World Bank Document

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

CPTM Forma Técnicos Em Manutenção Metroferroviária

Poder Executivo seção II Estado de São Paulo Geraldo Alckmin - Governador Palácio dos Bandeirantes • Av. Morumbi 4.500 • Morumbi • São Paulo • CEP 05650-000 • Tel. 2193-8000 Volume 127 • Número 196 • São Paulo, quinta-feira, 19 de outubro de 2017 www.imprensaofi cial.com.br CPTM forma técnicos em manutenção metroferroviária possibilidade de o aluno aprendiz boa parte fez curso técnico e de aprendizado ser contratado como profissional é no Senai”, menciona o diretor. A um dos atrativos do curso Técnico de Manutenção de Sistemas Metro- Guilherme (ao Teoria e prática – Na Via Perma- ferroviários. Ministrado no Centro lado do instrutor nente Didática há “treino de rede aérea de Formação Profissional Eng° James Cândido): “Ser (não energizada), que é baixa para facilitar C. Stewart, é mantido pela Compa- efetivado na CPTM a observação de detalhes”, informa o dire- FOTOS: GENIVALDO CARVALHO FOTOS: GENIVALDO nhia Paulista de Trens Metropoli- é meu objetivo” tor. Há trilhos com dormentes de madeira tanas (CPTM), em convênio com o e de concreto na via de 1,60 metro de bitola. Senai-SP. “O curso oferece formação “É para aprenderem as particularidades das muito específica – em São Paulo é o seis linhas da CPTM”. A Estação Ferroviária único curso de técnico em manuten- Didática serve para mostrar “o funcionamen- ção metroferroviária. Por isso, tem to da linha de bloqueio (catraca), sistemas uma concorrência gigantesca”, des- envolvidos na operação e segurança, além taca o diretor do Centro de For ma- de outros recursos disponíveis nas estações”. ção, Wilson Sanches. Há também vários laboratórios (hidráu- lica, pneumática, soldagem) usados para Três mil alunos já “ensaios técnicos e aplicação de conceitos”, diz Sanches. -

Asset Management in Rail Public Transport Sector and Industry 4.0 Technologies

Bruno Teixeira Cavalcante de Magalhães Daniel Machado dos Santos Débora Cristina Faria de Araújo Gustavo Henrique Lucas Jaquie ASSET MANAGEMENT IN RAIL PUBLIC TRANSPORT SECTOR AND INDUSTRY 4.0 TECHNOLOGIES Brasília, Brazil November 2020 Bruno Teixeira Cavalcante de Magalhães Daniel Machado dos Santos Débora Cristina Faria de Araújo Gustavo Henrique Lucas Jaquie A Final Educational Project Submitted to Deutsche Bahn AG in Partial Fulfillment of the Requirements for the Rail and Metro Rail Transportation Systems Management Certificate Program This Final Educational Project was prepared and approved under the direction of the DB Rail Academy, Mr. Marcus Braun. Brasilia, Brazil November 2020 ABSTRACT Industry 4.0 is the concept adopted to refer to new technologies that have been deeply impacting the entire industry, in practically all sectors. The development of technologies associated with the internet of things (IoT) and intelligent systems is driving the industry towards digital transformation. In this scenario, many possibilities arise for the rail public transport sector, mainly for Asset Management, considering that Asset Management represents a significant portion of the operator's efforts and costs to keep the commercial operation running. This work presents the traditional asset management concepts currently used in the public transport sector on rails, as well as some opportunities for using Industry 4.0 technologies in this sector. Then, a methodology for implementing these opportunities is proposed, with the agile methodology being suggested as an implementation strategy, considering a cost- benefit analysis, risk analysis, project plan, implementation plan and financial plan. It is expected that the ideas presented in this work can stimulate other sectors of the industry to move towards Industry 4.0, which is an inevitable trend and will certainly determine in the medium and long term who will survive in an increasingly competitive environment. -

Redalyc.The Maturity of Rail Freight Logistics Service Providers in Brazil

Production ISSN: 0103-6513 [email protected] Associação Brasileira de Engenharia de Produção Brasil Farias Bueno, Adauto; Hazin Alencar, Luciana The maturity of rail freight logistics service providers in Brazil Production, vol. 26, núm. 2, abril-junio, 2016, pp. 359-372 Associação Brasileira de Engenharia de Produção São Paulo, Brasil Available in: http://www.redalyc.org/articulo.oa?id=396745849009 How to cite Complete issue Scientific Information System More information about this article Network of Scientific Journals from Latin America, the Caribbean, Spain and Portugal Journal's homepage in redalyc.org Non-profit academic project, developed under the open access initiative Production, 26(2), 359-372, abr./jun. 2016 doi: http://dx.doi.org/10.1590/0103-6513.178414 The maturity of rail freight logistics service providers in Brazil Adauto Farias Buenoa*, Luciana Hazin Alencarb** aUniversidade do Estado de Mato Grosso, Barra do Bugres, MT, Brazil bUniversidade Federal de Pernambuco, Recife, PE, Brazil *[email protected], **[email protected] Abstract This study analyzes the maturity of three rail freight Logistics Service Providers (LSPs) in Brazil in a population of seven operators. After an exploratory review of the existing literature and research documents, a structured questionnaire based on the Supply Chain Capability Maturity Model S(CM)2 was applied. The study measured an overall average level, given in S(CM)2, as Managed, meaning that the managerial development standard of the logistics agents was at an intermediate level. The results showed that maturity was related to the size of the LSP and the complexity of the organizational management. These findings can support the development of policies and strategies for the improvement and adoption of practices that best lead to gains in competitiveness for both LSPs and the Supply Chains (SCs) that require their services. -

UNIVERSIDADE DE SÃO PAULO Faculdade De Filosofia, Letras E

UNIVERSIDADE DE SÃO PAULO Faculdade de Filosofia, Letras e Ciências Humanas Departamento de Geografia TRABALHO DE GRADUAÇÃO INDIVIDUAL EM GEOGRAFIA De espaço de circulação a objeto de uso turístico: A Estrada de Ferro do Paraná CRISTINA ASSIS PARADA N° USP 7245910 - NOTURNO São Paulo 2016 CRISTINA ASSIS PARADA De espaço de circulação a objeto de uso turístico: A Estrada de Ferro do Paraná Trabalho de Graduação Individual apresentado ao Departamento de Geografia da Faculdade de Filosofia, Letras e Ciências Humanas da Universidade de São Paulo para obtenção do título de Bacharela em Geografia Orientadora: Profa. Dra. Rita de Cássia Ariza da Cruz São Paulo 2016 AGRADECIMENTOS Agradeço, antes de qualquer palavra, meus pais, Sonia e Gim, minhas irmãs, Michelli e Priscilla. Pelo amor que nos mantem sempre unidos, pela força que nos faz acreditar em sermos tudo o que somos porque construímos à nossa maneira. Agradeço ao meu grande companheiro Heitor Faria Rodrigues. Em tudo me fez melhor e me fez acreditar. Aquilo que é invisível aos nossos olhos, invisível às palavras. Agradeço a toda minha família e a família que ganhei com o Heitor. Pelas palavras, olhares, desdobramentos, orações, pensamentos bons, força. Tudo isso me fez resistir àquilo que precisei passar. E passou. Aos meus amigos que estiveram sempre próximos. Aos amigos que a Universidade de São Paulo me confiou, amigos da Graduação, amigos extraídos do trabalho. A todos os Professores que tive contato em minha graduação, essenciais em minha formação. A Professora Rita, minha orientadora, não apenas por ter acreditado nesta pesquisa, mas também pelo apoio e a sua maneira de me fazer não desistir dos meus sonhos. -

AVISO DE LICITAÇÃO Companhia De Processamento De Dados Do

terça-feira, 15 de janeiro de 2019 Diário Ofi cial Empresarial São Paulo, 129 (9) – 17 continuação continuação continuação na Rua Boa Vista nº 175 - Edifício Cidade II - Térreo - Centro - São Paulo/SP, onde HOMOLOGAÇÃO HOMOLOGAÇÃO DE LICITAÇÃO, ocorrerá a sessão pública de processamento da licitação. A Sabesp comunica a homologação do PG 05.174/18 – CONSÓRCIO GUARUS ADJUDICAÇÃO E EXTRATO DE CONTRATO - Dossiê franqueado para vistas no MND14, R. Conselheiro Saraiva, 519 - Santa- Contrato CS-PE060/18 – BK CONSULTORIA E SERVIÇOS LTDA. – Prestação de AVISO DE LICITAÇÃO na - SP/SP, das 08:30/11:30 e 13:30/16:00h. SP, 15/01/19 – MN. serviços de suporte às atividades do Laboratório de Papel e Celulose, do Cen- LICITAÇÃO Nº 8383180001 - EXECUÇÃO DE OBRAS CIVIS PARA ADEQUAÇÃO tro de Tecnologia de Recursos Florestais, do IPT - prazo 12 meses - Valor R$ DE ACESSIBILIDADE DA ESTAÇÃO CAIEIRAS DA CPTM, VISANDO O ATENDI- HOMOLOGAÇÃO 92.400,00 - Modalidade: Pregão Eletrônico nº PE060/18 - Processo nº16965/18 MENTO AO TAC - TERMO DE AJUSTAMENTO DE CONDUTA. Sessão Pública: 19/02/2019 às 10:00 horas A Sabesp comunica a homologação do PG 05.173/18 – HR SERVIÇOS DE LEI- - Assinatura: 17/12/18. Funcional Programática 1966510215840 - Natureza O edital estará disponível a partir do dia 15/01/2019, nos sites www.cptm.sp. TURA E ENTREGA DE CONTAS DE ENERGIA LTDA - Dossiê franqueado para Econômica 33903999. Parecer Análise de Contrato AJ-1213/18 de 10/12/18 – gov.br e www.imprensaoficial.com.br e na Rua Boa Vista nº 175 - Edifício Ci- vistas no MND14, R. -

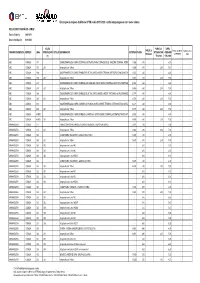

Rel.Tarifário Rmsp

Em função do reajuste do Metrô e CPTM no dia 01/01/2020 a tarifa integrada passa a ter novos valores. RELATÓRIO TARIFÁRIO - RMSP Data da Vigência: 20.01.2019 Data da Atualização: 03.01.2020 SEÇÃO/ PARCELA TARIFA PARCELA Ônibus com Metrô Complemento a CONSÓRCIO/EMPRESA SERVIÇO LINHA INTEGRAÇÃO CIRCULAR DENOMINAÇÃO EXTENSÃO TARIFA INTEGRAÇÃO + PEDÁGIO PEDÁGIO ou SPTRANS pagar (2) TRILHOS + TRILHOS ABC COMUM 195 - - SAO BERNARDO DO CAMPO (TERMINAL METROPOLITANO FERRAZOPOLIS)- DIADEMA (TERMINAL METROPOLITANO 13,096 PIRAPORIN 4,55HA) via SAO -BERNARDO DO - CAMPO (BAIRRO 4,55 DOS CASA) - - ABC COMUM 195 261 - Integração com Trilhos 13,096 4,55 - 2,90 7,45 - - ABC COMUM 196 - - SAO BERNARDO DO CAMPO (PARQUE SELECTA)- SANTO ANDRE (TERMINAL METROPOLITANO SANTO ANDRE-OESTE) 18,551 via SAO 4,60 BERNARDO DO- CAMPO (BAETA - NEVES) 4,60 - - ABC COMUM 196 261 - Integração com Trilhos 18,551 4,60 - 2,90 7,50 - - ABC COMUM 238 - - SAO BERNARDO DO CAMPO (PARQUE LOS ANGELES)- SANTO ANDRE (TERMINAL METROPOLITANO SANTO ANDRE-OESTE) 25,850 via 4,60 SAO BERNADO - DO CAMPO -(JARDIM DA 4,60 REPRESA) - - ABC COMUM 238 261 - Integração com Trilhos 25,850 4,60 - 2,90 7,50 - - ABC COMUM 366 - - SAO BERNARDO DO CAMPO (PARQUE SELECTA)- SANTO ANDRE (JARDIM CRISTIANE) via SAO BERNARDO DO CAMPO21,774 (BAET A 4,60 NEVES) - - 4,60 - - ABC COMUM 366 261 - Integração com Trilhos 21,774 4,60 - 2,90 7,50 - - ABC COMUM 409 - - SAO BERNARDO DO CAMPO (JARDIM LAS PALMAS)- SANTO ANDRE (TERMINAL METROPOLITANO SANTO ANDRE-OESTE) 25,577 4,60 - - 4,60 - - ABC COMUM 409 261 - Integração -

Fidc Companhia Paulista De Trens Metropolitanos - Cptm

FIDC COMPANHIA PAULISTA DE TRENS METROPOLITANOS - CPTM Processo CVM RJ-2006-7551 Histórico do Processo: Entrada: 29.Set.2006 Envio de ofício de exigências: 30.Out.2006 Resposta do regulado: 17.Nov.2006 Envio de ofício de oportunidade para suprir vícios sanáveis: 4.Dez.2006 Pleito do Regulado: Obtenção dos registros de funcionamento de que trata o art. 8º e de oferta pública de distribuição de cotas previsto no art. 20, ambos da Instrução CVM nº 356/01. Motivo do envio ao Colegiado: A parcela preponderante do patrimônio líquido do Fundo é composta por créditos não-performados, conforme disposto no item 9.1 do regulamento. Características do Fundo: Forma de condomínio: fundo fechado. Prazo de duração: 84 meses. Administrador: BEM DTVM Ltda. Cedente: Companhia Paulista de Trens Metropolitanos – CPTM Custodiante: Banco Bradesco S.A. Auditor Independente: KPMG Auditores Independentes. Assessoria Jurídica: Pinheiro Neto Advogados. Rating: Aa3.br, concedido pela Moody´s América Latina Ltda. Benchmark: O Fundo buscará atingir a rentabilidade equivalente à variação do IPCA no período, acrescida de uma taxa de juros anual a ser apurada em processo de bookbuilding. Houve pagamento da taxa de fiscalização de que trata a Lei nº 7940/89. O prospecto da presente oferta foi encaminhado à STN assim que recebido pela GER-1. O montante de R$ 50 milhões em cotas subordinadas será subscrito privadamente pela cedente, a qual transferirá a titularidade de tais cotas, imediatamente após sua integralização, à Companhia Paulista de Parcerias – CPP, mediante a celebração de instrumento particular de compra e venda de cotas subordinadas, consoante informação disposta na seção IX do prospecto do Fundo. -

Projection of Macroeconomic Impacts on the Toll Plazas Waiting Time Queueing: a Case Study in Brazil

International Journal of Research in Engineering and Science (IJRES) ISSN (Online): 2320-9364, ISSN (Print): 2320-9356 www.ijres.org Volume 4 Issue 3 ǁ March. 2016 ǁ PP.68-80 Projection of Macroeconomic Impacts on The Toll Plazas Waiting Time Queueing: A Case Study In Brazil Mariana Gonçalves de Carvalho Wolff*, Marco Antonio Farah Caldas Industrial Engineering, Universidade Federal Fluminense, Niterói, Brazil. Rua Passos da Pátria, 156, Bloco D, Sala 309, São Domingos, Niterói, Brazil. SUMMARY:- This study aims to understand the flows of vehicular traffic in a toll plaza impacted by macroeconomic events. The study provides the traffic demand of commercial and small vehicles on a Brazilian highway until the year 2020. This Highway plays an important role for the oil industry and the development of the region depends mostly on it. The population, the region's Gross Domestic Product and oil production are considered as explanatory variables. The data used is divided by the toll plaza, vehicle type and area of influence. A simulation model for discrete events is used based on the actual scenario and future events. The model concludes that the amount of commercial vehicles will rise significantly, generating an increase in the queue waiting time of the toll plazas, going up to nineteen minutes. To reduce the stakeholders impact the study suggests some steps for planning the highway in the medium term. Keywords:- logistics bottleneck; simulation; macroeconomic development; transportation planning; linear regression. I. INTRODUCTION The country´s economic development needs a quality infrastructure that allows a flow of vehicles and people and also allows developing less accessible areas, facilitating their access to major cities and ports. -

The Feasibility Study for Establishment of Passenger Rail in the Metropolitan Region of Belo Horizonte / Brazil

The Feasibility Study for Establishment of Passenger Rail in the Metropolitan Region of Belo Horizonte / Brazil Marcelo Franco PORTO School of Engineering, Federal University of Minas Gerais Belo Horizonte, Minas Gerais, Brazil and Luiz Carlos de Jesus MIRANDA Nilson Tadeu Ramos NUNES Cássio E. dos SANTOS Jr. School of Engineering, Federal University of Minas Gerais Belo Horizonte, Minas Gerais, Brazil ABSTRACT There are investments to existing lines disabled or in poor condition, as well as incentives for redeployment of passenger The rail transportation, either of passengers or cargo, is transport in sections where only the cargo remained. These essential to the country's economic growth. Due to a number of lines could play a strategic role in the mobility issue because factors, in particular, severe mobility problems experienced by they are in metropolitan regions or make the connection large cities and a demand for urban transport systems and between cities large and medium-sized with a large demand for suburban high capacity transport on rails going through a high capacity transportation. period of recovery with new investments being announced both for the construction of new railway sections, as for reclamation 2. HISTORICAL DEVELOPMENT and re-adaptation of existing railway networks. In this context, the liability of decades without investment, necessitates a The railroads arrived in Brazil still in the Imperial period. A rational use of available resources and agile enabling to country special law of 1852, which established the security interest on develop projects for the sector rapidly and consistently. This the capital invested in railway construction, besides other paper presents a proposal that aims to make it easier to review advantages is it possible to leverage the construction of the first and registration of a railroad. -

Abstracts Summaries by Session

2016 SCALE LATIN AMERICA CONFERENCE 70 MEMORIAL DR., E51-345, CAMBRIDGE MONDAY & TUESDAY, MARCH 21-22, 2016 ABSTRACTS SUMMARIES BY SESSION One Amherst St., E40-365 Cambridge, MA 02142 617.253.3630 http://scale.mit.edu 1 2016 SCALE LATIN AMERICA CONFERENCE 70 MEMORIAL DR., E51-345, CAMBRIDGE MONDAY & TUESDAY, MARCH 21-22, 2016 Conference Program Day 1 – Monday, March 21 8:00 Registration 8:30 Welcome & Breakfast 9:10 Keynote Speaker: Prof. Yossi Sheffi, MIT Center for Transportation & Logistics The Power of Resilience: How the Best Companies Manage the Unexpected 10:10 Break 10:30 Paper Presentations - Parallel Sessions Innovative Cases Studies in Logistics & SCM I. E51 – 372 Applied Operations Research I . E51 – 376 Urban Logistics I . E51 – 395 12:10 Break 12:30 Lunch. The MIT Graduate Certificate in Logistics & SCM - Informative Session 14:00 Paper Presentations - Parallel Sessions Innovative Cases Studies in Logistics & SCM II . E51 – 372 Applied Operations Research II. E51 – 376 Urban Logistics II . E51 – 395 15:40 Break 16:00 Paper Presentations - Parallel Sessions Innovative Cases Studies in Logistics & SCM III . E51 – 372 Urban Logistics III . E51 – 395 Student Paper Competition . E51 – 376 th 17:40 Reception – Samberg Conference Center, Building E52-7 Floor, Salon M One Amherst St., E40-365 Cambridge, MA 02142 617.253.3630 http://scale.mit.edu 2 2016 SCALE LATIN AMERICA CONFERENCE 70 MEMORIAL DR., E51-345, CAMBRIDGE MONDAY & TUESDAY, MARCH 21-22, 2016 Day 2 – Tuesday, March 22 8:00 Breakfast 8:30 Paper Presentations - Parallel Sessions Sustainability I . E51 – 372 General Topics on Logistics & SCM I . E51 – 376 10:10 Break 10:30 Paper Presentations - Parallel Sessions Sustainability II . -

Public Transportation in São Paulo, Brazil: the Development of Railway System

International Journal for Traffic and Transport Engineering, 2016, 6(4): 416 - 430 DOI: http://dx.doi.org/10.7708/ijtte.2016.6(4).05 UDC: 656.342.025.2(81) PUBLIC TRANSPORTATION IN SÃO PAULO, BRAZIL: THE DEVELOPMENT OF RAILWAY SYSTEM Vanessa Meloni Massara1 1University of São Paulo, Brazil Received 10 February 2016; accepted 16 September 2016 Abstract: This paper has the main objective, to show the evolution of passenger transport by railway in the metropolitan area of São Paulo (RMSP), with the central point in the capital city, one of the largest cities in the world with over 12 million inhabitants. At first, the Brazilian plan for urban mobility is presented. After, will be discussed the development of railway system in the RMSP and its six lines, focusing the administrative police until the creation of the Paulista Company of Metropolitan Trains (CPTM) and the gradual increase that reached a record of transported passengers: 3,025,185 on December, 2013. Also will be discussed the evolution of built stations as well as the technical characteristics of trains and the improvements through the traction technology. GHG emissions are addressed, making comparisons with others transports. To finalize, the text will be shown future projects of the “Metropolitan Transport Plan” and the conclusions about the service. Keywords: City of São Paulo, CPTM, railway, urban development, urban mobility. 1. Introduction intends the development of cities through sustainable urban mobility (MdC, 2007). In Brazil, the concern with the improvement and expansion of public transport is growing In Brazil, the Ministry of Cities has been and is based on the concept of urban mobility. -

São Paulo, 131 (88) – Suplemento Diário Oficial Poder Legislativo Sexta-Feira, 14 De Maio De 2021

252 – São Paulo, 131 (88) – Suplemento Diário Oficial Poder Legislativo sexta-feira, 14 de maio de 2021 Ação 2287 - Implantação do Corredor Metropolitano Itapevi - São Paulo - Estruturação parte dos locais para a exploração comercial, disposição de vagas e uma melhor distribuição de novos do Transporte na Região Oeste da RMSP bicicletários, permitindo uma cobertura maior da rede. Foram retirados os bicicletários das linhas 8- Diamante e 9-Esmeralda, que serão concedidas para a iniciativa privada, e o futuro operador decidirá como administrá-los. O traçado do Corredor Metropolitano Itapevi - São Paulo com 22,7 km inicia-se junto à Estação de Auxílio na concepção do chamamento público para apresentar projeto e elaborar estudos para Transferência Itapevi, da CPTM, passando por Jandira, Barueri, Carapicuíba terminando na divisa avaliar o potencial de estímulo à integração modal por modos ativos a partir da implantação de entre Osasco e São Paulo. Futuramente haverá integração com os ônibus municipais de São Paulo no infraestrutura de bicicletas compartilhadas nas estações Hebraica-Rebouças e Santo Amaro, com o Terminal Amador Bueno (Vila Yara). O projeto foi dividido nos seguintes trechos: objetivo de ampliar a mobilidade urbana ao longo da Linha 9-Esmeralda. Posteriormente, a parceria foi Trecho Itapevi – Jandira (5 km) – Trecho entregue desde 2018 em viário compartilhado, promovendo firmada com a empresa Tembici. maior mobilidade aos usuários das linhas intermunicipais e alternativa para evitar os Tratativas com as prefeituras de todas as 23 cidades atendidas pela CPTM para obtenção de dados congestionamentos na região oeste da RMSP. Nessa ligação também foi construída uma passarela e referentes à rede cicloviária local, como projetos, traçados e estudos, de forma entender a dinâmica de ampliada outra.