Demutualization Details

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Consolidation and Demutualization: What Strategies Should Exchanges

OECD, Tokyo Round Table, 11/2003 Consolidation and Demutualization: What Strategies Should Exchanges Adopt in the Future? Ruben Lee Oxford Finance Group Changing Market Structures & the Future of Trading Overview 1) Threatening Factors 2) Self-Sufficiency 3) Linkages 4) Mergers and Takeovers 5) Demutualization 6) Conclusions Changing Market Structures & the Future of Trading 1) Threatening Factors Threatening Factors Main Trends Small Number of Liquid Stocks International Listing & Trading of Domestic Stocks Internalization Regulatory Liberalization Threatening Factors Reasons for Small Number of Liquid Stocks Not Many Companies Privatization Stalled Concentration of Shareholdings Foreign/Private Purchases of Best Companies Changing Market Structures & the Future of Trading 2) Self-Sufficiency Self-Sufficiency Factors Supporting Domestic Stock Exchanges Positive “Network Externality” with Liquidity Competition Not Always Successful Foreign Listing/Trading Complements Local Trading Support of Domestic SMEs Adaptability to Local Conditions Declining IT Costs Self-Sufficiency Current Major Revenue Sources Membership Listing Trading Clearing Settlement Provision of Company News Provision of Quote and Price Data Self-Sufficiency Threats to Revenue Sources Membership - Demutualization Listing – Decline in Value + Competition Trading – Marginal Cost Pricing Clearing – Expensive + Antitrust Scrutiny Settlement – Antitrust Scrutiny Provision of Company News – Competition Provision of Quote and Price Data – Antitrust Scrutiny Changing Market Structures -

Pension Risk Strategy Summit Supplement

Advertising Supplement PENSION RISK MANAGEMENT STRATEGIES Understanding All the Derisking Possibilities PS001_PI_20170612.pdf RunDate: 06/12/17 pi Pension Risk Strategies supp 8 x 10.875 Color: 4?C Advertising Supplement SPONSORS Fidelity Institutional Asset Management 900 Salem Street Smitheld, RI 02917 Daniel Tremblay Senior Vice President and Director of Institutional Fixed Income Solutions 603.791.6599 [email protected] www.institutional.delity.com MetLife 200 Park Avenue New York, NY 10166 Asif Mohamed Director, U.S. Pensions 212.578.8624 [email protected] www.metlife.com/pensions NISA Investment Advisors, LLC 101 South Hanley Road, Suite 1700 St. Louis, MO 63105 Gregory J. Yess Managing Director, Client Services 314.721.1900 [email protected] www.nisa.com Prudential Retirement 280 Trumbull Street Hartford, CT 06103 Scott Gaul, FSA Senior Vice President and Head of Distribution, Pension Risk Transfer 860.534.4263 [email protected] www.pensionrisk.prudential.com Schroders 7 Bryant Park New York, NY 10018-3706 Jennifer Horne, CFA Head of U.S. Institutional Clients 212.641.3800 [email protected] www.schroders.com/us This special advertising supplement is not created, written or produced by the editors of Pensions & Investments and does not represent the views or opinions of the publication or its parent company, Crain Communications Inc. 2 Pension Risk Management Strategies PS002_PI_20170612.pdf RunDate: 06/12/17 pi Pension Risk Strategies supp 8 x 10.875 Color: 4?C Advertising Supplement CONTENTS 4 Taking a Journey Along the Derisking Spectrum Corporate plan sponsors wishing to mitigate pension risk have a myriad of possible strategies at their disposal 12 Underfunded? Taking the LDI Path to Full Funding Most plan sponsors looking to dial down funded status volatility turn to liability-driven investing. -

State Authority, Economic Governance and the Politics Of

THE DIVERSITY OF CONVERGENCE: STATE AUTHORITY, ECONOMIC GOVERNANCE AND THE POLITICS OF SECURITIES FINANCE IN CHINA AND INDIA A Dissertation Presented to the Faculty of the Graduate School of Cornell University In Partial Fulfillment of the Requirements for the Degree of Doctor of Philosophy by Matthew C.J. Rudolph May 2006 © 2006 Matthew C.J. Rudolph THE DIVERSITY OF CONVERGENCE: STATE AUTHORITY, ECONOMIC GOVERNANCE AND THE POLITICS OF SECURITIES FINANCE IN CHINA AND INDIA Matthew C.J. Rudolph, Ph.D. Cornell University 2006 This dissertation explains contrasting patterns of financial reform in China and India. It focuses on “securitization” – the structural shift from credit-based finance (banking) to securities-based finance (stocks and bonds) – as a politically consequential phenomenon in comparative and international political economy. The analysis revises common theories of the developmental state – theories derived from Gerschenkron’s emphasis on directed-credit and the state’s role in capital formation – in light of securitization’s growing global importance in the last twenty years. Contrasting responses to securitization are explained using international and domestic variables including the profile of a country’s exposure to the world economy, the distributional coalition supporting the state and the prevailing structure of property rights. At a theoretical level, the dissertation highlights the political consequences of securitization for state authority in the economy, arguing that directed-credit; 1) enhanced state discretion in the management of distributional coalitions; 2) facilitated the perpetuity of poorly specified property rights; and 3) mitigated the consequences of the country’s position with respect to external trade and investment. Empirically, the research presented here demonstrates that China and India responded differently to the process of securitization, contrary to the expectations of globalization theories that identify finance as a domain in which international forces favoring convergence should be strongest. -

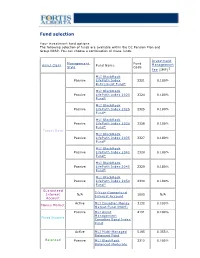

Fund Selection

Fund selection Y our investment fund options The following selection of funds are available within the DC Pension Plan and Group RRSP. You can choose a combination of these funds. Investment Management Fund Asset Class Fund Name Management Style Code Fee (IMF)1 MLI BlackRock Passive LifeP ath Index 2321 0.180% Retirement Fund* MLI BlackRock Passive LifeP ath Index 2020 2324 0.180% Fund* MLI BlackRock Passive LifeP ath Index 2025 2325 0.180% Fund* MLI BlackRock Passive LifeP ath Index 2030 2326 0.180% Fund* Target Date MLI BlackRock Passive LifeP ath Index 2035 2327 0.180% Fund* MLI BlackRock Passive LifeP ath Index 2040 2328 0.180% Fund* MLI BlackRock Passive LifeP ath Index 2045 2329 0.180% Fund* MLI BlackRock Passive LifeP ath Index 2050 2330 0.180% Fund* Guaranteed 5-Y ear Guaranteed Interest N/A 1005 N/A Interest Account Account Active MLI Canadian Money 3132 0.100% Money Market Market Fund (MAM) Passive MLI Asset 4191 0.100% Management Fixed Income Canadian Bond Index Fund Active MLI Multi-Managed 5195 0.355% Balanced Fund Balanced Passive MLI BlackRock 2312 0.105% Balanced Moderate Index Fund Active MLI Canadian Equity 7011 0.210% Fund Canadian Passive MLI Asset 7132 0.100% Equity Management Canadian Equity Index Fund Active MLI U.S. Diversified 8196 0.375% Grow th Equity (Wellington) Fund U.S. Equity Passive MLI BlackRock U.S. 8322 0.090% Equity Index Fund* Active MLI MFS MB 8162 0.280% International Equity International Fund Equity Passive MLI BlackRock 8321 0.160% International Equity Index Fund* 1 IMFs shown do not include applicable taxes. -

NP Key Contacts.Pdf

IGP Network Partners: Key Contacts Region: Americas Country / Territory IGP Network Partner IGP Contact Email Type IGP Regional Coordinator Mr. Michael Spincemaille [email protected] Argentina SMG LIFE Mr. Nicolas Passet [email protected] Partner Brazil MAPFRE Vida S.A. Ms. Débora Nunes Santos [email protected] Partner Canada Manulife Financial Corporation Mr. Kajan Ramanathan [email protected] Partner Chile MAPFRE Chile Ms. Nathalie Gonzalez [email protected] Partner Colombia MAPFRE Colombia Ms. Ingrid Olarte Pérez [email protected] Partner Costa Rica MAPFRE Costa Rica Mr. Armando Sevilla [email protected] Partner Dominican Republic (Life) MAPFRE BHD Mrs. Alejandra Quirico [email protected] Partner Dominican Republic (Health) MAPFRE Salud ARS, S. A. Mr. Christian Wazar [email protected] Partner Ecuador MAPFRE Atlas * Mr. Carlos Zambrano [email protected] Correspondent El Salvador MAPFRE Seguros El Salvador S.A. Mr. Daniel Acosta González [email protected] Partner French Guiana Refer to France - - Partner Guadeloupe Refer to France - - Partner Guatemala MAPFRE Guatemala Mr. Luis Pedro Chavarría [email protected] Partner Honduras MAPFRE Honduras Mr. Carlos Ordoñez [email protected] Partner Martinique Refer to France - - Partner Mexico Seguros Monterrey New York Life Ms. Paola De Uriarte [email protected] Partner Nicaragua MAPFRE Nicaragua Mr. Dany Lanuza Flores [email protected] Partner Panama MAPFRE Panama Mr. Manuel Rodriguez [email protected] Partner Paraguay MAPFRE Paraguay Mr. Sergio Alvarenga [email protected] Partner Peru MAPFRE Peru Mr. Ramón Acuña Huerta [email protected] Partner Saint Martin Refer to France - - Partner Saint Barthélemy Refer to France - - Partner Saint Pierre & Miquelon Refer to France - - Partner United States Prudential Insurance Company of America Mr. -

Part VII Transfers Pursuant to the UK Financial Services and Markets Act 2000

PART VII TRANSFERS EFFECTED PURSUANT TO THE UK FINANCIAL SERVICES AND MARKETS ACT 2000 www.sidley.com/partvii Sidley Austin LLP, London is able to provide legal advice in relation to insurance business transfer schemes under Part VII of the UK Financial Services and Markets Act 2000 (“FSMA”). This service extends to advising upon the applicability of FSMA to particular transfers (including transfers involving insurance business domiciled outside the UK), advising parties to transfers as well as those affected by them including reinsurers, liaising with the FSA and policyholders, and obtaining sanction of the transfer in the English High Court. For more information on Part VII transfers, please contact: Martin Membery at [email protected] or telephone + 44 (0) 20 7360 3614. If you would like details of a Part VII transfer added to this website, please email Martin Membery at the address above. Disclaimer for Part VII Transfers Web Page The information contained in the following tables contained in this webpage (the “Information”) has been collated by Sidley Austin LLP, London (together with Sidley Austin LLP, the “Firm”) using publicly-available sources. The Information is not intended to be, and does not constitute, legal advice. The posting of the Information onto the Firm's website is not intended by the Firm as an offer to provide legal advice or any other services to any person accessing the Firm's website; nor does it constitute an offer by the Firm to enter into any contractual relationship. The accessing of the Information by any person will not give rise to any lawyer-client relationship, or any contractual relationship, between that person and the Firm. -

Manulife Global Fund Unaudited Semi-Annual Report

Unaudited Semi-Annual Report Manulife Global Fund Société d'Investissement à Capital Variable for the six month period ended 31 December 2020 No subscription can be received on the basis of nancial reports. Subscriptions are only valid if made on the bases of the current prospectus, accompanied by the latest annual report and semi-annual report if published thereaer. SICAV R.C.S Luxembourg B 26 141 Contents Directors ..................................................................................................................................................... 1 Management and Administration ............................................................................................................. 2 Directors’ Report ........................................................................................................................................ 4 Statement of Net Assets ........................................................................................................................... 10 Statement of Changes in Net Assets ........................................................................................................ 15 Statement of Operations ........................................................................................................................... 20 Statistical Information ............................................................................................................................... 25 Statement of Changes in Shares ............................................................................................................. -

Cohen & Steers Preferred Securities and Income Fund

Cohen & Steers Preferred Securities and Income Fund As of 06/30/2021 Current % of Total Security Name Sector Market Value Market Value Wells Fargo & Company Flt Perp Banking $219,779,776.15 1.81 % Charles Schwab Corp Flt Perp Sr:I Banking $182,681,675.00 1.51 % Bp Capital Markets Plc Flt Perp Energy $158,976,029.00 1.31 % Bank of America 6.25% Banking $148,052,279.38 1.22 % Bank of Amrica 6.10% Banking $144,075,863.52 1.19 % Citigroup Inc Flt Perp Banking $139,736,756.25 1.15 % Emera 6.75% 6/15/76-26 Utilities $134,370,096.24 1.11 % Transcanada Trust 5.875 08/15/76 Pipeline $116,560,837.50 0.96 % JP Morgan 6.75% Banking $116,417,211.75 0.96 % JP Morgan 6.1% Banking $115,050,549.38 0.95 % Credit Suisse Group AG 7.5 Perp Banking $112,489,090.00 0.93 % Enbridge Inc Flt 07/15/80 Sr:20-A Pipeline $101,838,892.50 0.84 % Charles Schwab Corp Flt Perp Sr:G Banking $101,715,980.40 0.84 % Bank of America Corp 5.875% Perp Banking $99,269,540.97 0.82 % Sempra Energy Flt Perp Utilities $97,680,337.50 0.81 % BNP Paribas 7.375% Banking $96,328,288.48 0.79 % Jpmorgan Chase & Co Flt Perp Sr:Kk Banking $95,672,863.00 0.79 % Metlife Capital Trust IV 7.875% Insurance $94,971,600.00 0.78 % Citigroup 5.95% 2025 Call Banking $89,482,599.30 0.74 % Transcanada Trust Flt 09/15/79 Pipeline $88,170,468.75 0.73 % Ally Financial Inc Flt Perp Sr:C Banking $86,422,336.00 0.71 % Banco Santander SA 4.75% Flt Perp Banking $83,189,000.00 0.69 % American Intl Group 8.175% 5/15/58 Insurance $82,027,104.20 0.68 % Prudential Financial 5.625% 6/15/43 Insurance $80,745,314.60 0.67 -

Memorandum from the Division of Investment Management Regarding

MEMORANDUM TO: Proposed Rule: Updated Disclosure Requirements and Summary Prospectus for Variable Annuity and Variable Life Insurance Contracts (Release No. IC-33286; File No. S7-23-18) FROM: Dan Chang Senior Counsel, Division of Investment Management RE: Meeting with Representatives of the Committee of Annuity Insurers DATE: May 31, 2019 On May 29, 2019, Sarah G. ten Siethoff (Associate Director, Division of Investment Management (“IM”)), Brian M. Johnson (Assistant Director, IM); William J. Kotapish (Assistant Director, IM); Naseem Nixon (Senior Special Counsel, IM), Michael Kosoff (Senior Special Counsel, IM), Keith Carpenter (Senior Special Counsel, IM), Harry Eisenstein (Senior Special Counsel, IM), Michael Pawluk (Senior Special Counsel, IM), Sumeera Younis (Branch Chief, IM), Dan Chang (Senior Counsel, IM), Amy Miller (Senior Counsel, IM), Sonny Oh (Senior Counsel, IM), Alberto H. Zapata (Senior Counsel, IM), Patrick F. Scott (Senior Counsel, IM), DeCarlo McLaren (Special Counsel, IM), Daniel Deli (Financial Economist, Division of Economic and Risk Analysis (“DERA”)), Walter Hamscher (Senior IT Program Manager, DERA), and PJ Hamidi (Senior Counsel, DERA) met with the following representatives from the Committee of Annuity Insurers: Shane Daly, Vice President & Associate General Counsel, AXA Equitable Scott Durocher, Assistant Vice President & Senior Counsel, Lincoln Financial Jamie Castro, Managing Counsel, Nationwide Financial Bill Evers, Vice President & Chief Counsel, Prudential Financial Jordan Thomsen, Vice President & Corporate Counsel, Prudential Financial Steve Roth, Partner, Eversheds Sutherland Dodie Kent, Partner, Eversheds Sutherland Ron Coenen, Associate, Eversheds Sutherland Among other things, the participants discussed the SEC’s proposal relating to updated disclosure requirements and a summary prospectus for variable annuity and variable life insurance contracts. -

John Hancock Investments Adds Financial Results

Recent Highlights A Global Leader John Hancock Financial is a unit of Manulife Financial Corporation, a leading October: John Hancock completes acquisition Canada-based financial services group with principal operations in Asia, of Symetra Investment Services. Canada and the United States. October: John Hancock Investments adds Financial Results . For the quarter ended Sept. 30, 2013, the U.S. Division operations doing three new managing directors to its Institutional business under the John Hancock brand (John Hancock)2 reported earnings 3 team. attributed to shareholders of $894 million. Total premiums and deposits for the quarter from John Hancock were $11 Sept. 30: John Hancock ends quarter with 26 billion or 55% of Manulife Financial’s overall third-quarter premiums and four- and five-star rated mutual funds. deposits. 4 1 (Source: Morningstar, Inc.) . John Hancock’s funds under management were $311 billion, 56% of Manulife’s total funds under management as of Sept. 30, 2013.4 September: John Hancock Retirement Plan Services Offers Partnership Program for Retirement Plan Consultants. Strong Claims Paying Ability/Financial Strength Ratings5 A+ A.M. Best (2nd highest of 15 ratings) September: John Hancock Insurance launches Superior ability to meet ongoing obligations a new survivorship indexed universal life AA- Fitch Ratings (4th highest of 19 ratings) product. Very strong capacity to meet policyholder and contract obligations th A1 Moody’s (5 highest of 21 ratings) September: John Hancock Funds changes its Good financial security th name to John Hancock Investments. AA- Standard & Poor’s (4 highest of 21 ratings) Very strong financial security characteristics August: John Hancock's 2013 Boston Marathon Fundraising Program nets record $7.9 million for non-profit organizations. -

Demystifying Negative Screens: the Full Implications of ESG Exclusions

Marketing material for professional investors or advisers only Demystifying negative screens: The full implications of ESG exclusions December 2017 Contents Demystifying negative screens: Appendix: A close look at the full implications of ESG different screening options exclusions 14 Alcohol 3 Executive summary 15 Fossil fuels 3 Screening remains very popular 16 Fur in general 17 Gambling 4 But some individual screens are more 18 Nuclear popular than others 19 Pornography 4 Our Global Investor Survey highlights 20 Sin changing attitudes towards 21 Tobacco negative screens 22 Weapons 5 Interest in fossil fuel and tobacco divestment is rising 7 Focusing narrowly on returns can be deeply misleading 9 Screens can have a heavy impact on specific investment strategies 11 Details matter when implementing screens 11 Screen definition decisions can significantly alter exclusion lists and investment results 12 Different data providers can produce very different exclusion lists 12 Active management can add more value than passive when applying screens Demystifying negative screens: the full implications of ESG exclusions Screening out investments that Alexander Monk Sustainable do not meet environmental, social Investment Analyst or governance (ESG) criteria is and the Sustainable superficially simple but fraught with Investment Team practical challenges. Understanding the complexities and biases screens create before they are implemented and appropriately assessing performance afterward is crucial for investors. In this paper, we investigate the pitfalls when implementing different screens. Executive summary The chart in Figure 1 shows the extent to which typical Negative screens that sieve investments on environmental, negative exclusions constrain managers. Implementing social and governance grounds remain critical to many screens may be mechanical, but assessing their impact on investors. -

2018 Annual Report Fellow Shareholders, Governance and Shareholder Outreach

Manulife Financial Corporation Who Manulife Financial Corporation is Our five Portfolio Optimization we are a leading international financial strategic We are actively managing our priorities services group providing financial 1 legacy businesses to improve advice, insurance, as well as returns and cash generation while wealth and asset management reducing risk. solutions for individuals, groups, and institutions. We operate as John Hancock in the United States Expense Efficiency and Manulife elsewhere. We are getting our cost structure 2 into fighting shape and simplifying and digitizing our processes to position us for efficient growth. Accelerate Growth We are accelerating growth in our 3 highest-potential businesses. Our Digital, Customer Leader mission Decisions We are improving our customer 4 experiences, using digitization and made easierr. innovation to put customers first. Lives High-Performing Team made betterr. We are building a culture that 5 drives our priorities. Our Our Values represent how we Obsess Do the Values operate. They reflect our culture, about right thing inform our behaviours, and help define how we work together. customers Manulife Note: Growth in core earnings, assets under Core Earnings (C$ billions) management and administration (AUMA), and by the new business value are presented on a constant $5.6 billion exchange rate basis. numbers Total Company, Global Wealth and Asset Management (Global WAM), and Asia core earnings up 23%, 21%, and 20%, respectively, from 2017. 5.6 4.6 4.0 3.4 2.9 2014 2015 2016 2017 2018 Assets Under Management and Administration Net Income Attributed to Shareholders (C$ billions) (C$ billions) $1,084 billion $4.8 billion Over $1 trillion in AUMA.