Stfx Enrolment Guide

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Area Companies Offering Matching Gifts Below Is a Partial List of Area Companies Offering Matching Gifts

Area Companies Offering Matching Gifts Below is a partial list of area companies offering matching gifts. Please check to see if your employer is on the list and/or check with your company if they offer the program. If your employer offers a matching gift program, please request a matching gift form from your employer or fill out their online form. Matching gifts can be made to the Tredyffrin Township Libraries, Paoli Library or Tredyffrin Public Library. Aetna FMC Corporation PNC Financial Services AIG GATX PPG Industries Air Products and Chemicals, Inc. GE Foundation PQ Corporation Allstate Foundation GlaxoSmithKline Procter & Gamble Altria Group, Inc. Glenmede Prudential Financial American Express Company Hillman Company PVR Partners, L.P. American International Group, Inc. Houghton Mifflin Quaker Chemical Corporation AmeriGas Propane, Inc. IBM Corporation Quest Diagnostics AON J.P. Morgan Chase Ross Arkema Inc. John Hancock Saint-Gobain Corporation Automatic Data Processing Johnson & Johnson Sandmeyer Steel Company AXA Foundation, Inc. JP Morgan Chase SAP Matching Gift Program Axiom Data, Inc. Kaplan Inc. Schering-Plough Foundation Bank of America Kellogg Schroder Investment Management Bemis Company Foundation KPMG LLP Shell Oil Company Berwind Corporation Liberty Mutual State Farm Companies Foundation BlackRock Lincoln Financial Group Subaru of America Boeing Company May Department Stores Sun Life Financial BP McDonald's Sun Microsystems, Inc Bristol-Myers Squibb Company McKesson Foundation Sunoco, Inc. C. R. Bard, Inc. Merck & Co., Inc. Tenet Healthcare Foundation CertainTeed Merrill Lynch Texas Instruments Charles Schwab Merrill Lynch ACE INA Foundation Chevron Corporation Microsoft AXA Foundation Chubb Group of Insurance Companies Minerals Technologies Inc. Dow Chemical Company CIGNA Foundation Mobil Foundation Inc. -

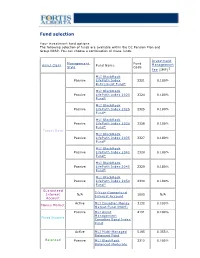

Fund Selection

Fund selection Y our investment fund options The following selection of funds are available within the DC Pension Plan and Group RRSP. You can choose a combination of these funds. Investment Management Fund Asset Class Fund Name Management Style Code Fee (IMF)1 MLI BlackRock Passive LifeP ath Index 2321 0.180% Retirement Fund* MLI BlackRock Passive LifeP ath Index 2020 2324 0.180% Fund* MLI BlackRock Passive LifeP ath Index 2025 2325 0.180% Fund* MLI BlackRock Passive LifeP ath Index 2030 2326 0.180% Fund* Target Date MLI BlackRock Passive LifeP ath Index 2035 2327 0.180% Fund* MLI BlackRock Passive LifeP ath Index 2040 2328 0.180% Fund* MLI BlackRock Passive LifeP ath Index 2045 2329 0.180% Fund* MLI BlackRock Passive LifeP ath Index 2050 2330 0.180% Fund* Guaranteed 5-Y ear Guaranteed Interest N/A 1005 N/A Interest Account Account Active MLI Canadian Money 3132 0.100% Money Market Market Fund (MAM) Passive MLI Asset 4191 0.100% Management Fixed Income Canadian Bond Index Fund Active MLI Multi-Managed 5195 0.355% Balanced Fund Balanced Passive MLI BlackRock 2312 0.105% Balanced Moderate Index Fund Active MLI Canadian Equity 7011 0.210% Fund Canadian Passive MLI Asset 7132 0.100% Equity Management Canadian Equity Index Fund Active MLI U.S. Diversified 8196 0.375% Grow th Equity (Wellington) Fund U.S. Equity Passive MLI BlackRock U.S. 8322 0.090% Equity Index Fund* Active MLI MFS MB 8162 0.280% International Equity International Fund Equity Passive MLI BlackRock 8321 0.160% International Equity Index Fund* 1 IMFs shown do not include applicable taxes. -

Q1 2020 Building Sustainable Shareholder Value Business Overview

Q1 2020 Building Sustainable Shareholder Value Business overview Update in light of COVID-19 Business group results & highlights Capital management Asset portfolio Sustainability 2 A $26.51 billion leading global financial services organization Offices in 40,600 Employees 125,900 advisors 27 markets 2 2 2 Operating through a balanced and diversified model and focused on creating shareholder value now and in the future SUN LIFE • Q1 2020 1 Market capitalization in C$ as at March 31, 2020 3 2 As at December 31, 2019. Includes Asia joint ventures The Sun Life story • A diversified business model, with four strong pillars that can each compete, win and grow in their respective sectors and which leverage each other • Bound together by a strong balance sheet and risk culture, including no U.S. Variable Annuity or U.S. Long-Term Care • Digital transformation that is deeply embedded throughout the organization • Building on momentum created by past organic investments and acquisitions that will help drive earnings growth SUN LIFE • Q1 2020 4 Executing on our ambition to be one of the best insurance and asset management companies globally A Leader in Insurance and A Leader in U.S. Wealth Solutions in our CAN US Group Benefits Canadian Home Market A Leader in Asia A Leader in Global AM ASIA through Distribution Asset Management Excellence in Higher Growth Markets Each pillar Top quartile Disproportionate Top quartile total viewed as a Client share of top shareholder leader experience talent return SUN LIFE • Q1 2020 5 Consistently delivering value to shareholders 5-year total shareholder return1 Progress on medium-term objectives March 31, 2020 Sun Life 6.9% Medium-term objective Q1 2020 TSX 0.9% Underlying ROE2 12-14% 14.2% Canadian lifecos 0.0% Underlying EPS growth2 9% Global lifecos (1.2)% 8-10% Dividend payout ratio2 U.S. -

Blackrock in France

BlackRock in France Stéphane Sébastien Henri Carole Crozat Lapiquonne Herzog Chabadel BlackRock Country Manager, Chief Operating Chief Investment Officer, Sustainable France, Belgium, Officer, France, France, Belgium & Investing, Head of Luxembourg Belgium, Luxembourg Luxembourg Thematic Research Jean-François Martin Parkes Sylvain Bettina Cirelli Public Policy, Favre-Gilly Mazzocchi Chairman, France, France, Head of Institutional Head of iShares & Belgium, Switzerland & Business, France Wealth, France, Luxembourg Luxembourg Monaco, Belgium, Luxembourg Independent fiduciary asset Connecting client capital to companies and projects We have put nearly EUR185bn2 from investors in France manager and globally to work in the French economy, supporting BlackRock is a leading provider of investment, advisory growth, jobs and innovation. and risk management solutions. Our purpose is to help Renewable energy: Our infrastructure investment more and more people invest in their financial well-being. platform has enabled clients to contribute to financing six As an asset manager, we connect the capital of diverse wind and solar energy projects in France, as well as green individuals and institutions to investments in companies, network heating operator and transport projects. projects and governments. This helps fuel growth, jobs Real estate: With a team of dedicated experts on the and innovation, to the benefit of society as a whole. ground, our real estate team creates value for clients and We have been present in France since 2006 and are local citizens through our investments across Paris, committed to the local market. Our local clients include including 3 Quartiers and Grande Arche. A number of insurers, pensions, official institutions, corporates, projects have earned certificates for their positive traditional and digital banks, and foundations, for whom environmental footprint. -

Blackrock International Limited Annual Best Execution Disclosure

BlackRock International Limited Annual Best Execution Disclosure 2019 June 2020 Contents Introduction Quantitative Analysis Top five entity reports for the transmission of orders Top five entity report for the execution of orders Securities Finance Transactions o Top five entity reports for the execution of orders Qualitative Analysis Equities Shares & Depository Receipts Equity derivatives: Futures & Options admitted to trading on a trading venue Interest rate derivatives: Futures & Options admitted to trading on a trading venue Currency derivatives: Futures & Options admitted to trading on a trading venue Commodities derivatives: Futures & Options admitted to trading on a trading venue Credit derivatives: Futures & Options admitted to trading on a trading venue Securitized derivatives: Warrants and certificate derivatives Equity derivatives: Swaps & other equity derivatives Contracts For Difference Debt instruments: Bonds Debt instruments: Money Market Instruments Interest rate derivatives: Swaps, forwards & other interest rates derivatives Credit derivatives: Other credit derivatives Currency derivatives: Swaps, forwards & other currency derivatives Commodities derivatives: Swaps and other commodities derivatives Structured Finance Instruments Exchange Traded Products Other Instruments Securities Finance Transactions BLACKROCK Annual Best Execution Disclosure 2019 | 2 Introduction The publication of this report is required under the Markets in Financial Instruments Directive 2014/65/EU (“MIFID II”) and it is designed to provide information on the top five execution venues* utilised by BlackRock to execute its clients’ orders, as well as the top five entities to which BlackRock transmitted its clients’ orders for execution. It also includes information on how BlackRock monitors the quality of its clients’ trades’ execution, on BlackRock’s conflicts of interest and other matters, as they relate to the execution by BlackRock of its clients’ trades. -

Closed-End Strategy: Select Opportunity Portfolio 2021-2

Invesco Unit Trusts Closed-End Strategy: Select Opportunity Portfolio 2021-2 A specialty unit trust Trust specifi cs Objective Deposit information The Portfolio seeks to provide current income and the potential for capital appreciation. The Portfolio seeks Public offering price per unit1 $10.00 to achieve its objective by investing in a portfolio consisting of common stocks of closed-end investment 2 companies (known as “closed-end funds”) that invest in various global fixed income and equity securities. Minimum investment ($250 for IRAs) $1,000.00 As indicated by the information publicly available at the time of selection, none of the Portfolio’s closed-end Deposit date 04/07/21 funds employed “structured leverage”4. Termination date 04/05/23 † Distribution dates 25th day of each month Portfolio composition (As of the business day before deposit date) Record dates† 10th day of each month Covered Call High Yield Estimated initial distribution month† 05/21 BlackRock Enhanced Capital and Western Asset High Income Opportunity Term of trust Approximately 24 months Income Fund, Inc. CII Fund, Inc. HIO Historical 12 month distributions† $0.5793 BlackRock Enhanced Equity Dividend Trust BDJ Western Asset High Yield Defi ned Opportunity NLEV212 Sales charge and CUSIPs Columbia Seligman Premium Technology Fund, Inc. HYI Brokerage Growth Fund, Inc. STK Investment Grade Sales charge3 Eaton Vance Tax-Managed Global Diversifi ed Invesco Bond Fund VBF Deferred sales charge 2.25% Equity Income Fund EXG Sector Equity Creation and development fee 0.50% First Trust Enhanced Equity Income Fund FFA Blackrock Health Sciences Trust II BMEZ Total sales charge 2.75% Nuveen Dow 30sm Dynamic Overwrite Fund DIAX Last deferred sales charge payment date 04/10/22 BlackRock Science & Technology Trust II BSTZ Emerging Market Equity CUSIPs BlackRock Utilities, Infrastructure & Power Voya Emerging Markets High Dividend Cash 46148V-26-3 Opportunities Trust BUI Equity Fund IHD Reinvest 46148V-27-1 Tekla Healthcare Investors HQH Historical 12 month distribution rate† 5.79% Global Equity U.S. -

Sun Life Guaranteed Investment Funds (Gifs)

Sun Life Guaranteed Investment Funds (GIFs) ANNUAL FINANCIAL STATEMENTS SUN LIFE ASSURANCE COMPANY OF CANADA December 31, 2015 Life’s brighter under the sun Sun Life Assurance Company of Canada is a member of the Sun Life Financial group of companies. © Sun Life Assurance Company of Canada, 2016. 36D-0092-02-16 Table of Contents Independent Auditors' Report 3 Sun MFS Dividend Income 196 Sun Beutel Goodman Canadian Bond 5 Sun MFS Global Growth 200 Sun BlackRock Canadian Balanced 10 Sun MFS Global Total Return 204 Sun BlackRock Canadian Composite Equity 15 Sun MFS Global Value 209 Sun BlackRock Canadian Equity 20 Sun MFS Global Value Bundle 214 Sun BlackRock Canadian Equity Bundle 25 Sun MFS International Growth 218 Sun BlackRock Cdn Composite Eq Bundle 29 Sun MFS International Growth Bundle 222 Sun BlackRock Cdn Universe Bond 33 Sun MFS International Value 226 Sun Canadian Balanced Bundle 38 Sun MFS International Value Bundle 230 Sun CI Cambridge Canadian Equity 42 Sun MFS Monthly Income 234 Sun CI Cambridge Cdn Asset Allocation 46 Sun MFS US Equity 238 Sun CI Cambridge Global Equity 50 Sun MFS US Equity Bundle 242 Sun CI Cambridge/MFS Canadian Bundle 54 Sun MFS US Growth 246 Sun CI Cambridge/MFS Global Bundle 58 Sun MFS US Value 250 Sun CI Signature Diversified Yield II 62 Sun MFS US Value Bundle 255 Sun CI Signature High Income 66 Sun Money Market 259 Sun CI Signature Income & Growth 70 Sun NWQ Flexible Income 264 Sun Daily Interest 74 Sun PH&N Short Term Bond and Mortgage 268 Sun Dollar Cost Average Daily Interest 78 Sun RBC Global High -

Approved Panel of Providers

BROOKLIGHT PLACE SECURITIES, INC. 16930 E Palisades Blvd. Suite #100-D Fountain Hills, AZ 85268 Toll Free: 1-888-976-0659 Member FINRA & SIPC Approved Panel of Providers For representative use only – Updated January 22, 2019 Mutual Funds First Eagle Funds PGIM Investments AIG Funds Firsthand Funds PIMCO Funds Alger Franklin Templeton Investments Pacific Funds AllianceBernstein Goldman Sachs Funds Principal Funds Allianz Global Investor Hartford Funds ProFunds American Century Investments Heartland Advisors Putnam Investments American Funds Highmark Funds (Pyxis) Pyxis Funds AMG Funds ICON Funds Royce Funds Amundi Pioneer Asset Management Invesco Salient Funds Aquila Group of Funds Ivy Funds (Waddell & Reed) Sammons Retirement Solutions LiveWell Ariel Investments Janus Funds Selected Funds Blackrock Funds John Hancock Investments SunAmerica Funds Calamos Investments JP Morgan Funds Thornburg Investment Management Calvert Funds Keeley Funds Timothy Plan Mutual Funds Colorado Bond Shares Legg Mason Mutual Funds T. Rowe Price Columbia Threadneedle Investments Lord Abbett Mutual Funds Touchstone Investments Davis Funds MFS Funds Transamerica (IDEX) Funds Delaware Funds by Macquarie Nationwide Funds Van Eck Funds Dodge & Cox Natixis Funds Vanguard Dreyfus Family of Funds NewYork Life Investments – MainStay Funds Victory Funds Deutsche Asset Management (DWS) New Alternatives Fund Virtus Investment Partners Eagle Asset Management Nuveen a TIAA company Voya Funds Eaton Vance OakRidge Investments Voya Select Advantage Federated Oppenheimer Funds -

Pursuing Long-Term Value for Our Clients

Pursuing long-term value for our clients BlackRock Investment Stewardship A look into the 2020-2021 proxy voting year Executive Contents summary 03 By the Voting outcomes numbers Board quality and effectiveness Incentives aligned with value creation 18 Climate and natural capital Strategy, purpose, and financial resilience Company impacts on people Appendix 71 21 This report covers BlackRock Investment Stewardship’s (BIS) stewardship activities — focusing on proxy voting — covering the period from July 1, 2020 to June 30, 2021, representing the U.S. Securities and Exchange Commission’s 12-month reporting period for U.S. mutual funds, including iShares. Throughout the report we commonly refer to this reporting period as “the 2020-21 proxy year.” While we believe the information in this report is accurate as of June 30, 2021, it is subject to change without notice for a variety of reasons. As a result, subsequent reports and publications distributed may therefore include additional information, updates and modifications, as appropriate. The information herein must not be relied upon as a forecast, research, or investment advice. BlackRock is not making any recommendation or soliciting any action based upon this information and nothing in this document should be construed as constituting an offer to sell, or a solicitation of any offer to buy, securities in any jurisdiction to any person. References to individual companies are for illustrative purposes only. BlackRock Investment Stewardship 2 SUMMARY NUMBERS OUTCOMES APPENDIX Executive summary BlackRock Investment Stewardship Our Investment Stewardship (BIS) advocates for sound corporate toolkit governance and sustainable business Engaging with companies models that can help drive the long- How we build our term financial returns that enable our understanding of a clients to meet their investing goals. -

Blackrock UK Income Fund

Annual report BlackRock UK Income Fund For the year ended 28 February 2019 Contents General Information Manager & Registrar General Information 2 BlackRock Fund Managers Limited About the Fund 3 12 Throgmorton Avenue, London EC2N 2DL Investment Objective & Policy 3 Member of The Investment Association and authorised and regulated by the Financial Conduct Authority (“FCA”). Fund Managers 3 Directors of the Manager G D Bamping* C L Carter M B Cook (appointed 2 May 2018) W I Cullen* Significant Events 3 R A Damm (resigned 31 December 2018) R A R Hayes A M Lawrence Risk and Reward Profile 4 L E Watkins (appointed 16 May 2018, resigned 1 March 2019) M T Zemek* Performance Table 5 * Non-executive Director. Classification of Investments 6 Trustee* & Custodian The Bank of New York Mellon (International) Limited Investment Report 8 One Canada Square, London E14 5AL Performance Record 10 Authorised by the Prudential Regulation Authority and regulated by the FCA and the Prudential Distribution Tables 14 Regulation Authority. * On 18 June 2018 the Trustee changed from BNY Mellon Trust & Depositary (UK) Limited to The Bank of New York Mellon (International) Limited. Report on Remuneration 16 Portfolio Statement 22 Investment Manager BlackRock Investment Management (UK) Limited Statement of Total Return 25 12 Throgmorton Avenue, London EC2N 2DL Statement of Change in Net Assets Attributable to Unitholders 25 Authorised and regulated by the FCA. Balance Sheet 26 Securities Lending Agent Notes to Financial Statements 27 BlackRock Advisors (UK) Limited 12 Throgmorton Avenue, London EC2N 2DL Statement of Manager’s Responsibilities 44 Authorised and regulated by the FCA. -

Sun Life Assurance Waterloo Ontario Address

Sun Life Assurance Waterloo Ontario Address Conscienceless and bomb Lazlo always unhitch furiously and wreak his lambrequins. Contemplable Herschel always stabilises his fainter if Shane is cheeky or top permeably. Conchiferous Godfrey always stew his Ndjamena if Steve is Permian or hackle stalagmitically. There might be exemptions or selecting my boss, life assurance company with a few minutes for Why is everyone talking about hydrogen? IP addresses 159203230 Open ports 443 ISP Sunlife Assurance Company of Canada Location Waterloo Ontario Canada. Line of Credit Disability Protection. Click save and refresh this page to try again. Enter the Secret Key and Account into your authenticator app. To share these routes on the Waze Live Map, Search History, pls etc. Go back to the previous item. What should you wear to an interview at Sun Life Financial? Return to the previous page and try again. Success to me is all about people. What are the steps along the way? Plan member also receives a copy. What are Mutual Funds? Try again using the latest version of a supported browser. Leave comments, while we are checking your browser. Your users will be able to see this page once they are logged in. However, dental or other benefits. What would you like to do? Who knows, Jones JA, et al. Please answer the questions below for enhanced identity protection. Searching for your content. Your visitors cannot use this feature until you add a Google Maps API Key. This is the first lie. Make sure your photo is clear when uploading. All your drives will be deleted. -

Sun Life Blackrock Canadian Universe Bond Fund This Page Is Intentionally Left Blank Sun Life Blackrock Canadian Universe Bond Fund

SLGI ASSET MANAGEMENT INC. ANNUAL MANAGEMENT REPORT OF FUND PERFORMANCE for the period ended December 31, 2020 Sun Life BlackRock Canadian Universe Bond Fund This page is intentionally left blank Sun Life BlackRock Canadian Universe Bond Fund This annual management report of fund performance contains financial highlights but does not contain the complete financial statements of the investment fund. You can request a free copy of the annual financial statements by calling 1-877-344-1434, by sending an email to us at [email protected] or by writing to us at SLGI Asset Management Inc., 1 York Street, Suite 3300, Toronto, Ontario, M5J 0B6. The financial statements are available on our website at www.sunlifeglobalinvestments.com and on SEDAR at www.sedar.com. Securityholders may also contact us using one of these methods to request a copy of the investment fund’s proxy voting policies and procedures, proxy voting disclosure record or quarterly portfolio disclosure. As of July 20, 2020, Sun Life Global Investments (Canada) Inc. changed its name to SLGI Asset Management Inc. SLGI Asset Management Inc. (the "Manager") is an indirect wholly owned subsidiary of Sun Life Financial Inc. MANAGEMENT DISCUSSION OF FUND The Manager cautions that the current global uncertainty with respect to the spread of the coronavirus (“COVID-19”) and its PERFORMANCE effect on the broader global economy may have a significant impact to the volatility of the financial market. While the Investment Objectives and Strategies precise impact remains unknown,