Press and Media

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Londonderry Times 09/17/2020

HOMETOWN NEWS DELIVERED TO EVERY HOME IN TOWN FREE September 17, 2020 N Volume 21 – Issue 38 A FREE Weekly Publication Town Council Keeps Local Water Restrictions on Hold CHRIS PAUL newly revised ordi- As far as implement- LONDONDERRY TIMES ————–––––————–N nance. ing the plan, Board uring the Monday On Monday night the Member Tom Dolan was night, Sept. 14, discussion started with the first to address the DLondonderry Councilor Deb Paul ask- need for water restric- Town Council meeting, ing to reopen the ordi- tions. members decided that nance to make changes Dolan said, “When implementing water to the language, saying we did this a few years restrictions through a that she thought the fine ago, I was inundated newly adopted water amounts were too with emails and phone ordinance was not nec- severe. Paul also felt calls from residents that essary quite yet. One that the municipalities either had problems member also had addi- should be added into the with their wells going tional thoughts on plan, saying that the dry, or slowly recover- adjusting the plan, if it town should lead by ing, quality of the water were to be implemented. example. and so forth. I can tell At the last meeting, Farrell responded by you, this year, with the at the end of August, saying that those exception of Ms. Mele, I Council Chair, John Far- changed could be haven’t had a single rell, tabled the discus- addressed, but it would phone call or a single sion on whether or not have to be re-noticed email on this topic.” to implement the plan. -

Holland & Knight

Post-Election Analysis November 2020 Holland & Knight President President President-Elect Donald J. Trump Joseph R. Biden Trump: 217 Biden: 290 2 Source: Bloomberg, as of 4:00 PM EST on Nov. 11, 2020 New House of Representatives Democrats: 218 Republicans: 202 Uncalled races: 15 Source: Bloomberg, as of 4:00 PM EST on Nov. 11, 2020 3 Key House Race Results . Arizona o FL-15 Scott Franklin* (R) defeated Alan Cohn (D) o AZ-01 Tom O’Halleran* (D) defeated Tiffany Shedd (R) o FL-16 Vern Buchanan* (R) defeated Margaret Good (D) o AZ-02 Ann Kirkpatrick* (D) defeated Brandon Martin (R) o FL-26 Carlos Gimenez (R) defeated Debbie Mucarsel-Powell* o AZ-06 David Schweikert* (R) defeated Hiral Tipirneni (D) (D) DR DR . California o FL-27 Maria Elvira Salazar (R) defeated Donna Shalala* (D) o CA-10 Josh Harder* (D) defeated Ted Howze (R) . Georgia o CA-21 TJ Cox* (D) vs. David Valadao (R) Not called o GA-06 Lucy McBath* (D) defeated Karen Handel (R) o CA-25 Christy Smith (D) vs. Mike Garcia* (R) Not called o GA-07 Carolyn Bourdeaux (D) defeated Rich McCormick (R) R D o CA-39 Gil Cisneros* (D) vs. Young Kim (R) Not called . Illinois CA-45 Katie Porter* (D) defeated Greg Raths (R) o o IL-06 Sean Casten* (D) defeated Jeanne Ives (R) CA-48 Michelle Steel (R) defeated Harley Rouda* (D) DR o o IL-13 Rodney Davis* (R) defeated Betsy Londrigan (D) CA-49 Mike Levin* (D) defeated Brian Maryott (R) o o IL-14 Lauren Underwood* (D) vs. -

2018 Political Contributions and Related Activity Report

2018 Political Contributions & Related Activity Report 2018 BOARD OF DIRECTORS Scott Anglin Morgan Kendrick SVP, Treasurer & President, National Accounts Chief Investment Officer Gloria McCarthy LeAnn Behrens EVP & Chief Transformation President, Officer Medicaid West Region Kristen Metzger Laurie Benintendi President, Medicaid VP & Counsel, CSBD/Clinical Central Region Elizabeth Canis Tom Place VP, Strategic Initiatives VP, IT Operations Brandon Charles Maria Proulx VP, Enterprise Clinical Ops VP, Segment Solutions Tracy Edmonds Kevin Riordan VP, Diversity & Inclusion RVP Federal Affairs/ Anthem PAC Treasurer Jeff Fusile President, GA Commercial Marc Russo President, Medicare Julie Goon SVP, Public Affairs Tracy Winn Anthem PAC Chairman PAC Manager; Anthem PAC Assistant Treasurer John Jesser VP, Provider Engagement Strategy Live Health Online 1 CHAIRMAN LETTER Anthem’s vision to be the most innovative, valuable, and inclusive partner extends to the relationships we build with lawmakers at every level of government. These partnerships ensure that we are able to educate policymakers on how their decisions impact our ability to deliver a simpler, more affordable, and more accessible health care experience for our customers and their families. We work to build these political partnerships with both Democrats and Republicans through a public affairs strategy that includes direct advocacy, grassroots engagement, and political contributions. This report lists all political candidates and committees that received support in 2018 from our eligible associates through Anthem’s Political Action Committee (Anthem PAC) and through permissible corporate contributions made by Anthem and its subsidiaries. It also includes a summary of our 2018 PAC receipts and expenditures and the criteria used to determine which candidates and committees received our support. -

Key State Legislative Contacts

Key State Legislative Contacts mac.mccutcheon@alhous Speaker of the House ALABAMA e.gov State Capitol Room 208 Governor Kay Ivey Phone: 334-261-0505 Juneau, AK 99801 600 Dexter Avenue Representative.Bryce.Edg Montgomery, AL 36130- Rep. Victor Gaston [email protected] 2751 11 South Union St Phone: 907-465-4451 Email via this portal Suite 519-G Phone: 334-242-7100 Montgomery, AL 36130 Rep. Steve Thompson [email protected] House Minority Leader Lt. Governor Will v State Capitol Room 204 Ainsworth Phone: 334-261-0563 Juneau, AK 99801 11 South Union St Representative.Steve.Tho Suite 725 Rep. Nathaniel Ledbetter [email protected] Montgomery, AL 36130 11 South Union St Phone: 907-465-3004 [email protected] Suite 401-G Montgomery, AL 36130 Rep. Lance Pruitt Senator Del Marsh nathaniel.ledbetter@alho House Minority Leader 11 South Union St use.gov State Capitol Room 404 Suite 722 Phone: 334-261-9506 Juneau, AK 99801 Montgomery, AL 36130 Representative.Lance.Pruit [email protected] Rep. Anthony Daniels [email protected] Phone: 334-261-0712 11 South Union St 907-465-3438 Suite 428 Senator Greg Reed Montgomery, AL 36130 Senator Cathy Giessel 11 South Union St anthony.daniels@alhouse. Senate President Suite 726 gov State Capitol Room 111 Montgomery, AL 36130 Phone: 334-261-0522 Juneau, AK 99801 [email protected] Senator.Cathy.Giessel@akl Phone: 334-261-0894 eg.gov ALASKA Phone: 907-465-4843 Senator Bobby Singleton Governor Mike Dunleavy 11 South Union St PO BOX 110001 Senator Lyman Huffman Suite 740 Juneau, AK 99811-0001 Majority Leader Montgomery, AL 36130 Email via this portal State Capitol Room 508 [email protected] Juneau, AK 99801 Phone: 334-261-0335 Lt. -

What You Need to Know John Colbert, ESQ Capitol Hill Partners

WHAT YOU NEED TO KNOW JOHN COLBERT, ESQ CAPITOL HILL PARTNERS Areas for Discussion FY 20 FUNDING UPDATE WHAT’S HAPPENING ON THE WHAT TO EXPECT HILL AND IN THE ADMINISTRATION MOVING FORWARD 3 STATUS OF FY20 FUNDING FY20 budget request 4 Administration’s FY 20 budget request Proposes 9.5% cut to domestic programs 12% cut to the Department of Education FY 20 House Budget 5 House Democrats created Provided 5.7% increase or their own budget bill this domestic programs above spring – no agreement FY 19. with Senate on overall funding. FY 20 House Labor-HHS funding 6 New House Labor-HHS Chair – Rosa DeLauro (D-CT) •$11.8 billion increase for Labor-HHS •Passed on party line vote through House 7 House Labor-HHS Bill Department of Education FY 20 House WIOA Title II Adult +$30 million Labor-HHS Education Appropriations bill Increases Pell Grant by $150 CTE +37 million 8 House Labor-HHS Bill Department of Labor FY 20 House Labor-HHS WIOA +380 million Appropriations bill Adult +$55 million Youth +$61 million 9 House Labor-HHS Bill Department of Labor FY 20 House Apprenticeships +90 million Labor-HHS New $150 million Appropriations Strengthening bill Community College Grants initiative House Labor-HHS Appropriations bill 10 House bill will be high point for FY 20 funding this year 11 Unlike the House, Senate Majority Leader Mitch McConnell refused to move forward on any Senate refused to appropriations bills until budget move forward agreement put in place. without a budget No Senate appropriations bill has passed on the Senate floor to date. -

SUNUNU LEADS PRIMARY and GENERAL ELECTION CHALLENGERS; VOLINSKY and FELTES EVENLY MATCHED AMONG DEMOCRATS By: Sean P

September 2, 2020 SUNUNU LEADS PRIMARY AND GENERAL ELECTION CHALLENGERS; VOLINSKY AND FELTES EVENLY MATCHED AMONG DEMOCRATS By: Sean P. McKinley, M.A. [email protected] Zachary S. Azem, M.A. 603-862-2226 Andrew E. Smith, Ph.D. cola.unh.edu/unh-survey-center DURHAM, NH – With less than one week to go before the primary, Execu ve Councilor Andru Volinsky and State Senate Majority Leader Dan Feltes are evenly matched in the race for the Democra c nomina on for governor. Incumbent Chris Sununu holds a commanding lead over Franklin City Councilor Karen Testerman and con nues to enjoy leads of more than twenty percentage points over his prospec ve Democra c rivals for the governorship. Approval of Sununu’s tenure as governor remains high; seven in ten approve of his overall job performance and three-quarters approve of his handling of the COVID-19 situa on. These findings are based on the latest Granite State Poll*, conducted by the University of New Hampshire Survey Center. One thousand and nine hundred forty-nine (1,949) Granite State Panel members completed the survey online between August 28 and September 1, 2020. The margin of sampling error for the survey is +/- 2.2 percent. Included were 1,889 likely 2020 general elec on voters (MSE = +/- 2.3%), 839 likely Democra c primary voters (MSE = +/- 3.4%) and 703 likely Republican primary voters (MSE = +/- 3.7%). Data were weighted by respondent sex, age, educa on, and region of the state to targets from the most recent American Community Survey (ACS) conducted by the U.S. -

Berlindailysun.Com

Hiking columnist hikes Mount Success in Mahoosuc Range — see page 13 THURSDAY, JULY 1, 2021 VOL. 30 NO. 31 BERLIN, N.H. 752-5858 FREE $22m in state investments to benefi t Coos parks BY BARBARA TETREAULT the state park system which is receiving $22.6 mil- ture. Much of the money will go to state parks in THE BERLIN SUN lion in federal funding to allow the state to make Coos County including Jericho Mountain State Park COOS COUNTY — These are exciting times for needed improvements to its aging park infrastruc- see PARKS page 6 Police train with transit van Supreme Court hears ‘Fallen 7’ driver’s request BY BARBARA TETREAULT THE BERLIN SUN CONCORD — After hearing oral argu- ments Tuesday, the state Supreme Court must now decide whether the truck driver implicated in the “Fallen 7” collision is enti- tled to an evidentiary hearing on whether he can be released on bail. Volodymyr Zhukovskyy, 25, has been held at the Coos County Jail in West Stewart- stown for two years in preventive detention while waiting for trial in the crash that killed seven motorcyclists to get underway. Three times, Coos County Superior Court Justice Peter Bornstein has denied his request for an evidentiary bail hearing. Zhukovskyy of West Springfi eld, Mass., has pleaded not guilty to multiple counts of negligent homicide, negligent homicide-DUI, and manslaughter in the June 2019 crash that killed seven members of the JarHeads Motorcycle Club on Route 2 in Randolph. Killed were Albert Mazza, 59, of Lee; Daniel Pereira, 58, of Riverside, R.I.; Michael Ferazzi, 62, of Contoocook; Aaron Perry, 45, of Lee; Desma Oakes, 42, of Concord; and Edward and Tri-County Community Action Program lent its North Country Transit bus to the Berlin Police Department for its barricaded subject and Joan Corr, both 58 of Lakeview, Mass. -

Political Contributions & Related Activity Report 1

2017 Political Contributions & Related Activity Report 1 2017 BOARD OF DIRECTORS Carter Beck Gloria McCarthy SVP & Counsel EVP & Chief Transformation Officer LeAnn Behrens President Medicaid West Mike Melloh Region VP Learn & Development & Chief Learning Officer Jeff Fusile President GA Commercial Kristen Metzger President Medicaid Health Julie Goon Plan – Indiana SVP Public Affairs Anthem PAC Chairman Tom Place VP IT Operations John Jesser VP Provider Engagement Kevin Riordan Strategy RVP Federal Affairs, Anthem PAC Treasurer Morgan Kendrick President National Accounts Marc Russo President Medicare David Kretschmer SVP Treasurer & Tracy Winn Chief Investment Officer PAC Manager Public Affairs, Anthem PAC Assistant Treasurer & Executive Director 2018 INCOMING BOARD OF DIRECTORS Scott Anglin Brandon Charles SVP Treasurer & VP Clinical Accountability Chief Investment Officer Tracy Edmonds Laurie Benintendi VP Diversity & Inclusion VP & Counsel Maria Proulx Elizabeth Canis VP Segment Solutions VP Strategic Initiatives 1 CHAIRMAN LETTER Here at Anthem, we are committed to bringing more accessible and affordable health care to all Americans by working together with lawmakers in the dynamic public policy arena. Our state and federal elected representatives play a large role in shaping the present and future of health care, and we want to take this opportunity to help you to understand why Anthem engages with elected officials and how our company participates in the political process. I am proud to share this comprehensive annual report with you about the financial political activity of Anthem and Anthem PAC in 2017. Our political contributions are essential to the company’s strategic ability to build trusted relationships with policymakers and educate them about policy issues important to Anthem, our members, and our associates. -

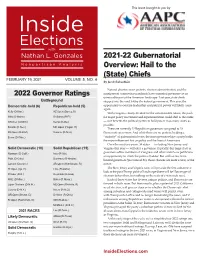

2021-22 Gubernatorial Overview: Hail to the (State) Chiefs FEBRUARY 19, 2021 VOLUME 5, NO

This issue brought to you by 2021-22 Gubernatorial Overview: Hail to the (State) Chiefs FEBRUARY 19, 2021 VOLUME 5, NO. 4 By Jacob Rubashkin Natural disaster, mass protests, election administration, and the 2022 Governor Ratings omnipresent coronavirus pandemic have cemented governors as an unmissable part of the American landscape. Last year, state chiefs Battleground stepped into the void left by the federal government. This year, the Democratic-held (6) Republican-held (5) opportunity to exercise leadership and political power will likely come again. Kelly (D-Kan.) AZ Open (Ducey, R) With Congress closely divided for the unforeseeable future, the push Mills (D-Maine) DeSantis (R-Fl.) for major policy movement and experimentation could shift to the states Whitmer (D-Mich.) Kemp (R-Ga.) — so it benefits the political parties to hold power in as many states as possible. Sisolak (D-Nev.) MD Open (Hogan, R) There are currently 27 Republican governors compared to 23 PA Open (D-Wolf) Sununu (R-N.H.) Democratic governors. And while there are no perks to holding a Evers (D-Wisc.) “majority” of gubernatorial seats, the more governorships a party holds, the more influence it has on policy and the lives of Americans. Over the next two years, 38 states — including New Jersey and Solid Democratic (10) Solid Republican (15) Virginia this year — will elect a governor. Typically, this large class of Newsom (D-Calif.) Ivey (R-Ala.) governors offers members of Congress and other ambitious politicians an opportunity to climb the political ladder. But with so few term- Polis (D-Colo.) Dunleavy (R-Alaska) limited governors (just nine of 38), those chances are more scarce, at the Lamont (D-Conn.) AR Open (Hutchinson, R) outset. -

Election Wrap up and Look Ahead

Election Wrap Up and Look Ahead November 4, 2020 0 Index Big Picture Key Takeaways Election Results House of Representatives Senate Governors Congressional Leadership Committee Leadership Lame Duck Agenda Key Dates We are Invariant. Contact us. 1 Big Picture Amid unprecedented early voting and historic total turnout under coronavirus pandemic conditions, voting in the 2020 election is complete. And while the count will continue, it is clear many voters like the political team they are on. In an era of taking sides – with cable news and social media offering tailored information streams and voters able to choose their own set of facts – results so far reveal an increasingly tribal electorate. President Donald Trump spoke early this morning from the East Room of the White House to call the vote count underway a “major fraud on our nation” and threatened he is “going to the US Supreme Court.” He described this as a “very sad moment” and called on “all voting to stop.” He concluded by claiming: “We will win this, and as far as I’m concerned, we already have won it.” Former Vice President Joe Biden spoke from a drive-in rally in Wilmington, Delaware to say he believes he is “on track to win this election” and that “it ain’t over until every ballot is counted.” While both candidates can credibly claim momentum going forward, vote tallies have Biden steadily adding votes in Arizona and Nevada and awaiting the count of more than one million ballots in Pennsylvania. President Trump held his ground with victories in Florida and Ohio. -

2020 U.S. Elections Roundup Introduction

2020 U.S. ELECTIONS ROUNDUP INTRODUCTION Welcome to McGuireWoods Consulting’s 2020 U.S. Elections Roundup interactive website — your one-stop resource for this year’s presidential, congressional, gubernatorial, attorneys general and state legislative races. Complete with concise information about how elections are shaping up around the country — including snapshots of primary results and hot-button ballot initiatives — our site provides a landscape view of our nation’s political scene and insights on potential shifts in the tide. Our goal is to provide business leaders and constituents quick, reliable access to comprehensive information about this year’s elections. Based on a compilation of public polling and forecasting data collected and analyzed by Politico, UVA Center for Elections, Inside Elections, 270toWin and the Cook Political Report, information provided on our site will be updated as appropriate. We hope you find our site helpful, and please let us know if you have any questions about our country’s most anticipated elections. Gov. James Hodges Mona Mohib Scott Binkley President Senior Vice President Vice President +1 803 251 2301 +1 202 857 2912 +1 202 857 2921 Email Email Email 2 WHY ARE THE 2020 STATE ELECTIONS IMPORTANT? During a presidential election, state races often take a backseat. But for 2020, the electoral battles in the states are critical because there is much at stake: Whichever party ends up controlling the governorships and state legislatures in key states after the election will have substantial influence over the congressional redistricting process after the 2020 census. How district maps are drawn will have an impact on state and congressional races for the next 10 years. -

September 18, 2020 Volume 4, No

This issue brought to you by The Senate Deserves Your Attention By Nathan L. Gonzales & Jacob Rubashkin SEPTEMBER 18, 2020 VOLUME 4, NO. 18 While the race for the White House dominates the news, the fight for the Senate is closer. The easiest thing to do after 2016 would be to declare every race with 2020 Senate Ratings President Donald Trump on the ballot as a toss-up. But that would be at the expense of the data. After analyzing polling at the national, state Toss-Up and congressional district level, our current projection gives Joe Biden a Collins (R-Maine) Ernst (R-Iowa) 319-187 advantage in the Electoral College with 32 votes in the Toss-up Daines (R-Mont.) Tillis (R-N.C.) category. That doesn’t mean the presidential race is over, but there’s more certainty about who is leading than which party will control the Senate. Tilt Democratic Tilt Republican Our current Senate outlook is a Democratic net gain of 3-5 seats. That puts Gardner (R-Colo.) Perdue (R-Ga.) Democratic control (which requires a three-seat net gain with a White House McSally (R-Ariz.) victory or a four-seat net gain for a majority) within our range of most likely Lean Democratic Lean Republican outcomes. But if the results dip one seat below our projection (Democrats only gain two seats) then Republicans will maintain their majority. And right Peters (D-Mich.) KS Open (Roberts, R) now there are a handful of races, specifically North Carolina, Maine, Iowa, Cornyn (R-Texas) Montana, Georgia, and even South Carolina, where a shift of a few points is Graham (R-S.C.)# the difference between a Republican majority and a Democratic landslide.