2017-2022 Philippine Coffee Industry Roadmap

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Managing Shade Coffee

ManagingManaging ShadeShade Caribbean Area CoffeeCoffee Fact Sheet November 2012 An Agroforestry System Shade coffee production in Puerto Rico has experi- enced a resurgence in growth during recent years, after undergoing a dramatic period of deforestation to convert to coffee production under full sun. The re- vival of shade coffee production utilizes a combina- tion of coffee shrubs and shade trees that form a sec- ondary forest. Shade coffee production has been proven to provide environmental benefits such as soil erosion control, water quality and quantity improve- ment, and wildlife habitat. Shade coffee production also provides socioeconomic benefits such as the opportunity to develop other sustainable forest prod- Coffee fruits in process of ripening. ucts, and the reintroduction of traditional jobs and cultural activities for local coffee pickers. are achieved by planting coffee in locations with the most suitable environmental conditions. In Puerto The coffee growing zone in Puerto Rico is located Rico, not all coffee plantations may be located in are- mostly in the humid mountains of the west-central as that are ecologically suitable for coffee growth. section of the “Cordillera Central.” This area is char- Therefore, recreating favorable coffee growing condi- acterized by steep, mountainous topography and a tions may be beneficial for both coffee production cool climate in the humid and wet subtropical forest. and for the environment. The coffee tree or shrub originated in Ethiopia. The For example, the optimum growth temperature for most common species grown in Puerto Rico are the arabica coffee varies from 60° to 65° F. With these Coffea arabica and C. -

2013 September Affair Sets Records! with a Projected Gross Income of $70,000, and Estimated Net Proceeds of Just Over $38,000, This

2013 September Affair Sets Records! With a projected gross income of $70,000, and estimated net proceeds of just over $38,000, this year’s edition of the annual gala event of the Filipino Association is most certainly headed for the record books! A monthly publication of the Filipino Association ‘This is a marvelous record, an astonishing achievement,’ says Maria ‘Bing’ Sakach, 2013 FA- of Greater Kansas City GKC President. Headed by a dynamic and dedicated third th 9810 West 79 Street generation quartet, the celebration also fea- Overland Park, KS 66204 tured not one but three honorary chairs! In addition, the founders and the past chairper- www.filipino-association.org sons of previous September Affairs since 1971 were honored at the event held on September 28, 2013 at the Westin Kansas OCTOBER 2013 City Crown Center Hotel, one of the select VOLUME 45 NUMBER 4 Kevinfew in Bautista,the metro Executive area to winChair and of maintainthe the coveted AAA Four Diamond rating. 2013 September Affair Event Chairs Bernadette In this issue… Kevin Bautista, Executive Chair of the Rabang, Kevin Bautista, Claudette dela Cruz event, said he was thankful for the honorary and Cindy Kulphongpatana pose for a photo) - September Affair chair, major contributors, underwriters, ad- 1 - Shrimp Dinner vertisers and volunteers who helped support the September Affair. ‘We did it again!’ Shrimp Dinner - From the President said Kevin. ‘This year's event raised more 2 When: Held October 12, 2013 - From the Editor than we could ever expect, making it an in- Where: Filipino Cultural Center credible success for our Association. -

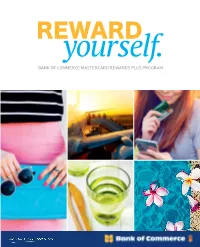

REWARDS PLUS PROGRAM Shopping Dining

Rewayourself.Rd BANK OF COMMERCE MASTERCARD REWARDS PLUS PROGRAM Shopping Dining Rustan’s GC P1,000 Store Specialist, Inc. Points: 19,115 Code: RUGC1K GC P1,000 Red Ribbon GC P500 Figaro Coffee Company Points: 19,115 Code: SSGC1K Points: 11,034 Code: RRGC5H GC P500 Points: 11,034 Code: FIGC5H SM Gift Pass P1,000 Forever 21 Gift Card P1,000 Points: 19,115 Code: SMGC1K Points: 19,115 Code: FOGC1K Jollibee GC P500 The Coffee Bean & Tea Leaf Points: 11,034 Code: JOGC5H GC P500 Points: 11,034 Code: CBGC5H Toys R Us GC P1,000 Robinson’s GC P1,000 Points: 19,115 Code: TUGC1K Points: 19,115 Code: ROGC1K Greenwich GC P500 Bistro Group GC P1,000 Points: 11,034 Code: GRGC5H Points: 19,115 Code: BGGC1K Nike Park GC P1,000 Metro Gaisano GC P1,000 Points: 19,115 Code: NPGC1K Points: 19,115 Code: MGGC1K Gerry’s Restaurant & Bar Sambokojin GC P1,000 GC P1,000 Points: 19,115 Code: SKGC1K S&R GC P1,000 Abenson GC P1,000 Points: 19,115 Code: GGGC1K Points: 19,115 Code: SRGC1K Points: 19,115 Code: ABCG1K Dad’s, Kamayan, Makati Shangri-La Circles National Book Store Saisaki GC P1,000 Event Cafe GC P2,000 GC P1,000 Points: 19,115 Code: DKGC1K Points: 35,400 Code: SHGC2K Points: 19,115 Code: NBGC1K Annual Air Miles Membership Fee Waiver 1,000 PAL Mabuhay Miles Classic Principal P1,200 Points: 15,000 Code: AMCP01 Card Type Points Code Classic Card 12,000 PALCL1 Gold Card 12,000 PALGO1 Classic Supplementary P600 Platinum Card 6,000 PALPL1 Points: 7,500 Code: AMCS02 Gold Principal P2,500 Points: 31,250 Code: AMGP01 500 GetGo Points Card Type Points Code Classic Card 6,000 GTGOCL Gold Card 6,000 GTGOGO Gold Supplementary P1,250 Points: 15,625 Code: AMGS02 Platinum Card 3,000 GTGOPL Points Required Code Shopping Rustan’s GC P1,000 19,115 RUGC1K Terms and Conditions Store Specialist, Inc. -

Coffee Production Costs and Farm Profitability: Strategic Literature Review

A Specialty Coffee Association Research Report Coffee Production Costs and Farm Profitability: Strategic Literature Review Dr Christophe Montagnon, RD2 Vision October 2017 Coffee Production Costs and Farm Profitability | Specialty Coffee Association Contents: 1)! Introduction 2)! Methodology: Document selection 2.1) Reviewing method 3)! Document comparison: Raw data collection 3.1) Variable and fixed costs 3.2) Family labor and net income 3.3) Distinguishing between averaged farms and different farm types 3.4) Focus on the Echeverria and Montoya document 3.5) Yield, profitability and production costs across Colombian regions in 2012 3.6) Correlating yield, profitability and production costs 3.7) Agronomic factors impacting yield, profitability and production costs 4)! Conclusions: Meta-analysis of different studies 4.1) Valuing the cost of production and profitability across different documents 4.2) Relationship between profitability, cost per hectare, cost per kg and yield 4.3) Main conclusions of the meta-analysis 4.4) Causes of household food insecurity 4.5) Limitations and recommendations of this literature review 5)! Next steps: Taking a strategic approach 6)! Annexes 7)! Glossary of terms List of tables Table 1: Grid analysis of reviewed documents Table 2: Description of the different reviewed documents according to the grid anlysis Table 3: Description of different coffee farm types (clusters) in Uganda Table 4: Yield, profitability and coffee costs in different regions of Colombia Table 5: Correlations between yield, profitability -

Universidade De São Paulo

UNIVERSIDADE DE SÃO PAULO FACULDADE DE FILOSOFIA, LETRAS E CIÊNCIAS HUMANAS DEPARTAMENTO DE SOCIOLOGIA PROGRAMA DE PÓS-GRADUAÇÃO EM SOCIOLOGIA A Universidad de los Andes e o estabelecimento da Frente Nacional Colômbia, 1948 - 1968 PAOLA GIRALDO - HERRERA V. 1 [versão corrigida] São Paulo 2013 UNIVERSIDADE DE SÃO PAULO FACULDADE DE FILOSOFIA, LETRAS E CIÊNCIAS HUMANAS DEPARTAMENTO DE SOCIOLOGIA PROGRAMA DE PÓS-GRADUAÇÃO EM SOCIOLOGIA A Universidad de los Andes e o estabelecimento da Frente Nacional Colômbia, 1948 - 1968 Paola Giraldo - Herrera Tese apresentada ao Programa de Pós- Graduação em Sociologia do Departamento de Sociologia da Faculdade de Filosofia, Letras e Ciências Humanas da Universidade de São Paulo, para a obtenção do título de Doutora em Sociologia. [versão corrigida] Orientador: Prof. Dr. Sedi Hirano São Paulo 2013 Página | 2 Resumo Esta pesquisa explora o papel da Universidad de Los Andes (Uniandes) de Bogotá, Colômbia, na constituição do regime de coalizão conhecido como Frente Nacional (1958- 1978). Combinando a revisão do arquivo do conselho diretivo da Uniandes com a reconstrução das trajetórias e redes de contato dos seus membros, esboça-se aqui um mapa do campo do poder no período entre a fundação da universidade (1948) e a consolidação da Frente Nacional. Nesta tese é desenvolvida uma análise das elites colombianas e da utilização da educação superior como mecanismo de reorganização do campo político colombiano em um contexto de reivindicações sociais. Educação superior, Elites, Colômbia século XX, Universidad de Los Andes, regime da Frente Nacional Resumen Esta investigación explora el papel de la Universidad de los Andes (Uniandes, 1948), Bogotá, Colombia, en el proceso de conformación del régimen de coalición conocido como Frente Nacional (1958- 1978). -

Lavazza Annual Report ENG.Pdf

ANNUAL REPORT 2019 COMPANY OFFICERS - GROUP STRUCTURE COMPANY OFFICERS GROUP STRUCTURE BOARD OF DIRECTORS Chairman Alberto Lavazza LUILUGIIGI LAVA LAVAZZAZZA S.p.A .S .p.A. CONTENTS Vice Chairmen Giuseppe Lavazza Marco Lavazza Company Officers Chief Executive Officer Antonio Baravalle LAVAZZA LAVAZZA OTHER BRAND OTHER SERVICE PROFESSIONAL SUBSIDIARIES SUBSIDIARIES SUBSIDIARIES COMPANIES Group Structure SUBSIDIARIES Directors Antonella Lavazza Francesca Lavazza 100% 97,3% 80% 100% 99% Directors’ Single Report on Operations LAVAZZA PROFESSIONAL NIMS S.p.A. KICKING HORSE LAVAZZA TRADING COFINCAF S.p.A. Manuela Lavazza HOLDING EUROPE S.r.l. COFFEE Co. Ltd SHENZHEN Co. Ltd Pietro Boroli 100% 100% 100% 100% Gabriele Galateri di Genola 93% LAVAZZA PROFESSIONAL LAVAZZA PREMIUM CARTE NOIRE LAVAZZA SPAGNA LAVAZZA CAPITAL Robert Kunze-Concewitz (UK) Ltd COFFEES Corp. S.a.s. S.L. S.r.l. LAVAZZA GROUP Antonio Marcegaglia 100% LPCC Canadian 100% 100% 100% Consolidated Financial Statements LAVAZZA PROFESSIONAL Branch CARTE NOIRE LAVAZZA MAROC IMMOBILIARE I.N.N.E.T. FRANCE S.a.s OPERATIONS S.a.r.l. S.r.l. at 31 December 2019 S.a.s. BOARD OF STATUTORY AUDITORS 100% 100% 100% LAVAZZA PROFESSIONAL LAVAZZA KAFFEE MERRILD KAFFE Accounting Statements GERMANY G.m.b.H . G.m.b.H. ApS Chairman Gianluca Ferrero 100% 100% 100% Consolidated Statement of Financial Position LAVAZZA PROFESSIONAL LAVAZZA DEUTSCHLAND MERRILD BALTICS Statutory Auditors Angelo Gilardi HOLDING NORTH AMERICA G.m.b.H. SIA Consolidated Statement of Profit or Loss Inc. Bernardo Bertoldi 100% 100% Consolidated Statement of Comprehensive LAVAZZA PROFESSIONAL LAVAZZA FRANCE Income NORTH AMERICA LLC S.a.s. Consolidated Statement of Cash Flows INDEPENDENT AUDITORS LPNA Canadian 100% Branch LAVAZZA SWEDEN AB Consolidated Statement of Changes in Equity EY S.p.A. -

Ten Years of the Nescafé Plan Ay S D Ta R R U T

TEN YEARS OF THE NESCAFÉ PLAN RTS 2 A A T S H Y T A I D W R U R O Y E T B E T SINCE THE LAUNCH OF THE NESCAFÉ PLAN iN 2010 A lot of love went into the cup of coffee in your hands: nurturing the soil, growing the tree, protecting it from climate change. A lot of energy was poured into things you can’t taste: nurturing the community, growing women’s roles, protecting children and workers. A lot of people did things you can’t see: nurturing hope, growing incomes, protecting the environment. A lot of voices discussed things you haven’t heard yet. So, we asked them why they think your day starts better with a cup of respect. And this is what they said… 3 CONTENTS 5 6 9 12 14 16 FOREWORD THE NESCAFÉ STORY: THE NESCAFÉ PLAN: RESPECT A DECADE TEN YEARS OF Magdi Batato STIRRING SUCCESS A COMMITMENT TO OF PROGRESS THE NESCAFÉ PLAN & David Rennie SUSTAINABLE COFFEE AROUND THE WORLD 21 30 34 41 46 52 IMPACT A CUP WITH TRUST DISCOVERY SUPPORT A CUP WITH AN EXPERT: AN EXPERT: Chris Wille Carlos Brando 55 60 68 74 78 83 THE BUSINESS WOMEN FARMERS COLLABORATION TEN YEARS LOOKING AHEAD OF FARMING IN COFFEE OF THE FUTURE OF LEARNING: Philipp Navratil A PERSONAL REFLECTION Marcelo Burity 4 FOREWORD A MILESTONE ON OUR Every year, Nescafé supports around 100,000 coffee These achievements (and many others) would not farmers and buys more than 800,000 metric tons have been possible without our outstanding and of green coffee – more than 13 million bags, from dedicated teams – both past and present – who more than 20 countries. -

Breads and Dips Olives Greek Starters

Breads and Dips EatEat----inininin TakeTake----awayaway 001 Pitta Bread £1.00 / £5.00 (5pk) £0.80 / £4.00 (5pk) 002 Garlic Pitta Bread £1.20 / £6.00 (5pk) £1.00 / £5.00 (5pk) 003 Melitzanosalata (a smoked aubergine dip) £3.50 (150g) £3.00 (150g) 004 Tzatziki (yoghurt, cucumber & garlic dip) £3.50 (150g) £3.00 (150g) 005 Homous (chickpeas with olive oil, parsley, lemon & garlic) £3.50 (150g) £3.00 (150g) 006 Strofilia (feta cheese with chilli peppers & olive oil) £3.50 (150g) £3.00 (150g) 007 Olive Paté (olives, sun dried tomatoes, garlic & olive oil) £3.70 (150g) £3.20 (150g) 008 Dips Meze (serves 2 people) (tzatziki, homous, strofilia & olive paté) £8.40 (400g total) £7.90 (400g total) OliveOlivessss EatEat----inininin TakeTake----awayaway 009 Marinated kalamata olives £3.50 (130g) £3.00 (130g) 010 Pitted kalamata olives £3.50 (130g) £3.00 (130g) 011 Marinated green queen olives £3.50 (130g) £3.00 (130g) 012 a Green olives stuffed with feta £3.50 (130g) £3.00 (130g) 012b Green olives stuffed with sun dried tomatoes £3.50 (130g) £3.00 (130g) 012c Green olives stuffed with garlic £3.50 (130g) £3.00 (130g) 012d Green olives stuffed with almonds £3.50 (130g) £3.00 (130g) 012e Green olives stuffed with chilli £3.50 (130g) £3.00 (130g) Greek StarterStarterssss EatEat----inininin TakeTake----awayaway 013 Stuffed Vine Leaves (with rice & herbs) £4.60 (200g) £4.10 (200g) 014 Stuffed Tomatoes (with beef, pork mince, rice & feta) dairy free upon request £4.60 each £4.10 each 014a Stuffed Tomatoes (with vegetables, rice, herbs & feta) dairy free -

Appetizer Soup Salads

APPETIZER SALADS Nurture Spring Roll Nurture Salad Golden fried spring roll stuffed with heart of Kale, mesclun lettuce, wild herbs, kesong puti, palm and wrapped in lettuce and basil leaves roasted cashew nuts, balsamic vinaigrette P220 P230 Bruschetta Farm Salad Homemade bread, tomatoes, olive oil and Garden greens, kale, herbs, tofu croutons, fresh herbs tomato, green mango, cucumber, oriental P200 dressing P230 Mushroom Tempura Fresh oyster mushroom deep in beer Skinny Caesar batter P200 Romaine lettuce with our famous eggless caesar dressing, croutons and parmesan Kakaibang Lumpia shaving Stuffed with smoked mackerel, green mango P230 and cheese served with sweet chili sauce P200 Fresh Garden Wrap Fresh vegetables wrapped in kale leaves, lettuce, wild herbs, kesong puti, roasted SOUP cashew nuts, P230 Tomato Basil Our take on the famous Italian soup with tomato and basil picked from our garden P170 Roasted Pumpkin Soup finished with curries P170 Tinola Mushroom Soup The essence of a traditional Filipino soup with a vegetarian twist: oyster mushrooms P170 Potato leek Traditional European soup P170 Sweet Potato and Carrot Soup A classic comfort superfood soup P170 All prices are inclusive of government taxes and service charge. September 2020 MAIN ENTREE Asian Garden Curry Pork Binagoongan Lemongrass, ginger, turmeric curry paste, Pork slices slowly simmered in shrimp paste sautéed oyster mushrooms, fried tofu, P420 garden vegetables, organic rice P280 Gabriela’s Bulalo Calderetang Osso Bucco Regional cuisine slowly simmered Batangas Batangas style caldereta of beef shank in beef until tender, served with vegetables liver sauce P730 P480 English Fish and Wedges Beef Steak Tagalog Golden fried beer battered mahi-mahi with Beef strips cooked in soy sauce, calamansi hand cut wedges served with tartar sauce and onions P400 P380 Moroccan Chicken 150g grilled chicken breast, coated in various Mediterranean spices. -

Intellectual Property Center, 28 Upper Mckinley Rd

Intellectual Property Center, 28 Upper McKinley Rd. McKinley Hill Town Center, Fort Bonifacio, Taguig City 1634, Philippines Tel. No. 238-6300 Website: http://www.ipophil.gov.ph e-mail: [email protected] Publication Date < April 29, 2019 > 1 ALLOWED MARKS PUBLISHED FOR OPPOSITION .................................................................................................... 2 1.1 ALLOWED NATIONAL MARKS .............................................................................................................................................. 2 Intellectual Property Center, 28 Upper McKinley Rd. McKinley Hill Town Center, Fort Bonifacio, Taguig City 1634, Philippines Tel. No. 238-6300 Website: http://www.ipophil.gov.ph e-mail: [email protected] Publication Date < April 29, 2019 > 1 ALLOWED MARKS PUBLISHED FOR OPPOSITION 1.1 Allowed national marks Application No. Filing Date Mark Applicant Nice class(es) Number 8 January 1 4/2010/00000291 PEARLIE WHITE CORLISON PTE. LTD. [SG] 3 2010 23 SAN MIGUEL FOOD AND 2 4/2016/00015617 December RED DRAGON NOVA BEVERAGE, INC. 30 2016 [PH] 14 July 3 4/2016/00503478 ALFAGRES ALFAGRES S.A. [CO] 27 2016 15 4 4/2016/00506493 December FILTER PROTECT Philip Morris Brands Sàrl [CH] 34 2016 19 January ELI LILLY AND COMPANY 5 4/2017/00000811 HUMAPEN 10 2017 [US] 3 March DMCI PROJECT 6 4/2017/00003063 ALEA RESIDENCES 36 and37 2017 DEVELOPERS, INC. [PH] 13 March GRUPO BIMBO S.A.B. DE 7 4/2017/00003682 SANISSIMO 100 30 2017 C.V. [MX] 20 April 8 4/2017/00006020 SPARTAN GENEVA FOOD INC. [PH] 30 2017 8 June CLEVELAND 9; 16; 18; 25; 28 9 4/2017/00008888 NBA Properties, Inc. [US] 2017 CAVALIERS and41 Jerry. M. Tiu [PH]; Stanley S. 15 June 10 4/2017/00009196 AERO TECH Ching [PH] andJian Xiong 12 2017 Liang [PH] 11 4/2017/00010369 3 July 2017 STAR ORSOLA INC. -

Kapeng Barako Coffee Liqueur

what’s inside? R&D Notes: Farm repurposed into novel products > 4 Cacao: Food of the gods turned into wine > 6 Kapeng Barako Coffee Liqueur: Keeping the spirit of Batangas Coffee > 8 Sweet success from Queen Pineapple vinegar >12 Maize Silky Sip: Your diuretic juice fix >14 Ice cream cone made from Adlay >16 Kapis chips: A nutritious finger food from the sea >18 Goat meat on-the-go >20 Feeding your skin with coffee >22 SalOkra: Wonder-duo for health and wellness >26 This magazine is copyrighted by the Department of Agriculture-Bureau of Agricultural Research. No parts of this publication may be reproduced and distributed without the permission from the management and proper attributions from its original source. BAR R&D Digest is the official quarterly publication of the Department of Agriculture-Bureau of Agricultural Research (DA-BAR). A staff bureau of DA, it PRODUCTION TEAM was established to lead and coordinate the agriculture and fisheries research and development (R&D) in the country. Specifically, BAR is tasked to consolidate, Editor and Layout: Rita T. dela Cruz strengthen, and develop the R&D system to improve its effectiveness and efficiency Consulting Editors: Julia A. Lapitan and Victoriano B. Guiam by ensuring customer satisfaction and continous improvement through work Writers: excellence, teamwork and networking, accountability and innovation. Daryl Lou A. Battad, Rita T. dela Cruz, Leoveliza C. Fontanil, Ephraim John J. Gestupa, Rena S. Hermoso, Victoriano B. Guiam, and This publication contains articles on the latest technologies, research results, Patrick Raymund A. Lesaca updates, and breakthroughs in agriculture and fisheries R&D based from the studies Print Manager: Ricardo G. -

The Coffee Bean: a Value Chain and Sustainability Initiatives Analysis Melissa Murphy, University of Connecticut, Stamford CT USA Timothy J

The Coffee Bean: A Value Chain and Sustainability Initiatives Analysis Melissa Murphy, University of Connecticut, Stamford CT USA Timothy J. Dowding, University of Connecticut, Stamford CT USA ABSTRACT This paper examines Starbucks’ corporate strategy of sustainable efforts in Ethiopia, particularly in the sustainable sourcing Arabica coffee. The paper discusses the value chain of coffee, issues surrounding the coffee supply chain and the need for sustainable coffee production. In addition it also discusses Starbucks’ position and influence on the coffee trade, and the measures that Starbucks is taking to ensure sustainability efforts throughout the coffee supply chain. COFFEE VALUE CHAIN & P3G ANALYSIS Coffee is produced in more than fifty developing countries in Latin America, Africa, and Asia and it is an important source of income for 20-25 million families worldwide [1]. The initial production of coffee beans including farming, collecting, and processing is labor intensive and as a result is performed in more labor abundant developing countries. The roasting and branding of coffee is more capital intensive and therefore is situated in northern industrialized countries. The top five coffee consumers are United States of America, Brazil, Germany, Japan, and France [1]. The structure of the value chain is very similar regardless of producing or consuming country. The coffee value chain is made up of the four main phases: Cultivation, Processing, Roasting, and Consumption. Each phase in the process has environmental, social, economic