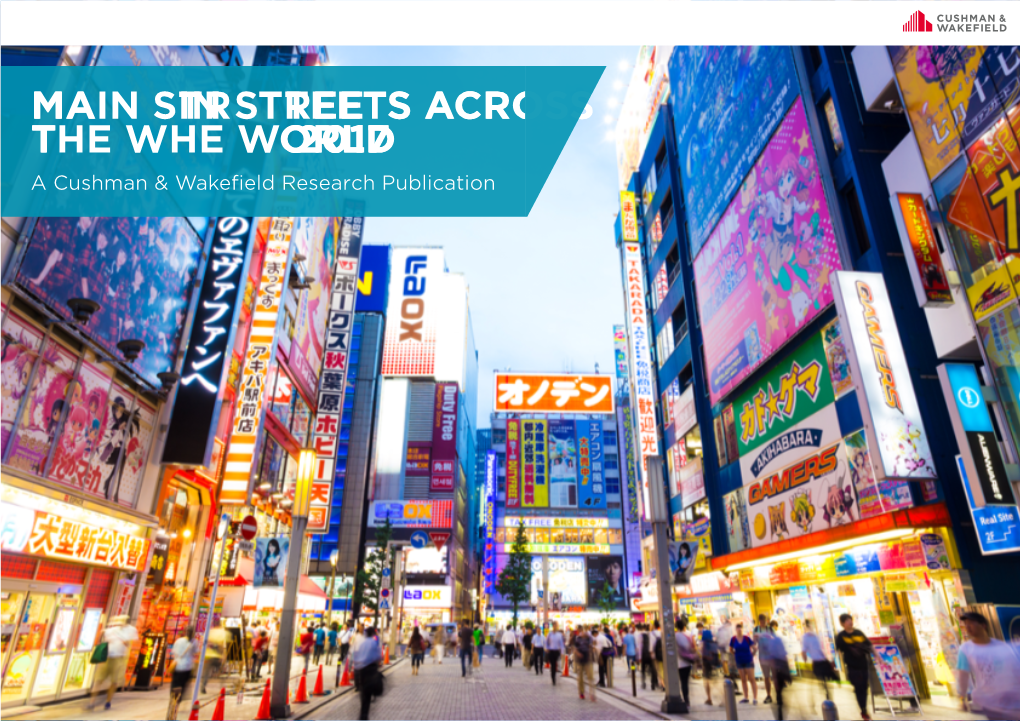

S Main Street Treets Across the W

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

DIE BESTEN STATIONÄRE HÄNDLER 2021 – Einleitung & Methodik

Deutschlands beste Händler DIE BESTEN STATIONÄRE HÄNDLER 2021 – Einleitung & Methodik WILLKOMMEN Die Antwortskala sah folgende Antwortmöglichkeiten vor Einleitung Erkunden Sie das Ranking „Deutschlands beste stationäre Händler“. (in Klammern die interpretative Bedeutung): Das Inhaltsverzeichnis finden Sie auf der nächsten Seite (S. 2). 1 = „Beste Händler“ (am besten in der Branche XYZ) Inhalts- verzeichnis Tippen Sie auf die verschiedenen farbigen Schaltflächen um zu 2 = „Besser als die meisten Händler“ (besser) den entsprechenden Seiten dieses interaktiven Dokuments zu 3 = „Guter Händler“ (gut) Auswertungen gelangen. 4 = „Weder noch“ (nicht gut oder gar besser) 5 = „Nutze ich nur selten“ (nicht bewertungsrelevant) 6 = „Nutze ich gar nicht“ (nicht bewertungsrelevant) DAS RANKING Im Auftrag des Handelsblatts untersuchte das Forschungs- 7 = „Ist mir nicht bekannt“ (nicht bewertungsrelevant) institut ServiceValue insgesamt 1.327 Online-Händler aus 93 Branchen. Je Händler wurden für das Ranking nur die Antworten von den Der Befragung liegen über 306.000 Urteile zu Grunde. Befragten ausgewertet, die in den letzten 12 Monaten Leistun- Das Institut hat die Kunden befragt, wie sie einen Online- gen von dem zu bewertenden Händler wahrgenommen haben Händler im Vergleich zu anderen Online-Händlern der (Antwortmöglichkeiten 1-4). gleichen Branche bewerten. DIE AUSWERTUNG Basis der Untersuchung war eine repräsentativ ausgesteuerte … erfolgte in mehreren Schritten: Online-Erhebung als Kundenbefragung. Die Fragestellung in • Mittelwert: Berechneter Mittelwert -

Heritage and the Economy 2018

HERITAGE AND THE ECONOMY 2018 HERITAGE COUNTS HERITAGE AND THE ECONOMY 2018 England The heritage sector is an VALUE (GVA) important source of economic prosperity and growth For every £1 of GVA directly generated, an additional £1.21 of GVA is supported total GVA of in the wider economy Direct Indirect Induced £ bn £1 + 68p + 53p £6 n 29.0(equivalent to 2% £ £8.9 bn .9 b 13. b n of national GVA) 1 Heritage is an EMPLOYMENT important employer in England For every direct job created, an additional 1.34 jobs are supported in jobs total over the wider economy Direct Indirect Induced 1 +0.78 + 0.56 110 00 1 153 00 ,0 459,000 96,000 ,0 Heritage attracts millions of TOURISM domestic and international tourists each year no. of visits 17.8 Visit / Spend (£bn) ■ International 3.2 trip m visitors ■ Domestic 236.6 203.9 day visit 9.3 (m) tourist spend ■ Domestic 4.4 overnight trip £16.9bn 14.9 Source: (Cebr 2018) 2 HERITAGE AND THE ECONOMY 2018 HERITAGE AND THE ECONOMY The historic environment is intrinsically linked to economic activity, with a large number of economic activities occurring within it, dependent on it or attracted to it. Heritage and the Economy examines the economic aspects of heritage conservation and presents evidence on the numerous ways that the historic environment contributes to the national economy and to local economies. I. Heritage and the economics of uniqueness (p.4) 1. Heritage shapes peoples’ perceptions of place (p.6) 2. Heritage is an important ‘pull’ factor in business location decisions (p.8) 3. -

Zebra Japan KK Flying Tiger Copenhagen, Established in Denmark, Opens Its Flagship Store in Omotesando, Tokyo

Success StoriesーWholesale/Retail Zebra Japan KK Flying Tiger Copenhagen, established in Denmark, opens its flagship store in Omotesando, Tokyo. The brand aims to take Japan’s market by storm together with its partner in Japan. In October 2013, Zebra Japan KK opened Flying are designed so that customers can make new Tiger Copenhagen, its flagship store in discoveries when visiting one of Tiger’s stores. Omotesando, Tokyo for the miscellaneous goods The items, sold by the company, are produced in a chain brand established in Denmark. This is the limited quantity and replaced when they are sold second store for Zebra Japan, a joint venture out. There are 7,500 types of products each year. between the Danish company Zebra A/S and a Price-setting is also a major feature of the Japanese company, Sazaby League, following the company. All items are between ¥100 and ¥2000, opening of its first store in Americamura in and are usually set at good, cut-off prices of ¥100 Shinsaibashi, Osaka in the summer of 2012. and ¥200. The company plans and designs its own Tiger is a lifestyle and miscellaneous goods line of products, and mass-produces items for store developed by Zebra A/S in Copenhagen, each country’s stores, which is the secret to its low Denmark. It opened its first store in 1995, where prices. The company also employs a business almost all items were sold for 10 Denmark Kroner model of “fast, miscellaneous goods” to hold down (about ¥87※as of October 15, 2013). The brand costs related to site locations and advertising. -

Annual Report 2019.Pdf (6.93

Annual Report 2019 Headphones with microphone DKK 70 An invitation to a richer life At Flying Tiger Copenhagen, we don’t design to make products look nice. We design to make people feel good. Whether we are designing extraordinary products for everyday life, or making everyday products look extraordinary, we want to bring you something that can bring you closer to someone else. Things that make you smile. Gifts you’ll want to give. Stuff you feel the urge to try and desperately want to share with others. Because real value lies not in the products we own, but in the experiences we share. Every month, Flying Tiger Copenhagen launches an array of new products. Things you need. Things you dream of. Things you didn’t know existed. Products made with thought for you and the resources we share. Each one designed to make the things you care about happen. A richer life doesn’t cost a fortune. At least not at Flying Tiger Copenhagen. Content 04 The world of Flying Tiger Copenhagen 43 Risk management 06 Message from the Chairman and the CEO 50 Board of Directors 09 Key figures 52 Executive Management 11 Mission and strategy 57 Consolidated financial statements 17 Operating and financial review 2019 107 Financial statements – Parent Company 25 Corporate social responsibility 135 Management statement 39 Corporate governance 136 Independent Auditors’ report We are online 14 Sustainably managed 22 forests Easy Store 38 Diversity 48 matters 4 Management Commentary Zebra A/S Annual Report 2019 Norway 42 stores (-4) Norway 42 stores (-4) Finland Sweden -

Matas A/S Annual Report 2017/18 (1 April 2017 – 31 March 2018)

Matas A/S Annual Report 2017/18 (1 April 2017 – 31 March 2018) Matas A/S, Rørmosevej 1, DK-3450 Allerød, Denmark, CVR no. 27 52 84 06 Five-year key financials DKKm 2013/14 2014/15 2015/16 2016/17 2017/18 Statement of comprehensive income Revenue 3,344.5 3,433.3 3,426.1 3,463.4 3,419.1 Gross profit 1,541.3 1,595.0 1,604.5 1,611.8 1,549.3 EBITDA 599.8 660.5 652.1 620.1 534.5 EBIT 464.4 526.2 513.6 475.1 368.9 Net financials (82.5) (64.5) (36.5) (38.7) (19.7) Profit before tax 381.9 461.7 477.1 436.4 349.2 Profit for the year 248.9 340.3 364.5 338.7 280.3 EBIT 464.4 526.2 513.6 475.1 368.9 Amortisation, intangible assets 99.3 99.0 101.4 102.3 109.9 Amortisation, software* (22.8) (23.1) (25.4) (26.3) (32.7) Special items 29.9 0.0 0.0 0.0 20.1 Special items, impairment 0.0 0.0 0.0 0.0 5.3 EBITA 570.8 602.1 589.6 551.1 471.5 Special items, change of CEO - - - - (12.7) EBITA before special items (guidance) - - - - 458.8 Adjusted profit after tax 374.1 397.5 422.5 398.0 356.2 Statement of financial position Assets 5,487.6 5,336.8 5,315.3 5,270.6 5,303.6 Equity 2,599.9 2,643.5 2,658.3 2,572.5 2,620.9 Net working capital (121.1) (77.4) (172.0) (158.0) (127.3) Net interest-bearing debt 1,623.3 1,564.4 1,423.6 1,515.0 1,471.9 Statement of cash flows Cash flow from operating activities 350.0 422.3 566.9 482.6 383.6 Investments in property, plant and equipment (39.9) (27.9) (45.4) (43.3) (51.7) Free cash flow 173.8 360.2 496.6 348.1 281.5 Ratios Revenue growth 4.5% 2.7% (0.2)% 1.1% (1.3)% Underlying (like-for-like) revenue growth 3.4% 1.5% 0.3% 1.3% -

BORDEAUX Cushman & Wakefield Global Cities Retail Guide

BORDEAUX Cushman & Wakefield Global Cities Retail Guide Cushman & Wakefield | Bordeaux | 2019 0 Located in southwestern France, Bordeaux is the capital of the Nouvelle Aquitaine region and the country’s fifth largest metropolitan area, with more than 1,200,000 inhabitants. Totalling around 92,000 students, the city has a long tradition of teaching excellence, thus providing large tech and industrial groups a highly-qualified workforce. A European hub for aeronautics and space industries, Bordeaux is also considered the wine capital of the world, with the region boasting the most famous grape varieties including Merlot and Cabernet. In the nineties, the historic city centre of Bordeaux underwent a massive urban redevelopment project comprised of the creation of new tramway lines and the conversion of former industrial sites on the now ‘cleaned up’ waterfront. This large- scale project gave a boost to the city as a key tourist destination, also now listed a UNESCO world heritage site. Benefiting from its local residents’ high purchasing power, Bordeaux’s prime retail scene is mainly located in the vast pedestrian area located on the left bank of the Garonne River and hosts a wide range of retailers. Rue Sainte-Catherine and Rue de la Porte Dijeaux are the main hubs for middle- range players in the fashion sector, whereas Cours de l’Intendance is a key destination for upper-range retailers. While prime opportunities in the city centre of Bordeaux are traditionally scarce, it hosts two major shopping centres downtown: Meriadeck (Auchan hypermarket) and the Promenade Sainte-Catherine, providing international retailers with quality space so as to expand their French retail network (e.g. -

Coloured Pencils. 36 Pcs. DKK 30 an Invitation to a Richer Life

Annual Report 2020 Coloured pencils. 36 pcs. DKK 30 An invitation to a richer life At Flying Tiger Copenhagen, we don’t design to make products look nice. We design to make people feel good. Whether we are designing extraordinary products for everyday life, or making everyday products look extraordinary, we want to bring you something that can bring you closer to someone else. Things that make you smile. Gifts you’ll want to give. Stuff you feel the urge to try and desperately want to share with others. Because real value lies not in the products we own, but in the experiences we share. Every month, Flying Tiger Copenhagen launches an array of new products. Things you need. Things you dream of. Things you didn’t know existed. Products made with thought for you and the resources we share. Each one designed to make the things you care about happen. A richer life doesn’t cost a fortune. At least not at Flying Tiger Copenhagen. Content 04 The world of Flying Tiger Copenhagen 46 Board of Directors 06 Message from Executive Management 47 Executive Management 07 Key figures 49 Consolidated financial statements 09 Mission and strategy 101 Financial statements – Parent Company 15 Operating and financial review 2020 127 Management statement 23 Sustainability 128 Independent Auditors’ report 39 Risk management We are 12 online Conscious stores 34 Global Retail 38 Operation One country, one entity 44 Sweden 51 stores (-4) Norway 39 stores (-3) Finland 31 stores Iceland 5 stores Denmark 52 stores (-20) Estonia 8 stores United Kingdom 86 stores (-6) Latvia 6 stores Netherlands 22 stores Lithuania 6 stores Ireland 23 stores (-3) Poland 45 stores Belgium 23 stores (-1) Czech Republic 17 stores (+1) Germany* South Korea 36 stores (-18) Slovakia 18 stores (+4) 8 stores France 52 stores (-4) Hungary 11 stores Austria 13 stores Portugal 36 stores (-1) Spain Switzerland Greece 127 stores (-1) 12 stores (+1) 13 stores Cyprus Japan Italy Malta 6 stores 31 stores (+2) 130 stores 3 store Flying Numbers* Revenue Approx. -

Recueil Des Actes Administratifs

RECUEIL DES ACTES ADMINISTRATIFS Recueil n°83 du 11 janvier 2021 Direction départementale de l’emploi, du travail et des solidarités (DDETS34) Direction départementale des territoires et de la mer (DDTM34) Direction des sécurités – Bureau de la planifcation et des opérations (PREF34 DS BPO) Direction des sécurités – Bureau des préventions et des polices administratives (PREF34 DS BPPA) Secrétariat général commun (SGC34) DDETS34 Arrêté n°2021-0087 composition comité médical 2 DDETS34 Arrêté n°2021-0088 liste médecins agréés du comité médical et commission de réforme 4 DDETS34 Arrêté n°2021-XVIII-115 dérogation travail du dimanche 6 DDTM34 Arrêté n°30-2021-06-02-00003 classement BRL 8 DDTM34 Arrêté n°DDTM34-2021-06-11993 mise à jour des parties prenantes par SLGRI Orb Libron Herault 17 DDTM34 Arrêté n°DDTM34-2021-06-11997 creation ZAD Les Mouliers Est Clapiers 21 DDTM34 Arrêté n°DDTM34-2021-06-11998 creation ZAD Moureze 25 DDTM34 Arrêté n°DDTM34-2021-06-12012 suddélégation SAF 37 DDTM34 Arrêté n°DDTM34-2021-06-12013 avenant n°1 cahier charges concession plages Frontignan 39 DDTM34 Arrêté n°DDTM34-2021-06-12014 prescriptions spécifiqu- es réparation ouvrage permettant à l'A9 de franchir le Pallas Loupian 41 DDTM34 Arrêté n°R 21 034 0005 0 délivrance agrément SOS PERMIS M. Gautier AYME 47 PREF34 DS BPO Arrêté n°2021-01-525 modification composition CHSCT de la police nationale 50 PREF34 DS BPPA Arrêté autorisation enregistrement audiovisuel agents PM Jacou 52 PREF34 DS BPPA Arrêté autorisation enregistrement audiovisuel agents PM Portiragnes -

2016 Holiday Shopping Guide

Dear Fellow Floridians, Happy holidays! Once again, as the holiday season approaches, the Office of Attorney General is happy to offer this 2016 Holiday Consumer Protection Guide, a compilation of product safety information and consumer tips put together to help you enjoy a safer and more satisfying shopping experience. This year, the Guide includes tips on purchasing items online and avoiding charity scams. We have also included a list of items recalled by the U.S. Consumer Products Safety Commission in the past year, specifically focusing on children’s toys and items that pose particular risk to children. These products have been recalled by their manufacturers because of safety and health concerns. Products recalled include toys, furniture, sporting goods and other home products that may be unsafe for children. I urge you to review this list for unsafe items that may need to be removed from your home. Please also keep this Guide handy and review it as you purchase and receive gifts this holiday season. If you have any questions on product recalls or any of the other issues discussed in this Guide, feel free to contact my Citizens Services hotline at 1-866-966-7226, or visit our website at www.MyFloridaLegal.com. You can also find updated lists of recalled items year-round at the U.S. Consumer Product Safety Commission’s website www.CPSC.gov/en/Recalls. Let’s really focus on protecting our children this holiday season! Sincerely, Pam Bondi Florida Attorney General Table of Contents Holiday Shopping Tips……………………………......…………….................................….5 -

L'orientamento Al Cliente

the Italian member of In coll Omniexperience, Engagement e Smart shopping: 45 casi da 17 Paesi a Retail Innovations 14. Quando l’innovazione porta al successo Si è appena concluso con successo a Milano il convegno ‘Retail Innovations 14. Quando l’innovazione porta al successo’, organizzato da Kiki Lab, all’interno del quale è stata presentata la quattordicesima edizione della ricerca realizzata in partnership con il consorzio internazionale Ebeltoft Group. Ad arricchire l’evento le testimonianze aziendali di DMO – Isola dei Tesori, Conad Adriatico, Lanieri, OVS, Nova Coop, Flying Tiger Copenhagen e Huawei con i loro casi di innovazione e di successo. ‘Quest’anno l’Award per il caso più innovativo del mondo, assegnato dal nostro consorzio Ebeltoft Group, è andato a Hema, il concept di superstore lanciato dal gruppo cinese Alibaba, che ha profondamente innovato l’idea di negozio alimentare, in una dimensione omniexperience – Jack Ma preferisce definirla di New Retail. Una prospettiva in cui la fisicità estrema, come pescare con le proprie mani dalle vasche pesci e crostacei vivi che si vogliono acquistare, si integra in modo fluido con la digitalizzazione più radicale, con smartphone che si attivano per scoprire tutte le informazioni sui prodotti e runners che attraversano il negozio per raccogliere i prodotti ordinati online dai clienti.’ – ha spiegato Fabrizio Valente, Founder e Amministratore di Kiki Lab-Ebeltoft Italy – ‘Oggi per una maggiore attrazione e soddisfazione dei clienti è richiesta una rivoluzione copernicana. Le tre aree chiave dell’innovazione individuate quest’anno sono: Omniexperience, Engagement e Smart Shopping.’ Oggi non si può più ragionare in termini di canali, multi-canalità, omni-canalità, ma è necessario mettere al centro l’esperienza complessiva di ogni singolo cliente, ovvero l’omniexperience. -

Annual Report 2018.Pdf (10.41

Annual Report 2018 Kitchen utensils. Assorted DKK 15 · The very first Zebra store opened in 1988 · In 1995 we became a chain of retail stores named Tiger · In 2016 we changed our name to Flying Tiger Copenhagen About across all markets · In our stores you can find things for your home, your hobby, for fun and parties, great gifts and award-winning design. us All at affordable prices · In 2018 we grew revenue by 11 percent to more than DKK 5.5 billion · We have more than 6,000 employees worldwide · We introduce around 300 fun and useful new products each month · There are 77 Flying Tiger Copenhagen stores in Denmark · Our biggest markets are Italy with 126 stores, Spain with 127 stores and United Kingdom with 98 stores · We have a total of 990 stores in 30 countries across three continents Content 04 The world of Flying Tiger Copenhagen 31 Risk management 06 Message from the Chairman and the CEO 38 Board of Directors 07 Key figures 40 Executive Management 09 Mission and strategy 43 Consolidated financial statements 15 Operating and financial review 2018 87 Financial statements – Parent Company 19 Corporate social responsibility 111 Management statement 27 Corporate governance 112 Independent Auditors’ report A more sustainable packaging design 08 Sustainable 22 plastic We support UNGC 30 Meet our 34 colleagues 4 Management Commentary Zebra A/S Annual Report 2018 Norway 46 stores (+2) Faroe IslandsNorway 1 store 46 stores (+2) The world Faroe Islands Finland 1 store Sweden 32 stores (+1) 54 stores (+6) Finland Iceland Sweden 32 stores (+1) of Flying Tiger 5 stores 54 stores (+6) Iceland 5 stores Denmark 77 stores (+2) Estonia 7 stores Denmark Estonia Copenhagen 77 stores (+2) Netherlands 7 stores Latvia 23 stores (+1) Germany 62 stores (+8) 6 stores Zebra A/S, the parent company of the Flying Tiger Copenhagen stores, Flying Tiger Copenhagen stores opened every week. -

L'urbanisme Commercial

Les Scot de l’aire métropolitaine Lyon - Saint-Etienne Agglomération lyonnaise Beaujolais Boucle du Rhône en Dauphiné Bugey-Côtière-Plaine de l’Ain La Dombes Loire Centre Monts du Lyonnais Nord-Isère Ouest lyonnais Rives du Rhône Roannais Sud Loire Val de Saône-Dombes L’urbanisme commercial dans l’aire métropolitaine Lyon - Saint-Etienne Bulletin de veille n° 8 Octobre 2019 1 Urbanisme commercial - Bulletin de veille n° 8 - octobre 2019 Sommaire 1 Conjoncture nationale 4 2 Nouveaux concepts 8 La vie des projets commerciaux 3 de l’aire métropolitaine de Lyon - Saint-Etienne 12 4 Actualité juridique : la loi ELAN et le commerce 16 2 Urbanisme commercial - Bulletin de veille n° 8 - octobre 2019 Le commerce, secteur aux évolutions rapides et à l’impact considérable sur l’aménagement du territoire, nécessite un suivi régulier. Dans le cadre du programme de travail de l’inter-Scot de l’aire métropolitaine Lyon - Saint-Etienne, et à l’initiative des présidents des établissements publics porteurs de Scot, les Agences d’urbanisme de Lyon et de Saint-Etienne sont chargées de mettre en place un système de veille et d’observation mutualisé avec le Pôle Métropolitain. Les Agences publient ainsi un bulletin de veille biannuel qui s’appuie sur différentes sources, principalement issues de la presse et d’entretiens réalisés au sein d’un réseau d’informations (communes, EPCI, Scot, établissements publics d’aménagement, opérateurs privés de l’immobilier commercial, CCI). Ce huitième numéro propose une actualité juridique, conjoncturelle, prospective ainsi qu’un état des lieux des grands projets commerciaux de l’aire métropolitaine Lyon - Saint-Etienne pour la période de juillet 2018 à juillet 2019.