Public-Private Partnerships for Real Estate Development: Beyond Bridges and Roads

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Updated 1.3.17 No Boxes.Indd

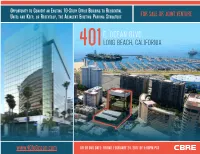

OPPORTUNITY TO CONVERT AN EXISTING 10-STORY OFFICE BUILDING TO RESIDENTIAL FOR SALE OR JOINT VENTURE UNITS AND KEEP, OR REDEVELOP, THE ADJACENT EXISTING PARKING STRUCTURE E. OCEAN BLVD. 401 LONG BEACH, CALIFORNIA www.401eOcean.com OFFER DUE DATE: FRIDAY, FEBRUARY 24, 2017 BY 5:00PM PST FOR SALE OR JOINT VENTURE PLEASE DO NOT DISTURB OR CONTACT TENANTS for more information contact: Laurie Lustig-Bower Executive Vice President Lic. 00979360 310.550.2556 [email protected] Gary Stache Executive Vice President Lic. 00773736 949.725.8532 [email protected] Kadie Presley Wilson Senior Sales Director Lic. 01476551 310.550.2575 [email protected] OFFER DUE DATE: FRIDAY, FEBRUARY 24, 2017 BY 5:00PM PST www.401eOcean.com © 2017 CBRE, Inc. The information contained in this document has been obtained from sources believed reliable. While CBRE, Inc. does not doubt its accuracy, CBRE, Inc. has not verified it and makes no guarantee, warranty or representation about it. It is your responsibility to independently confirm its accuracy and completeness. Any projections, opinions, assumptions or estimates used are for example only and do not represent the current or future performance of the property. The value of this transaction to you depends on tax and other factors which should be evaluated by your tax, financial and legal advisors. You and your advisors should conduct a careful, independent investigation of the property to determine to your satisfaction the suitability of the property for your needs. Pacific Ocean east ocean boulevard -

Belmont Plaza Olympic Pool to Be Demolished

Volume 23, No. 2, Spring 2013 Belmont Plaza Olympic Pool to Be Demolished The Belmont Plaza in 2012 another study determined that the natato- Olympic Pool complex rium might not be reparable after an earthquake was built in 1967 in measuring five magnitude or higher. This building, anticipation of the which measures 224’x148,’ was constructed with a 1968 Olympic trials. shear-wall frame, cast in place reinforced concrete columns, and prestressed concrete girders. It has a 23’ high glass curtain wall below a 25’ high precast concrete shear wall. In 1968 this type of construc- tion clearly met the code requirements, but today, more stringent rules are applied to such buildings. According to the latest seismic report, some cracks have appeared in the natatorium and the walls ap- pear to be deteriorating. When completed, the Belmont Pool mea- sured 50 X 75 meters, had eight lanes ranging from 3½ to 12 feet deep, six lifeguard towers equipped with television monitors, and movable plastic pan- PHOTOGRAPHY BY LOUISE IVERS LOUISE BY PHOTOGRAPHY els in the roof that could be opened to allow the By Louise Ivers to the Los Angeles Times, Mark Spitz, Don Schol- sun to shine on the swimmers. A computerized lander, and Charles Hickox set men’s records during scoreboard provided extremely accurate record- In January 1967 plans were approved for a group these trials. During the 1975 Olympic development ing of athletes’ prowess. Bleachers seated 3,500 of structures at Belmont Plaza, a site west of the meet, Shirley Babashoff took first place in the 400 spectators and a press box with the most modern pier on the beach in Belmont Shore. -

Element City of Long Beach General Plan

LAND USEelement City of Long Beach General Plan August 2016 creating vibrant and exciting places LONG BEACH DEVELOPMENT SERVICES BUILDING A BETTER LONG BEACH “Growth is inevitable and desirable, but destruction of community character is not. The question is not whether your part of the world is going to change. The question is how.” Edward T. McMahon The Conservation Fund land use City of Long Beach LAND USEelement of the City’s General Plan Adopted by the City Council on ____________ Prepared by Long Beach Development Services Assisted by MIG and Cityworks Design ACKNOWLEDGEMENTS Mayor and City Council Honorable Mayor Robert Garcia Lena Gonzalez, Councilmember, 1st District Vice Mayor Suja Lowenthal, Councilmember, 2nd District Suzie Price, Councilmember, 3rd District Daryl Supernaw, Councilmember, 4th District Stacy Mungo, Councilmember, 5th District Dee Andrews, Councilmember, 6th District Roberto Uranga, Councilmember, 7th District Al Austin, Councilmember, 8th District Rex Richardson, Councilmember, 9th District Office of the City Manager Patrick H. West, City Manager Tom Modica, Assistant City Manager Arturo M. Sanchez, Deputy City Manager City of Long Beach Planning Commission Alan Fox, Chair Mark Christoffels, Vice Chair Ron Cruz Andy Perez Jane Templin Donita Van Horik Erick Verduzco-Vega City of Long Beach Development Services Staff Amy J. Bodek, AICP, Director Linda F. Tatum, AICP, Planning Manager Christopher Koontz, AICP, Advance Planning Officer Craig Chalfant Ira Brown Fern Nueno, AICP Angela Reynolds, AICP (retired) Pat Garrow (retired) Steve Gerhardt, AICP (retired) Special Thanks A special thanks is extended to the Long Beach Department of Technology Services for their able assistance in the preparation of the maps contained in this document. -

History of Legal Professionals, Incorporated

HISTORY OF LEGAL PROFESSIONALS, INCORPORATED (Rev. 5/1/2020) AD HOC HISTORY COMMITTEE 1982: CATHARINE RYAN, PLS, Chairman, San Francisco LSA HELEN G. BANGS, Orange County LSA DARLENE JONES, Glendale-Burbank LSA JUDITH SCHNITZER, Long Beach LSA Revised: 1986 - RHODA C. SPENCER, PLS, CCLS, LSI Executive Advisor 1993 - CAROLINE E. VAN DE POL, PLS, CLA/CAS, CCLS LSI Executive Advisor 1996 - CHERYL WOODSON, CCLS LSI Executive Advisor 1997 - LINDA DUARTE LSI Executive Advisor 2000 - DEANNA A. PEPE, CCLS, PLS LSI Executive Advisor 2002 - PATRICIA E. MILLER, PLS, CCLS LSI Executive Advisor 2004 - YVONNE WALDRON-ROBINSON, CCLS LSI Executive Advisor 2006 - KAY J. THORNBURG LSI Executive Advisor 2008 - MARY S. ROCCA, CCLS LSI Executive Advisor 2010 - LORRAINE BETTEN COURT, PLS, CCLS LSI Executive Advisor 2012 - CHRISTA DAVIS LSI Executive Advisor 2014 – SANDRA T. JIMENEZ, CCLS LSI Executive Advisor 2016 – MARY J. BEAUDROW, CCLS LSI Executive Advisor 2019 – JENNIFER L. PAGE, CCLS LSI Executive Advisor Dedicated to The members of LEGAL SECRETARIES, INCORPORATED Dedication made in 1982 under the direction of JOAN M. MOORE, PLS, CCLS LSI President 1980-1982 (Rev. 5/1/2020) TABLE OF CONTENTS Title Page Number Preface..............................................................................................................................................4 California Associations ....................................................................................................................5 Past Presidents .................................................................................................................................8 -

Master Inventory of Millard Sheets Studio and Home Savings Art and Architecture-Published Version August 2018.Xlsx

Master Inventory of Millard Sheets Studio and Home Savings Art and Architecture-Published Version August 2018.xlsx Branch Name Owner Date Acquired Art Construction Branch (if different before Date Last Stained Fabric Painted Archival Firm Address City State or Opened Date Location Closed Number than city) Home Status Seen Mosaic? Glass? Sculpture? work? Furnishings? mural? No Art? Subject(s) Worked On By Records Copyright 2018 by Adam Arenson - please use to support documentation and preservation efforts, crediting the source. South Pasadena Junior High frescoes - School 1500 Fair Oaks Avenue South Pasadena CA 1929 1929 destroyed by 1935 Y California Millard Sheets (Unknown Name) beach club Long Beach CA before 1932 1930 Millard Sheets, Phil Dike (date and Scripps College Art Building Claremont CA 1930 specifics before 1932, before 1932, likely destroyed before Sheets Robinson’s Company Los Angeles CA likely 1929-1932 1929-1932 1975 Y Y Fantasie Millard Sheets exhibit State Mutual Building and before 1932, before 1932, likely AAA- Loan Los Angeles CA likely 1929-1932 1929-1932 Y Millard Sheets Millard before 1932, before 1932, likely Sheets YMCA Pasadena CA likely 1929-1932 1929-1932 Y exhibit covered then Modern Bullock’s Men’s Store 640 S Hill St Los Angeles CA 1934 1934 uncovered in 1975; Y World Millard Sheets mural in Beverly Hills Hotel 9641 Sunset Blvd Beverly Hills CA 1935 main lobby: Millard Sheets (date and Beverly Hills Tennis Club 340 North Maple Drive Beverly Hills CA 1935 not there, if ever 2014 Y specifics Millard Sheets -

I UNIVERSITY of CALIFORNIA RIVERSIDE the “Stylish Battle

UNIVERSITY OF CALIFORNIA RIVERSIDE The “Stylish Battle" World War II and Clothing Design Restrictions in Los Angeles A Dissertation submitted in partial satisfaction of the requirements for the degree of Doctor of Philosophy in History by Laura Bellew Hannon December 2012 Dissertation Committee: Dr. Catherine Gudis, Chairperson Dr. Molly McGarry Dr. Susan Carter i Copyright by Laura Bellew Hannon 2012 ii The Dissertation of Laura Bellew Hannon is approved: __________________________________________________________________ __________________________________________________________________ __________________________________________________________________ Committee Chairperson University of California, Riverside iv ACKNOWLEDGEMENTS This Dissertation, as written, would not have been possible without the support of many. Research funding was partially supported by the Graduate Division of the University of California, Riverside in the form of the Dissertation Year Fellowship. I am also, without question, indebted to the Costume Society of American for their exceptional support. As the recipient of the Stella Blum Student Research Award, I received funding which allowed me to research my dissertation at the Costume Institute of the Metropolitan Museum of Art, the Archives of the Fashion Institute of Technology, the Manuscript and Archives Division of the New York Public Library, and the Margaret Herrick Library of the Academy of Motion Picture Arts and Sciences. I also received funding to attend the National Symposium of the CSA in Boston in May 2011, and there received many suggestions and much needed encouragement. Additionally, through the Western Regional Branch of the Costume Society, I received the Jack Hanford Summer Internship Award. I received the funding to support a summer-long internship at the Los Angeles County Museum of Art during which I learned much about the history of western fashion and had the ability to research my own project. -

City of Long Beach Historic Context Statement

City of Long Beach Historic Context Statement Prepared for: City of Long Beach Department of Development Services Office of Historic Preservation 333 West Ocean Boulevard Long Beach, California 90802 Prepared by: Sapphos Environmental, Inc. 430 North Halstead Street Pasadena, California 91107 July 10, 2009 TABLE OF CONTENTS SECTIONS PAGE 1.0 INTRODUCTION .............................................................................................................. 5 1.1 Objectives and Scope............................................................................................. 5 1.2 Working Definitions............................................................................................... 6 1.3 Report Preparation ................................................................................................. 8 1.4 Historic Context Statement Organization................................................................ 8 2.0 LOCATION...................................................................................................................... 10 3.0 STUDY METHODS.......................................................................................................... 14 3.1 Historical Research............................................................................................... 14 3.2 Previous Surveys................................................................................................... 15 3.3 Field Reconnaissance........................................................................................... -

Women's Opportunity Week Opening Ceremony Office of Publicnfor I Mation

University of San Diego Digital USD News Releases USD News 1982-10-11 Women's Opportunity Week Opening Ceremony Office of Publicnfor I mation Follow this and additional works at: http://digital.sandiego.edu/newsreleases Digital USD Citation Office of Public Information, "Women's Opportunity Week Opening Ceremony" (1982). News Releases. 3027. http://digital.sandiego.edu/newsreleases/3027 This Press Release is brought to you for free and open access by the USD News at Digital USD. It has been accepted for inclusion in News Releases by an authorized administrator of Digital USD. For more information, please contact [email protected]. University of San Die8o PUBLIC RELATIONS October 11, 1982 Re: Women's Opportunity Week Opening Ceremony Dear Most Reverend Maher Recently, Public Relations Director Sara Finn presented the University of San Diego's Board of Trustees a plan con cerning Women's Opportunity Week at Fashion Valley during the week of October 18-22. This "discovery" event is being coordi nated by member s of USD Alcala ~omen's Club, a newly-formed service oriented group on campus. Attached is the schedule of speakers for the upcoming event. We especially look forward to the christening of SHIPSHAPE, COURTSHIP, and SCHOLARSHIP by President Author Hughes on Monday, October 18, at 2:00 p.m. We want to personally invite you to this opening ceremony, as well as to all the week-long presentations by USD faculty and administration. Thank you for your time and support. ~~ Sharon Dudek & Maria Brightbill Co-Chairpersons for W.O.W. Alcala Park, San Diego, California 92110 714/291-6480 Welcome Aboard USD'S Place: Fashion Valley Mall D ate: October 18-22 Discovery Ships! Time: I p.m. -

Are Retailing Mergers Anticompetitive? an Event Study Analysis

Are Retailing Mergers Anticompetitive? An Event Study Analysis Abstract We examine the abnormal returns of rival firms to determine whether four retailing mergers that occurred during the late 1980s reduced competition. We use the stock returns of retailers in geographic markets unaffected by the merger to control for the efficiency-signaling effect of the merger. Using this methodology, we find that rival firms experienced positive abnormal returns from May Company’s 1986 acquisition of Associated Dry Goods and American Stores’ 1988 acquisition of Lucky Stores. These results offer some evidence that retailing mergers that lead to large increases in concentration in already concentrated markets may lessen competition and lead to higher product market prices. John David Simpson Federal Trade Commission and Daniel Hosken Federal Trade Commission January 1998 I) Introduction Antitrust enforcement of retailing mergers has varied over time. In the 1960s, the antitrust agencies and the courts pursued a very aggressive antitrust policy. For example, the Supreme Court blocked a 1960 merger between Von’s Grocery and Shopping Bag Food Stores that would have given the merged firm a 7.5 percent share of the grocery retailing business in Los Angeles.1 In contrast, the antitrust agencies followed a much more relaxed antitrust policy in the 1980s. For instance, the Federal Trade Commission did not challenge May Department Stores Company’s 1986 acquisition of Associated Dry Goods which would have given the combined firm control of nearly all of the traditional department stores in the Pittsburgh area.2 More recently, the antitrust agencies and the courts have adopted a more moderate position with respect to retailing mergers. -

To Search the Index to the Slides in Series 1

Historical Society of Long Beach Long Beach Redevelopment Agency Collection 1 4260 Atlantic Ave, Long Beach, CA 90807 Series 1 Slide Inventory www.hslb.org 562/424-2220 Object ID # Box Title General Streets(s) and Address(es) Description/Keywords Dates Slide Photogr- # Area(s) # apher(s) 2017.029.001 1A Bank of America, Pine St. Downtown Banks; Pine Street; BoA 1981 9 /Waterfront 2017.029.002 1A Bradley Building, Pine Ave. & Downtown 201-209 Pine Ave. Birdland; Live Jazz Window 1982- 82 3rd St. /Waterfront 1991 2017.029.003 1A Breakers, Ocean Blvd. Downtown 200-220 E. Ocean Blvd. Hilton; Wilton; Breakers International; Hotels 1983- 2 /Waterfront 1984 2017.029.004 1A California Veterans / State Downtown Veterans Affairs; V.A. Hospital; Construction 1981- 49 Office Building /Waterfront 1982 2017.029.005 1A Chamber of Commerce Downtown 1 World Trade Center #1650 Downtown Long Beach; Buildings; Government 1981- 14 /Waterfront 1982 2017.029.006 1A City Centre Building Downtown 200 Pine Ave. Downtown Long Beach; Buildings; Government 1995- 2 Andy /Waterfront 1996 Witherspo on 2017.029.007 1A - City Hall / Civic Center Downtown 333 Ocean Blvd. Downtown Long Beach; Buildings; Government 1981- 86 Peg 1B /Waterfront 2000 Owens, John Robinson 2017.029.008 1B Convention Center Downtown 300 Ocean Blvd. Long Beach Arena; Terrace Theatre; Aerial; Parking Signage; Convention Center Signage; 1978- 103 John /Waterfront Interior; Trade Show 1997 Robinson, Michele and Tom Grimm, G. Metiver 2017.029.009 1B- Crocker Plaza Downtown 180 E. Ocean Blvd. Construction; Bank 1980- 84 1C /Waterfront 1984 2017.029.010 1C Harbor Bank Building Downtown 11 Golden Shore Ave. -

Edward A. Killingsworth Papers, Circa 1940-Circa 2006 0000148

http://oac.cdlib.org/findaid/ark:/13030/kt3h4nf299 No online items Finding Aid for the Edward A. Killingsworth papers, circa 1940-circa 2006 0000148 Finding aid prepared by Chris Marino, Julia Larson The finding aid for this collection was made possible by a Getty Foundation Archival Arrangement & Description Grant. Architecture and Design Collection, Art, Design & Architecture Museum Arts Building Room 1434 University of California Santa Barbara, California, 93106-7130 805-893-2724 [email protected] August 2, 2017 Finding Aid for the Edward A. 0000148 1 Killingsworth papers, circa 1940-circa 2006 000014... Title: Edward A. Killingsworth papers Identifier/Call Number: 0000148 Contributing Institution: Architecture and Design Collection, Art, Design & Architecture Museum Language of Material: English Physical Description: 358.0 Linear feet(65 record storage boxes, 80 flat file drawers, and 18 models) Date (inclusive): circa 1936-circa 2006 Location note: Boxes 1-23/ADC - regular Box 24/ADC - oversize* Boxes 25-53/ADC - regular Box 54/ADC - oversize* Boxes 55-64/ADC - regular 80 Flat File Drawers/ADC - flat files 8 presentation boards/Mosher - box of presentation boards 18 Models/Mosher - models Kuching Hilton Hotel, Kuching Borneo, 1995 UC Riverside, Student Union, 1965 unidentified development Queen Mary access structures Queen Mary access structure, 1978 Hotel (Montego Bay, Jamaica), 1978 Typical Condominium unit for Jamaica Project Apartment building for Syndicated Developers The Kahala Beach (Honolulu, Hawaii) Djakarta Hilton Hotel (Kjakarta, Indonesia) USC, University Religious Center Pacific Terrace Halekulani Hotel (Los Angeles, Calif.) California State University & Colleges, Headquarters Building (Long Beach, Calif.) Atlantic Research Corporation, Missile Systems Division, Offices and factory Hotel for Ernie Hahn (Inglewood, Calif.), 1960 Unidentified resort development creator: Brady, Jules Ellsworth creator: Killingsworth, Brady and Associates . -

Redevelopment of the Westminster Mall

THE WEST END Redevelopment of the Westminster Mall Christopher Cortez City and Regional Planning Page Intentionally Left Blank Approval Page Title The West End Author Christopher Cortez Date Submitted January 2021 Grade:_____ Vicente del Rio, Ph.D. ___________ ____ Signature Date Senior Project Advisor Michael Boswell, Ph.D. ___________ ____ Signature Date Department Head Page Intentionally Left Blank The purpose of this project is to create a redevelopment plan for the Westminster Mall in Westminster, CA that will successfully reinvigorate itself as an active and vibrant center for the city. Redeveloping malls and the property they sit on is a prominent planning issue. Malls are becoming less popular commercial centers and must adapt to fulfill the local community’s needs. This can be accomplished through changes to the volume of commercial space and introducing new land uses, such as multifamily residential and open space, all of which are planning methods. This project will explore how North American Malls, such as Westminster Mall, went from dominating the consumer market to failing. Prime examples of successful mall redevelop- ments will be reviewed and provide guidance for the proposed redevelopment of West- minster Mall. The background on the mall and its location will give insight as to how the property is currently used and how it could potentially be used to benefit the City of Westminster and surrounding communities. Goals, objectives, and design concepts will serve as guidelines as to what is envisioned for this new development and how it can be accomplished. The completed design of the project will fulfill the purpose of this project, to redevelopment the Westminster Mall into a flourishing center.