Manulife's Investor Day 2017 in Hong Kong-Slides-Day 1

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Group Life Insurance Product Information Booklet

GROUP LIFE INSURANCE PRODUCT INFORMATION BOOKLET July 2021 aia.com.au GROUP LIFE INSURANCE PRODUCT INFORMATION BOOKLET | About AIA Australia About AIA AIA Australia is a leading life insurance specialist with over AIA Group Limited and its subsidiaries (collectively “AIA” 48 years’ experience and a commitment to help Australians or the “Group”) comprise the largest independent publicly live healthier, longer, better lives. In 2014 the company listed pan-Asian life insurance group. It has a presence in launched AIA Vitality, a world leading, science-based health 18 markets across the Asia-Pacific region – whollyowned and wellbeing program, to the Australian market. In July branches and subsidiaries in Hong Kong SAR, Thailand, 2017, AIA and its partners launched AIA’s health insurance Singapore, Malaysia, Mainland China, South Korea, the business, now known as AIA Health Insurance. Philippines, Australia, Indonesia, Taiwan (China), Vietnam, New Zealand, Macau SAR, Brunei, Cambodia, Myanmar, and a In 2021, CommInsure Life was integrated into AIA Australia. 49 per cent joint venture in India. The lives of more than 3.8 million Australians are protected and enhanced through AIA Australia’s unique value proposition The business that is now AIA was first established in of life, health and wellbeing. Our vision is to embrace shared Shanghai a century ago in 1919. It is a market leader in value in championing Australia and New Zealand to be the the Asia-Pacific region (ex-Japan) based on life insurance healthiest and best protected nations in the world. premiums and holds leading positions across the majority of its markets. It had total assets of US$326 billion as of AIA Australia has been recognised with multiple awards, 31 December 2020. -

Ethics Agreement in Order to Avoid Any Financial Conflict

Date: 7 .-e-•15 Iett..% 1--4 17 MEMORANDUM FOR THE RECORD SUBJECT: Ethics Agreement In order to avoid any financial conflict of interest in violation of 18 U.S.C. § 208(a) or the appearance of a financial conflict of interest as defined in the Standards of Ethical Conduct for Employees of the Executive Branch, 5 C.F.R. § 2635.502, and to adhere to the Ethics Pledge instituted by Executive Order 13770 issued on January 28, 2017, and entitled "Ethics Commitments by Executive Branch Appointees" (the Ethics Pledge), I am issuing the following statement. I understand that as an appointee I must sign the Ethics Pledge and that I will be bound by the requirements and restrictions therein even if not specifically mentioned in this or any other ethics agreement. Before beginning my covered Federal position, I resigned from my non-Federal positions with the Association of State and Territorial Health Officials (ASTHO) and the State of Georgia on July 6, 2017. Pursuant to the Ethics Pledge, I will not, for a period of two years from the date of my appointment to my covered Federal position, participate in an official capacity in any particular matter involving specific parties that is directly and substantially related to ASTHO, unless an exception applies or I am granted a waiver. I understand that this provision in the Ethics Pledge does not apply to state government entities, including the State of Georgia. Even when the two-year restriction of the Ethics Pledge does not apply, under 5 C.F.R. § 2635.502, I will not, for a period of one year from the date of my resignation from ASTHO and the State of Georgia, participate in any particular matter involving specific parties in which ASTHO or the State of Georgia is a party or represents a party, unless I am first authorized to participate, pursuant to 5 C.F.R. -

ESG Report 2020”)

ENVIRONMENTAL, SOCIAL AND GOVERNANCE REPORT 2020 STOCK CODE 1299 AIA GROUP LIMITED 友邦保險控股有限公司 AIA GROUP LIMITED | Environmental, Social and Governance Report 2020 CONTENTS CONTENTS 1 2020 ESG AT-A-GLANCE 16 Health and 52 People and Culture 3 Chairman’s Statement Wellness 2020 ESG 55 Developing Our People AT-A-GLANCE 6 Statement from Group 18 Engaging and Inspiring 58 Diversity and Inclusion Chief Executive and Healthy Living CHAIRMAN’S 60 A Risk-aware Culture STATEMENT President Greater Access to 21 61 Recognising and Quality Care Rewarding Our People STATEMENT FROM 23 Champion Financial GROUP CHIEF 9 About This Report 66 SUPPLEMENT: EXECUTIVE AND Inclusion Supporting Our PRESIDENT 9 Who We Are 25 Delivering Better Health Employees During Outcomes COVID-19 ABOUT THIS 10 Our Purpose REPORT 11 Our ESG Strategy 30 SUPPLEMENT: Supporting Our HEALTH AND 14 Our Material Issues Communities Through 67 Effective WELLNESS 15 Our Approach to COVID-19 Governance ESG Reporting GREEN 69 Board Governance OPERATIONS 35 Green Operations 70 Effective Risk SUSTAINABLE Management and INVESTMENT 37 Digital Transformation Responsible Business 37 Encouraging Good Practices PEOPLE AND CULTURE ESG Practice 77 Promoting ESG Best 38 Green Buildings Practice EFFECTIVE 40 Reducing our Carbon 78 ESG Ratings and Index GOVERNANCE Footprint Inclusions OUR TCFD REPORT FEEDBACK 41 Sustainable 80 SUPPLEMENT: Our Investment TCFD Report GRI AND HKSE GUIDE CONTENT 43 ESG Engagements 81 Governance of Climate INDEX 46 ESG Training and Change Risks and Development Impacts 48 Broadening -

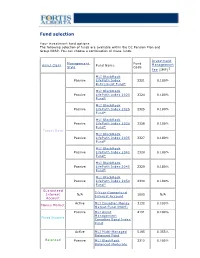

Fund Selection

Fund selection Y our investment fund options The following selection of funds are available within the DC Pension Plan and Group RRSP. You can choose a combination of these funds. Investment Management Fund Asset Class Fund Name Management Style Code Fee (IMF)1 MLI BlackRock Passive LifeP ath Index 2321 0.180% Retirement Fund* MLI BlackRock Passive LifeP ath Index 2020 2324 0.180% Fund* MLI BlackRock Passive LifeP ath Index 2025 2325 0.180% Fund* MLI BlackRock Passive LifeP ath Index 2030 2326 0.180% Fund* Target Date MLI BlackRock Passive LifeP ath Index 2035 2327 0.180% Fund* MLI BlackRock Passive LifeP ath Index 2040 2328 0.180% Fund* MLI BlackRock Passive LifeP ath Index 2045 2329 0.180% Fund* MLI BlackRock Passive LifeP ath Index 2050 2330 0.180% Fund* Guaranteed 5-Y ear Guaranteed Interest N/A 1005 N/A Interest Account Account Active MLI Canadian Money 3132 0.100% Money Market Market Fund (MAM) Passive MLI Asset 4191 0.100% Management Fixed Income Canadian Bond Index Fund Active MLI Multi-Managed 5195 0.355% Balanced Fund Balanced Passive MLI BlackRock 2312 0.105% Balanced Moderate Index Fund Active MLI Canadian Equity 7011 0.210% Fund Canadian Passive MLI Asset 7132 0.100% Equity Management Canadian Equity Index Fund Active MLI U.S. Diversified 8196 0.375% Grow th Equity (Wellington) Fund U.S. Equity Passive MLI BlackRock U.S. 8322 0.090% Equity Index Fund* Active MLI MFS MB 8162 0.280% International Equity International Fund Equity Passive MLI BlackRock 8321 0.160% International Equity Index Fund* 1 IMFs shown do not include applicable taxes. -

NP Key Contacts.Pdf

IGP Network Partners: Key Contacts Region: Americas Country / Territory IGP Network Partner IGP Contact Email Type IGP Regional Coordinator Mr. Michael Spincemaille [email protected] Argentina SMG LIFE Mr. Nicolas Passet [email protected] Partner Brazil MAPFRE Vida S.A. Ms. Débora Nunes Santos [email protected] Partner Canada Manulife Financial Corporation Mr. Kajan Ramanathan [email protected] Partner Chile MAPFRE Chile Ms. Nathalie Gonzalez [email protected] Partner Colombia MAPFRE Colombia Ms. Ingrid Olarte Pérez [email protected] Partner Costa Rica MAPFRE Costa Rica Mr. Armando Sevilla [email protected] Partner Dominican Republic (Life) MAPFRE BHD Mrs. Alejandra Quirico [email protected] Partner Dominican Republic (Health) MAPFRE Salud ARS, S. A. Mr. Christian Wazar [email protected] Partner Ecuador MAPFRE Atlas * Mr. Carlos Zambrano [email protected] Correspondent El Salvador MAPFRE Seguros El Salvador S.A. Mr. Daniel Acosta González [email protected] Partner French Guiana Refer to France - - Partner Guadeloupe Refer to France - - Partner Guatemala MAPFRE Guatemala Mr. Luis Pedro Chavarría [email protected] Partner Honduras MAPFRE Honduras Mr. Carlos Ordoñez [email protected] Partner Martinique Refer to France - - Partner Mexico Seguros Monterrey New York Life Ms. Paola De Uriarte [email protected] Partner Nicaragua MAPFRE Nicaragua Mr. Dany Lanuza Flores [email protected] Partner Panama MAPFRE Panama Mr. Manuel Rodriguez [email protected] Partner Paraguay MAPFRE Paraguay Mr. Sergio Alvarenga [email protected] Partner Peru MAPFRE Peru Mr. Ramón Acuña Huerta [email protected] Partner Saint Martin Refer to France - - Partner Saint Barthélemy Refer to France - - Partner Saint Pierre & Miquelon Refer to France - - Partner United States Prudential Insurance Company of America Mr. -

Manulife Global Fund Unaudited Semi-Annual Report

Unaudited Semi-Annual Report Manulife Global Fund Société d'Investissement à Capital Variable for the six month period ended 31 December 2020 No subscription can be received on the basis of nancial reports. Subscriptions are only valid if made on the bases of the current prospectus, accompanied by the latest annual report and semi-annual report if published thereaer. SICAV R.C.S Luxembourg B 26 141 Contents Directors ..................................................................................................................................................... 1 Management and Administration ............................................................................................................. 2 Directors’ Report ........................................................................................................................................ 4 Statement of Net Assets ........................................................................................................................... 10 Statement of Changes in Net Assets ........................................................................................................ 15 Statement of Operations ........................................................................................................................... 20 Statistical Information ............................................................................................................................... 25 Statement of Changes in Shares ............................................................................................................. -

Q1 2020 Building Sustainable Shareholder Value Business Overview

Q1 2020 Building Sustainable Shareholder Value Business overview Update in light of COVID-19 Business group results & highlights Capital management Asset portfolio Sustainability 2 A $26.51 billion leading global financial services organization Offices in 40,600 Employees 125,900 advisors 27 markets 2 2 2 Operating through a balanced and diversified model and focused on creating shareholder value now and in the future SUN LIFE • Q1 2020 1 Market capitalization in C$ as at March 31, 2020 3 2 As at December 31, 2019. Includes Asia joint ventures The Sun Life story • A diversified business model, with four strong pillars that can each compete, win and grow in their respective sectors and which leverage each other • Bound together by a strong balance sheet and risk culture, including no U.S. Variable Annuity or U.S. Long-Term Care • Digital transformation that is deeply embedded throughout the organization • Building on momentum created by past organic investments and acquisitions that will help drive earnings growth SUN LIFE • Q1 2020 4 Executing on our ambition to be one of the best insurance and asset management companies globally A Leader in Insurance and A Leader in U.S. Wealth Solutions in our CAN US Group Benefits Canadian Home Market A Leader in Asia A Leader in Global AM ASIA through Distribution Asset Management Excellence in Higher Growth Markets Each pillar Top quartile Disproportionate Top quartile total viewed as a Client share of top shareholder leader experience talent return SUN LIFE • Q1 2020 5 Consistently delivering value to shareholders 5-year total shareholder return1 Progress on medium-term objectives March 31, 2020 Sun Life 6.9% Medium-term objective Q1 2020 TSX 0.9% Underlying ROE2 12-14% 14.2% Canadian lifecos 0.0% Underlying EPS growth2 9% Global lifecos (1.2)% 8-10% Dividend payout ratio2 U.S. -

2018 Annual Report Fellow Shareholders, Governance and Shareholder Outreach

Manulife Financial Corporation Who Manulife Financial Corporation is Our five Portfolio Optimization we are a leading international financial strategic We are actively managing our priorities services group providing financial 1 legacy businesses to improve advice, insurance, as well as returns and cash generation while wealth and asset management reducing risk. solutions for individuals, groups, and institutions. We operate as John Hancock in the United States Expense Efficiency and Manulife elsewhere. We are getting our cost structure 2 into fighting shape and simplifying and digitizing our processes to position us for efficient growth. Accelerate Growth We are accelerating growth in our 3 highest-potential businesses. Our Digital, Customer Leader mission Decisions We are improving our customer 4 experiences, using digitization and made easierr. innovation to put customers first. Lives High-Performing Team made betterr. We are building a culture that 5 drives our priorities. Our Our Values represent how we Obsess Do the Values operate. They reflect our culture, about right thing inform our behaviours, and help define how we work together. customers Manulife Note: Growth in core earnings, assets under Core Earnings (C$ billions) management and administration (AUMA), and by the new business value are presented on a constant $5.6 billion exchange rate basis. numbers Total Company, Global Wealth and Asset Management (Global WAM), and Asia core earnings up 23%, 21%, and 20%, respectively, from 2017. 5.6 4.6 4.0 3.4 2.9 2014 2015 2016 2017 2018 Assets Under Management and Administration Net Income Attributed to Shareholders (C$ billions) (C$ billions) $1,084 billion $4.8 billion Over $1 trillion in AUMA. -

Ng Keng Hooi to Retire As AIA Group Chief Executive and President to Be Succeeded by Lee Yuan Siong from 1 June 2020

This announcement is for information purposes only and does not constitute an invitation or offer by any person to acquire, purchase or subscribe for securities. This announcement is not, and is not intended to be, an offer of securities of the Company for sale in the United States. The securities of the Company have not been, and will not be, registered under the U.S. Securities Act of 1933, as amended (the “U.S. Securities Act”) and may not be offered or sold in the United States absent registration or an applicable exemption from registration requirements under the U.S. Securities Act. There is not, and is not intended to be, any public offering of the securities of the Company in the United States. Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. Ng Keng Hooi to retire as AIA Group Chief Executive and President To be succeeded by Lee Yuan Siong from 1 June 2020 HONG KONG, 22 November 2019 – AIA Group Limited (“AIA” or the “Company”) announces today that its Group Chief Executive and President, Ng Keng Hooi, has informed the Board of Directors of the Company (the “Board”) of his intention to retire from his executive positions with the Company and its subsidiaries (the “Group”) effective 31 May 2020. -

Demutualization Details

Demutualization Details 1. American Mutual Life – AmerUs- Indianapolis Life Insurance Company - Central Life Assurance - Central Life Assurance merged with American Mutual in 1994. American Mutual Life was renamed AmerUs Life Insurance Company in 1995. On September 20, 2000, it demutualized to become AmerUs Group. In 2001, the company merged with Indianapolis Life, which had also undergone a demutualization. Approximately 300,000 policyholders and heirs became entitled to receive $452 million in AmerUs Group common stock and $340 million in cash and policy credits. Distribution began on July 31, 2001. Eligible policyholders received a fixed component of 20 AmerUS common shares, as well as a variable component based on policy value. Those who elected to receive cash were compensate $26 per share entitlement. In the first year after the initial public offering, the price of an AmerUS common share increased 99%. The current value of AmerUS Group stock is approximately $45 per share. 2. Anthem Insurance - On July 31, 2002 Anthem Insurance Companies, Inc. completed its conversion from a mutual insurance company to a stock company, and became a wholly owned subsidiary of Anthem, Inc. Eligible policyholders and heirs became entitled to approximately 48 million shares of Anthem, Inc. common stock and cash totaling $2.06 billion. Compensation consisted of a fixed component of 21 Anthem common shares, as well as a variable component based on policy value. The shares were offered to the public at $36. In the first year after the initial public offering, the price of an Anthem common share increased 54%. 3. Equitable Life – Axa - In 1992 the Equitable Life Assurance Society of the United States demutualized and a new parent holding company, the Equitable Companies, was listed on the New York Stock Exchange. -

INSURANCE AGENT of the YEAR Joyce Chan Prudential Assurance Company, Singapore

5th Asia Trusted Life Agents & Advisers Awards 2020 The Winners Organisers Co-Organiser Strategic Partner Organisers Co-Organiser Strategic Partner Supporting Organisations CONTENTS 21 27 Bank Partner Insurance Agency of the Year Leader of the Year 2 22 28 Messages Digital Agency Insurance Agent Leader of the Year of the Year 6 23 29 The Judges InsurTech of the Year Young Executive of the Year 18 24 30 Rookie Insurance Agent Digital Transformation Insurance Company of the Year of the Year of the Year 19 25 31 Rookie Insurance Agency Inspirational Agency Executive Champion Leader of the Year Leader of the Year of the Year 20 26 37 Financial Adviser Lifetime Achievement The Finalists of the Year Award 1 5th Asia Trusted Life Agents & Advisers Awards 2020 MESSAGE-PATRON Going from strength to strength s the Founding Patron of the Asia Trusted Life Agents & Advisers Insurance is still fundamentally all Awards, I am delighted to see them continue to go from strength to about making promises to people. strength in their fifth year, in spite of the many challenges we are facing The true value of agents and advisers as a result of COVID-19. comes in the way that they combine A the use of exciting new technologies As the focus shifts towards rebuilding and repairing economies, financial with excellence in customer service. services generally – and our industry specifically – will play a leading role. The For many, they are the human face requirement for long-term capital and need to manage new kinds of risk clearly of our promises – and their ability play to our industry’s strengths – but we will also need to adapt to the new to build trusted relationships with normal. -

Aia Group Adds Paul Groves to Its Leadership Team As Group Chief Marketing Officer

AIA Group Limited 35/F AIA Central 1 Connaught Road Central Hong Kong T: (852) 2832 1800 F: (852) 2572 4695 AIA.COM Media Release Contact: Patricia Chua/Emerald Ng +852 2832 1366/+852 2832 4720 AIA GROUP ADDS PAUL GROVES TO ITS LEADERSHIP TEAM AS GROUP CHIEF MARKETING OFFICER HONG KONG, 3 DECEMBER 2010 – AIA Group Limited, (“AIA”; stock code: 1299), the world’s largest independent listed pan-Asian life insurance group, announced the appointment of Paul Groves as Executive Vice President & Group Chief Marketing Officer effective 12 January 2011. Mr. Groves will be joining AIA from MetLife International (previously ALICO) where he was most recently Senior Vice-President, Head of International Marketing and Direct to Consumer channel including oversight for 125 marketing colleagues across 65 countries. Prior to MetLife, he was Chief Marketing Officer, UK & Ireland for GE Money, and had spent another 27 years with Barclays and Barclaycard in the UK, including Channel Strategy & Management Director for Retail Banking, Head of Customer Retention and Marketing Communications Director. Mr. Mark Tucker, AIA Group Executive Chairman & Chief Executive Officer said: “Paul joins us with almost 30 years of marketing experience in financial services – experience that is very focused on the delivery of results and creation of shareholder value. The breadth and depth of Paul’s experience makes him an extremely valuable addition to my leadership team. He will oversee AIA Group’s strategic marketing functions with the ultimate goal of helping AIA attract and retain customers.” Mr. Groves, who will be based in Hong Kong, will be in charge of the Group’s marketing functions including development of overall marketing strategy and planning, communications and branding, product management, business intelligence, customer value group and digital marketing, as well as providing leadership support to AIA’s country marketing operations.