Moving Forward. Driving Results. Euronet Worldwide Annual Report 2004 Report Annual Worldwide Euronet

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Xoom Rolls out Domestic Money Transfer Services in the U.S

Xoom Rolls Out Domestic Money Transfer Services in the U.S. November 12, 2019 PayPal's international money transfer service works with Walmart and Ria to offer cash pick-up in minutes at 4,700 Walmart and 175 Ria locations across the country SAN JOSE, Calif., Nov. 12, 2019 /PRNewswire/ -- Xoom, PayPal's international money transfer service, today rolled out the ability for customers to send money to recipients in the U.S. for the first time. Through strategic alliances with Walmart and Ria, Americans can now use Xoom to send money fast for cash pick-up typically in minutes at nearly 5,000 locations across the country*. Xoom's services potentially benefit more than 44 million foreign-born people in the U.S.1 who send remittances to family and friends in their home countries. With the introduction of domestic money transfer services, Xoom will now serve even more customers, including more than half of Americans who make domestic person-to-person (P2P) payments2. Using Xoom's mobile app or website, consumers will have the ability to send money quickly and securely for cash pick-up at any Walmart or Ria-owned store in the U.S. "Many of our customers in the U.S. already send money to loved ones in the country, and they usually prefer that the money is available right away," shared Julian King, Xoom's Vice President and General Manager. "This rollout reinforces our commitment to make money transfers fast, easy and affordable for everyone, whether they are at home or on-the-go." "At Ria, we are delighted to further consolidate our relationship with Xoom and Walmart," said Juan Bianchi, CEO of Euronet's Money Transfer Segment. -

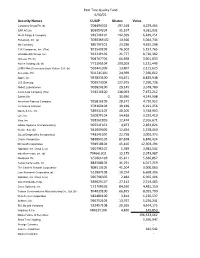

Pear Tree Quality Fund 6/30/21

Pear Tree Quality Fund 6/30/21 Security Names CUSIP Shares Value Compass Group Plc (b) '20449X302 197,348 4,229,464 SAP AG (b) '803054204 31,197 4,381,931 Wells Fargo & Company '949746101 142,399 6,449,251 Facebook, Inc. (a) '30303M102 14,566 5,064,744 3M Company '88579Y101 23,286 4,625,298 TJX Companies, Inc. (The) '872540109 76,502 5,157,765 UnitedHealth Group, Inc. '91324P102 21,777 8,720,382 Unilever Plc (b) '904767704 66,698 3,901,833 Roche Holding Ltd. (b) '771195104 109,203 5,131,449 LVMH Moët Hennessy-Louis Vuitton S.A. (b) '502441306 13,407 2,115,625 Accenture Plc 'G1151C101 24,969 7,360,612 Apple, Inc. '037833100 64,471 8,829,948 U.S. Bancorp '902973304 127,975 7,290,736 Abbott Laboratories '002824100 29,145 3,378,780 Coca-Cola Company (The) '191216100 138,093 7,472,212 Safran SA 0 30,650 4,249,998 American Express Company '025816109 28,572 4,720,952 Johnson & Johnson '478160104 38,189 6,291,256 Merck & Co., Inc. '589331107 48,205 3,748,903 Lyft, Inc. '55087P104 54,438 3,292,410 Visa, Inc. '92826C839 12,474 2,916,671 Adobe Systems Incorporated (a) '00724F101 4,873 2,853,824 Nestle, S.A. (b) '641069406 12,654 1,578,460 Quest Diagnostics Incorporated '74834L100 22,758 3,003,373 Oracle Corporation '68389X105 87,878 6,840,424 Microsoft Corporation '594918104 45,416 12,303,194 Alphabet, Inc. Class C (a) '02079K107 1,589 3,982,542 salesforce.com, inc. -

VX690 User Manual

Sivu 1(36) 28.9.2016 VX690 User Manual English Author: Verifone Finland Oy Date: 28.9.2016 Pages: 20 Sivu 2(36) 28.9.2016 INDEX: 1. BEFORE USE ............................................................................................................................... 5 1.1 Important ......................................................................................................................................... 5 1.2 Terminal Structure ......................................................................................................................... 6 1.3 Terminal start-up and shutdown .................................................................................................. 6 1.4 Technical data ................................................................................................................................ 7 1.5 Connecting cables ......................................................................................................................... 7 1.6 SIM-card.......................................................................................................................................... 8 1.7 Touchscreen ................................................................................................................................... 8 1.8 Using the menus ............................................................................................................................ 9 1.9 Letters and special characters.................................................................................................... -

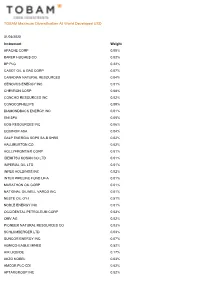

TOBAM Maximum Diversification All World Developed USD

TOBAM Maximum Diversification All World Developed USD 31/03/2020 Instrument Weight APACHE CORP 0.00% BAKER HUGHES CO 0.02% BP PLC 0.22% CABOT OIL & GAS CORP 0.07% CANADIAN NATURAL RESOURCES 0.04% CENOVUS ENERGY INC 0.01% CHEVRON CORP 0.08% CONCHO RESOURCES INC 0.02% CONOCOPHILLIPS 0.09% DIAMONDBACK ENERGY INC 0.01% ENI SPA 0.05% EOG RESOURCES INC 0.06% EQUINOR ASA 0.04% GALP ENERGIA SGPS SA-B SHRS 0.02% HALLIBURTON CO 0.02% HOLLYFRONTIER CORP 0.01% IDEMITSU KOSAN CO LTD 0.01% IMPERIAL OIL LTD 0.01% INPEX HOLDINGS INC 0.02% INTER PIPELINE FUND LP-A 0.01% MARATHON OIL CORP 0.01% NATIONAL OILWELL VARCO INC 0.01% NESTE OIL OYJ 0.51% NOBLE ENERGY INC 0.01% OCCIDENTAL PETROLEUM CORP 0.03% OMV AG 0.02% PIONEER NATURAL RESOURCES CO 0.03% SCHLUMBERGER LTD 0.03% SUNCOR ENERGY INC 0.07% AGNICO-EAGLE MINES 0.52% AIR LIQUIDE 0.17% AKZO NOBEL 0.03% AMCOR PLC-CDI 0.02% APTARGROUP INC 0.02% TOBAM Maximum Diversification All World Developed USD 31/03/2020 Instrument Weight AVON RESOURCES LTD 0.20% BALL CORP 0.06% CCL INDUSTRIES INC - CL B 0.01% CHR HANSEN HOLDING A/S 0.05% CLARIANT AG-REG 0.01% CORTEVA INC 0.04% CRODA INTERNATIONAL PLC 0.02% EMS-CHEMIE HOLDING AG-REG 0.01% FIRST QUANTUM MINERALS LTD 0.01% FORTESCUE METALS GROUP LTD 0.04% FRANCO-NEVADA CORP 1.01% GIVAUDAN-REG 0.07% INTL FLAVORS & FRAGRANCES 0.04% JAMES HARDIE INDUSTRIES-CDI 0.01% KANSAI PAINT CO LTD 0.01% KIRKLAND LAKE GOLD LTD 0.31% LINDE PLC 0.03% MARTIN MARIETTA MATERIALS 0.03% MOSAIC CO/THE 0.01% NEWCREST MINING LTD 0.60% NEWMONT CORP 1.89% NIPPON PAINT CO LTD 0.03% NORTHERN STAR RESOURCES -

Payments and Market Infrastructure Two Decades After the Start of the European Central Bank Editor: Daniela Russo

Payments and market infrastructure two decades after the start of the European Central Bank Editor: Daniela Russo July 2021 Contents Foreword 6 Acknowledgements 8 Introduction 9 Prepared by Daniela Russo Tommaso Padoa-Schioppa, a 21st century renaissance man 13 Prepared by Daniela Russo and Ignacio Terol Alberto Giovannini and the European Institutions 19 Prepared by John Berrigan, Mario Nava and Daniela Russo Global cooperation 22 Prepared by Daniela Russo and Takeshi Shirakami Part 1 The Eurosystem as operator: TARGET2, T2S and collateral management systems 31 Chapter 1 – TARGET 2 and the birth of the TARGET family 32 Prepared by Jochen Metzger Chapter 2 – TARGET 37 Prepared by Dieter Reichwein Chapter 3 – TARGET2 44 Prepared by Dieter Reichwein Chapter 4 – The Eurosystem collateral management 52 Prepared by Simone Maskens, Daniela Russo and Markus Mayers Chapter 5 – T2S: building the European securities market infrastructure 60 Prepared by Marc Bayle de Jessé Chapter 6 – The governance of TARGET2-Securities 63 Prepared by Cristina Mastropasqua and Flavia Perone Chapter 7 – Instant payments and TARGET Instant Payment Settlement (TIPS) 72 Prepared by Carlos Conesa Eurosystem-operated market infrastructure: key milestones 77 Part 2 The Eurosystem as a catalyst: retail payments 79 Chapter 1 – The Single Euro Payments Area (SEPA) revolution: how the vision turned into reality 80 Prepared by Gertrude Tumpel-Gugerell Contents 1 Chapter 2 – Legal and regulatory history of EU retail payments 87 Prepared by Maria Chiara Malaguti Chapter 3 – -

Online User Guide

Online User Guide Terms and conditions and fees apply to the use of your card. Minimum and maximum transfer amounts may apply. Refer to the PDS. Gobsmacked Loyalty Pty Ltd ABN 60 098 218 216 (AFSL 444609) is the issuer of the card. The PDS is available on the above link. You should consider the PDS in deciding whether or not to acquire or keep the card. Moorebank Sports Club Limited is responsible for the Infinity Plus Rewards program and promotions and the conversion of reward points to monetary value. Refer to the Moorebank Sports Club Limited reward promotions and program terms and conditions. Infinity Plus Prepaid eftpos Card So you’ve got your new Moorebank Sports Club Infinity Plus Prepaid eftpos Card. Now what do you do? This User Guide will explain how to start using your Infinity Plus Card for everyday purchases. If you have any enquiries at all whilst you are a Infinity Plus cardholder please visit Moorebank Sports Club and we will help you. Please refer to the Product Disclosure Statement (PDS) for the terms and conditions governing the use of the Infinity Plus Card. A copy of the PDS is also available online at www.moorebanksports.com.au Table of Contents WHAT IS THE INFINITY PLUS PREPAID eftpos CARD? GETTING STARTED Activate my Infinity Plus Card At the Club At home USING MY INFINITY PLUS CARD Card Loads How do I transfer my rewards onto my Infinity Plus Card? How do I load my card with extra funds so I can spend more? Making Purchases Where can I use my Infinity Plus Card? INFINITY PLUS CARDHOLDER ACCOUNT PAGE Features PIN -

AUTOMATED TELLER MACHINE (Athl) NETWORK EVOLUTION in AMERICAN RETAIL BANKING: WHAT DRIVES IT?

AUTOMATED TELLER MACHINE (AThl) NETWORK EVOLUTION IN AMERICAN RETAIL BANKING: WHAT DRIVES IT? Robert J. Kauffiiian Leollard N.Stern School of Busivless New 'r'osk Universit,y Re\\. %sk, Net.\' York 10003 Mary Beth Tlieisen J,eorr;~rd n'. Stcr~iSchool of B~~sincss New \'orl; University New York, NY 10006 C'e~~terfor Rcseai.clt 011 Irlfor~i~ntion Systclns lnfoornlation Systen~sI)epar%ment 1,eojrarcl K.Stelm Sclrool of' Busir~ess New York ITuiversity Working Paper Series STERN IS-91-2 Center for Digital Economy Research Stem School of Business Working Paper IS-91-02 Center for Digital Economy Research Stem School of Business IVorking Paper IS-91-02 AUTOMATED TELLER MACHINE (ATM) NETWORK EVOLUTION IN AMERICAN RETAIL BANKING: WHAT DRIVES IT? ABSTRACT The organization of automated teller machine (ATM) and electronic banking services in the United States has undergone significant structural changes in the past two or three years that raise questions about the long term prospects for the retail banking industry, the nature of network competition, ATM service pricing, and what role ATMs will play in the development of an interstate banking system. In this paper we investigate ways that banks use ATM services and membership in ATM networks as strategic marketing tools. We also examine how the changes in the size, number, and ownership of ATM networks (from banks or groups of banks to independent operators) have impacted the structure of ATM deployment in the retail banking industry. Finally, we consider how movement toward market saturation is changing how the public values electronic banking services, and what this means for bankers. -

GBIC Approval Scheme

GBIC Approval Scheme Version 1.11 11.10.2018 GBIC Approval Scheme Content 1 Management Summary ................................................................................................... 8 2 Introduction .................................................................................................................... 11 2.1 Scope ................................................................................................................... 11 2.2 Objectives ............................................................................................................ 11 2.3 GBIC as Approval Authority .................................................................................. 12 2.4 Starting Points ...................................................................................................... 13 2.4.1 Development of the GBIC Approval Scheme ............................................. 13 2.4.2 Extension to Other Payment Schemes and Approval Bodies .................... 14 2.4.3 Necessity of a Common and Uniform Approval Scheme for Payment Schemes .................................................................................... 14 3 Approval Policy .............................................................................................................. 16 3.1 Overall Objectives ................................................................................................ 16 3.1.1 Compliance with Legal Requirements ....................................................... 16 3.1.2 Interoperability ......................................................................................... -

Unionpay: Visa and Mastercard's Tough Chinese Rival

1.35% AXP American Express Co $66.0 USD 0.87 1.32% Market data is delayed at least 15 minutes. Company Lookup Ticker Symbol or Company Go Among the myriad designer brands at the Harrods flagship store in London, Chinese housewife Li Yafang spotted a corporate logo she knows from back home: the red, blue, and green of UnionPay cards. “It’s very convenient,” said Li, 39, as a salesperson rang up a £1,190 ($1,920) Prada Saffiano Lux handbag. With 2.9 billion cards in circulation—equal to 45 percent of the world’s total last year—UnionPay has grown into a payments processing colossus just 10 years after the company was founded. Now accepted in 135 countries, its share of global credit- and debit-card transaction volume for the first half of 2012 rose to 23.8 percent, propelling it to No. 2 behind Visa International (V), according to the Nilson Report, an industry newsletter. “UnionPay has absolute dominance in China, and it’s now expanding beyond that to become a top global player,” says James Friedman, an analyst at Susquehanna International Group. “Their numbers show they are already in the league of Visa and MasterCard (MA).” Yin Lian, UnionPay’s name in Mandarin, means “banks united,” which reflects its ownership structure. Its founding shareholders were 85 Chinese banks, led by the five biggest state-owned lenders. UnionPay’s top managers are former senior officials at the People’s Bank of China, the nation’s central bank. (The company would not make executives available for interviews.) At home, the Shanghai-based firm enjoys a big competitive edge: The government requires that all automated teller machines and Chinese merchants use UnionPay’s electronic payments network to process payments in the local currency. -

Frequently Asked Questions

FREQUENTLY ASKED QUESTIONS SM How do I activate my Insight Visa® How do I use my Insight Card to pay We recommend that you consider paying inside Prepaid Card? bills? with the attendant for the exact amount and Call 1.888.572.8472 to activate your Insight Card Insight Online Bill Pay is a fast, easy, and signing the receipt instead. and set your PIN. secure way to make payments online. Use it at no charge to pay your rent, utilities, and other Is my Insight Card safe to use on the Where can I use my Insight Card? monthly bills. Internet? Your Insight Card can be used everywhere Visa • Pay virtually anyone online Yes, the purchases you make online using Debit cards are accepted to make purchases • Schedule single, recurring, or future-dated your Insight Card are as safe as any other Visa in-store, online, or by phone. Use your Card to payments Prepaid Card. withdraw cash and check your balance at any • Make changes to scheduled payments ATM worldwide displaying the Visa®, Plus® or before they are sent What should I do if my Card is lost or Maestro® logo. • Track your payment status and history stolen? If you believe that your Insight Card has How much money can I load on my What happens to my direct deposit if been lost or stolen, call us immediately at Card? I change jobs? 1.888.572.8472. You will have the option of The maximum amount of cash loads is $5,000 If you change jobs, the deposits from your obtaining a replacement card and your available per day. -

ANNUAL REPORT June 30, 2021

JOB TITLE SA FUNDS AR REVISION 8 SERIAL <12345678> TIME Friday, August 27, 2021 JOB NUMBER 393837-1 TYPE PAGE NO. I ANNUAL REPORT June 30, 2021 PORTFOLIOS OF INVESTMENTS SA U.S. Fixed Income Fund SA Global Fixed Income Fund SA U.S. Core Market Fund SA U.S. Value Fund SA U.S. Small Company Fund SA International Value Fund SA International Small Company Fund SA Emerging Markets Value Fund SA Real Estate Securities Fund SA Worldwide Moderate Growth Fund Beginning on January 1, 2022, as permitted by regulations adopted by the Securities and Exchange Commission, we intend to no longer mail paper copies of each Fund’s shareholder reports, unless you specifically request paper copies of the reports from the SA Funds - Investment Trust (the “Trust”) or from your financial intermediary, such as a broker-dealer or bank. Instead, the reports will be made available on the Trust’s website (http://www.sa-funds.com), and you will be notified by mail each time a report is posted and provided with a website link to access the report. If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to continue to receive paper copies of all future reports free of charge. If you invest through a financial intermediary, you may contact your financial intermediary to request that you continue to receive paper copies of your shareholder reports. If you invest directly with the Trust, you may inform the Trust that you wish to continue receiving paper copies of your shareholder reports by contacting us at (844) 366-0905. -

Transaction Fees in Banking Machine Networks: a Spatial and Empirical Analysis

TRANSACTION FEES IN BANKING MACHINE NETWORKS: A SPATIAL AND EMPIRICAL ANALYSIS by ELIZABETH W. CROFT A THESIS SUBMITTED IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE DEGREE OF DOCTOR OF PHILOSOPHY in THE FACULTY OF GRADUATE STUDIES Department of Commerce and Business Administration, Policy Programme We accept this thesis as conforming to the required standard. THE UNIVERSITY OF BRITISH COLUMBIA April 1999 © Elizabeth W. Croft, 1999 In presenting this thesis in partial fulfilment of the requirements for an advanced degree at the University of British Columbia, I agree that the Library shall make it freely available for reference and study. I further agree that permission for extensive copying of this thesis for scholarly purposes may be granted by the head of my department or by his or her representatives. It is understood that copying or publication of this thesis for financial gain shall not be allowed without my written permission. Department of Co^ rvxACQL -* r__>QXj (j[ JUv^k The University of British Columbia Vancouver, Canada Date AfC\ > ZofW DE-6 (2/88) ABSTRACT This thesis concerns the effects of network member features on the pricing of automated teller machine (ATM) transactions. The first chapter outlines the development of ATM networks and provides an institutional and public policy backdrop for the theoretical and empirical analysis in the thesis. ATM fees have recently received increased attention in North America due to the Interac abuse of dominance case in Canada and the widespread introduction of surcharge fees at ATMs in the United States. In Chapter 2, a new circular spatial model of ATM networks is developed and used to analyze the pricing preferences of banks when choosing to link their proprietary ATM networks into a shared network.