Current Revitalization Strategy and Initiatives in Downtown Pomona…………….………..…………….56

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

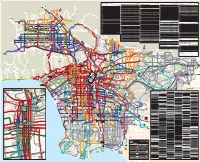

Metro Bus and Metro Rail System

Approximate frequency in minutes Approximate frequency in minutes Approximate frequency in minutes Approximate frequency in minutes Metro Bus Lines East/West Local Service in other areas Weekdays Saturdays Sundays North/South Local Service in other areas Weekdays Saturdays Sundays Limited Stop Service Weekdays Saturdays Sundays Special Service Weekdays Saturdays Sundays Approximate frequency in minutes Line Route Name Peaks Day Eve Day Eve Day Eve Line Route Name Peaks Day Eve Day Eve Day Eve Line Route Name Peaks Day Eve Day Eve Day Eve Line Route Name Peaks Day Eve Day Eve Day Eve Weekdays Saturdays Sundays 102 Walnut Park-Florence-East Jefferson Bl- 200 Alvarado St 5-8 11 12-30 10 12-30 12 12-30 302 Sunset Bl Limited 6-20—————— 603 Rampart Bl-Hoover St-Allesandro St- Local Service To/From Downtown LA 29-4038-4531-4545454545 10-12123020-303020-3030 Exposition Bl-Coliseum St 201 Silverlake Bl-Atwater-Glendale 40 40 40 60 60a 60 60a 305 Crosstown Bus:UCLA/Westwood- Colorado St Line Route Name Peaks Day Eve Day Eve Day Eve 3045-60————— NEWHALL 105 202 Imperial/Wilmington Station Limited 605 SANTA CLARITA 2 Sunset Bl 3-8 9-10 15-30 12-14 15-30 15-25 20-30 Vernon Av-La Cienega Bl 15-18 18-20 20-60 15 20-60 20 40-60 Willowbrook-Compton-Wilmington 30-60 — 60* — 60* — —60* Grande Vista Av-Boyle Heights- 5 10 15-20 30a 30 30a 30 30a PRINCESSA 4 Santa Monica Bl 7-14 8-14 15-18 12-18 12-15 15-30 15 108 Marina del Rey-Slauson Av-Pico Rivera 4-8 15 18-60 14-17 18-60 15-20 25-60 204 Vermont Av 6-10 10-15 20-30 15-20 15-30 12-15 15-30 312 La Brea -

New Mexico State. Poucedepartl11ent .. . an N Nair

If you have issues viewing or accessing this file contact us at NCJRS.gov. ,,' ~ '..' (- .... New Mexico State. PoUceDepartl11ent .. - .. ' . An nnaiR eport19J 6 . " .'~ \" , ' ';- '. , '. r.;. ' NEW MEXICO STATE POLICE DISTRICTS Captain Frank Lucero Captain C. P.Anaya ' CommlUlder ~ District 01 Commander - District 07 P. O. Box, 1628 P. O. DrawerD Santa Fe, N. M. 87501 Esp:mola, N.M. 87532 827-2551 753-4277 Captain J. D. Mae.s Captain M. A. Matteson Command!:r • District 02 Commander - District' 08 P. O. Box 497 P .. O. Box 716 La$ Vegas, N. M. 87701 Alamogordo,N. M. 88310 425-6771 437-1313 Captain FIoyd Miles Captain A. C. Jones Commander -' District 03 Commander • District 09 P. O. Box 760 812 West 6th Street Roswell, N. M. 88201 Clovi~, N. M. $8101 622-7200 763-3426 Captain W. J. Kruse Captain R. J. McCool Commande~ ~ District 04 Commander - District 10 3000 E, University P.D. Box 1049 Las Cruces, N. M. 88001 Farmington, N. M. 87401 522-2222 n5-7547 Captain MelVin West CaptaIn S. Doitchinoff Commander - District 05 Commander • District 11 2501 . Carlisle .BlVd., N~ E. P. a.Box. 1455 Albuquerque, N. M. 87110 Socorro,. N. M. 87801 842-3082 835-0741 Captain M. L. Cordova Captain Otis A •.. Haley Commander - District 06 Commander- District 12 P. O. BoX 490 P. O. Box 566 Gnllup, N. M. 87301 Hobbs, N. M.88240 863-9353 392-5588 JAN 0 111978 GOVERNOR JERRY APODACA NEW MEXICO STATE POllCr; NEW MEXICO STATE POLICE DEPARTMENT ORGANllA1'lONAL CHART 1976 ANNUAL REPORT NEW Mr;XICO STATE'POLICE BOARD TABLE OF CONTENTS PAGE Dr. -

Executive Order 9066 and the Residents of Santa Cruz County

Executive Order 9066 and the Residents of Santa Cruz County By Rechs Ann Pedersen Japanese American Citizens League Float, Watsonville Fourth of July Parade, 1941 Photo Courtesy of Bill Tao Copyright 2001 Santa Cruz Public Libraries. The content of this article is the responsibility of the individual author. It is the library’s intent to provide accurate information, however, it is not possible for the library to completely verify the accuracy of all information. If you believe that factual statements in a local history article are incorrect and can provide documentation, please contact the library. 1 Table of Contents Introduction Bibliography Chronology Part 1: The attack on Pearl Harbor up to the signing of Executive Order 9066 (December 7, 1941 to February 18, 1942) Part 2: The signing of Executive Order 9066 to the move to Poston (February 19, 1942 to June 17, 1942) Part 3: During the internment (July 17, 1942 to December 24, 1942) Part 4: During the internment (1943) Part 5: During the internment (1944) Part 6: The release and the return of the evacuees (January 1945 through 1946) Citizenship and Loyalty Alien Land Laws Executive Order 9066: Authorizing the Secretary of War to Prescribe Military Areas Fear of Attack, Fear of Sabotage, Arrests Restrictions on Axis Aliens Evacuation: The Restricted Area Public Proclamation No. 1 Public Proclamation No. 4 Salinas Assembly Center and Poston Relocation Center Agricultural Labor Shortage Military Service Lifting of Restrictions on Italians and Germans Release of the Evacuees Debate over the Return of Persons of Japanese Ancestry Return of the Evacuees 2 Introduction "...the successful prosecution of the war requires every possible protection against espionage and against sabotage." (Executive Order 9066) "This is no time for expansive discourses on protection of civil liberties for Japanese residents of the Pacific coast, whether they be American citizens or aliens." Editorial. -

Military and Veterans' Affairs Committee

MILITARY AND VETERANS' AFFAIRS COMMITTEE 2012 INTERIM FINAL REPORT New Mexico Legislature Legislative Council Service 411 State Capitol Santa Fe, New Mexico 87501 MILITARY AND VETERANS' AFFAIRS COMMITTEE 2012 INTERIM FINAL REPORT TABLE OF CONTENTS 2012 Interim Summary 2012 Work Plan and Meeting Schedule Agendas Minutes Endorsed Legislation 2012 INTERIM SUMMARY MILITARY AND VETERANS' AFFAIRS COMMITTEE 2012 INTERIM SUMMARY The Military and Veterans' Affairs Committee held five meetings in 2012. The committee focused on many areas affecting veterans and military personnel, including: (1) housing issues; (2) family and community support; (3) treatment options for posttraumatic stress disorder (PTSD); and (4) opportunities at educational institutions around the state. Don Arnold, a United States Department of Veterans Affairs (VA) prior approval lender and veteran advocate, gave a presentation to the committee on the problems some veterans are having with losing their homes and the foreclosure process. The committee suggested that Mr. Arnold work with Secretary of Veterans' Services Timothy L. Hale to discuss the issues and develop possible solutions. Representatives from Cannon Air Force Base and from the National Guard spoke about the comprehensive community and family support services provided to military personnel. These programs include relocation and transition assistance, financial management, youth and community programs and help with behavioral health, suicide prevention and sexual assault issues. The committee heard several presentations on the topic of PTSD, including the services available from community-based outpatient clinics and the New Mexico VA health care system. The VA is striving to provide effective treatments that can be accessed by all veterans in the state, including through telehealth services. -

Shop California Insider Tips 2020

SHOP CALIFORNIA INSIDER TIPS 2020 ENJOY THE ULTIMATE SHOPPING AND DINING EXPERIENCES! Exciting Shopping and Dining Tour Packages at ShopAmericaTours.com/shop-California Purchase with code ShopCA for 10% discount. Rodeo Drive 2 THROUGHOUT CALIFORNIA From revitalizing beauty services, to wine, spirits and chocolate tastings, DFS offers unexpected, BLOOMINGDALE’S complimentary and convenient benefits to its See all the stylish sights – starting with a visit to shoppers. Join the DFS worldwide membership Bloomingdale’s. Since 1872, Bloomingdale’s has program, LOYAL T, to begin enjoying members- been at the center of style, carrying the most only benefits while you travel.DFS.com coveted designer fashions, shoes, handbags, cosmetics, fine jewelry and gifts in the world. MACERICH SHOPPING DESTINATIONS When you visit our stores, you’ll enjoy exclusive Explore the U.S.’ best shopping, dining, and personal touches – like multilingual associates entertainment experiences at Macerich’s shopping and special visitor services – that ensure you feel destinations. With centers located in the heart welcome, pampered and at home. These are just of California’s gateway destinations, immerse a few of the things that make Bloomingdale’s like yourself in the latest fashion trends, hottest no other store in the world. Tourism services cuisine, and an unrivaled, engaging environment. include unique group events and programs, Macerich locations provide a variety of benefits special visitor offers and more, available at our to visitors, including customized shopping, 11 stores in California including San Francisco experiential packages, visitor perks and more. Centre, South Coast Plaza, Century City, Beverly To learn more about Macerich and the exclusive Center, Santa Monica Place, Fashion Valley and visitor experiences, visit macerichtourism.com. -

Confinement in the Land of Enchantment: Japanese Americans

The goal of “Confinement in the Land of Enchantment: Japanese Americans in New Mexico during WWII” (CLOE) is to reach a wide and diverse audience of New Mexicans and Americans about the histories of Japanese internment in the state, and to inspire thought and conversation about issues of citizenship, identity, and civil liberty. The project focuses on the stories of World War II Japanese confinement sites that were located at Santa Fe, Ft. Stanton, Old Raton Ranch (Baca Camp), and Camp Lordsburg in New Mexico. In addition to telling the stories of detainees held at each of these facilities, the project examines how the surrounding communities interacted with these camps. Stories of how various communities across New Mexico treated their Japanese and Japanese American community members are also explored. *Fort Stanton is part of this project, but a sketch is not included in this packet. It served primarily as a German non-combatant detainee camp, but did house the Japanese from Clovis who went to Old Raton Ranch and some internees who were sent from the camp in Santa Fe. Prior to the bombing of Pearl Harbor, the FBI began to compile lists of persons considered to be dangerous to national security. These “enemy aliens” included Japanese language teachers, religious ministers, former Japanese Army veterans, fishermen, officials of Japanese association and Japanese Consulate offices, and those who had donated to Japanese Widows and Orphans funds or victims of Sino-Japanese War, among others. On December 7, 1941, the arrest of these individuals began. This project is designed to document the confinement of those of Japanese descent in sites located in New Mexico. -

The New Mexican Review, 06-16-1910

University of New Mexico UNM Digital Repository Santa Fe New Mexican, 1883-1913 New Mexico Historical Newspapers 6-16-1910 The ewN Mexican Review, 06-16-1910 New Mexican Printing Co. Follow this and additional works at: https://digitalrepository.unm.edu/sfnm_news Recommended Citation New Mexican Printing Co.. "The eN w Mexican Review, 06-16-1910." (1910). https://digitalrepository.unm.edu/sfnm_news/7983 This Newspaper is brought to you for free and open access by the New Mexico Historical Newspapers at UNM Digital Repository. It has been accepted for inclusion in Santa Fe New Mexican, 1883-1913 by an authorized administrator of UNM Digital Repository. For more information, please contact [email protected]. ft if" THE NEW MEXICAN REVIEW. FORTY-SEVE- N YEAH SANTA FTi N. M.. THUItSDA JUNE Id 1910. NO 12 TAFT IN5ISI5 REQUISITION FE SLEPT OUTDOORS: SENATE LEADERS ASKED FOR IN KILLED ON; TRACK BY HE I! OIE Act Will Be Law Governor Haskell of Okla- Enabling President Will Get Tariff He Was Throvi Under Riot in Colorado and Ohio Chimayo Rancher Was Beat But Friends of Territories End of Next homa Wants Note by Alleged Board, and New Mexico Train in Albt'jperque and Fatal Feud in en With Hammer While Must Wait Until Postal Week Embezzler Returned Statehood Railroad Yards Kentucky Asleep Last Night Saving Bill Is Disposed WILL ADJOURN ON SATURDAY GUHRY REACHES WASHINGTON HIS BODY FEARFULLY iViANGLED CONVICT SHOOTS UP CHURCH REVENGE SUPPOSED MOTIVE $30,000,000 FOB IRRIGATION Beveridge and Other Member Judge McFie Returns From Las for the Remains Hope Again Springs Up Sent to This City and "tattle of Two Hours in Coal Sheriff Closson Hurries nn Auto- Reclamation Act Tacked as a of Territorial Committee at Vegas Where He Held . -

Millard Sheets Was Raised and Became Sensitive to California’S Agricultural Lifestyle

YYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYY I A A R R N T O F C I L L U A B C CALIFORNIA ART CLUB NEWSLETTER Documenting California’s Traditional Arts Heritage for More Than 100 Years e s 9 t a 9 0 b lis h e d 1 attracted 49,000 visitors. It was in this rural environment that Millard Sheets was raised and became sensitive to California’s agricultural lifestyle. Millard Sheets’ mother died in childbirth. His father, John Sheets, was deeply distraught and unable to raise his son on his own. Millard was sent to live with his maternal grandparents, Louis and Emma Owen, on their neighbouring horse ranch. His grandmother, at age thirty-nine, and grandfather, at age forty, were still relatively young. Additionally, with two of their four youngest daughters, ages ten and fourteen, living at home, family life appeared normal. His grandfather, whom Millard would call “father,” was an accomplished horseman and would bring horses from Illinois to race against Elias Jackson “Lucky” Baldwin (1828-1909) at Baldwin’s “Santa Anita Stable,” later to become Santa Anita Park. The older of Millard’s two aunts babysat him and kept him occupied Abandoned, 1934 with doing drawings. Oil on canvas 39 5/80 3 490 Collection of E. Gene Crain he magic of making T pictures became a fascination to Sheets, as he would later explain in Millard Sheets: an October 28, 1986 interview conducted A California Visionary by Paul Karlstrom for the Archives of American Art, Smithsonian by Gordon T. McClelland and Elaine Adams Institution: “When I was about ten, I found out erhaps more than any miles east of downtown Los Angeles. -

Learn English in Beautiful Southern California Why Cel?

CEL PACIFIC BEACH CEL SAN DIEGO CEL SANTA MONICA LEARN ENGLISH IN BEAUTIFUL SOUTHERN CALIFORNIA WHY CEL? ................................................ 3 GENERAL ENGLISH .......................... 4 EXAM PROGRAMS ............................ 5 OUR LEVELS .......................................... 6 WHY CEL? 9 More than 35 years of experience in teaching English TEACHING METHODS .................... 7 9 Small class size (average of 6-7, maximum of 10 students per class) 9 Recognized and accredited by language industry associations 9 New classes start every week SAN DIEGO ............................................. 8 9 Certified and experienced teachers OUR SCHOOL ..................................................... 10 9 Friendly and comfortable English speaking homestay families ACCOMODATION ............................................... 12 9 Great locations in San Diego Downtown, San Diego Pacific Beach and Los Angeles Santa Monica ACTIVITIES ............................................................ 16 9 Students from around the world 9 A wide choice of residential accommodation options 9 Fun activity program PACIFIC BEACH ................................... 18 OUR SCHOOL ..................................................... 20 OUR MISSION ACCOMODATION ............................................... 22 The mission of CEL is to provide English Language instruction and educational programs to speakers of other languages ACTIVITIES ............................................................ 16 who want to improve their English -

Updated 1.3.17 No Boxes.Indd

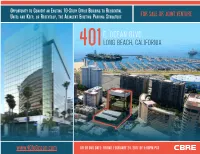

OPPORTUNITY TO CONVERT AN EXISTING 10-STORY OFFICE BUILDING TO RESIDENTIAL FOR SALE OR JOINT VENTURE UNITS AND KEEP, OR REDEVELOP, THE ADJACENT EXISTING PARKING STRUCTURE E. OCEAN BLVD. 401 LONG BEACH, CALIFORNIA www.401eOcean.com OFFER DUE DATE: FRIDAY, FEBRUARY 24, 2017 BY 5:00PM PST FOR SALE OR JOINT VENTURE PLEASE DO NOT DISTURB OR CONTACT TENANTS for more information contact: Laurie Lustig-Bower Executive Vice President Lic. 00979360 310.550.2556 [email protected] Gary Stache Executive Vice President Lic. 00773736 949.725.8532 [email protected] Kadie Presley Wilson Senior Sales Director Lic. 01476551 310.550.2575 [email protected] OFFER DUE DATE: FRIDAY, FEBRUARY 24, 2017 BY 5:00PM PST www.401eOcean.com © 2017 CBRE, Inc. The information contained in this document has been obtained from sources believed reliable. While CBRE, Inc. does not doubt its accuracy, CBRE, Inc. has not verified it and makes no guarantee, warranty or representation about it. It is your responsibility to independently confirm its accuracy and completeness. Any projections, opinions, assumptions or estimates used are for example only and do not represent the current or future performance of the property. The value of this transaction to you depends on tax and other factors which should be evaluated by your tax, financial and legal advisors. You and your advisors should conduct a careful, independent investigation of the property to determine to your satisfaction the suitability of the property for your needs. Pacific Ocean east ocean boulevard -

Renovation Last Fall

Going Places Macerich Annual Report 2006 It’s more than the end result—it’s the journey. At Macerich®, what’s important isn’t just the destination. It’s the bigger picture, the before and after...the path we take to create remarkable places. For retailers, it’s about collaboration and continual reinvestment in our business and theirs. For the communities we serve, it’s about working together to create destinations that reflect their wants and needs. For investors, it’s about long-term value creation stemming from a clear vision. For consumers, it’s about the total experience our destinations deliver. 0 LETTER TO STOCKHOLDERS Letter to Our Stockholders Macerich continued to create significant value in 2006 by elevating our portfolio and building a sizeable return for our stockholders. Total stockholder return for the year was 33.9%, contributing to a three-year total return of 121.5% and a five-year total return of 326.2%. In 2006, the company increased dividends for the 13th consecutive year. As a company that considers its pipeline a tremendous source of strength BoulderTwenty Ninth is a prime Street example is a prime of howexample 2006 of was how indeed 2006 awas remarkable indeed a yearremark of - and growth, Macerich reached an important milestone in 2006 with the buildingable year netof building asset value net for asset Macerich. value for We Macerich. also completed We also the completed redevelop the- re- opening of Twenty Ninth Street in Boulder, Colorado. Not only is this a mentdevelopment of Carmel of CarmelPlaza in Plaza Northern in Northern California, California, another another excellent excellent model of model terrific new asset in an attractive, affluent community—it represents a sig- valueof value creation, creation, where where we we realized realized a significant a significant return return on onour our investment. -

Belmont Plaza Olympic Pool to Be Demolished

Volume 23, No. 2, Spring 2013 Belmont Plaza Olympic Pool to Be Demolished The Belmont Plaza in 2012 another study determined that the natato- Olympic Pool complex rium might not be reparable after an earthquake was built in 1967 in measuring five magnitude or higher. This building, anticipation of the which measures 224’x148,’ was constructed with a 1968 Olympic trials. shear-wall frame, cast in place reinforced concrete columns, and prestressed concrete girders. It has a 23’ high glass curtain wall below a 25’ high precast concrete shear wall. In 1968 this type of construc- tion clearly met the code requirements, but today, more stringent rules are applied to such buildings. According to the latest seismic report, some cracks have appeared in the natatorium and the walls ap- pear to be deteriorating. When completed, the Belmont Pool mea- sured 50 X 75 meters, had eight lanes ranging from 3½ to 12 feet deep, six lifeguard towers equipped with television monitors, and movable plastic pan- PHOTOGRAPHY BY LOUISE IVERS LOUISE BY PHOTOGRAPHY els in the roof that could be opened to allow the By Louise Ivers to the Los Angeles Times, Mark Spitz, Don Schol- sun to shine on the swimmers. A computerized lander, and Charles Hickox set men’s records during scoreboard provided extremely accurate record- In January 1967 plans were approved for a group these trials. During the 1975 Olympic development ing of athletes’ prowess. Bleachers seated 3,500 of structures at Belmont Plaza, a site west of the meet, Shirley Babashoff took first place in the 400 spectators and a press box with the most modern pier on the beach in Belmont Shore.