Case M.8149 – Mastercard/ Vocalink REGULATION (EC)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Vocalink and BGC Application Failover

VocaLink and BGC Application Failover Martin McGeough Database Technical Architect VocaLink: at the heart of the transaction A specialist provider of payment transaction services Our history Driving automated payments for more than 40 years From domestic supplier to large-scale international provider of modern payment services Our scale We securely process over 9 billion payments a year, including 15% of all European bank-to-bank payments On a peak day the payment platform processes over 90 million transactions and its switching technology powers the world's busiest network of over 60,000 ATMs Our customers The world’s top banks, their corporate customers and Government departments Sterling Cards and Our services Real-Time Euro clearing Connectivity ATM Payments Services services services 2009 awards Best payment system deployment (Faster Payments Service) Best outsourcing partnership (BGC) Overall winner (Faster Payments Service) 3 VocaLink’s history with Oracle • In 2007 VocaLink initiated a joint programme with BGC – the Swedish clearing house - to renew the BGC Service – the goal was to replace the heritage mainframe technology with a highly scalable, highly available and modular infrastructure that would reduce costs while simultaneously improving performance. • Main Architecture requirements − High Availability – No single points of failure − Disaster Recovery – remote site with zero data loss − Site Failover – Site failover SLA is 15 minutes − High Throughput – Process payments within very tight SLA’s − Manageability – Ability to manage independent payments services 4 VocaLink’s history with Oracle contd. • Technology − WebLogic Server was chosen to provide the Application Server software − Sun/Oracle was chosen to provide the hardware. − Oracle Database was chosen to provide the Database software using RAC (Real Application Cluster) for a solution that provided high availability and performance and Data Guard + Data Guard Broker provided an easily managed DR solution. -

Authorisation Service Sales Sheet Download

Authorisation Service OmniPay is First Data’s™ cost effective, Supported business profiles industry-leading payment processing platform. In addition to card present POS processing, the OmniPay platform Authorisation Service also supports these transaction The OmniPay platform Authorisation Service gives you types and products: 24/7 secure authorisation switching for both domestic and international merchants on behalf of merchant acquirers. • Card Present EMV offline PIN • Card Present EMV online PIN Card brand support • Card Not Present – MOTO The Authorisation Service supports a wide range of payment products including: • Dynamic Currency Conversion • Visa • eCommerce • Mastercard • Secure eCommerce –MasterCard SecureCode, Verified by Visa and SecurePlus • Maestro • Purchase with Cashback • Union Pay • SecureCode for telephone orders • JCB • MasterCard Gaming (Payment of winnings) • Diners Card International • Address Verification Service • Discover • Recurring and Installment • BCMC • Hotel Gratuity • Unattended Petrol • Aggregator • Maestro Advanced Registration Program (MARP) Supported authorisation message protocols • OmniPay ISO8583 • APACS 70 Authorisation Service Connectivity to the Card Schemes OmniPay Authorisation Server Resilience Visa – Each Data Centre has either two or four Visa EAS servers and resilient connectivity to Visa Europe, Visa US, Visa Canada, Visa CEMEA and Visa AP. Mastercard – Each Data Centre has a dedicated Mastercard MIP and resilient connectivity to the Mastercard MIP in the other Data Centre. The OmniPay platform has connections to Banknet for both European and non-European authorisations. Diners/Discover – Each Data Centre has connectivity to Diners Club International which is also used to process Discover Card authorisations. JCB – Each Data Centre has connectivity to Japan Credit Bureau which is used to process JCB authorisations. UnionPay – Each Data Centre has connectivity to UnionPay International which is used to process UnionPay authorisations. -

Mastercard Announces Acquisition of Vocalink Enhancing Choice, Driving Innovation Across All Payment Types and Payment Flows

MasterCard Announces Acquisition of VocaLink Enhancing Choice, Driving Innovation Across All Payment Types and Payment Flows PURCHASE, N.Y. – July 21, 2016 – MasterCard Incorporated (NYSE: MA) today announced that it has entered into a definitive agreement to acquire 92.4 percent of VocaLink Holdings Limited for about £700 million (approximately US$920 million), after adjusting for cash and certain other estimated liabilities. VocaLink’s existing shareholders have the potential for an earn-out of up to an additional £169 million (approximately US$220 million), if performance targets are met. This transaction is subject to regulatory approval and other customary closing conditions. Under the agreement, a majority of VocaLink’s shareholders will retain 7.6 percent ownership for at least three years. Based in London, VocaLink operates key payments technology platforms on behalf of UK payment schemes, including: BACS – the Automated Clearing House (ACH) enabling direct credit and direct debit payments between bank accounts Faster Payments – the real-time account-to-account service enabling payments via mobile, internet and telephone LINK – the UK ATM network In addition, VocaLink offers innovative products with global potential, including ZAPP, a mobile payments app that leverages Fast ACH technology, and licenses its software and provides services to support ACH activities in Sweden, Singapore, Thailand and the United States. In 2015, the company reported revenues of £182 million as it processed more than 11 billion transactions. This acquisition accelerates MasterCard’s efforts to be an active participant in all types of electronic payments and payment flows and to enhance its services for the benefit of customers and partners. -

New Debit Card Solutions At

New Debit Card Solutions Debit Mastercard and Visa Debit are ready Swiss Banking Services Forum, 22 May 2019 Philippe Eschenmoser, Head Cards & A2A, Swisskey Ltd Maestro/V PAY Have Established Themselves As the “Key to the Account” – Schemes, However, Are Forcing Market Entry For Successor Products Response from the Maestro and V PAY are successful… …but are not future-capable products schemes # cards Maestro V PAY on Lower earnings potential millions8 for issuers as an alternative payment traffic products (e.g. 6 credit cards, TWINT) Issuer 4 V PAY will be 2 decommissioned by VISA Functional limitations: in 20211 – Visa Debit as 0 • No e-commerce the successor 2000 2018 • No preauthorizations Security and stability have End- • No virtualization proven themselves customer High acceptance in CH and Merchants with an online MasterCard is positioning abroad in Europe offer are demanding an DMC in the medium term online-capable debit as the successor to Standard product with an Merchan product Maestro integrated bank card t 2 1: As of 2021 no new V PAY may be issued TWINT (Still) No Substitute For Debit Cards – Credit Cards With Divergent Market Perception TWINT (still) not alternative for debit Credit cards a no alternative for debit Lacking a bank card Debit function Limited target group (age, ~1.1 M 1 ~10 M. creditworthiness...) Issuer ~48.5 k ~170 k1 No direct account debiting DMC/ Visa Debit Potentially high annual fee End-customer Lower customer penetration Banks and merchants DMC/ P2P demand an online- Higher costs Merchant Visa Debit -

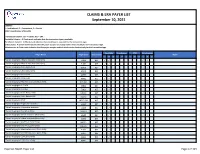

Claims and Remits Payer List

CLAIMS & ERA PAYER LIST September 10, 2021 LEGEND: I = Institutional, P = Professional, D = Dental COB = Coordination of Benefits Transaction Column: 837 = Claims, 835 = ERA Available Column: A Check-mark indicates that the transaction type is available. Enrollment Column: A Check-mark indicates that enrollment is required for the transaction type. COB Column: A Check-mark Indicates that the payer accepts secondary claims electronically for the transaction type. Attachments: A Check-mark indicates that the payer accepts medical attachments electronically for the transaction type. Available Enrollment COB Attachments Payer Name Payer Code Transaction Notes I P D I P D I P D I P D *Carisk Imaging to Allstate Insurance (Auto Only) E1069 837 ✓ ✓ ✓ ✓ *Carisk Imaging to Allstate Insurance (Auto Only) E1069 835 ✓ ✓ *Carisk Imaging to Geico (Auto Only) GEICO 837 ✓ ✓ ✓ ✓ *Carisk Imaging to Geico (Auto Only) GEICO 835 ✓ ✓ *Carisk Imaging to Nationwide A0002 837 ✓ ✓ ✓ ✓ *Carisk Imaging to Nationwide A0002 835 ✓ ✓ *Carisk Imaging to New York City Law Department NYCL001 837 ✓ ✓ ✓ ✓ *Carisk Imaging to NJ-PLIGA E3926 837 ✓ ✓ ✓ ✓ *Carisk Imaging to NJ-PLIGA E3926 835 ✓ ✓ *Carisk Imaging to North Dakota WSI NDWSI 837 ✓ ✓ ✓ ✓ *Carisk Imaging to North Dakota WSI NDWSI 835 ✓ ✓ *Carisk Imaging to NYSIF NYSIF1510 837 ✓ ✓ ✓ ✓ *Carisk Imaging to Progressive Insurance E1139 837 ✓ ✓ ✓ ✓ *Carisk Imaging to Progressive Insurance E1139 835 ✓ ✓ *Carisk Imaging to Pure (Auto Only) PURE01 837 ✓ ✓ ✓ ✓ *Carisk Imaging to Safeco Insurance (Auto Only) E0602 837 ✓ ✓ ✓ ✓ -

Delivery and Regulation of the New Payments Architecture LINK’S Response to the Payment Systems Regulator’S Consultation Paper, February 2021

Delivery and Regulation of the New Payments Architecture LINK’s response to the Payment Systems Regulator’s consultation paper, February 2021 8th March 2021 Contact: John Howells, LINK CEO e-mail: [email protected] Mobile: 07974 326 390 Web: www.link.co.uk Classification: “Public” and available at www.link.co.uk LINK’s Experience of Competitive Infrastructure Tenders 1. On 5 February 2021 the PSR issued a consultation paper on the renewal of the UK’s interbank payment infrastructure. This consultation covers the PSR’s Specific Directions 2 and 3 (SDs). These require Pay.UK to run a competitive procurement for the central infrastructure for Bacs and Faster Payment Service (FPS) respectively. The PSR notes in its consultation paper that “In the light of our conclusions, we will consider whether the directions should be varied, revoked or replaced”. 2. LINK has recently conducted its own competitive tender for its central infrastructure service under a PSR SD (SD4), similar to those now being considered by Pay.UK for Bacs and FPS. LINK is therefore responding because its experience is directly relevant to the PSR’s deliberations. 3. Although the consultation paper poses a number of detailed questions, LINK is providing this single overall response which it believes best summarises its experience. 4. LINK’s recent competitive tender and the resulting Vocalink contract are subject to extensive commercial confidentiality constraints. Therefore, it is not possible to include commercial details in this public document. However, all the key points are set out. The PSR has already been provided with great detail relating to these events in its role as one of LINK’s regulators and therefore has access to other evidence. -

Submission to the Reserve Bank of Australia Response to EFTPOS

Submission to the Reserve Bank of Australia Response To EFTPOS Industry Working Group By The Australian Retailers Association 13 September 2002 Response To EFTPOS Industry Working Group Prepared with the assistance of TransAction Resources Pty Ltd Australian Retailers Association 2 Response To EFTPOS Industry Working Group Contents 1. Executive Summary.........................................................................................................4 2. Introduction......................................................................................................................5 2.1 The Australian Retailers Association ......................................................................5 3. Objectives .......................................................................................................................5 4. Process & Scope.............................................................................................................6 4.1 EFTPOS Industry Working Group – Composition ...................................................6 4.2 Scope Of Discussion & Analysis.............................................................................8 4.3 Methodology & Review Timeframe.........................................................................9 5. The Differences Between Debit & Credit .......................................................................10 5.1 PIN Based Transactions.......................................................................................12 5.2 Cash Back............................................................................................................12 -

2021 Prime Time for Real-Time Report from ACI Worldwide And

March 2021 Prime Time For Real-Time Contents Welcome 3 Country Insights 8 Foreword by Jeremy Wilmot 3 North America 8 Introduction 3 Asia 12 Methodology 3 Europe 24 Middle East, Africa and South Asia 46 Global Real-Time Pacific 56 Payments Adoption 4 Latin America 60 Thematic Insights 5 Glossary 68 Request to Pay Couples Convenience with the Control that Consumers Demand 5 The Acquiring Outlook 5 The Impact of COVID-19 on Real-Time Payments 6 Payment Networks 6 Consumer Payments Modernization 7 2 Prime Time For Real-Time 2021 Welcome Foreword Spurred by a year of unprecedented disruption, 2020 saw real-time payments grow larger—in terms of both volumes and values—and faster than anyone could have anticipated. Changes to business models and consumer behavior, prompted by the COVID-19 pandemic, have compressed many years’ worth of transformation and digitization into the space of several months. More people and more businesses around the world have access to real-time payments in more forms than ever before. Real-time payments have been truly democratized, several years earlier than previously expected. Central infrastructures were already making swift For consumers, low-value real-time payments mean Regardless of whether real-time schemes are initially progress towards this goal before the pandemic immediate funds availability when sending and conceived to cater to consumer or business needs, intervened, having established and enhanced real- receiving money. For merchants or billers, it can mean the global picture is one in which heavily localized use time rails at record pace. But now, in response to instant confirmation, settlement finality and real-time cases are “the last mile” in the journey to successfully COVID’s unique challenges, the pace has increased information about the payment. -

ACI Worldwide and Vocalink Join Forces to Speed up Adoption of Immediate Payments Around the World

September 27, 2016 ACI Worldwide and VocaLink Join Forces to Speed up Adoption of Immediate Payments Around the World Partnership will combine VocaLink's market-leading IPS solution for central payment infrastructures and ACI's UP Immediate Payments solution for financial institutions Combined offering will accelerate the availability of real-time payments globally and speed up the adoption in new markets LONDON--(BUSINESS WIRE)-- ACI Worldwide (NASDAQ: ACIW), a leading global provider of real-time electronic payment and banking solutions, and VocaLink, a global payments systems company, today announced a partnership to offer a complete end-to-end immediate payments solution to launch a domestic or regional immediate payments network. This Smart News Release features multimedia. View the full release here: http://www.businesswire.com/news/home/20160926005151/en/ It is the first global strategic partnership of its kind and will offer participants a pre-integrated solution, enabling quicker onboarding to the payments scheme and broader reach to more scheme participants in a fast and efficient manner. As part of the partnership agreement, VocaLink will provide its Immediate Payments System solution and connectivity software to clearing houses and central banks globally; ACI will deliver its UP Immediate Payments solution, with VocaLink's Immediate Payments Gateway pre-integrated, to enable individual organizations such as financial institutions and other payment providers to access the scheme and process transactions. VocaLink offers a global, market-leading solution for central infrastructures to manage the clearing of real-time payments according to the rules decided by a particular country or region. The solution supports the central infrastructures of the UK Faster Payments and the Singapore FAST schemes, and is also being implemented in the U.S. -

DEBIT CARD POLICY 1. Debit Card a Debit Card Is a Plastic Card That

DEBIT CARD POLICY 1. Debit Card A debit card is a plastic card that provides the cardholder electronic access to his/her bank account(s). It is an instrument that can be used to: Avail of banking services such as cash withdrawal, balance enquiry etc., from any ATM and Micro ATM. Make payments to merchants against purchase, withdrawal of cash at POS or both within the prescribed limit by RBI at merchant outlets. e-Commerce transactions. 2. Understanding a Debit Card. a) Card Number: It is a 16 or 19 digit number linked to customer’s bank account. First 6 digits represent Bank’s identification no., next 4 digits represent Branch Sol ID. Remaining digits indicates serial number of the cards issued by that particular branch. Currently Bank issue debit cards with 16 digit length. b) Name of the Person: Person authorized to use the card. This field is present only on personalized card. c) Valid Date: It is in mm/yy format. The card is valid till the last day of the month. d) Card Verification Value (CVV) /CVV2: A 03 (Three) digit number printed on the back side of every debit card. This is used for validation of online transactions. e) Magnetic Strip: Important information regarding the debit card is stored in electronic format here and hence any kind of scratches or exposure to magnetic fields will cause damage to the card. f) EMV Chip Card: EMV stands for Europay, MasterCard and Visa. EMV is a global standard for credit and debit payment cards based on chip card technology. -

Multi-Lateral Mechanism of Cash Machines: Virtue Or Hassel

International Journal of Engineering Technology Science and Research IJETSR www.ijetsr.com ISSN 2394 – 3386 Volume 4, Issue 10 October 2017 Multi-Lateral Mechanism of Cash Machines: Virtue or Hassel Peeush Ranjan Agrawal1 and Sakshi Misra Shukla2 1 Professor, School of Management studies, MNNIT, Allahabad, Uttar Pradesh,India 2Assistant Professor, Department of MBA, S.P. Memorial Institute of Technology, Allahabad, India ABSTRACT Automated Teller Machines or Cash Machines became an organic constituent of the banking sector. The paper envisionsthe voyage that these cash machines have gone through since their initiation in the foreign banks operating in India. The study revolves around the indispensible factors in the foreign banking environment like availability, connectivity customer base, security, network gateways and clearing houses which were thoroughly reviewed and analyzed in the research paper. The methodology of the research paper includes literature review, derivation of variables, questionnaire formulation, pilot testing, data collectionand application of statistical tools with the help of SPSS software. The paper draws out findings related to the usage, congregation, multi-lateral functioning, security and growth of ATMs in the foreign banks operating in the country. The paper concludes by rendering recommendations to theforeign bankers to vanquish the stumbling blocks of the cash machines functioning. Keywords: ATMs, Cash Machines, Anywhere Banking, Foreign Banking, Online Banking 1. INTRODUCTION The Automated Teller Machine (ATM) has become an integral part of banking operations. Initially perceived as ‘cash machines’, which dispenses cash to depositors, ATMs can accept deposits, sell postage stamps, print statements and be used at institutions where the depositor does not have an account. -

Assessing Payments Systems in Latin America

Assessing payments systems in Latin America An Economist Intelligence Unit white paper sponsored by Visa International Assessing payments systems in Latin America Preface Assessing payments systems in Latin America is an Economist Intelligence Unit white paper, sponsored by Visa International. ● The Economist Intelligence Unit bears sole responsibility for the content of this report. The Economist Intelligence Unit’s editorial team gathered the data, conducted the interviews and wrote the report. The author of the report is Ken Waldie. The findings and views expressed in this report do not necessarily reflect the views of the sponsor. ● Our research drew on a wide range of published sources, both government and private sector. In addition, we conducted in-depth interviews with government officials and senior executives at a number of financial services companies in Latin America. Our thanks are due to all the interviewees for their time and insights. May 2005 © The Economist Intelligence Unit 2005 1 Assessing payments systems in Latin America Contents Executive summary 4 Brazil 17 The financial sector 17 Electronic payments systems 7 Governing institutions 17 Electronic payment products 7 Banks 17 Conventional payment cards 8 Clearinghouse systems 18 Smart cards 8 Electronic payment products 18 Stored value cards 9 Credit cards 18 Internet-based Payments 9 Debit cards 18 Payment systems infrastructure 9 Smart cards and pre-paid cards 19 Clearinghouse systems 9 Direct credits and debits 19 Card networks 10 Strengths and opportunities 19