Listed Companies Results a LOCKDOWN EFFECT WIDELY

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

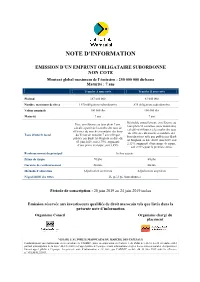

Note D'information

NOTE D’INFORMATION EMISSION D’UN EMPRUNT OBLIGATAIRE SUBORDONNE NON COTE Montant global maximum de l’émission : 250 000 000 dirhams Maturité : 7 ans Tranche A non cotée Tranche B non cotée Plafond 167 000 000 83 000 000 Nombre maximum de titres 1 670 obligations subordonnées 830 obligations subordonnées Valeur nominale 100 000 dhs 100 000 dhs Maturité 7 ans 7 ans Révisable annuellement, en référence au Fixe, en référence au taux plein 7 ans, taux plein 52 semaines (taux monétaire) calculé à partir de la courbe des taux de calculé en référence à la courbe des taux référence du marché secondaire des bons de référence du marché secondaire des Taux d’intérêt facial du Trésor de maturité 7 ans telle que bons du trésor telle que publiée par Bank publiée par Bank Al-Maghrib en date du Al-Maghrib en date du 03 juin 2019, soit 03 juin 2019, soit 2,75%, augmenté 2,31%, augmenté d’une prime de risque, d’une prime de risque, soit 3,45% soit 2,91% pour la première année Remboursement du principal In fine au pair Prime de risque 70 pbs 60 pbs Garantie de remboursement Aucune Aucune Méthode d’allocation Adjudication au prorata Adjudication au prorata Négociabilité des titres De gré à gré (hors Bourse) Période de souscription : 20 juin 2019 au 24 juin 2019 inclus Emission réservée aux investisseurs qualifiés de droit marocain tels que listés dans la présente note d’information Organisme Conseil Organisme chargé du placement VISA DE L’AUTORITE MAROCAINE DU MARCHE DES CAPITAUX Conformément aux dispositions de la circulaire de l’AMMC, prise en application de l’article 5 du Dahir n°1-12-55 du 28 décembre 2012 portant promulgation de la loi n° 44-12 relative à l’appel public à l’épargne et aux informations exigées des personnes morales et organismes faisant appel public à l’épargne, la présente note d’information a été visée par l’AMMC en date du 12 juin 2019 sous la référence n° VI/EM/012/2019. -

Flash Quotidien Recherche - Actions Jeudi 15 Juillet 2021

Flash Quotidien Recherche - Actions jeudi 15 juillet 2021 SYNTHESE DU MARCHE PERFORMANCE DU MARCHE Performance 13 000 12 565,7 3 000 Indice Valeur Quotidienne YtD 12 000 2 500 Points MMAD 2 000 MASI 12 140,26 -0,24% +7,56% 11 000 1 500 MSI 20 989,68 -0,27% +7,02% 10 000 1 000 FTSE CSE 15 11 465,02 -0,20% +12,12% 9 952,6 9 000 500 FTSE CSE All 10 346,78 -0,26% +6,19% 8 000 0 Capi (Md MAD) 625,2 -0,11% +6,87% 15/07/20 15/09/20 15/11/20 15/01/21 15/03/21 15/05/21 15/07/21 Volumes MC (MMAD) MASI CINQ PREMIERES CAPITALISATIONS PERFORMANCE QUOTIDIENNE PAR SECTEUR -4, 5% -3, 5% -2, 5% -1, 5% -0, 5% 0,5% 1,5% 0,8% Promotion Immobilière 0,7% BTP & Matériaux 118,9 0,7% Sociétés financières 0,2% NTI 0,2% Industries 94,0 0,1% Stés placement immobilier 0,0% Services aux collectivités 0,0% Courtage 0,0% Holdings 53,2 Agroalimentaire 41,7 -0,0% 34,3 -0,1% Marché -0,1% Banques -0,2% Télecommunications -0,2% +0,1% -1,2% +1,1% +1,8% -0,2% Distribution -0,2% Assurances IAM ATW BCP LHM BCE -0,5% Transport -0,7% Pétrole, Chimie et Mines Capi (en Md MAD) % Var. quotidienne -2,4% Hôtellerie VOLUME DU MARCHE ACTIONS PRINCIPALES VARIATIONS DU JOUR Volume (MMAD) % Valeur Cours Var.% Titres échangés P/E 201 Marché Central 64,7 67,7% Fenie Brossette 98,62 +4,00% 749 ns Attijariwafa Bank 14,8 22,9% Microdata 652,00 +3,84% 5 15,5 Maroc Telecom 10,8 16,6% Stokvis Nord Afrique 13,73 +3,23% 2 435 ns Sonasid 6,7 10,3% Med Paper 15,59 +2,16% 2 045 ns Managem 6,3 9,8% M2M Group 824,00 -4,00% 11 ns Label Vie 4,9 7,6% Total Maroc 1 480,00 -3,58% 89 22,7 Marché de Blocs 30,8 47,6% CIH Bank 281,00 -3,10% 84 26,0 Marché Global 95,6 100,0% Risma 116,00 -2,40% 366 ns . -

Flash Quotidien Recherche - Actions Jeudi 17 Février 2021

Flash Quotidien Recherche - Actions jeudi 17 février 2021 SYNTHESE DU MARCHE PERFORMANCE DU MARCHE 13 000 12 507,0 1 200 Performance 12 000 1 000 Points Indice Valeur MMAD 800 Quotidienne YtD 11 000 MASI 11 521,02 -0,51% +2,07% 600 10 000 400 MADEX 9 387,12 -0,53% +2,15% 9 000 200 FTSE CSE 15 10 552,49 -0,53% +3,20% 8 987,9 8 000 0 FTSE CSE All 9 901,31 -0,50% +1,62% 17/02/20 17/04/20 17/06/20 17/08/20 17/10/20 17/12/20 17/02/21 Capi (Md MAD) 595,4 -0,47% +1,78% Volumes MC (MMAD) MASI CINQ PREMIERES CAPITALISATIONS PERFORMANCE QUOTIDIENNE PAR SECTEUR -3, 0% -2, 0% -1, 0% 0,0% 1,0% 2,0% 3,0% 2,6% Hôtellerie 127,6 0,5% Distribution 0,5% Télecommunications 0,4% Stés placement immobilier 89,2 0,1% NTI 0,0% Holdings 0,0% Industries 0,0% Courtage 51,4 0,0% Services aux collectivités 0,0% Sociétés financières 37,7 32,0 -0,0% 0,0% Assurances -0,2% 0,0% Transport -0,4% 0,0% Agroalimentaire +0,5% -0,8% +0,0% -1,8% -1,8% -0,5% 0,0% Marché -0,6% 0,0% Promotion Immobilière IAM ATW BCP LHM BCE -0,8% 0,0% Banques -1,3% Pétrole, Chimie et Mines Capi (en Md MAD) % Var. quotidienne -1,3% BTP & Matériaux VOLUME DU MARCHE ACTIONS PRINCIPALES VARIATIONS DU JOUR Volume (MMAD) % Valeur Cours Var.% Titres échangés P/E 201 Marché Central 106,0 100,0% Lesieur Cristal 174,95 +2,91% 25 29,1 Attijariwafa Bank 34,7 32,7% Risma 110,80 +2,59% 22 11,3 Sté Boissons du Maroc 32,5 30,7% Promopharm 743,50 +1,99% 50 14,3 Maroc Telecom 14,5 13,7% Disway 500,00 +1,81% 1 100 13,9 Marsa Maroc 5,4 5,1% Sonasid 367,00 -2,91% 1 794 ns BCP 2,8 2,7% CIH Bank 258,00 -2,64% 1 000 17,1 Marché de Blocs 0,0% Managem 1 292,00 -2,49% 2 169 ns Marché Global 106,0 100,0% Total Maroc 1 255,00 -1,95% 33 18,7 . -

Flash Quotidien Recherche - Actions Mercredi 12 Décembre 2018

Flash Quotidien Recherche - Actions Mercredi 12 Décembre 2018 SYNTHESE DU MARCHE PERFORMANCE DU MARCHE 14 400 2 000 13 284,9 Performance 13 400 Points Indice Valeur 1 500 MMAD Quotidienne YtD 12 400 MASI 11 214,37 -0,59% -9,48% 11 400 1 000 10 400 10 885,5 MADEX 9 112,17 -0,62% -9,78% 500 FTSE CSE 15 10 124,06 -0,69% -12,81% 9 400 FTSE CSE All 9 605,34 -0,69% -9,31% 8 400 0 12/12/17 12/02/18 12/04/18 12/06/18 12/08/18 12/10/18 12/12/18 Capi (Md MAD) 572,0 -0,54% -8,77% Volumes MC (MMAD) MASI CINQ PREMIERES CAPITALISATIONS PERFORMANCE QUOTIDIENNE PAR SECTEUR 1,8% Holdings 123,4 0,8% Distribution 0,7% NTI 0,2% Pétrole, Chimie et Mines 91,0 0,1% Promotion Immobilière 0,1% Industries 0,1% Courtage 0,0% Télecommunications 50,5 0,0% Transport 39,6 0,0% Stés placement immobilier 33,7 0,0% Hôtellerie 0,0% Sociétés financières 0,0% +0,0% -1,5% -1,9% -1,6% -0,0% Services aux collectivités -0,2% Agroalimentaire Marché IAM ATW BCP LHM BCE -0,5% -1,1% BTP & Matériaux -1,2% Banques Capi (en Md MAD) % Var. quotidienne -1,6% Assurances VOLUME DU MARCHE ACTIONS PRINCIPALES VARIATIONS DU JOUR Volume (MMAD) % Valeur Cours Var.% Titres échangés P/E 18E Marché Central 166,1 100,0% Stroc Industrie 26,60 +9,92% 2 nd LafargeHolcim Maroc 96,4 58,0% Aluminium Du Maroc 1 664,00 +3,94% 1 12,4 CIH Bank 13,7 8,2% Managem 1 038,00 +3,80% 1 106 23,4 Maroc Telecom 13,6 8,2% Auto Hall 80,00 +3,07% 11 24,3 Attijariwafa Bank 13,6 8,2% Med Paper 21,00 -4,46% 20 7,8 Cosumar 5,0 3,0% Stokvis Nord Afrique 13,00 -3,70% 590 nd Marché de Blocs 0,0% SNEP 432,65 -3,61% 350 10,0 Marché Global 166,1 100,0% Jet Contractors 327,05 -3,47% 200 6,1 Clôture dans le rouge. -

Guide Des Valeurs 2018

GUIDE DES VALEURS 2018 SPECIAL RESULTATS SEMESTRIELS Guide des valeurs - Spécial résultats semestriels - SOMMAIRE ABREVIATIONS ................................................................................................................................................... 3 EXECUTIVE SUMMARY .................................................................................................................................... 4 METHODES ET PRINCIPALES HYPOTHESES DE VALORISATION ....................................................... 4 SYNTHESE DES RECOMMANDATIONS ....................................................................................................... 5 FICHES VALEURS .............................................................................................................................................. 6 Addoha .......................................................................................................................................................... 7 Attijariwafa Bank ........................................................................................................................................... 7 Banque Centrale Populaire ......................................................................................................................... 7 BMCE Bank of Africa ................................................................................................................................... 7 CIH Bank ...................................................................................................................................................... -

Stock Guide Des Principales Valeurs Marocaines

Mai 2021 STOCK GUIDE DES PRINCIPALES VALEURS MAROCAINES Mai 2021 Mai 2021 Abréviations GAZ AFRIQUIA GAZ LHM LAFARGEHOLCIM MAROC ATL ATLANTA LES LESIEUR CRISTAL ATW ATTIJARIWAFA BANK MNG MANAGEM ATH AUTO HALL MIC MICRODATA BCP BANQUE CENTRALE POPULAIRE IAM MAROC TELECOM BCI BMCI MSA MARSA MAROC SBM SOCIETES DES BOISSONS DU MAROC CMT MINIERE DE TOUISSIT CDM CDM OUL OULMES CIH CIH SAH SAHAM ASSURANCE CMA CIMENTS DU MAROC SMI SM IMITER CSR COSUMAR SNP SNEP DHO DELTA HOLDING SID SONASID DWY DISWAY SOT SOTHEMA EQD EQDOM TQM TAQA MOROCCO HPS HPS TMA TOTAL MAROC LBV LABEL’VIE WAA WAFA ASSURANCE P.2 Mai 2021 Synthèse des recommandations et des cours cibles Ce stock guide couvre les réalisations, les perspectives et les recommandations de 32 principales valeurs cotées à la Bourse de Casablanca, représentant 88,3% de sa capitalisation globale : ~ Les valeurs à Acheter ~ Les valeurs à Conserver ~ Les valeurs à Alléger Cours au Cours Cible % de la capi Cours au Cours au Cours % de la Valeurs 21/05/21 Valeurs Cours Cible % de la capi Valeurs 21/05/2021 21/05/2021 Cible capi CDM 444 650 0,8% AFRIQUIA GAZ 4180 4050 2,3% BOISSONS DU MAROC 2700 2238 1,2% DISWAY 545 665 0,2% AUTO HALL 89 85 0,7% TOTAL MAROC 1450 1400 2,1% MICRODATA 690 770 0,2% BMCI 684 655 1,4% TOTAL 3,3% TOTAL 1,1% CIH BANK 279 285 276 CIMENTS DU MAROC 1868 1714 4,3% ~ Les valeurs à Accumuler DELTA HOLDING 34 36 0,5% Cours au Cours Valeurs % de la capi EQDOM 1208 1300 0,3% 21/05/21 Cible ATLANTASANAD 94 97 0,9% HPS 6050 5900 0,7% ATTIJARIWAFA BANK 456 490 15,5% LESIEUR CRISTAL 189 191 -

29 March 2021

MARCH 29 2021 MARKET INSIGHT | MASI | 11 483 pts | MADEX | 9 338 pts | CAPI | 595 MAD Bn | VOLUME | 74 MAD Mn Daily -0,14% Daily -0,16% High 607 MC 74 YTD 1,73% YTD 1,61% Low 581 MB - THE DAY IN REVIEW TOP PERFORMERS BOTTOM PERFORMERS JET CONTRACTORS BOA At the end of this trading session, 4,0% 203,8 -3,8% 154,0 the MASI index decreased by 0.14% to 11,483 points. In this context, the EQDOM SALAFIN annual performance of the market 1 206,0 -3,3% 551,2 settles at 1.73%. STROC BMCI Jet Contractors topped the highest 3,7% 17,0 -2,8% 700,0 increases recording a gain of 4.0%. In the opposite, Bank Of Africa INVOLYS CTM dropped by 3.8%, i.e. the strongest 107,0 694,0 2,6% -2,0% decline of this trading session. SOTHEMA RISMA 2,0% 3 072,0 -1,6% 103,0 MOST ACTIVE (MAD Mn) LARGEST CAP (MAD Bn) ATTIJARIWAFA BANK IAM Volume on the central market 21 0,0% 123 reached MAD 74 Mn. SONASID ATTIJARIWAFA BANK This was mainly driven by Attijariwafa 10 0,6% 90 bank and Sonasid which monopolized 42% of the total flow. MICRODATA BCP 7 51 -0,1% SNEP LAFARGEHOLCIM MAROC 6 0,5% 39 HPS BOA 4 -0,5% 32 -3,8% Attijari Global Research Mahat Zerhouni MASI INDEX EVOLUTION (pts) ADV- MONTHLY BASIS VOLUME (MAD Mn) +212 529 03 68 16 [email protected] 500 13 500 400 12 500 Attijari Intermédiation 300 11 500 Anis Hares 200 +212 529 03 68 34 10 500 Alae Yahya 100 9 500 +212 529 03 68 15 0 Sofia Mohcine 8 500 +212 522 49 59 52 oct.-19 oct.-20 juin-19 juin-20 juil.-19 juil.-20 mai-19 mai-20 avr.-19 avr.-20 nov.-19 nov.-20 déc.-19 déc.-20 août-19 août-20 févr.-19 févr.-20 févr.-21 janv.-20 janv.-21 sept.-19 sept.-20 mars-19 mars-20 28/02/2019 31/03/2019 30/04/2019 31/05/2019 30/06/2019 31/07/2019 31/08/2019 30/09/2019 31/10/2019 30/11/2019 31/12/2019 31/01/2020 29/02/2020 31/03/2020 30/04/2020 31/05/2020 30/06/2020 31/07/2020 31/08/2020 30/09/2020 31/10/2020 30/11/2020 31/12/2020 31/01/2021 28/02/2021 KEY ECONOMIC RELEASES/EVENTS OVER THE WEEK | Mar. -

11 December 2020

DECEMBER 11 2020 MARKET INSIGHT | MASI | 11 367 pts | MADEX | 9 257 pts | CAPI | 584 MAD Bn | VOLUME | 323 MAD Mn Daily 2,45% Daily 2,51% High 649 MC 323 YTD -6,61% YTD -6,68% Low 467 MB - THE DAY IN REVIEW TOP PERFORMERS BOTTOM PERFORMERS SBM COLORADO At the end of the last trading session 4,0% 2 447,0 -2,0% 48,0 of the week, the MASI index rose significantly by 2.45% to 11,367 LABEL VIE CTM points. In this context, the annual 3 310,0 -1,9% 696,3 underperformance of the market settles at -6.61%. WAFA ASSURANCE MANAGEM 3 910,0 -0,7% 1 090,0 SBM is among the highest increases up 4,0% while Colorado declined by HPS IMMORENTE 2.0%, i.e. the strongest decrease. 6 135,0 -0,5% 92,5 RDS STOKVIS 27,5 -0,4% 11,1 MOST ACTIVE (MAD Mn) LARGEST CAP (MAD Bn) ATTIJARIWAFA BANK IAM Volume on the central market 60 2,9% 129 reached MAD 323 Mn. LAFARGEHOLCIM MAROC ATTIJARIWAFA BANK Among the most active stocks, we 57 3,9% 90 note Attijariwafa bank and LafargeHolcim Maroc with respective volumes of MAD 60 Mn and MAD 57 CIMAR BCP 29 51 Mn. IAM LAFARGEHOLCIM MAROC 2,1% 38 BCP BOA 26 1,2% 32 3,3% Attijari Global Research Mahat Zerhouni MASI INDEX EVOLUTION (pts) ADV- MONTHLY BASIS VOLUME (MAD Mn) +212 529 03 68 16 [email protected] 500 13 500 400 12 500 Attijari Intermédiation 300 11 500 Anis Hares 200 +212 529 03 68 34 10 500 Kaoutar Sbiyaa 100 9 500 +212 529 03 68 21 0 Alae Yahya 8 500 +212 529 03 68 15 oct.-19 oct.-20 juin-19 juin-20 juil.-19 juil.-20 mai-19 mai-20 avr.-19 avr.-20 nov.-18 nov.-19 nov.-20 déc.-18 déc.-19 août-19 août-20 févr.-19 févr.-20 janv.-19 janv.-20 sept.-19 sept.-20 mars-19 mars-20 30/11/2018 31/12/2018 31/01/2019 28/02/2019 31/03/2019 30/04/2019 31/05/2019 30/06/2019 31/07/2019 31/08/2019 30/09/2019 31/10/2019 30/11/2019 31/12/2019 31/01/2020 29/02/2020 31/03/2020 30/04/2020 31/05/2020 30/06/2020 31/07/2020 31/08/2020 30/09/2020 31/10/2020 30/11/2020 Wafa Bourse Sofia Mohcine +212 522 49 59 52 KEY ECONOMIC RELEASES/EVENTS OVER THE WEEK | Dec. -

26 November 2020

NOVEMBER 26 2020 MARKET INSIGHT | MASI | 11 032 pts | MADEX | 8 985 pts | CAPI | 568 MAD Bn | VOLUME | 73 MAD Mn Daily -0,66% Daily -0,68% High 649 MC 73 YTD -9,36% YTD -9,42% Low 467 MB - THE DAY IN REVIEW TOP PERFORMERS BOTTOM PERFORMERS STROC CARTIER SAADA At the end of this trading session, 4,0% 18,9 -3,5% 28,5 the MASI index decreased by 0.66% to 11,032 points. In this context, the DELATTRE LEVIVIER WAFA ASSURANCE annual underperformance of the 42,6 -3,2% 3 610,0 market settles at -9.36%. ENNAKL INVOLYS Stroc Industrie showed the highest 3,8% 27,5 -2,9% 118,0 increase up 4,0% while Cartier Saada declined by -3.5% i.e. the MED PAPER CIH strongest decrease. 3,7% 14,7 250,6 HPS TAQA MOROCCO 3,6% 5 799,0 -2,0% 945,7 MOST ACTIVE (MAD Mn) LARGEST CAP (MAD Bn) LABEL VIE IAM Volumes traded on the central market 20 0,0% 126 amounted to MAD 73 Mn. IAM ATTIJARIWAFA BANK These were driven by Label Vie and 14 -0,7% 86 -1,7% Maroc Telecom which monopolized 47% of the total flow. HPS BCP 5 3,6% 50 -0,3% ATTIJARIWAFA BANK LAFARGEHOLCIM MAROC -1,7% -0,4% 4 37 BMCI BOA 3 2,1% 32 -1,3% Attijari Global Research Mahat Zerhouni MASI INDEX EVOLUTION (pts) ADV- MONTHLY BASIS VOLUME (MAD Mn) +212 529 03 68 16 [email protected] 500 13 500 400 12 500 Attijari Intermédiation 300 11 500 Anis Hares 200 +212 529 03 68 34 10 500 Kaoutar Sbiyaa 100 9 500 +212 529 03 68 21 0 Alae Yahya 8 500 +212 529 03 68 15 oct.-18 oct.-19 oct.-20 juin-19 juin-20 juil.-19 juil.-20 mai-19 mai-20 avr.-19 avr.-20 nov.-18 nov.-19 déc.-18 déc.-19 août-19 août-20 févr.-19 févr.-20 janv.-19 janv.-20 sept.-19 sept.-20 mars-19 mars-20 30/11/2018 31/12/2018 31/01/2019 28/02/2019 31/05/2019 30/06/2019 31/07/2019 31/10/2019 30/11/2019 31/12/2019 30/04/2020 31/05/2020 30/06/2020 30/09/2020 31/10/2020 30/10/2018 31/03/2019 30/04/2019 31/08/2019 30/09/2019 31/01/2020 29/02/2020 31/03/2020 31/07/2020 31/08/2020 Wafa Bourse Sofia Mohcine +212 522 49 59 52 KEY ECONOMIC RELEASES/EVENTS OVER THE WEEK | Nov. -

Rapport De Gestion 2016

Rapport de gestion 2016 Sommaire Environnement économique........................................................................................6 Monde Afrique Maroc Environnement Bancaire et Financier.............................................................12 Afrique Maroc Analyse des résultats du Groupe..........................................................................18 Activité au Maroc Résultats sociaux Affectation du résultat Activité et résultats des principales filiales Résultats consolidés Gestion Globale des Risques ...................................................................................30 Mission et Organisation de la GGR Dispositions Générales Risque de Crédit Risque Marché Risque Pays Risque Opérationnel & PCA Risk Management Gestion ALM Pilier III : Risques et adéquation des fonds propres ........................56 Résolutions de l’Assemblée Générale Ordinaire...................................66 Comptes consolidés...........................................................................................................68 Comptes sociaux................................................................................................................100 Contacts.......................................................................................................................................124 Europe Afrique du Nord CEMAC UEMOA Aquisition en cours de closing ATTIJARIWAFA BANK : UN GROUPE BANCAIRE ET FINANCIER A VOCATION INTERNATIONALE Europe Afrique du Nord CEMAC UEMOA Aquisition en cours de closing -

Market Summary → International Markets

Week from 08/04/2014 to 08/08/2014 Market Summary 2 International Markets 2 Market and Sector News 3 At the international level Italy: The country back into recession At the national level Banking liquidity: The deficit worsens Consumer Credit: The LOP months seductive Financial Institutions: Fitch Ratings maintains its rating Dairy products: Reny Picot arrives in Morocco Telecommunications: Rates fall Addoha: Buckle its bond Afriquia Gas: Development Program in 2017 CDM: Capital increase CIH Bank: Massira Capital Management reduced its stake ... Holmarcom strengthens Lafarge: Special dividend approved Managem: Lifting 1bn MAD Fundamental Data 5 Technical Data 67 5 6 1 3 Market Summary MARKET PERFORMANCE Performance Weekly evolution for Moroccan indexes vs. volume INDEXES Value Weekly 2014 40 101 MASI 9 426,32 1,09% 3,43% 35 101 MADEX 7 699,47 1,10% 3,79% 101 30 FTSE CSE 15 9 060,30 1,03% 2,69% 101 25 FTSE CSE All 8 114,66 1,31% 4,55% 101 20 100 Capi. (Billions of MAD) 463,84 0,38% 2,82% 15 100 100 10 MARKET VOLUME OF THE WEEK 100 5 In Millions of MAD VOLUME % ADV* 100 0 99 Central Market 157,43 100,00% 31,49 OTC Market 0,00 0,00% 0,00 8/4 8/5 8/6 8/7 8/8 Global Market 157,43 100,0% 31,49 CM vol ume O TC vol ume M ASI M ADEX * Average Daily Volume A week in an upward trend for the Moroccan market. Indeed, both indicators showed a weekly change of +1.09% for MASI and +1.03% for the FTSE 15, bringing their annual performances respectively to +3.43 % and +2.69%. -

Exploratory Study on the Impact of the Transition to IAS/IFRS on Moroccan Groups —Case of Performance Indicators

Open Journal of Business and Management, 2021, 9, 1527-1544 https://www.scirp.org/journal/ojbm ISSN Online: 2329-3292 ISSN Print: 2329-3284 Exploratory Study on the Impact of the Transition to IAS/IFRS on Moroccan Groups —Case of Performance Indicators Rachid El Oud, Yassine Haitou, Abderrahim Amedjar Laboratory of Economics, Management and Business Administration, Hassan First University, Settat, Morocco How to cite this paper: El Oud, R., Haitou, Abstract Y., & Amedjar, A. (2021). Exploratory Study on the Impact of the Transition to IAS/IFRS Since the entry into force of IAS/IFRS in 2005, the issue of the impact of on Moroccan Groups. Open Journal of Busi- IAS/IFRS on economic and financial performance has been a complex debate ness and Management, 9, 1527-1544. in EU member countries. Indeed, several studies have been carried out in this https://doi.org/10.4236/ojbm.2021.94082 context, such as Spain (Callao et al., 2007), France (Boukari & Richard, 2007), Received: February 5, 2021 Canada (Blanchette et al., 2011) … With the exception of the research carried Accepted: June 7, 2021 out by Ahsina et al. in 2014, the analysis of the impact of the adoption of IFRS Published: June 10, 2021 on companies listed on the Casablanca stock exchange has so far remained Copyright © 2021 by author(s) and non-existent in the case of Morocco. As a result, our article aims to study and Scientific Research Publishing Inc. analyse the impact of the first “IFRS 1” transition on the 16 listed groups on This work is licensed under the Creative the Moroccan financial market.