Blackrock International Limited Annual Best Execution Disclosure

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Fund Selection

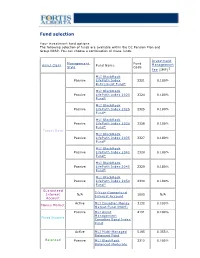

Fund selection Y our investment fund options The following selection of funds are available within the DC Pension Plan and Group RRSP. You can choose a combination of these funds. Investment Management Fund Asset Class Fund Name Management Style Code Fee (IMF)1 MLI BlackRock Passive LifeP ath Index 2321 0.180% Retirement Fund* MLI BlackRock Passive LifeP ath Index 2020 2324 0.180% Fund* MLI BlackRock Passive LifeP ath Index 2025 2325 0.180% Fund* MLI BlackRock Passive LifeP ath Index 2030 2326 0.180% Fund* Target Date MLI BlackRock Passive LifeP ath Index 2035 2327 0.180% Fund* MLI BlackRock Passive LifeP ath Index 2040 2328 0.180% Fund* MLI BlackRock Passive LifeP ath Index 2045 2329 0.180% Fund* MLI BlackRock Passive LifeP ath Index 2050 2330 0.180% Fund* Guaranteed 5-Y ear Guaranteed Interest N/A 1005 N/A Interest Account Account Active MLI Canadian Money 3132 0.100% Money Market Market Fund (MAM) Passive MLI Asset 4191 0.100% Management Fixed Income Canadian Bond Index Fund Active MLI Multi-Managed 5195 0.355% Balanced Fund Balanced Passive MLI BlackRock 2312 0.105% Balanced Moderate Index Fund Active MLI Canadian Equity 7011 0.210% Fund Canadian Passive MLI Asset 7132 0.100% Equity Management Canadian Equity Index Fund Active MLI U.S. Diversified 8196 0.375% Grow th Equity (Wellington) Fund U.S. Equity Passive MLI BlackRock U.S. 8322 0.090% Equity Index Fund* Active MLI MFS MB 8162 0.280% International Equity International Fund Equity Passive MLI BlackRock 8321 0.160% International Equity Index Fund* 1 IMFs shown do not include applicable taxes. -

Blackrock in France

BlackRock in France Stéphane Sébastien Henri Carole Crozat Lapiquonne Herzog Chabadel BlackRock Country Manager, Chief Operating Chief Investment Officer, Sustainable France, Belgium, Officer, France, France, Belgium & Investing, Head of Luxembourg Belgium, Luxembourg Luxembourg Thematic Research Jean-François Martin Parkes Sylvain Bettina Cirelli Public Policy, Favre-Gilly Mazzocchi Chairman, France, France, Head of Institutional Head of iShares & Belgium, Switzerland & Business, France Wealth, France, Luxembourg Luxembourg Monaco, Belgium, Luxembourg Independent fiduciary asset Connecting client capital to companies and projects We have put nearly EUR185bn2 from investors in France manager and globally to work in the French economy, supporting BlackRock is a leading provider of investment, advisory growth, jobs and innovation. and risk management solutions. Our purpose is to help Renewable energy: Our infrastructure investment more and more people invest in their financial well-being. platform has enabled clients to contribute to financing six As an asset manager, we connect the capital of diverse wind and solar energy projects in France, as well as green individuals and institutions to investments in companies, network heating operator and transport projects. projects and governments. This helps fuel growth, jobs Real estate: With a team of dedicated experts on the and innovation, to the benefit of society as a whole. ground, our real estate team creates value for clients and We have been present in France since 2006 and are local citizens through our investments across Paris, committed to the local market. Our local clients include including 3 Quartiers and Grande Arche. A number of insurers, pensions, official institutions, corporates, projects have earned certificates for their positive traditional and digital banks, and foundations, for whom environmental footprint. -

Closed-End Strategy: Select Opportunity Portfolio 2021-2

Invesco Unit Trusts Closed-End Strategy: Select Opportunity Portfolio 2021-2 A specialty unit trust Trust specifi cs Objective Deposit information The Portfolio seeks to provide current income and the potential for capital appreciation. The Portfolio seeks Public offering price per unit1 $10.00 to achieve its objective by investing in a portfolio consisting of common stocks of closed-end investment 2 companies (known as “closed-end funds”) that invest in various global fixed income and equity securities. Minimum investment ($250 for IRAs) $1,000.00 As indicated by the information publicly available at the time of selection, none of the Portfolio’s closed-end Deposit date 04/07/21 funds employed “structured leverage”4. Termination date 04/05/23 † Distribution dates 25th day of each month Portfolio composition (As of the business day before deposit date) Record dates† 10th day of each month Covered Call High Yield Estimated initial distribution month† 05/21 BlackRock Enhanced Capital and Western Asset High Income Opportunity Term of trust Approximately 24 months Income Fund, Inc. CII Fund, Inc. HIO Historical 12 month distributions† $0.5793 BlackRock Enhanced Equity Dividend Trust BDJ Western Asset High Yield Defi ned Opportunity NLEV212 Sales charge and CUSIPs Columbia Seligman Premium Technology Fund, Inc. HYI Brokerage Growth Fund, Inc. STK Investment Grade Sales charge3 Eaton Vance Tax-Managed Global Diversifi ed Invesco Bond Fund VBF Deferred sales charge 2.25% Equity Income Fund EXG Sector Equity Creation and development fee 0.50% First Trust Enhanced Equity Income Fund FFA Blackrock Health Sciences Trust II BMEZ Total sales charge 2.75% Nuveen Dow 30sm Dynamic Overwrite Fund DIAX Last deferred sales charge payment date 04/10/22 BlackRock Science & Technology Trust II BSTZ Emerging Market Equity CUSIPs BlackRock Utilities, Infrastructure & Power Voya Emerging Markets High Dividend Cash 46148V-26-3 Opportunities Trust BUI Equity Fund IHD Reinvest 46148V-27-1 Tekla Healthcare Investors HQH Historical 12 month distribution rate† 5.79% Global Equity U.S. -

The Impact of Portfolio Financing on Alpha Generation by H…

The Impact of Portfolio Financing on Alpha Generation by Hedge Funds An S3 Asset Management Commentary by Robert Sloan, Managing Partner and Krishna Prasad, Partner S3 Asset Management 590 Madison Avenue, 32nd Floor New York, NY 10022 Telephone: 212-759-5222 www.S3asset.com September 2004 Building a successful hedge fund requires more than just the traditional three Ps of Pedigree, Performance and Philosophy. As hedge funds’ popularity increases, it is increasingly clear that Process needs to be considered the 4th P in alpha generation. Clearly, balance sheet management, also known as securities or portfolio financing, is a key element of “process” as it adds to alpha (the hedge fund manager’s excess rate of return as compared to a benchmark). Typically, hedge funds surrender their balance sheet to their prime broker and do not fully understand the financing alpha that they often leave on the table. The prime brokerage business is an oligopoly and the top three providers virtually control the pricing of securities financing. Hedge funds and their investors therefore need to pay close heed to the value provided by their prime broker as it has a direct impact on alpha and the on-going health of a fund. Abstract As investors seek absolute returns, hedge funds have grown exponentially over the past decade. In the quest for better performance, substantial premium is being placed on alpha generation skills. Now, more than ever before, there is a great degree of interest in deconstructing and better understanding the drivers of hedge fund alpha. Investors and hedge fund managers have focused on the relevance of asset allocation, stock selection, portfolio construction and trading costs on alpha. -

Stfx Enrolment Guide

my money @ work Start saving guide it’s time to save Welcome to my money @ work Millions of Canadians participate in workplace retirement and savings plans. Now, it’s your turn because it’s your money and your future. Saving at work helps you meet your financial goals whether you’re just starting your career, midway through it or close to retirement. And this guide has what you need to get started: practical savings information to help you save and enrol in the Improved Retirement Plan for Teaching, Administration & Other Employees of St. Francis Xavier University. Being part of the Sun Life Financial community has its advantages. From making the most of your workplace plan to helping you plan for your financial future, my money @ work and Sun Life Financial are here for you. To take advantage of your dedicated Sun Life Financial Customer Care Centre representative, call 1-866-733-8612 from 8 a.m. to 8 p.m. ET any business day. Service is available in more than 190 languages. Group Retirement Services are provided by Sun Life Assurance Company of Canada, 2 aSun member Life Financial of the Sun Life Financial group of companies. Three easy steps… 1 READ 4 my money @ work Why save now? My plan What’s in it for me? 2 INVEST 9 my investments A choice of investment approaches Diverse selection of investment options Investment risk profiler 3 ENROL 15 mysunlife.ca It’s action time! We’re with you World of information & tools FORMS 18 my money @ work 3 READ 4 Sun Life Financial my money @ work There is no better way to save for your future than through your plan @ work. -

Datalend Api

DATALEND API Business intelligence and data analytics tools are increasingly crucial for securities finance market participants. DataLend’s robust and award-winning securities finance market data allows firms to make the most informed trading decisions with its comprehensive, global data set and powerful analytical tools. The DataLend API offers direct access to DataLend’s database in a fast, flexible and developer-friendly solution ready to be tailored for a firm’s proprietary system. $19.6 trillion $2.5 trillion 49,000+ lendable on loan securities on loan * Data as of June 2018 THE DATALEND API ADVANTAGE » Instant access to the DataLend ecosystem » Simplified integration to your business intelligence tools » No expensive or time-consuming storage and ETL process to maintain » Amendments to data are automatically reflected » New data fields are easily implemented » Historical data NOTES FOR DEVELOPERS » Up-to-date RESTful API architecture implemented on scalable, cloud-based technologies » Built with HTTP Web standards for direct compatibility with open-source libraries in many software languages » Sub-second response times, ensuring a consistent and swift experience » Well-formed concrete nouns for the securities lending industry and standard HTTP verbs for the request » All queries are executed over HTTPS, ensuring secure BEST SECURITIES FINANCE communication MARKET DATA PROVIDER » Authentication and authorization based on latest OAuth GLOBALLY 2.0 standards Global Investor/ISF Awards 2013, 2014, 2015, 2016, 2017 WHO WE ARE EquiLend is a leading provider of trading, post-trade, market data and clearing services for the securities finance industry with offices in New York, London, Hong Kong and Toronto. EquiLend is owned by BlackRock, Credit Suisse, Goldman Sachs, JP Morgan, JP Morgan Chase, Bank of America Merrill Lynch, Morgan Stanley, Northern Trust, State Street and UBS. -

Pursuing Long-Term Value for Our Clients

Pursuing long-term value for our clients BlackRock Investment Stewardship A look into the 2020-2021 proxy voting year Executive Contents summary 03 By the Voting outcomes numbers Board quality and effectiveness Incentives aligned with value creation 18 Climate and natural capital Strategy, purpose, and financial resilience Company impacts on people Appendix 71 21 This report covers BlackRock Investment Stewardship’s (BIS) stewardship activities — focusing on proxy voting — covering the period from July 1, 2020 to June 30, 2021, representing the U.S. Securities and Exchange Commission’s 12-month reporting period for U.S. mutual funds, including iShares. Throughout the report we commonly refer to this reporting period as “the 2020-21 proxy year.” While we believe the information in this report is accurate as of June 30, 2021, it is subject to change without notice for a variety of reasons. As a result, subsequent reports and publications distributed may therefore include additional information, updates and modifications, as appropriate. The information herein must not be relied upon as a forecast, research, or investment advice. BlackRock is not making any recommendation or soliciting any action based upon this information and nothing in this document should be construed as constituting an offer to sell, or a solicitation of any offer to buy, securities in any jurisdiction to any person. References to individual companies are for illustrative purposes only. BlackRock Investment Stewardship 2 SUMMARY NUMBERS OUTCOMES APPENDIX Executive summary BlackRock Investment Stewardship Our Investment Stewardship (BIS) advocates for sound corporate toolkit governance and sustainable business Engaging with companies models that can help drive the long- How we build our term financial returns that enable our understanding of a clients to meet their investing goals. -

Blackrock UK Income Fund

Annual report BlackRock UK Income Fund For the year ended 28 February 2019 Contents General Information Manager & Registrar General Information 2 BlackRock Fund Managers Limited About the Fund 3 12 Throgmorton Avenue, London EC2N 2DL Investment Objective & Policy 3 Member of The Investment Association and authorised and regulated by the Financial Conduct Authority (“FCA”). Fund Managers 3 Directors of the Manager G D Bamping* C L Carter M B Cook (appointed 2 May 2018) W I Cullen* Significant Events 3 R A Damm (resigned 31 December 2018) R A R Hayes A M Lawrence Risk and Reward Profile 4 L E Watkins (appointed 16 May 2018, resigned 1 March 2019) M T Zemek* Performance Table 5 * Non-executive Director. Classification of Investments 6 Trustee* & Custodian The Bank of New York Mellon (International) Limited Investment Report 8 One Canada Square, London E14 5AL Performance Record 10 Authorised by the Prudential Regulation Authority and regulated by the FCA and the Prudential Distribution Tables 14 Regulation Authority. * On 18 June 2018 the Trustee changed from BNY Mellon Trust & Depositary (UK) Limited to The Bank of New York Mellon (International) Limited. Report on Remuneration 16 Portfolio Statement 22 Investment Manager BlackRock Investment Management (UK) Limited Statement of Total Return 25 12 Throgmorton Avenue, London EC2N 2DL Statement of Change in Net Assets Attributable to Unitholders 25 Authorised and regulated by the FCA. Balance Sheet 26 Securities Lending Agent Notes to Financial Statements 27 BlackRock Advisors (UK) Limited 12 Throgmorton Avenue, London EC2N 2DL Statement of Manager’s Responsibilities 44 Authorised and regulated by the FCA. -

Sun Life Blackrock Canadian Universe Bond Fund This Page Is Intentionally Left Blank Sun Life Blackrock Canadian Universe Bond Fund

SLGI ASSET MANAGEMENT INC. ANNUAL MANAGEMENT REPORT OF FUND PERFORMANCE for the period ended December 31, 2020 Sun Life BlackRock Canadian Universe Bond Fund This page is intentionally left blank Sun Life BlackRock Canadian Universe Bond Fund This annual management report of fund performance contains financial highlights but does not contain the complete financial statements of the investment fund. You can request a free copy of the annual financial statements by calling 1-877-344-1434, by sending an email to us at [email protected] or by writing to us at SLGI Asset Management Inc., 1 York Street, Suite 3300, Toronto, Ontario, M5J 0B6. The financial statements are available on our website at www.sunlifeglobalinvestments.com and on SEDAR at www.sedar.com. Securityholders may also contact us using one of these methods to request a copy of the investment fund’s proxy voting policies and procedures, proxy voting disclosure record or quarterly portfolio disclosure. As of July 20, 2020, Sun Life Global Investments (Canada) Inc. changed its name to SLGI Asset Management Inc. SLGI Asset Management Inc. (the "Manager") is an indirect wholly owned subsidiary of Sun Life Financial Inc. MANAGEMENT DISCUSSION OF FUND The Manager cautions that the current global uncertainty with respect to the spread of the coronavirus (“COVID-19”) and its PERFORMANCE effect on the broader global economy may have a significant impact to the volatility of the financial market. While the Investment Objectives and Strategies precise impact remains unknown, -

QS-Holdco-Complaint.Pdf

Case 1:18-cv-00824-RJS Document 1 Filed 01/30/18 Page 1 of 104 UNITED STATES DISTRICT COURT SOUTHERN DISTRICT OF NEW YORK QS HOLDCO INC., Plaintiff, Index No. -against- COMPLAINT BANK OF AMERICA CORPORATION; MERRILL LYNCH, PIERCE, FENNER & SMITH DEMAND FOR JURY TRIAL INCORPORATED; MERRILL LYNCH L.P. HOLDINGS, INC.; CREDIT SUISSE AG; CREDIT SUISSE GROUP AG; CREDIT SUISSE SECURITIES (USA) LLC; CREDIT SUISSE FIRST BOSTON NEXT FUND, INC.; THE GOLDMAN SACHS GROUP, INC.; GOLDMAN, SACHS & CO. LLC; GOLDMAN SACHS EXECUTION & CLEARING, L.P.; J.P. MORGAN CHASE & CO.; J.P. MORGAN SECURITIES LLC; J.P. MORGAN PRIME, INC.; J.P. MORGAN STRATEGIC SECURITIES LENDING CORP.; J.P. MORGAN CHASE BANK, N.A.; MORGAN STANLEY; MORGAN STANLEY CAPITAL MANAGEMENT, LLC; MORGAN STANLEY & CO. LLC; PRIME DEALER SERVICES CORP.; STRATEGIC INVESTMENTS I, INC.; UBS GROUP AG; UBS AG; UBS AMERICAS INC.; UBS SECURITIES LLC; UBS FINANCIAL SERVICES INC.; EQUILEND LLC; EQUILEND EUROPE LIMITED; and EQUILEND HOLDINGS LLC, Defendants. Case 1:18-cv-00824-RJS Document 1 Filed 01/30/18 Page 2 of 104 TABLE OF CONTENTS OVERVIEW OF THE ACTION .....................................................................................................1 JURISDICTION AND VENUE ....................................................................................................10 PARTIES .......................................................................................................................................12 A. Plaintiff ..................................................................................................................12 -

Megatrends Product Brief

INVEST IN THE FUTURE iShares megatrends ETFs Introducing megatrends The modern world is changing at the speed of innovation, transforming the way we live and work. We see this change, and the pull of the future, through megatrends – powerful, transformative forces that can change the trajectory of the global economy by shifting the priorities of societies, driving innovation and redefining business models. BlackRock has identified 5 megatrends as the long-term forces shaping our future and offers a suite of megatrend ETFs to help investors position for tomorrow. Products: • iShares Exponential Technologies ETF (XT) Technology is driving Technological exponential progress in • iShares U.S. Tech Breakthrough Multisector ETF (TECB) Breakthrough the tech sector and far • iShares Robotics and Artificial Intelligence ETF (IRBO) beyond • iShares Cybersecurity ETF (IHAK) • iShares Cloud and 5G Multisector ETF (IDAT) Product: Longer lifespans and Demographics • iShares Genomics Immunology and Healthcare ETF (IDNA) & Social Change modern lifestyles will change medicine and • iShares Virtual Work and Life Multisector ETF (IWFH) consumer habits Products: Rapid Mass migration to cities • iShares Global Infrastructure ETF (IGF) Urbanization will require new business • iShares U.S. Infrastructure ETF (IFRA) models and infrastructure • iShares Emerging Markets Infrastructure ETF (EMIF) Products: Climate Change Demand for a clean, • iShares Global Clean Energy ETF (ICLN) & Resource green tomorrow will • iShares Self-Driving EV and Tech ETF (IDRV) Scarcity -

Investment Options — Portal I

Retirement Gateway® Group Variable Annuity investment options — Portal I Allocation Portfolios Large Cap Growth (Continued) Mid-Cap Growth (Continued) Short-Term Bonds AXA Aggressive Allocation B Franklin DynaTech R Eaton Vance Atlanta Capital SMID-Cap R EQ/PIMCO Ultra Short Bond IB AXA Conservative Allocation B Franklin Growth R Franklin Small-Mid Cap Growth R American Century Short Dur Inf PrBd R AXA Conservative PLUS Allocation B Janus Forty R Janus Enterprise R International Stocks AXA Growth Strategy IB MFS Growth R1 Lord Abbett Growth Opportunities R3 Developed Markets AXA Moderate Allocation B MFS Massachusetts Investors Growth Stock R1 Neuberger Berman Mid Cap Growth R3 EQ/International Core PLUS IB AXA Moderate PLUS Allocation B Neuberger Berman Guardian R3 Oppenheimer Discovery Mid Cap Growth R EQ/International Equity Index IB AXA/Franklin Templeton Allocation Neuberger Berman Socially Responsive R3 Mid-Cap Value ClearBridge International Value R Managed Volatility IB Prudential Jennison 20/20 Focus R AXA Mid Cap Value Managed Volatility IB Federated InterContinental R American Century One Choice 2020 Portfolio R Prudential Jennison Growth R AXA/Mutual Large Cap Equity Invesco International Growth R American Century One Choice 2025 Portfolio R T. Rowe Price Blue Chip Growth R Managed Volatility IB Janus International Equity R American Century One Choice 2030 Portfolio R T. Rowe Price Growth Stock R Multimanager Mid Cap Value IB Janus Overseas R American Century One Choice 2035 Portfolio R Large Cap Value AB Discovery Value R