Rating Report Sun Life Financial Inc

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Area Companies Offering Matching Gifts Below Is a Partial List of Area Companies Offering Matching Gifts

Area Companies Offering Matching Gifts Below is a partial list of area companies offering matching gifts. Please check to see if your employer is on the list and/or check with your company if they offer the program. If your employer offers a matching gift program, please request a matching gift form from your employer or fill out their online form. Matching gifts can be made to the Tredyffrin Township Libraries, Paoli Library or Tredyffrin Public Library. Aetna FMC Corporation PNC Financial Services AIG GATX PPG Industries Air Products and Chemicals, Inc. GE Foundation PQ Corporation Allstate Foundation GlaxoSmithKline Procter & Gamble Altria Group, Inc. Glenmede Prudential Financial American Express Company Hillman Company PVR Partners, L.P. American International Group, Inc. Houghton Mifflin Quaker Chemical Corporation AmeriGas Propane, Inc. IBM Corporation Quest Diagnostics AON J.P. Morgan Chase Ross Arkema Inc. John Hancock Saint-Gobain Corporation Automatic Data Processing Johnson & Johnson Sandmeyer Steel Company AXA Foundation, Inc. JP Morgan Chase SAP Matching Gift Program Axiom Data, Inc. Kaplan Inc. Schering-Plough Foundation Bank of America Kellogg Schroder Investment Management Bemis Company Foundation KPMG LLP Shell Oil Company Berwind Corporation Liberty Mutual State Farm Companies Foundation BlackRock Lincoln Financial Group Subaru of America Boeing Company May Department Stores Sun Life Financial BP McDonald's Sun Microsystems, Inc Bristol-Myers Squibb Company McKesson Foundation Sunoco, Inc. C. R. Bard, Inc. Merck & Co., Inc. Tenet Healthcare Foundation CertainTeed Merrill Lynch Texas Instruments Charles Schwab Merrill Lynch ACE INA Foundation Chevron Corporation Microsoft AXA Foundation Chubb Group of Insurance Companies Minerals Technologies Inc. Dow Chemical Company CIGNA Foundation Mobil Foundation Inc. -

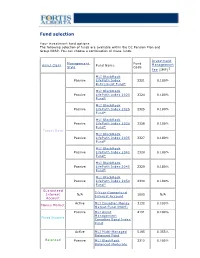

Fund Selection

Fund selection Y our investment fund options The following selection of funds are available within the DC Pension Plan and Group RRSP. You can choose a combination of these funds. Investment Management Fund Asset Class Fund Name Management Style Code Fee (IMF)1 MLI BlackRock Passive LifeP ath Index 2321 0.180% Retirement Fund* MLI BlackRock Passive LifeP ath Index 2020 2324 0.180% Fund* MLI BlackRock Passive LifeP ath Index 2025 2325 0.180% Fund* MLI BlackRock Passive LifeP ath Index 2030 2326 0.180% Fund* Target Date MLI BlackRock Passive LifeP ath Index 2035 2327 0.180% Fund* MLI BlackRock Passive LifeP ath Index 2040 2328 0.180% Fund* MLI BlackRock Passive LifeP ath Index 2045 2329 0.180% Fund* MLI BlackRock Passive LifeP ath Index 2050 2330 0.180% Fund* Guaranteed 5-Y ear Guaranteed Interest N/A 1005 N/A Interest Account Account Active MLI Canadian Money 3132 0.100% Money Market Market Fund (MAM) Passive MLI Asset 4191 0.100% Management Fixed Income Canadian Bond Index Fund Active MLI Multi-Managed 5195 0.355% Balanced Fund Balanced Passive MLI BlackRock 2312 0.105% Balanced Moderate Index Fund Active MLI Canadian Equity 7011 0.210% Fund Canadian Passive MLI Asset 7132 0.100% Equity Management Canadian Equity Index Fund Active MLI U.S. Diversified 8196 0.375% Grow th Equity (Wellington) Fund U.S. Equity Passive MLI BlackRock U.S. 8322 0.090% Equity Index Fund* Active MLI MFS MB 8162 0.280% International Equity International Fund Equity Passive MLI BlackRock 8321 0.160% International Equity Index Fund* 1 IMFs shown do not include applicable taxes. -

NP Key Contacts.Pdf

IGP Network Partners: Key Contacts Region: Americas Country / Territory IGP Network Partner IGP Contact Email Type IGP Regional Coordinator Mr. Michael Spincemaille [email protected] Argentina SMG LIFE Mr. Nicolas Passet [email protected] Partner Brazil MAPFRE Vida S.A. Ms. Débora Nunes Santos [email protected] Partner Canada Manulife Financial Corporation Mr. Kajan Ramanathan [email protected] Partner Chile MAPFRE Chile Ms. Nathalie Gonzalez [email protected] Partner Colombia MAPFRE Colombia Ms. Ingrid Olarte Pérez [email protected] Partner Costa Rica MAPFRE Costa Rica Mr. Armando Sevilla [email protected] Partner Dominican Republic (Life) MAPFRE BHD Mrs. Alejandra Quirico [email protected] Partner Dominican Republic (Health) MAPFRE Salud ARS, S. A. Mr. Christian Wazar [email protected] Partner Ecuador MAPFRE Atlas * Mr. Carlos Zambrano [email protected] Correspondent El Salvador MAPFRE Seguros El Salvador S.A. Mr. Daniel Acosta González [email protected] Partner French Guiana Refer to France - - Partner Guadeloupe Refer to France - - Partner Guatemala MAPFRE Guatemala Mr. Luis Pedro Chavarría [email protected] Partner Honduras MAPFRE Honduras Mr. Carlos Ordoñez [email protected] Partner Martinique Refer to France - - Partner Mexico Seguros Monterrey New York Life Ms. Paola De Uriarte [email protected] Partner Nicaragua MAPFRE Nicaragua Mr. Dany Lanuza Flores [email protected] Partner Panama MAPFRE Panama Mr. Manuel Rodriguez [email protected] Partner Paraguay MAPFRE Paraguay Mr. Sergio Alvarenga [email protected] Partner Peru MAPFRE Peru Mr. Ramón Acuña Huerta [email protected] Partner Saint Martin Refer to France - - Partner Saint Barthélemy Refer to France - - Partner Saint Pierre & Miquelon Refer to France - - Partner United States Prudential Insurance Company of America Mr. -

Manulife Global Fund Unaudited Semi-Annual Report

Unaudited Semi-Annual Report Manulife Global Fund Société d'Investissement à Capital Variable for the six month period ended 31 December 2020 No subscription can be received on the basis of nancial reports. Subscriptions are only valid if made on the bases of the current prospectus, accompanied by the latest annual report and semi-annual report if published thereaer. SICAV R.C.S Luxembourg B 26 141 Contents Directors ..................................................................................................................................................... 1 Management and Administration ............................................................................................................. 2 Directors’ Report ........................................................................................................................................ 4 Statement of Net Assets ........................................................................................................................... 10 Statement of Changes in Net Assets ........................................................................................................ 15 Statement of Operations ........................................................................................................................... 20 Statistical Information ............................................................................................................................... 25 Statement of Changes in Shares ............................................................................................................. -

Q1 2020 Building Sustainable Shareholder Value Business Overview

Q1 2020 Building Sustainable Shareholder Value Business overview Update in light of COVID-19 Business group results & highlights Capital management Asset portfolio Sustainability 2 A $26.51 billion leading global financial services organization Offices in 40,600 Employees 125,900 advisors 27 markets 2 2 2 Operating through a balanced and diversified model and focused on creating shareholder value now and in the future SUN LIFE • Q1 2020 1 Market capitalization in C$ as at March 31, 2020 3 2 As at December 31, 2019. Includes Asia joint ventures The Sun Life story • A diversified business model, with four strong pillars that can each compete, win and grow in their respective sectors and which leverage each other • Bound together by a strong balance sheet and risk culture, including no U.S. Variable Annuity or U.S. Long-Term Care • Digital transformation that is deeply embedded throughout the organization • Building on momentum created by past organic investments and acquisitions that will help drive earnings growth SUN LIFE • Q1 2020 4 Executing on our ambition to be one of the best insurance and asset management companies globally A Leader in Insurance and A Leader in U.S. Wealth Solutions in our CAN US Group Benefits Canadian Home Market A Leader in Asia A Leader in Global AM ASIA through Distribution Asset Management Excellence in Higher Growth Markets Each pillar Top quartile Disproportionate Top quartile total viewed as a Client share of top shareholder leader experience talent return SUN LIFE • Q1 2020 5 Consistently delivering value to shareholders 5-year total shareholder return1 Progress on medium-term objectives March 31, 2020 Sun Life 6.9% Medium-term objective Q1 2020 TSX 0.9% Underlying ROE2 12-14% 14.2% Canadian lifecos 0.0% Underlying EPS growth2 9% Global lifecos (1.2)% 8-10% Dividend payout ratio2 U.S. -

2018 Annual Report Fellow Shareholders, Governance and Shareholder Outreach

Manulife Financial Corporation Who Manulife Financial Corporation is Our five Portfolio Optimization we are a leading international financial strategic We are actively managing our priorities services group providing financial 1 legacy businesses to improve advice, insurance, as well as returns and cash generation while wealth and asset management reducing risk. solutions for individuals, groups, and institutions. We operate as John Hancock in the United States Expense Efficiency and Manulife elsewhere. We are getting our cost structure 2 into fighting shape and simplifying and digitizing our processes to position us for efficient growth. Accelerate Growth We are accelerating growth in our 3 highest-potential businesses. Our Digital, Customer Leader mission Decisions We are improving our customer 4 experiences, using digitization and made easierr. innovation to put customers first. Lives High-Performing Team made betterr. We are building a culture that 5 drives our priorities. Our Our Values represent how we Obsess Do the Values operate. They reflect our culture, about right thing inform our behaviours, and help define how we work together. customers Manulife Note: Growth in core earnings, assets under Core Earnings (C$ billions) management and administration (AUMA), and by the new business value are presented on a constant $5.6 billion exchange rate basis. numbers Total Company, Global Wealth and Asset Management (Global WAM), and Asia core earnings up 23%, 21%, and 20%, respectively, from 2017. 5.6 4.6 4.0 3.4 2.9 2014 2015 2016 2017 2018 Assets Under Management and Administration Net Income Attributed to Shareholders (C$ billions) (C$ billions) $1,084 billion $4.8 billion Over $1 trillion in AUMA. -

Demutualization Details

Demutualization Details 1. American Mutual Life – AmerUs- Indianapolis Life Insurance Company - Central Life Assurance - Central Life Assurance merged with American Mutual in 1994. American Mutual Life was renamed AmerUs Life Insurance Company in 1995. On September 20, 2000, it demutualized to become AmerUs Group. In 2001, the company merged with Indianapolis Life, which had also undergone a demutualization. Approximately 300,000 policyholders and heirs became entitled to receive $452 million in AmerUs Group common stock and $340 million in cash and policy credits. Distribution began on July 31, 2001. Eligible policyholders received a fixed component of 20 AmerUS common shares, as well as a variable component based on policy value. Those who elected to receive cash were compensate $26 per share entitlement. In the first year after the initial public offering, the price of an AmerUS common share increased 99%. The current value of AmerUS Group stock is approximately $45 per share. 2. Anthem Insurance - On July 31, 2002 Anthem Insurance Companies, Inc. completed its conversion from a mutual insurance company to a stock company, and became a wholly owned subsidiary of Anthem, Inc. Eligible policyholders and heirs became entitled to approximately 48 million shares of Anthem, Inc. common stock and cash totaling $2.06 billion. Compensation consisted of a fixed component of 21 Anthem common shares, as well as a variable component based on policy value. The shares were offered to the public at $36. In the first year after the initial public offering, the price of an Anthem common share increased 54%. 3. Equitable Life – Axa - In 1992 the Equitable Life Assurance Society of the United States demutualized and a new parent holding company, the Equitable Companies, was listed on the New York Stock Exchange. -

Sun Life Guaranteed Investment Funds (Gifs)

Sun Life Guaranteed Investment Funds (GIFs) ANNUAL FINANCIAL STATEMENTS SUN LIFE ASSURANCE COMPANY OF CANADA December 31, 2015 Life’s brighter under the sun Sun Life Assurance Company of Canada is a member of the Sun Life Financial group of companies. © Sun Life Assurance Company of Canada, 2016. 36D-0092-02-16 Table of Contents Independent Auditors' Report 3 Sun MFS Dividend Income 196 Sun Beutel Goodman Canadian Bond 5 Sun MFS Global Growth 200 Sun BlackRock Canadian Balanced 10 Sun MFS Global Total Return 204 Sun BlackRock Canadian Composite Equity 15 Sun MFS Global Value 209 Sun BlackRock Canadian Equity 20 Sun MFS Global Value Bundle 214 Sun BlackRock Canadian Equity Bundle 25 Sun MFS International Growth 218 Sun BlackRock Cdn Composite Eq Bundle 29 Sun MFS International Growth Bundle 222 Sun BlackRock Cdn Universe Bond 33 Sun MFS International Value 226 Sun Canadian Balanced Bundle 38 Sun MFS International Value Bundle 230 Sun CI Cambridge Canadian Equity 42 Sun MFS Monthly Income 234 Sun CI Cambridge Cdn Asset Allocation 46 Sun MFS US Equity 238 Sun CI Cambridge Global Equity 50 Sun MFS US Equity Bundle 242 Sun CI Cambridge/MFS Canadian Bundle 54 Sun MFS US Growth 246 Sun CI Cambridge/MFS Global Bundle 58 Sun MFS US Value 250 Sun CI Signature Diversified Yield II 62 Sun MFS US Value Bundle 255 Sun CI Signature High Income 66 Sun Money Market 259 Sun CI Signature Income & Growth 70 Sun NWQ Flexible Income 264 Sun Daily Interest 74 Sun PH&N Short Term Bond and Mortgage 268 Sun Dollar Cost Average Daily Interest 78 Sun RBC Global High -

Stfx Enrolment Guide

my money @ work Start saving guide it’s time to save Welcome to my money @ work Millions of Canadians participate in workplace retirement and savings plans. Now, it’s your turn because it’s your money and your future. Saving at work helps you meet your financial goals whether you’re just starting your career, midway through it or close to retirement. And this guide has what you need to get started: practical savings information to help you save and enrol in the Improved Retirement Plan for Teaching, Administration & Other Employees of St. Francis Xavier University. Being part of the Sun Life Financial community has its advantages. From making the most of your workplace plan to helping you plan for your financial future, my money @ work and Sun Life Financial are here for you. To take advantage of your dedicated Sun Life Financial Customer Care Centre representative, call 1-866-733-8612 from 8 a.m. to 8 p.m. ET any business day. Service is available in more than 190 languages. Group Retirement Services are provided by Sun Life Assurance Company of Canada, 2 aSun member Life Financial of the Sun Life Financial group of companies. Three easy steps… 1 READ 4 my money @ work Why save now? My plan What’s in it for me? 2 INVEST 9 my investments A choice of investment approaches Diverse selection of investment options Investment risk profiler 3 ENROL 15 mysunlife.ca It’s action time! We’re with you World of information & tools FORMS 18 my money @ work 3 READ 4 Sun Life Financial my money @ work There is no better way to save for your future than through your plan @ work. -

Manulife's Investor Day 2017 in Hong Kong-Slides-Day 1

June 21, 2017 Hong Kong Agenda Time Speaker Presentation 9:05 am Donald Guloien Delivering on commitments, driving shareholder value & preparing for the future 9:20 am Roy Gori A compelling opportunity and clear priorities to win 9:40 am Steve Roder Commitment to shareholder value creation 10:10 am Q&A Session 10:45 am Roy Gori & Phil Witherington Executing on our Asia opportunity 11:30 am Q&A Session 11:55 am Various Labs 12:25 pm Lunch with Guest Speaker 1:40 pm Linda Mantia Driving Customer Centricity and Innovation 2:10 pm Q&A Session 2:25 pm Various Labs 3:05 pm Kai Sotorp A global wealth and asset management platform with solid growth momentum 3:35 pm Q&A Session 3:50 pm Various Labs Caution regarding forward-looking statements From time to time, MFC makes written and/or oral forward-looking statements, including in this presentation. In addition, our representatives may make forward-looking statements orally to analysts, investors, the media and others. All such statements are made pursuant to the “safe harbour” provisions of Canadian provincial securities laws and the U.S. Private Securities Litigation Reform Act of 1995. The forward-looking statements in this presentation include, but are not limited to, statements with respect to demographic and market trends and their expected benefit, core ROE expansion over the medium term and the drivers of such expansion, our expected dividend payout ratio, annual core earnings per share growth over the medium term and dividend growth over time. The forward-looking statements in this presentation -

Approved Panel of Providers

BROOKLIGHT PLACE SECURITIES, INC. 16930 E Palisades Blvd. Suite #100-D Fountain Hills, AZ 85268 Toll Free: 1-888-976-0659 Member FINRA & SIPC Approved Panel of Providers For representative use only – Updated January 22, 2019 Mutual Funds First Eagle Funds PGIM Investments AIG Funds Firsthand Funds PIMCO Funds Alger Franklin Templeton Investments Pacific Funds AllianceBernstein Goldman Sachs Funds Principal Funds Allianz Global Investor Hartford Funds ProFunds American Century Investments Heartland Advisors Putnam Investments American Funds Highmark Funds (Pyxis) Pyxis Funds AMG Funds ICON Funds Royce Funds Amundi Pioneer Asset Management Invesco Salient Funds Aquila Group of Funds Ivy Funds (Waddell & Reed) Sammons Retirement Solutions LiveWell Ariel Investments Janus Funds Selected Funds Blackrock Funds John Hancock Investments SunAmerica Funds Calamos Investments JP Morgan Funds Thornburg Investment Management Calvert Funds Keeley Funds Timothy Plan Mutual Funds Colorado Bond Shares Legg Mason Mutual Funds T. Rowe Price Columbia Threadneedle Investments Lord Abbett Mutual Funds Touchstone Investments Davis Funds MFS Funds Transamerica (IDEX) Funds Delaware Funds by Macquarie Nationwide Funds Van Eck Funds Dodge & Cox Natixis Funds Vanguard Dreyfus Family of Funds NewYork Life Investments – MainStay Funds Victory Funds Deutsche Asset Management (DWS) New Alternatives Fund Virtus Investment Partners Eagle Asset Management Nuveen a TIAA company Voya Funds Eaton Vance OakRidge Investments Voya Select Advantage Federated Oppenheimer Funds -

Bestweek World's Largest Insurers

www.bestweek.com BESTWEEK BESTWEEKWeekly Insurance Newsletter January 2012 Weekly Insurance Newsletter Top Insurers Ranked by Assets, Net Premiums Aegon N.V. Chairman and Chief Executive: World’s Largest Insurers Alex Wynaendts Ranked by Non-Banking Assets Aegon is a public company specializing 2010 in life insurance, pensions and long- Total Non- term savings and investment products. Country of Banking Assets % It has 28,000 employees serving 40 AMB Company Name Domicile USD (000) Change* million clients in 20 countries. 1 Japan Post Insurance Co. Ltd. Japan 1,089,463,948 -5.26 www.aegon.com Wynaendts 2 Axa S.A. France 920,476,513 3.27 3 Allianz SE Germany 807,486,736 8.23 Allianz Societas Europae 4 MetLife Inc. US 730,906,000 35.53 Chairman and Chief Executive: 5 American International Group Inc. US 683,443,000 -19.37 Michael Diekmann 6 Aviva plc UK 572,208,859 4.45 Allianz is a public company specializing 7 Assicurazioni Generali S.p.A. Italy 559,858,937 -0.33 in property/casualty and life/health 8 Prudential Financial Inc. US 539,854,000 12.42 insurance, asset management and Nippon Life Insurance Co. Japan 527,095,201 6.20 banking. It has approximately 151,000 9 employees serving more than 76 mil- 10 Legal & General Group plc UK 501,063,918 9.03 lion clients in about 70 countries. Diekmann 11 National Mut Ins Fed of Agricultural Co-ops Japan 488,175,304 3.30 Rating: A.M. Best currently rates the financial strength of 12 Aegon N.V.