2018 Annual Report Fellow Shareholders, Governance and Shareholder Outreach

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Fund Selection

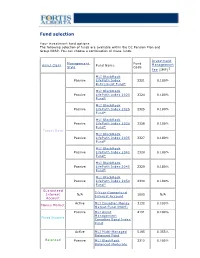

Fund selection Y our investment fund options The following selection of funds are available within the DC Pension Plan and Group RRSP. You can choose a combination of these funds. Investment Management Fund Asset Class Fund Name Management Style Code Fee (IMF)1 MLI BlackRock Passive LifeP ath Index 2321 0.180% Retirement Fund* MLI BlackRock Passive LifeP ath Index 2020 2324 0.180% Fund* MLI BlackRock Passive LifeP ath Index 2025 2325 0.180% Fund* MLI BlackRock Passive LifeP ath Index 2030 2326 0.180% Fund* Target Date MLI BlackRock Passive LifeP ath Index 2035 2327 0.180% Fund* MLI BlackRock Passive LifeP ath Index 2040 2328 0.180% Fund* MLI BlackRock Passive LifeP ath Index 2045 2329 0.180% Fund* MLI BlackRock Passive LifeP ath Index 2050 2330 0.180% Fund* Guaranteed 5-Y ear Guaranteed Interest N/A 1005 N/A Interest Account Account Active MLI Canadian Money 3132 0.100% Money Market Market Fund (MAM) Passive MLI Asset 4191 0.100% Management Fixed Income Canadian Bond Index Fund Active MLI Multi-Managed 5195 0.355% Balanced Fund Balanced Passive MLI BlackRock 2312 0.105% Balanced Moderate Index Fund Active MLI Canadian Equity 7011 0.210% Fund Canadian Passive MLI Asset 7132 0.100% Equity Management Canadian Equity Index Fund Active MLI U.S. Diversified 8196 0.375% Grow th Equity (Wellington) Fund U.S. Equity Passive MLI BlackRock U.S. 8322 0.090% Equity Index Fund* Active MLI MFS MB 8162 0.280% International Equity International Fund Equity Passive MLI BlackRock 8321 0.160% International Equity Index Fund* 1 IMFs shown do not include applicable taxes. -

NP Key Contacts.Pdf

IGP Network Partners: Key Contacts Region: Americas Country / Territory IGP Network Partner IGP Contact Email Type IGP Regional Coordinator Mr. Michael Spincemaille [email protected] Argentina SMG LIFE Mr. Nicolas Passet [email protected] Partner Brazil MAPFRE Vida S.A. Ms. Débora Nunes Santos [email protected] Partner Canada Manulife Financial Corporation Mr. Kajan Ramanathan [email protected] Partner Chile MAPFRE Chile Ms. Nathalie Gonzalez [email protected] Partner Colombia MAPFRE Colombia Ms. Ingrid Olarte Pérez [email protected] Partner Costa Rica MAPFRE Costa Rica Mr. Armando Sevilla [email protected] Partner Dominican Republic (Life) MAPFRE BHD Mrs. Alejandra Quirico [email protected] Partner Dominican Republic (Health) MAPFRE Salud ARS, S. A. Mr. Christian Wazar [email protected] Partner Ecuador MAPFRE Atlas * Mr. Carlos Zambrano [email protected] Correspondent El Salvador MAPFRE Seguros El Salvador S.A. Mr. Daniel Acosta González [email protected] Partner French Guiana Refer to France - - Partner Guadeloupe Refer to France - - Partner Guatemala MAPFRE Guatemala Mr. Luis Pedro Chavarría [email protected] Partner Honduras MAPFRE Honduras Mr. Carlos Ordoñez [email protected] Partner Martinique Refer to France - - Partner Mexico Seguros Monterrey New York Life Ms. Paola De Uriarte [email protected] Partner Nicaragua MAPFRE Nicaragua Mr. Dany Lanuza Flores [email protected] Partner Panama MAPFRE Panama Mr. Manuel Rodriguez [email protected] Partner Paraguay MAPFRE Paraguay Mr. Sergio Alvarenga [email protected] Partner Peru MAPFRE Peru Mr. Ramón Acuña Huerta [email protected] Partner Saint Martin Refer to France - - Partner Saint Barthélemy Refer to France - - Partner Saint Pierre & Miquelon Refer to France - - Partner United States Prudential Insurance Company of America Mr. -

Manulife Global Fund Unaudited Semi-Annual Report

Unaudited Semi-Annual Report Manulife Global Fund Société d'Investissement à Capital Variable for the six month period ended 31 December 2020 No subscription can be received on the basis of nancial reports. Subscriptions are only valid if made on the bases of the current prospectus, accompanied by the latest annual report and semi-annual report if published thereaer. SICAV R.C.S Luxembourg B 26 141 Contents Directors ..................................................................................................................................................... 1 Management and Administration ............................................................................................................. 2 Directors’ Report ........................................................................................................................................ 4 Statement of Net Assets ........................................................................................................................... 10 Statement of Changes in Net Assets ........................................................................................................ 15 Statement of Operations ........................................................................................................................... 20 Statistical Information ............................................................................................................................... 25 Statement of Changes in Shares ............................................................................................................. -

John Hancock Investments Adds Financial Results

Recent Highlights A Global Leader John Hancock Financial is a unit of Manulife Financial Corporation, a leading October: John Hancock completes acquisition Canada-based financial services group with principal operations in Asia, of Symetra Investment Services. Canada and the United States. October: John Hancock Investments adds Financial Results . For the quarter ended Sept. 30, 2013, the U.S. Division operations doing three new managing directors to its Institutional business under the John Hancock brand (John Hancock)2 reported earnings 3 team. attributed to shareholders of $894 million. Total premiums and deposits for the quarter from John Hancock were $11 Sept. 30: John Hancock ends quarter with 26 billion or 55% of Manulife Financial’s overall third-quarter premiums and four- and five-star rated mutual funds. deposits. 4 1 (Source: Morningstar, Inc.) . John Hancock’s funds under management were $311 billion, 56% of Manulife’s total funds under management as of Sept. 30, 2013.4 September: John Hancock Retirement Plan Services Offers Partnership Program for Retirement Plan Consultants. Strong Claims Paying Ability/Financial Strength Ratings5 A+ A.M. Best (2nd highest of 15 ratings) September: John Hancock Insurance launches Superior ability to meet ongoing obligations a new survivorship indexed universal life AA- Fitch Ratings (4th highest of 19 ratings) product. Very strong capacity to meet policyholder and contract obligations th A1 Moody’s (5 highest of 21 ratings) September: John Hancock Funds changes its Good financial security th name to John Hancock Investments. AA- Standard & Poor’s (4 highest of 21 ratings) Very strong financial security characteristics August: John Hancock's 2013 Boston Marathon Fundraising Program nets record $7.9 million for non-profit organizations. -

Widening the Circle Increasing Opportunities for Aboriginal People in the Workplace

Widening the circle Increasing opportunities for Aboriginal people in the workplace Deloitte’s Dialogue on Diversity Contents How can we increase opportunities for Aboriginal people in business? . 2 Just the facts . .4 What we learned - Begin with relationships . 6 Commit for the long term . .8 Bolster skills and education . 9 Review recruiting and hiring practices . .12 Foster cultural awareness . 15 Reach out to small business . 17 Prevent isolation . .18 Leverage goodwill . .19 Focus on retention . .19 Align programs . 21 Support Aboriginal businesses . .21 Break down myths and prejudices . 22 Tell a new story . .23 Top 10 best practices . .24 Why Dialogue on Diversity? . .25 The path from tolerance to acceptance to diversity to inclusion is a long one. Widening the circle 1 How can we increase opportunities for Aboriginal people in business? Recognizing that Aboriginal people make up the As more Aboriginal people attain higher- fastest-growing segment of Canada’s labour force level education, it is important that Canadian – with a sizeable under-25 population eager to employers provide them with a fair and fulfill its potential – Deloitte chose to make equal chance at a wide range of careers and “creating connections” between this group and advancement opportunities . By including business the focus of our Dialogue on Diversity . Aboriginal people in their talent pools, employers The dialogues, held in nine locations from can take advantage of the new perspectives that Vancouver to St . John’s, began on May 3 and often lead to innovation and improved business wrapped up on June 14, 2012 . We listened and results, while demonstrating leadership for other learned from passionate, proactive speakers who businesses . -

BMO Growth GIC Reference Portfolio

BMO® Growth GIC December 2011 - Series 56 Term 4 Years 100% Principal Protected Minimum Investment $1000 Maximum Rate of Return for the Term 17.00% (4.25% annually*) This medium term GIC allows you to participate in the growth This GIC may be right for you if you: of Canadian stocks with no risk to your principal investment. It are looking to diversify your portfolio with a medium term offers the potential to generate returns based on the investment peformance of a basket of 15 large Canadian companies. would like principal protection Reference Portfolio are willing to forego a guaranteed return for the potential to earn higher market-linked returns Company can keep your money invested until the end of the term Royal Bank of Canada (RY) Manulife Financial Corp. (MFC) Bank of Nova Scotia (The) (BNS) This GIC is an excellent way for you to gain access to the Toronto-Dominion Bank (The) (TD) returns on a portfolio of 15 large Canadian companies with the Canadian Imperial Bank of Commerce (CM) security of principal protection. Thomson Reuters (TRI) Principal protection - 100% of your original investment is returned to you at maturity Sun Life Financial Inc. (SLF) Manitoba Telecom Inc. (MBT) Higher return potential based on the performance of a portfolio of Canadian stocks Brookfield Asset Management, Class A (BAM.A) ® TransCanada Corp. (TRP) Designed in partnership with BMO Capital Markets , a market leader in creating innovative investment solutions Power Financial Corp. (PWF) Enbridge Inc. (ENB) Guaranteed by Bank of Montreal National Bank of Canada (NA) Eligible for Canada Deposit Insurance Corporation (CDIC) Teck Resources Ltd., Class B (TCK.B) deposit insurance up to applicable limits CI Financial Corp. -

2017 Preliminary Attendee List April 10-12, 2017 ● Hyatt Regency Toronto, on ● Procureconca.Wbresearch.Com

2017 Preliminary Attendee List April 10-12, 2017 ● Hyatt Regency Toronto, ON ● procureconca.wbresearch.com REGISTER NOW SPONSORSHIP Last Updated: Monday, March 27, 2017 Job Title Company Strategic Sourcing Manager 3M Canada CEO and Executive Board Chairperson ACSPE Supply Chain Manager Aecon Group Inc Senior Strategic Sourcing and Development Agropur Vice President Training, Process & Technologies Specialist – Agropur Strategic Sourcing & Development Business Travel Airbnb Marketing Analyst, Awareness and Verticals American Express, Inc. VP- Strategic Sourcing Amyantek Inc Field Marketing Mgr. - Canada Ariba Inc.(SAP Company) Association of Corporate Travel Executives Senior Regional Manager (ACTE) Sourcing Vice President Bank of Montreal Head Of Procurement Bayer Corporation Vice President, Supply Chain BC Clinical and Support Services Society Senior Strategic Procurement Manager Bell Mobility Supply and Studio Design Director Best Western International, Inc. Head, Technology Procurement BMO Financial Group Procurement Team Lead Bombardier Aerospace Manager, Sourcing Management Canada Post Corporation Manager, Sourcing Management Canada Post Corporation General Manager, Sourcing Management Canada Post Corporation Manager, Sourcing Manager Canada Post Corporation Director, Procurement Canada Post Corporation April 10-12, 2017 Hyatt Regency Toronto, ON 1.888.482.6012 Director, Strategic Sourcing, Procurement & Canadian Diabetes Association Facilities Senior Director, Vendor Governance, Expense Canadian Imperial Bank of Commerce & Contract -

Fort Hills Update

Teck Resources Limited +1 604 699 4000 Tel Suite 3300, 550 Burrard Street +1 604 699 4750 Fax Vancouver, BC Canada V6C 0B3 www.teck.com For Immediate Release Date: January 3, 2018 18-1-TR Teck Provides Update on Fort Hills Project Vancouver, B.C. – Teck Resources Limited (TSX: TECK.A and TECK.B, NYSE: TECK) (“Teck”) today provided an update on progress at the Fort Hills Project. Suncor, as operator of the Fort Hills Energy Limited Partnership, has confirmed that during 2017, the mine, primary extraction, utilities and froth assets were commissioned. More than 80% of the Fort Hills plant is now operational and has safely run at full capacity through the test runs over the past four months. All three secondary extraction trains are mechanically complete with the first train in its final commissioning stage. First oil is expected in mid-January. The second and third trains are currently being insulated and expected to start up in the first half of 2018, as planned. Fort Hills remains on track to reach 90% capacity by the end of 2018. The Fort Hills partners have resolved a previously announced commercial dispute. Suncor and Teck have each acquired an additional working interest in the Fort Hills project from Total E&P Canada (Total). Suncor’s share of the project has increased from 50.8% to 53.06% and Teck’s share has increased from 20% to 20.89%. Total’s share has decreased from 29.2% to 26.05%. Suncor and Teck have funded an increased share of the project capital, in the amounts of approximately $300M and $120M respectively, commensurate with the additional working interests, which may be further adjusted in accordance with the terms of the Fort Hills partnership agreement, as amended, based on the parties’ respective contributions to project costs. -

Match Your Gift When You Give To

Double the Impact of Your Gift Match Your Gift when you give to with the help of your employer LIST OF COMPANIES WITH MATCHING GIFT PROGRAMS Double or even triple your gift to the Schulich School of Business. Make your gift go even further! Many companies participate in gift matching programs. Some companies will even match gifts made by retirees and spouses of employees. To find out if your company has a matching gift policy, please look for your employer’s name below. If your company is eligible, request a matching gift form from your employer, complete it, and send it to us. We will do the rest. The impact of your gift may be doubled or possibly tripled! If you don’t see your company on the list, be sure to ask your Human Resources representative or Charitable Giving/ Grants Department if this is an option for you. Schulich School of Business, Development and Alumni Relations, Seymour Schulich Building, Room W362N, 4700 Keele Street, Toronto, ON M3J 1P3 Email: [email protected] • Phone: 416-736-5648 Access Pipeline Autodesk, Inc.,r,d,$50 CGC Canadian Gypsum KEY TO SYMBOLS Adobe Systems, Inc.,d,$25 B.F. Goodrich Canada Inc.,r,d,$25 Company,r,$25 Advanced Micro Devices,$25 BCD Travel,$25 CNA Financial Corporation,$25 Ratio - company matches gifts Aetna, Inc. Matching Grants,r,d BCE Inc. Canada Capital One Canada at a ratio other than 1:1 Agilent Technologies, Inc.,d,$100 BHP Billiton,$15 Carlyle Group,$25 d - board of Directors are eligible Agrium,$50 BMO Financial Group,r,d,$25 Caterpillar, Inc.,r,d,$50 to have gifts matched Aimia BP Canada Energy Company,$25 Celestica, Inc.,$25 r - retired employees are eligible Alaska Air Group, Inc. -

Q1 2021 Open Text Corp Earnings Call on November 05, 2020 / 10

REFINITIV STREETEVENTS EDITED TRANSCRIPT OTEX.TO - Q1 2021 Open Text Corp Earnings Call EVENT DATE/TIME: NOVEMBER 05, 2020 / 10:00PM GMT REFINITIV STREETEVENTS | www.refinitiv.com | Contact Us ©2020 Refinitiv. All rights reserved. Republication or redistribution of Refinitiv content, including by framing or similar means, is prohibited without the prior written consent of Refinitiv. 'Refinitiv' and the Refinitiv logo are registered trademarks of Refinitiv and its affiliated companies. NOVEMBER 05, 2020 / 10:00PM, OTEX.TO - Q1 2021 Open Text Corp Earnings Call CORPORATE PARTICIPANTS Harry Edward Blount Open Text Corporation - Senior VP & Global Head of IR Madhu Ranganathan Open Text Corporation - Executive VP & CFO Mark J. Barrenechea Open Text Corporation - Vice Chairman, CEO & CTO CONFERENCE CALL PARTICIPANTS Frank Joseph Surace Barclays Bank PLC, Research Division - Research Analyst Paul Steep Scotiabank Global Banking and Markets, Research Division - Analyst Paul Michael Treiber RBC Capital Markets, Research Division - Director of Canadian Technology & Analyst Richard Tse National Bank Financial, Inc., Research Division - MD & Technology Analyst Stephanie Doris Price CIBC Capital Markets, Research Division - Director of Institutional Equity Research and Software & Business Services Research Analyst Thanos Moschopoulos BMO Capital Markets Equity Research - VP & Analyst PRESENTATION Operator Thank you for standing by. This is the conference operator. Welcome to the OpenText Corporation First Quarter Fiscal 2021 Conference Call. (Operator Instructions) And the conference is being recorded. (Operator Instructions) I would like to turn the conference over to Mr. Harry Blount, Senior Vice President, Investor Relations. Please go ahead, sir. Harry Edward Blount - Open Text Corporation - Senior VP & Global Head of IR Thank you, operator, and good afternoon, everyone. -

Tony Jensen, President and CEO Scotiabank Mining Conference November 28, 2018 NASDAQ: RGD Cautionary Statement

NASDAQ: RGLD Tony Jensen, President and CEO Scotiabank Mining Conference November 28, 2018 NASDAQ: RGD Cautionary Statement Cautionary “Safe Harbor” Statement Under the Private Securities Litigation Reform Act of 1995: This presentation contains certain forward‐looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Such forward‐looking statements involve known and unknown risks, uncertainties, and other factors that could cause actual results to differ materially from the projections and estimates contained herein and include, but are not limited to statements with regard to: solid, steady and successful performance; expectations about second quarter sales and inventories; expectations to repay June 2019 bonds with cash from revolver; gold focus; reinvesting cash flow; disciplined capital allocation; timing of transactions; business opportunities from financial restructurings and M&A activity; growing and sustainable dividend and annual dividend increases; shareholder return; portfolio opportunity; investment in the Peak Gold Joint Venture; resultsof2017IMCresourceestimate for the Peak Gold Joint Venture and September 2018 updates thereto; results of 2018 Preliminary Economic Analysis for the Peak Gold Joint Venture, including estimates of gold production, mine life, throughput, gold and silver recovery, strip ratio, initial capital, total cash costs, and internal rate of return; expected expansion and target throughput and production at Pueblo Viejo; expected first gold and commercial production, -

Demutualization Details

Demutualization Details 1. American Mutual Life – AmerUs- Indianapolis Life Insurance Company - Central Life Assurance - Central Life Assurance merged with American Mutual in 1994. American Mutual Life was renamed AmerUs Life Insurance Company in 1995. On September 20, 2000, it demutualized to become AmerUs Group. In 2001, the company merged with Indianapolis Life, which had also undergone a demutualization. Approximately 300,000 policyholders and heirs became entitled to receive $452 million in AmerUs Group common stock and $340 million in cash and policy credits. Distribution began on July 31, 2001. Eligible policyholders received a fixed component of 20 AmerUS common shares, as well as a variable component based on policy value. Those who elected to receive cash were compensate $26 per share entitlement. In the first year after the initial public offering, the price of an AmerUS common share increased 99%. The current value of AmerUS Group stock is approximately $45 per share. 2. Anthem Insurance - On July 31, 2002 Anthem Insurance Companies, Inc. completed its conversion from a mutual insurance company to a stock company, and became a wholly owned subsidiary of Anthem, Inc. Eligible policyholders and heirs became entitled to approximately 48 million shares of Anthem, Inc. common stock and cash totaling $2.06 billion. Compensation consisted of a fixed component of 21 Anthem common shares, as well as a variable component based on policy value. The shares were offered to the public at $36. In the first year after the initial public offering, the price of an Anthem common share increased 54%. 3. Equitable Life – Axa - In 1992 the Equitable Life Assurance Society of the United States demutualized and a new parent holding company, the Equitable Companies, was listed on the New York Stock Exchange.