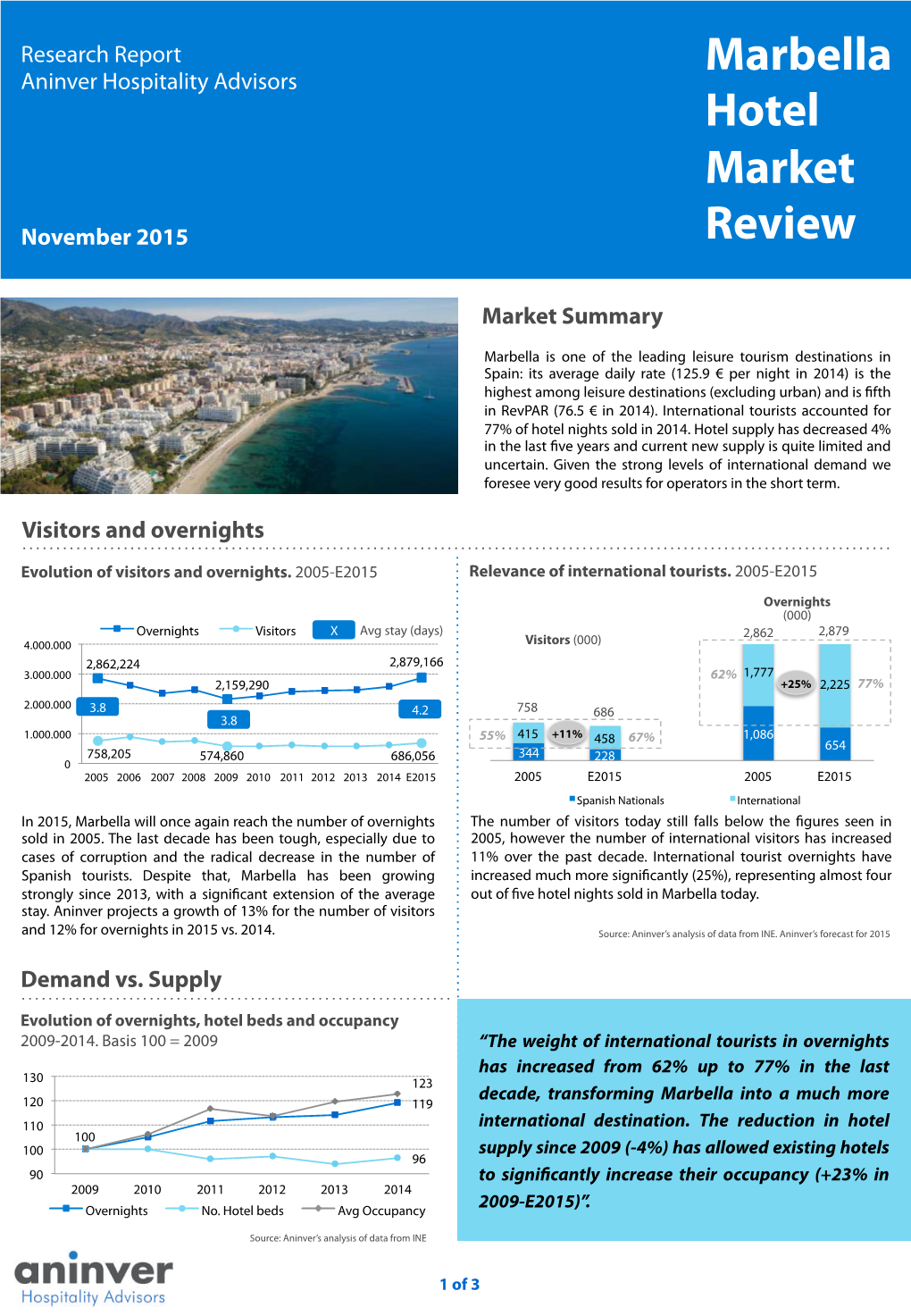

Marbella Hotel Market Review Nov 2015

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Other Businesses

WithWith operationsoperations inin 1414 countriescountries onon 44 continents,continents, Atento Atento hashas consolidatedconsolidated itsits positionposition asas thethe leadingleading CRMCRM businessbusiness withwith globalglobal reachreach OtherOther businessesbusinesses Over the past year, Atento has embarked upon the consolidation of its business, passing from a stage of rapid growth to the generation of profit Atento whole. The increasing outsourcing of CRM services is a clear sign that companies have assigned considerable strategic value to this activity. The CRM industry is a highly fragmented market in which Atento is pioneering the development and implementation of a global strategy. This represents a tremendous opportunity for Atento to confirm its position as a world leader in the industry. With operations in 14 countries spanning 4 continents, Atento already has a significant international presence and has been able to consolidate its position as the leading CRM provider with a truly global vocation. Atento’s growth strategy prioritizes the fast-growing markets of America, Europe and Atento is the Telefónica business line established to handle CRM Asia. (Customer Relationship Management) services, integrating Atento commenced its activities as a strategic partner of the personalized and value added services for each of its customers. It Telefónica Group companies in response to the increasingly includes a wide range of solutions such as telesales, customer care, competitive business environment in the telecommunications market, collections, loyalty, data base management, market research, CRM where the client plays an ever more important role. consultancy, and internet call centres, all of which rests on an From the outset, the company has been leadership oriented in advanced, multi-channel (telephone, fax, e-mail, direct mail, web, etc.) its various markets with the objective of achieving a volume of sales technology platform. -

HOTEL INVESTMENT in the IBERIAN PENINSULA Expansion & Evolution What’S Next?

HOTEL INVESTMENT IN THE IBERIAN PENINSULA Expansion & Evolution What’s Next? SEPTEMBER 2019 CONTENTS INTRODUCTION 03 IBERIAN PENINSULA - HOTSPOT FOR HOTEL INVESTMENT 05 Transaction Activity Momentum Expansion Outside the Core Maturing Markets Rise of Foreign Institutional Investors Evolution of Investment Forms Compressing Yields HEALTHY HOTEL PERFORMANCE FUELLED BY BUOYANT TOURISM 20 Decade of Growth Tourism Boom Hotel Supply - Big & Evolving EVOLVING NATURE OF THE HOSPITALITY SECTOR 39 The emergence of soft brands The rise of affordable lifestyle brands A new generation of hostels Innovative extended-stay concepts Expansion of shared accommodation platforms What do Millennials in Iberia Expect from Hotels? SHORT-TERM ACCOMMODATION APARTMENTS LEGAL & TAX OVERVIEW 56 Tourist Apartments in Spain Short-Term Accommodation Apartments in Portugal REITS IN IBERIAN PENINSULA LEGAL & TAX FRAMEWORK 60 “SOCIMI” - Spanish REIT “SIGI” - Portuguese REIT WHAT’S NEXT? 66 Market Outlook AUTHORS & OTHER CONTACTS 68 ABOUT THE CONTRIBUTORS 69 H10 Cubik Barcelona The tourism sector is one of the fastest-growing industries in the world, increasingly capturing interest from investors. INTRODUCTION We welcome you to our joint Cushman & Wakefield / since 2015, while Portugal took 12th place and continues CMS report ‘Hotel Investment in the Iberian Peninsula*: to rise up the ranks. Expansion & Evolution – What’s Next?’ In this report, we will explore the key investment trends in The tourism sector is one of the fastest-growing Iberia, analyse the underlying performance drivers across industries in the world, increasingly capturing interest all major sub-markets and discuss the innovative trends from investors attracted by the premium returns and shaping the local hospitality sector. We will also provide positive long-term prospects. -

Spanish Hotel Market Resort Destinations

es.christie.com Spanish Hotel Market Resort Destinations This report analyses the main Spanish coastal resort destinations in the Mediterranean and the Atlantic, including Balearic Islands and Canary Islands, highlighting the development of their main hotel performance indicators in 2018. Benefiting from the instability of Mediterranean competitors (Turkey, Tunisia and Egypt), the Spanish resort markets have experienced robust recovery with record numbers in demand, supply and profitability. Consequently, during the last years these markets have turned out as one of the main drivers of tourism growth in the country and, for two consecutive years, have seen a concentration of the majority of hotel investment volume in Spain. Due to qualitative improvements in hotel supply, as well as the opening of new hotels focused on the luxury segment, hotel rates have increased, driving hotel performance consolidation in a more competitive environment. However, the recovery of the Mediterranean competitor destinations and the decrease in UK demand (the main international feeder market) due to Brexit, in addition to the effects of climate change, might affect future demand levels. Throughout this report we analyse the economic, tourism and hotel framework of each resort destination, using public information sources that include: Exceltur, the National Statistics Institute (INE), AENA (Spanish Airports and Air Navigation), Ministerio de Fomento de España, and Alimarket, as well as Christie & Co’s sources. Due to qualitative improvements in hotel supply, as well as the opening of new hotels focused on the luxury segment, hotel rates have increased, driving hotel performance consolidation in a more competitive environment 2 | Christie & Co KEY OBSERVATIONS DEMAND CONSOLIDATION While international demand decreased mainly due to the recovery of Mediterranean competitor markets, the domestic segment consolidated, stabilising overall tourism demand EXCELLENT AIR ACCESSIBILITY There are 22 airports serving Spanish resort markets representing c. -

VACATION PROGRAM Vacation Program Dear Member

Vacation Program - VACATION PROGRAM - VACATION H10 PREMIUM H10 Premium Customer Service USA 1 866 964 0125 Canada 1866 940 5726 USA & Canada 011 800 4773 6486 Mexico 01 800 410 6292 [email protected] Dear Member, It is a great pleasure to present to you H10 Premium, the vacation exchange program by H10 Hotels, the best way to enjoy our hotels with all comforts and services for you and your family. H10 Premium offers you a selection of our best’s establishments at Riviera Maya and Dominican Republic, in the Caribbean, and Canary Islands and Costa del Sol, in Spain. These hotels are sea front, with various gastronomic choices and the best attentive service to make the most of your stay. Our 30 years of experience as hoteliers is the best guarantee to enjoy the holidays you have always dreamt of. We hope to see you soon enjoying your holidays in H10 Hotels. Yours faithfully, Jordi Espelt Managing Director of H10 Hotels Estimado Socio, Nos complace presentarle H10 Premium, el programa de intercambio vacacional de H10 Hotels, diseñado para que usted y su familia puedan disfrutar de nuestros hoteles con las máximas comodidades y servicios. Con H10 Premium le proponemos una selección de nuestros mejores establecimientos en Riviera Maya y República Dominicana, en el Caribe, y las Islas Canarias y la Costa del Sol, en España. Todos ellos ubicados en primera línea de mar, con una variada oferta gastronómica y un atento servicio para que su estancia entre nosotros sea inolvidable. Nuestros 30 años de experiencia como hoteleros es la mejor garantía para disfrutar de las vacaciones con las que siempre había soñado. -

Spanish Hotel Market Urban Destinations

Spanish Hotel Market Urban Destinations christie.es TABLE OF CONTENTS Glossary 3 Introduction 4 Key Observations 5 2018 Overview 6 Air Accessibility 7 Introducing the Urban Hotel Destinations 9 Who are the Feeder Markets? 11 Seasonality and Average Length of Stay 12 Supply 13 KPIs 16 Outlook 18 Overnight to Bed Ratio 20 Barcelona 22 Madrid 24 YTD June 2019 Urban Destinations 26 Team 27 2 | Christie & Co GLOSSARY ADR – Average Daily Rate. It is defined as the income per room for the period divided by the total number of rooms occupied during the mentioned period b – Billion CAGR – Compound Annual Growth Rate C&Co – Christie & Co ECB – European Central Bank INE - Instituto Nacional de Estadística k – Thousand KPI – Key Performance Indicator m – Million Occ – Occupancy. Proportion of occupied rooms over the total number of rooms available in a given period OECD – Organisation for Economic Co-operation and Development PEUAT – Pla Especial Urbanístic d’Allotjaments Turístics. Urban plan for tourist accommodation in Barcelona RevPAR – Revenue per Available Room. Defined as room occupancy multiplied by the average achieved room rate or rooms revenue divided by the number of available rooms GDP – Gross Domestic Product var – Variation YoY – Year-on-year vs – Versus 3 | Christie & Co INTRODUCTION This report analyses 14 Spanish cities (Barcelona, San Sebastian, Palma, Cadiz, Malaga, Madrid, Seville, Bilbao, Valencia, Santander, Alicante, Cordoba, Granada and Santiago de Compostela), highlighting the evolution of their main hotel performance indicators in 2018, as well as YTD 2019 data, the future outlook of the markets and a comparison between the Overnight to Bed Ratio of Barcelona and Madrid with other European urban destinations. -

European Chains & Hotels Report 2019

European Chains & Hotels Report 2019 Contents Welcome to Horwath HTL, the global leader in hospitality consulting. We are the industry choice; a global brand providing quality solutions for hotel, tourism & leisure projects. Page 5 Forward Page 32 Albania Page 7 Introduction Page 36 Croatia Page 42 Cyprus Page 10 Chain Hotels & Brands Page 46 Denmark Page 14 Year-on-Year Growth Page 50 France Page 16 Supply Page 56 Germany Page 18 Chain Hotels & Rooms Page 62 Greece Page 22 International Capital Flows Page 68 Hungary Page 24 Investment Page 74 Ireland Page 26 Openings & Deal Signing Page 80 Italy Page 28 Business Model Page 86 Montenegro Page 92 Netherlands Page 98 Norway Page 102 Poland Page 108 Portugal Page 114 Serbia Page 120 Slovenia Page 126 Spain Page 132 Sweden Click on this icon for easy navigation Page 136 Switzerland of the document Page 142 Turkey Page 148 United Kingdom Horwath HTL l European Hotels & Chains Report 2019 3 Forward The report looks at the relationship between hotel chains, their myriad of brands, and the wider world of hospitality and lodging. A very warm welcome to the new edition of the Horwath We look at the models used by the chain companies HTL Chains & Hotels Report, the third annual instalment. and see which ones are the most prevalent, in which The report looks at the relationship between hotel chains, market segment. and their myriad of brands, and the wider world of hospitality and lodging. In this edition, we have enhanced the report in a number of key ways. Firstly, we have greatly expanded the scope There have been two big stories over the last 25 years of the markets, from 12 last year to 22 this. -

Madrid, Spain

Special Market Reports Issue 77 - MADRID, SPAIN November 2016 MADRID IN NUMBERS Jan-April 2016 Occupancy 63% 71% 71% €71 ADR €174 €87 ∆6% ∆6% ∆10% €110 €62 €50 RevPAR ∆6% ∆11% ∆11% TOURIST DEMAND HOTEL SUPPLy TOURIST ARRIVALS 10 ExPECTED FOR 2016 266 MILLION HOTELS JULy 2016 ∆ 12.4 % ARRIVALS - MADRID 38 AIRPORT (JAN - SEP 2016) 67,581 HOTEL BEDS MILLION ∆ 7.7 % JULy 2016 TOTAL TOURIST ExPENDITURE (JAN - SEP 2016) % €5 PERCENTAGE OF 4* 52 ∆ 13 % HOTELS BILLION AVERAGE DAILy ExPENDITURE PER TOURIST (JAN - SEP 2016) PERCENTAGE OF HOTELS UNDER ∆ 8.6 % INTERNATIONAL % €208 BRAND 24 TRANSACTIONS PIPELINE ACCUMULATED HOTEL €310 INVESTMENT IN 2016 NEW ROOMS UNDER 1,165 Million (up to September) CONSTRUCTION Special Market Reports Issue 77 - Madrid, Spain Madrid: Tourism & Hotel Heritage sites by UNESCO: Alcalá de Henares, Aranjuez, El Market Analysis Escorial, Segovia, Avila, Toledo and Salamanca. Gastronomy: the city has a wide and rich gastronomic Political, social, demographic and economic offer, with 13 centenarian restaurants (including Casa situation in Madrid Botin, claimed to be the oldest restaurant in the world), 15 restaurants awarded a total of 23 Michelin stars (Diverxo Madrid, the capital and largest city in Spain and the fourth was awarded three stars in 2013), and nine gastronomic & largest in Europe, with 3.2 million inhabitants excluding culinary spaces (including Plataea, Mercado de San Miguel the metropolitan area, is the main financial and business and Mercado de San Anton), plus numerous gastronomic center in the country as well as a dynamic and growing events such as MadrEAT. destination for all types of tourism. -

European Hotel Transactions 2009 an Age of Austerity

MARCH 2010 £250 European Hotel Transactions 2009 An Age of Austerity CRISTINA BALEKJIAN, Market Intelligence Analyst ELKE GEIEREGGER, Senior Associate SAURABH CHAWLA, Associate Director HVS – London Offi ce 7-10 Chandos Street Cavendish Square London W1G 9DQ Tel: +44-20-7878-7700 Fax: +44-20-7878-7799 Key Issues ‘half’ a 50% stake in the Four Seasons GDP in the Eurozone is estimated Hotel des Bergues in Geneva. The UK to have declined by 4.1% in 2009, How does investment activity took the largest chunk of a relatively compared to growth of 0.8% in 2008. in 2009 compare to that of small distressed-assets pie. The As a result of plunging financial previous years? Aviemore Highland Resort; the Park markets and the general global Inn London, Russell Square; and the economic slowdown, the European What about distressed sales? Marconi building (the former Silken economy entered into an economic project) were the key assets taken out crisis the like of which had not been Who was still able to buy or of administration. seen for more than a decade. For much sell? A lack of funding from banks of the year, the economic environment meant that portfolio transactions How did Europe’s main continued to prove difficult and this faced considerable hurdles, as nearly transaction markets fare? further restricted hotel investment, all such transactions are highly as there was a lack of financing and What to expect in 2010. leveraged. Only €1 billion of the total a lack of confidence in the markets, transaction volumes (approximately and hotel performance continued to Introducti on 35%) were attributable to portfolios, weaken. -

European Hotels & Chains Report 2017

European Hotels & Chains Report 2017 Key Services Welcome to Horwath HTL, the global leader in hospitality consulting. We are the industry choice; a global brand providing quality solutions for hotel, tourism & leisure projects. Horwath HTL l The Global Leader in Hotel, Tourism and Leisure Consulting CONTENTS 6 FOREWORD 8 INTRODUCTION 14 AUSTRIA 20 CROATIA 26 CYPRUS 30 FRANCE 36 GERMANY 42 HUNGARY 48 IRELAND 54 ITALY 60 NETHERLANDS 66 POLAND 72 SPAIN 78 SWITZERLAND 84 UNITED KINGDOM Horwath HTL l European Hotels & Chains Report 2017 5 Horwath HTL l The Global Leader in Hotel, Tourism and Leisure Consulting FOREWORD “The goal behind the report was to try and accurately shed light on the current situation and see how markets were evolving. Investors need transparency and brands need to know what the competitive landscape looks like.” A few years ago, our team in Rome decided Some of this data exists elsewhere of course, to put together a report on the state of hotel there are a number of countries that have good chains in Italy, no easy task as you can imagine. amounts of data on their hospitality industry, some for sale and some free to access. What became clear as we investigated the market was that it was complicated and A surprising number of countries do not however, opaque, a labyrinth of family ownership and and we saw an opportunity to consolidate much local brands many of whom were unheard of of this data in one place to make it easier to have outside of their local city, let alone Italy itself. -

ESTABLECIMIENTOS HOTELEROS (18ª Edición)

CÓDIGO CNAE: 55.10 ESTABLECIMIENTOS HOTELEROS (18ª edición) ABRIL 2012 GRATUITO EJEMPLAR ESTABLECIMIENTOS HOTELEROS Abril 2012 CONDICIONES DE ADQUISICIÓN DEL ESTUDIO El presente estudio ha sido entregado a su adquirente exclusivamente para sí y para su propia organización en un sólo lugar de trabajo y, por tanto: Todos los derechos de reproducción, traducción, adaptación, incluso parcial, por cualquier medio incluido microfilm, soportes magnéticos, imprenta y fotocopia para España y para el resto del mundo están reservados a Informa D&B, S.A. Los estudios monográficos y documentos recibidos por el adquirente de Informa D&B, S.A. no pueden ser divulgados ni cedidos a terceros aunque se trate de asociados, vinculados o similares ni siquiera gratuitamente y/o en forma de ex- tracto sin autorización de Informa D&B, S.A. Informa D&B, S.A. se reserva los derechos de explotación de su obra en cual- quier forma (art. 17 del Texto Refundido de la Ley de Propiedad Intelectual, aprobado por Real Decreto Legislativo 1/1996 de 12 de abril). El adquirente asume la responsabilidad frente a Informa D&B, S.A. por cualquier vulneración de los derechos de propiedad intelectual y de los derechos de co- pia, por parte de los propios cotitulares, socios administradores, colaboradores y dependientes (art. 23 y 55 del Texto Refundido de la Ley de Propiedad Intelec- tual, aprobado por Real Decreto Legislativo 1/1996 de 12 de abril). GRATUITO EJEMPLAR EJEMPLAR ESTABLECIMIENTOS HOTELEROS Abril 2012 ÍNDICE DE CONTENIDOS Identificación y segmentación del sector ............................................................. 1 PRINCIPALES CONCLUSIONES ........................................................................ 2 1. ESTRUCTURA Y EVOLUCIÓN DEL SECTOR .................................................. -

03 Zyxwvutsrqponmlkjihgfedcb K Zywvutsrponmlkjihgedcbaz

Alimarket 16/03/2016 Tirada: 8.000 Categoría: Rev Alimentación Hosteleria y Difusión: 4.800 Edición: Nacional RestauraciÃn Audiencia: 14.400 Página: 52 AREA (cm2): 472,9 OCUPACIÓN: 75,8% V.PUB.: 1.907 NOTICIAS EXCELTUR Canarias, una nueva edad de oro l archipiélago canario parece zación Turística, que sólo permitía De hecho, algunos de los grupos estar viviendo una nueva construir nuevos hoteles en si eran hoteleros presentes en las islas no Eedad dorada turística al de 5E o superior. Este artículo comparten la supresión de la Ley y batir récords sucesivos en vetaba la edificación de nuevos recuerdan que "habría que seguir zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA el número de visitantes. En con- zyxwvutsrqponmlkjihgfedcbaVUTSRPONMLJIHGFEDCBAestablecimientos de 4E, una de las mejorando los productos, para creto, llegaron 11,58 M de turistas principales demandas del Cabildo lograr el objetivo de subir los pre- internacionales en 2015, un 1% más de Gran Canaria y sus empresarios cios", tal y como reconocen desde de los que recibió en 2014, año que turísticos, aunque no compartido Meeting Point Spain, filial hotelera había cerrado también con el que por otras administraciones locales. del touroperador alemán FTI en hasta entonces había sido el mejor dato de su historia, según las cifras del INE. Como viene siendo tradi- Ranking de grupos hoteleros en Canarias cional, contribuyeron a ese incre- mento los turistas llegados del Rei- 2015 2016 no Unido, Alemania y de los países N°Est Ud.Aloj. N°Est Ud.Aloj. nórdicos, aunque resulta reseñable, 1 RIU HOTELS & RESORTS 20 6.812 19 6.373 el crecimiento del 7% del turismo 2 H10 HOTELS 15 5.440 16 5.634 nacional, hasta llegar a los 1,6 M 3 LOPESÁN HOTELS & RESORTS 12 5.211 11 5.211 de visitantes españoles. -

Staying Power European Cities Hotel Forecast for 2016 and 2017

www.pwc.com/hospitality Staying power European cities hotel forecast for 2016 and 2017 March 2016 European cities hotel forecast 2016 and 2017 analyses trading trends and provides econometric forecasts for 19 cities, all national or regional capitals of finance, commerce and culture. This year, in addition to looking at what might go right or wrong for the economic and travel outlook, we also look at some of the key risks lurking for hotels, including cyber security, data theft and privacy. We also examine the impact of strong hotel trading on the deals outlook in Europe and the potential impacts of low oil prices for the sector. Foreword Despite global economic worries, The global fall in oil prices may also Responding to risks in today’s complex last year saw an exceptionally strong be helping. Consumers have more and changing market requires a new travel backdrop which led to record money in their wallets for discretionary focus. The principal vulnerabilities hotel trading and double digit Revenue spending and we are starting to see include cyber security, data theft and per available room (RevPAR) growth falls in airline fares. GDP growth has big data. In 2016 politicians, across eight of the cities in this survey. remained strong in the US and some regulators, insurance companies, We expect this trend to have staying of Europe’s key travel markets, credit-rating agencies, shareholders, power, with most cities in this survey although weaker performance in customers, suppliers and employees forecast to see positive revenue growth emerging economies such as China, will demand more care from those in 2016 and 2017, albeit growth is Russia and Brazil will dampen demand.