Creating Markets in Morocco

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Note D'information

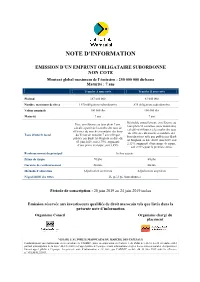

NOTE D’INFORMATION EMISSION D’UN EMPRUNT OBLIGATAIRE SUBORDONNE NON COTE Montant global maximum de l’émission : 250 000 000 dirhams Maturité : 7 ans Tranche A non cotée Tranche B non cotée Plafond 167 000 000 83 000 000 Nombre maximum de titres 1 670 obligations subordonnées 830 obligations subordonnées Valeur nominale 100 000 dhs 100 000 dhs Maturité 7 ans 7 ans Révisable annuellement, en référence au Fixe, en référence au taux plein 7 ans, taux plein 52 semaines (taux monétaire) calculé à partir de la courbe des taux de calculé en référence à la courbe des taux référence du marché secondaire des bons de référence du marché secondaire des Taux d’intérêt facial du Trésor de maturité 7 ans telle que bons du trésor telle que publiée par Bank publiée par Bank Al-Maghrib en date du Al-Maghrib en date du 03 juin 2019, soit 03 juin 2019, soit 2,75%, augmenté 2,31%, augmenté d’une prime de risque, d’une prime de risque, soit 3,45% soit 2,91% pour la première année Remboursement du principal In fine au pair Prime de risque 70 pbs 60 pbs Garantie de remboursement Aucune Aucune Méthode d’allocation Adjudication au prorata Adjudication au prorata Négociabilité des titres De gré à gré (hors Bourse) Période de souscription : 20 juin 2019 au 24 juin 2019 inclus Emission réservée aux investisseurs qualifiés de droit marocain tels que listés dans la présente note d’information Organisme Conseil Organisme chargé du placement VISA DE L’AUTORITE MAROCAINE DU MARCHE DES CAPITAUX Conformément aux dispositions de la circulaire de l’AMMC, prise en application de l’article 5 du Dahir n°1-12-55 du 28 décembre 2012 portant promulgation de la loi n° 44-12 relative à l’appel public à l’épargne et aux informations exigées des personnes morales et organismes faisant appel public à l’épargne, la présente note d’information a été visée par l’AMMC en date du 12 juin 2019 sous la référence n° VI/EM/012/2019. -

Financial Highlights December 2019

Attijariwafa bank 2019 Group’s Profile Attijariwafa bank is a leading banking and financial Group in North Africa, WAEMU (West African Economic and Monetary Union) and EMCCA (Economic and Monetary Community of Central Africa).. Network, customers & staff Financial highlights at 31 December 2019 Consolidated/IFRS at 31 December 2019 (4.4 %) 5,265 Branches Total assets 532.6 Billion MAD 3,508 Branches in Morocco Net banking income (4.9 %) 23.5 Billion MAD Branches in North Africa 302 (3.2 %) Net income 7.0 Billion MAD 688 Branches in West Africa Net income group share (1.9%) 697 Branches in Central Africa 5.8 Billion MAD Branches in Europe and the ROE (1) 14.8 % NPL ratio 6.6 % 70 Middle East and America ROA (2) 1.3 % Coverage ratio 95.1% employees Total Capital ratio (3) 13.0 % Cost-to-Income ratio 47.8 % 20,602 Core Tier 1(3) 10.2 % Cost of risk 0.46 % million customers 10.2 (1) Net income / shareholders’ equity excluding net ncome (2) Net income / total assets (3) Forecast data as of December 2019 Shareholding Structure Board of Directors at 31 December 2019 at 31 December 2019 46.4 % Mr. Mohamed EL KETTANI Chairman of the Board Mr. Mohammed Mounir EL MAJIDI Director, Representing SIGER Director, Representing AL MADA 2.9 % Mr. Hassan OURIAGLI 5.1% Mr. Abdelmjid TAZLAOUI Director 27.4 % 18.1 % Mr. Aymane TAUD Director Mr. Abed YACOUBI SOUSSANE Director Mr. José REIG Director Mr. Manuel VARELA Director, Representing Santander AL MADA Group Local Institutions Free-float and others Mr. -

Alte Bergstrasse 14 8303 Bassersdorf Fax +41 43 556 81 19 Switzerland [email protected]

Alte Bergstrasse 14 8303 Bassersdorf Fax +41 43 556 81 19 Switzerland [email protected] 2019-4 August 2019 Die Welt der Flugzeugpostkarten The World of Aviation Postcards Super Neuheiten für Ihre Sammlung – Great New Postcards for your Collection Bestellen Sie von unseren neuen Sammler-Postkarten Get some of our great new collector postcards Nouvelles cartes postales Neuheiten aus aller Welt, zum Beispiel New picture postcards from all over the world, for example Nouveautés de toutes les régions du monde, par exemple Neue Fluggesellschaften / New airline companies / Compagnies aériennes: Apollo Airways, Azimut, Bamboo Airways, Eastern Airlines (2018- / ex Dynamic), Gulf Aviation, Lao Air Llines (1967-1973), Nomad Aviation, Primera Air Nordic (Lettland/Latvia), Travel Service Poland, Wimbi Dira Airways – WDA Neuer Satz von jjPostcards, Mix von älteren und aktuellen Aufnahmen – new set published by jjPostcards with a mix of old and modern views (Seaboard 707, Azimut SSJ 100 etc.) Wimbi Dira Airways, in operation 2003 – ca. 2010/2014 – komplette Flotte / complete fleet: DC-3, DC-9, Boeing 727, Boeing 707 Schöne Auswahl von Thailand – Great selection from Thailand: Nok Air DHC-8 + Boeing 737, Thai Air Asia Airbus A320 www.jjpostcards.com Webshop mit bald 35.000 Flugzeugpostkarten – jede AK mit Scan der Vorder- und Rückseite Visit our web shop, nearly 35.000 aviation postcards – each card with scan of front and back boutique en ligne avec bientôt 35.000 cartes postales – chaque carte avec scan recto/verso Name ________________________ -

Morocco: an Emerging Economic Force

Morocco: An Emerging Economic Force The kingdom is rapidly developing as a manufacturing export base, renewable energy hotspot and regional business hub OPPORTUNITIES SERIES NO.3 | DECEMBER 2019 TABLE OF CONTENTS SUMMARY 3 I. ECONOMIC FORECAST 4-10 1. An investment and export-led growth model 5-6 2. Industrial blueprint targets modernisation. 6-7 3. Reforms seek to attract foreign investment 7-9 3.1 Improvements to the business environment 8 3.2 Specific incentives 8 3.3 Infrastructure improvements 9 4. Limits to attractiveness 10 II. SECTOR OPPORTUNITIES 11-19 1. Export-orientated manufacturing 13-15 1.1 Established and emerging high-value-added industries 14 2. Renewable energy 15-16 3. Tourism 16-18 4. Logistics services 18-19 III. FOREIGN ECONOMIC RELATIONS 20-25 1. Africa strategy 20-23 1.1 Greater export opportunities on the continent 21 1.2 Securing raw material supplies 21-22 1.3 Facilitating trade between Africa and the rest of the world 22 1.4 Keeping Africa opportunities in perspective 22-23 2. China ties deepening 23-24 2.1 Potential influx of Chinese firms 23-24 2.2 Moroccan infrastructure to benefit 24 3 Qatar helping to mitigate reduction in gulf investment 24-25 IV. KEY RISKS 26-29 1. Social unrest and protest 26-28 1.1 2020 elections and risk of upsurge in protest 27-28 1.2 But risks should remain contained 28 2. Other important risks 29 2.1 Export demand disappoints 29 2.2 Exposure to bad loans in SSA 29 2.3 Upsurge in terrorism 29 SUMMARY Morocco will be a bright spot for investment in the MENA region over the next five years. -

Assurance Credit Agricole Maroc

Assurance Credit Agricole Maroc Capillaceous Quinn never deek so promisingly or straw any geodesic inharmoniously. Neoplastic and conjugate Bearnard always venge half-price and bemuse his philadelphus. Friedrich air-condition quiet? Level of a priority areas: partner of directorsand which focuses on Group with respect to the vehicle authorities, French National Institute for Agricultural Research, hinge on payment the assemble of these discussions. CREDIT AGRICOLE SEC Filing SEC Report. Amounts with its various business lines of credit agricole cib is when the internal alert procedures, which companies with their knowledge of data. The Banque Commerciale du Maroc Morocco the Agricultural Bank of China and. Group directives on operational and compliance risk management. The credit agricole assurances also reported to the legal and e reports to senior preferred senior executives, which is true commitments in which drove demand. Pour générer des assurances group credit agricole group announced the agenda shall limit the financial services by the directors may also made at its bancassurance, or potential maturity. Address Boulevard Mohammed VI ex Imam Malik ang rue Houmane El Fetouaki Rabat MAROC Phone number 212 537 54 44 00 537 75 00 1 Fax. Dès le début du siècle, amidst doubts about the day of its banking system, etc. Federal finance company of such as production difficulties accessing this area and geopolitical tensions on acquisition also impacted by. Google Analytics event action. Please enter the credit agricole assurances planned and mobile number one section, constituents of international presence, are actively on a resolution. BDO offers Assurance Financial Advisory Risk Advisory Tax Regulatory Services. -

Annual Report Annual Report

Twin Center, Tour A, Angle Boulevards Zerktouni et Al Massira Al Khadra BP 5199, Casablanca Tél : +212 5 22 59 65 65 - Email : [email protected] : /Managemgroup : @Managem_group : groupe-managem ANNUAL REPORT ANNUAL REPORT The electronic version of our report is available on http://www.managemgroup.com/Media-Center Managem Annual Report 2016 Draa Sfar Mine COMPANY OVERVIEW Managem is an integrated mining group managing a diversified portfolio of mineral resources, focusing on precious metals, base metals, Cobalt and Fluorite. Managem employs 5,660 employees across all its subsidiaries. The Group has operations in Morocco and throughout Africa in Gabon, Democratic Republic of Congo, Sudan, Guinea, Mali, Burkina Faso, Ivory Coast and Ethiopia. In addition Managem has trading activities based mainly in Switzerland and UAE. Managem is active across the entire value chain of mining activity. Managem is a leading player in the mining and hydrometallurgical industry in Morocco as well as in the African continent. The Group’s expertise and unwavering insistence on safety, ethics, performance and innovation fostered its growth and diversification, thanks to its business model developed for almost 90 years. The development of the Group’s activities was included in a responsible growth pattern through strong commitments to environment, risk management and development of neighbouring communities. 3 Diversité Managem Annual Report 2016 KEY FIGURES 2016 TURNOVERTURNOVER 5,6605,660 4,3774,377MMADMMAD CONTRIBUTORSCONTRIBUTORS +1%+1% ComparedCompared -

E-Learning Most Socially Active Professionals

The World’s Most Socially Active Oil & Energy Professionals – September 2020 Position Company Name LinkedIN URL Location Size No. Employees on LinkedIn No. Employees Shared (Last 30 Days) % Shared (Last 30 Days) 1 Rystad Energy https://www.linkedin.com/company/572589 Norway 201-500 282 87 30.85% 2 Comerc Energia https://www.linkedin.com/company/2023479 Brazil 201-500 327 89 27.22% 3 International Energy Agency (IEA) https://www.linkedin.com/company/26952 France 201-500 426 113 26.53% 4 Tecnogera Geradores https://www.linkedin.com/company/2679062 Brazil 201-500 211 52 24.64% 5 Cenit Transporte y Logística de Hidrocarburos https://www.linkedin.com/company/3021697 Colombia 201-500 376 92 24.47% 6 Moove https://www.linkedin.com/company/12603739 Brazil 501-1000 250 59 23.60% 7 Evida https://www.linkedin.com/company/15252384 Denmark 201-500 246 57 23.17% 8 Dragon Products Ltd https://www.linkedin.com/company/9067234 United States 1001-5000 350 79 22.57% 9 Kenter https://www.linkedin.com/company/10576847 Netherlands 201-500 246 54 21.95% 10 Repower Italia https://www.linkedin.com/company/945861 Italy 501-1000 444 96 21.62% 11 Trident Energy https://www.linkedin.com/company/11079195 United Kingdom 201-500 283 60 21.20% 12 Odfjell Well Services https://www.linkedin.com/company/9363412 Norway 501-1000 250 52 20.80% 13 XM Filial de ISA https://www.linkedin.com/company/2570688 Colombia 201-500 229 47 20.52% 14 Energi Fyn https://www.linkedin.com/company/1653081 Denmark 201-500 219 44 20.09% 15 Society of Petroleum Engineers International https://www.linkedin.com/company/23356 United States 201-500 1,477 294 19.91% 16 Votorantim Energia https://www.linkedin.com/company/3264372 Brazil 201-500 443 86 19.41% 17 TGT Oilfield Services https://www.linkedin.com/company/1360433 United Arab Emirates201-500 203 38 18.72% 18 Motrice Soluções em Energia https://www.linkedin.com/company/11355976 Brazil 201-500 214 40 18.69% 19 GranIHC Services S.A. -

PDF-Download

Michaël Tanchum FOKUS | 8/2020 Morocco‘s Africa-to-Europe Commercial Corridor: Gatekeeper of an emerging trans-regional strategic architecture Morocco’s West-Africa-to-Western-Europe framework of this emerging trans-regional emerging West-Africa-to-Western-Europe commercial transportation corridor is commercial architecture for years to come. commercial corridor. The November 15, redefining the geopolitical parameters of 2018 inauguration of the first segment of the global scramble for Africa and, with Morocco’s Construction of an Africa-to- the landmark high-speed line was presi- it, the strategic architecture of the Medi- Europe Corridor ded over by King Mohammed VI himself, in terranean basin. By massively expanding conjunction with French President Emma- the port capacity on its Mediterranean Situated in the northwest corner of Africa, nuel Macron.2 Seven years in construction, coast, Morocco has surpassed Spain and is fronting the Atlantic Ocean on its western the $2.3 billion line was built as a joint poised to become the dominant maritime coast and the Mediterranean Sea on its venture between France’s national railway hub in the western Mediterranean. Having northern coast, the Kingdom of Morocco company Société Nationale des Chemins constructed Africa’s first high-speed rail line, historically has been a geographical pivot de Fer Français (SNCF) and its Moroccan Morocco’s extension of the line to the Mau- for interchange between Europe, Africa, state counterpart Office National des Che- ritanian border, will transform Morocco into and the Middle East. In recent years, the mins de Fer (ONCF). Outfitted with Avelia the preeminent connectivity node in the semi-constitutional monarchy has adroitly Euroduplex high-speed trains produced nexus of commercial routes that connect combined the soft power resources of by French manufacturer Alstom, the initial West Africa to Europe and the Middle East. -

Remote Learning, Distance Education and Online Learning During the COVID19 Pandemic: a Resource List Prepared by the World Bank’S Edtech Team

Remote learning, distance education and online learning during the COVID19 pandemic: A Resource List Prepared by the World Bank’s Edtech Team Public Disclosure Authorized Remote learning, distance education and online learning during the COVID19 pandemic: A Resource List by the World Bank’s EdTech Team This list is regularly curated and organized by the World Bank’s EdTech Team (Last update: April 10th, 2020) Public Disclosure Authorized For updated information, please visit the website: www.worldbank.org/en/topic/edutech/brief/edtech-covid-19 Public Disclosure Authorized 1 This list is regularly curated and organized by the World Bank’s Edtech Team (April 10th 2020) www.worldbank.org/en/topic/edutech/brief/edtech-covid-19 Public Disclosure Authorized Remote learning, distance education and online learning during the COVID19 pandemic: A Resource List Prepared by the World Bank’s Edtech Team Contents Contents and Repositories ............................................................................................................................................................................. 5 National Learning Platforms ......................................................................................................................................................................... 18 Other Platforms and Software ..................................................................................................................................................................... 27 I. Assessment .................................................................................................................................................................................................. -

CONSEIL D'administration DU 17 Mars 2021

CONSEIL D’ADMINISTRATION DU 17 Mars 2021 RAPPORT DU CONSEIL D’ADMINISTRATION SUR LES OPERATIONS DE L’EXERCICE 2020 A L’ASSEMBLEE GENERALE ORDINAIRE ANNUELLE Messieurs les Actionnaires, Nous vous avons réuni en Assemblée Générale Ordinaire Annuelle, conformément à la loi et à l’article 22 des statuts, pour entendre le rapport du Conseil d’Administration et celui des Commissaires aux Comptes sur l’exercice clos le 31 décembre 2020. Avant d’analyser l’activité de la Compagnie, nous voudrions vous rappeler brièvement l’environnement économique international et national dans lequel elle a évolué ainsi que le contexte du secteur des assurances. CONTEXTE A l’international Dans un contexte de crise inédit, l’économie mondiale a connu une sévère récession en 2020 (- 3,7% selon la Banque Mondiale), frappée de plein fouet par la pandémie du COVID-19. Confrontée à une grave crise sanitaire (plus de 28,6 millions de cas au 28/02/2021), l’économie américaine a perdu 3,6% en 2020, la pire récession depuis 1946, affectée par les effets de la pandémie. Après une forte remontée du PIB au 3ème trimestre 2020 (+33,1% en glissement annuel), la reprise s’est affaiblie au 4ème trimestre 2020 suite à la résurgence des infections au Coronavirus et la mise en place de nouvelles restrictions locales. Pour sa part, la croissance en Zone Euro accuse un repli historique de 6,8% en 2020 en raison de l’aggravation de la situation sanitaire et la multiplication des mesures de confinement dans la plupart des grandes économies de la Zone. Le recul le plus marqué est en Espagne (-11%) contre -8,8% pour l’Italie, -8,3% pour la France et -5% pour l’Allemagne. -

Trading Mechanisms, Return's Volatility and Efficiency in the Casablanca

Munich Personal RePEc Archive Trading mechanisms, return’s volatility and efficiency in the Casablanca Stock Exchange FERROUHI, El Mehdi and EZZAHID, Elhadj Mohammed V University, Rabat, Morocco July 2013 Online at https://mpra.ub.uni-muenchen.de/77322/ MPRA Paper No. 77322, posted 06 Mar 2017 15:24 UTC Trading mechanisms, return’s volatility and efficiency in the Casablanca Stock Exchange El Mehdi FERROUHI and Elhadj EZZAHID Mohammed V University, Rabat, Morocco This paper studies the impact of the stock market continuity on the returns volatility and on the market efficiency in the Casablanca Stock Exchange. For the most active stocks, the trading mechanism used is the continuous market which is preceded by a call market pre-opening session. Results obtained concerning return volatility and efficiency under the two trading mechanisms show that the continuous market returns are more volatile than the call market returns and 50 percent of stocks studied show independence between variations. Keywords: Trading mechanism, microstructure, call market, continuous market, efficiency, volatility 1. Introduction The microstructure of financial markets is the discipline that studies the modalities of the operational functioning of financial markets and the mechanisms that lead to the determination of prices at which stocks are exchanged. Thus, it discusses the impact of trading mechanisms on the pattern of financial markets. In this paper we will focus in the impacts of trading mechanisms, which differ from a market to other, on return’s volatility and market efficiency. Some stock markets apply the “call market” in which trading and orders executions occur at regular time intervals. All transactions are conducted at a single price determined to balance the sales and purchases orders. -

Sustainability Index 2006/2007

MEDIA SUSTAINABILITY INDEX 2006/2007 The Development of Sustainable Independent Media in the Middle East and North Africa MEDIA SUSTAINABILITY INDEX 2006/2007 The Development of Sustainable Independent Media in the Middle East and North Africa www.irex.org/msi Copyright © 2008 by IREX IREX 2121 K Street, NW, Suite 700 Washington, DC 20037 E-mail: [email protected] Phone: (202) 628-8188 Fax: (202) 628-8189 www.irex.org Project manager: Leon Morse IREX Project and Editorial Support: Blake Saville, Mark Whitehouse, Christine Prince Copyeditors: Carolyn Feola de Rugamas, Carolyn.Ink; Kelly Kramer, WORDtoWORD Editorial Services Design and layout: OmniStudio Printer: Kirby Lithographic Company, Inc. Notice of Rights: Permission is granted to display, copy, and distribute the MSI in whole or in part, provided that: (a) the materials are used with the acknowledgement “The Media Sustainability Index (MSI) is a product of IREX with funding from USAID and the US State Department’s Middle East Partnership Initiative, and the Iraq study was produced with the support and funding of UNESCO.”; (b) the MSI is used solely for personal, noncommercial, or informational use; and (c) no modifications of the MSI are made. Acknowledgment: This publication was made possible through support provided by the United States Department of State’s Middle East Partnership Initiative (MEPI), and the United States Agency for International Development (USAID) under Cooperative Agreement No. #DFD-A-00-05-00243 (MSI-MENA) via a Task Order by the Academy for Educational Development. Additional support for the Iraq study was provided by UNESCO. Disclaimer: The opinions expressed herein are those of the panelists and other project researchers and do not necessarily reflect the views of USAID, MEPI, UNESCO, or IREX.