account numbers start with 36 or 55. -

Virtual Debit Cards and Consumer Protection

Virtual debit cards and consumer protection RESEARCH REPORT Produced by Option consommateurs and presented to Industry Canada’s Officer of Consumer Affairs June 2014 Virtual debit cards and consumer protection Option consommateurs received funding for this report under Industry Canada’s Program for Non-Profit Consumer and Voluntary Organizations. The opinions expressed in the report are not necessarily those of Industry Canada or of the Government of Canada. Reproduction of limited excerpts of this report is permitted, provided the source is mentioned. Its reproduction or any reference to its content for advertising purposes or for profit, are strictly prohibited, however. Legal Deposit Bibliothèque nationale du Québec National Library of Canada ISBN: 978-2-89716-017-3 Option consommateurs Head Office 50, rue Ste-Catherine Ouest, Suite 440 Montréal (Québec) H2X 3V4 Tel.: 514 598-7288 Fax: 514 598-8511 Email: [email protected] Website: www.option-consumers.org Option consommateurs, 2014 ii Virtual debit cards and consumer protection Table of Contents Option consommateurs ................................................................................................................... iv Acknowledgements .......................................................................................................................... v Summary .......................................................................................................................................... vi 1. Introduction .................................................................................................................................7