2017 Economic Development for a Growing Economy (EDGE)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

In This Month's Newsletter

Data-Based Consulting Heavy Equipment Rental In this month’s newsletter: 2 Monthly Commentary and Summary 3 Recent Industry News 6 Loan Market Update & Technical Conditions Knowledge-Based Cons. Non-Heavy Equip. Rental 8 Revolver and Term Loan Recent Issuance 11 Investment Grade Bond Market Update & Outlook 13 Investment Grade Recent Bond Issuance 14 Investment Grade Debt Comparables Advertising / Marketing Facility Services 17 High Yield Bond Market Update & Outlook 19 High Yield Recent Bond Issuance 20 High Yield Debt Comparables 22 Equity Capital Markets Update & Outlook Printing Services Auction Services 24 Equity Capital Markets Relative Valuation 25 Equity Capital Markets Recent Issuance 26 Operating Statistics Diversified / Other 29 Macroeconomic Indicators 32 Current Interest Rate Environment 33 Notable Mergers and Acquisitions Activity 36 KeyCorp & KBCM Overview & Capabilities Disclosure: KeyBanc Capital Markets is a trade name under which corporate and investment banking products and services of KeyCorp and its subsidiaries, KeyBanc Capital Markets Inc., Member NYSE/FINRA/SIPC, and KeyBank National Association (“KeyBank N.A.”), are marketed. Securities products and services are offered by KeyBanc Capital Markets Inc. and its licensed securities representatives, who may also be employees of KeyBank N.A. Banking products and services are offered by KeyBank N.A. This report was not issued by our research department. The information contained in this report has been obtained from sources deemed to be reliable but is not represented to be complete, and it should not be relied upon as such. This report does not purport to be a complete analysis of any security, issuer, or industry and is not an offer or a solicitation of an offer to buy or sell any securities. -

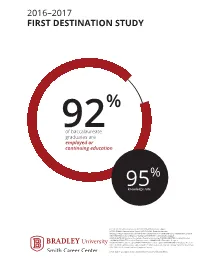

2016–2017 First Destination Study

2016–2017 FIRST DESTINATION STUDY % 92of baccalaureate graduates are employed or continuing education % 95knowledge rate JOE BATTELLINE–Associate Director JUDY BROWN–Administrative Support JESSICA CURRAN–Administrative Support JESSICA DEPKE–Graduate Assistant KRYSTLE DORSEY–Assistant Director KIM DUNN–Assistant Director HANNAH GODSIL–Administrative Support KEN HARDING–Director of Employer Testing LISA HINTHORN–Administrative Support DAWN KOELTZOW–Director of the Springer Center for Internships CARMEN KREMITZKI–Assistant Director SANDRA MCDERMOTT–Director of Employer Services AMANDA MELLEY–Graphic Designer DYLAN PASHKE–Graphic Designer JANET PESEK–Administrative Support HANNAH RAMLO–Graduate Assistant KIRSTEN RINGEL–Administrative Support DAVID SCHWARTZ–Assistant Director, Springer Center for Internships RICK SMITH, PH.D.–Senior Director of Employer Services JON C. NEIDY - Executive Director, Assistant Vice President of Student Affairs 2016–2017 BACCALAUREATE GRADUATES FIRST DESTINATION STUDY EXECUTIVE SUMMARY 13% 78% continuing education employed 9% still seeking baccalaureate graduates participated used the services knowledge in experiential of Smith Career 1,117 of 1,065 96% learning 96% Center 576 EMPLOYERS hired our ‘16–’17 across 30 states and 5 countries baccalaureate graduates 2016–2017 BACCALAUREATE GRADUATES 85% 7% 8% 20 40 60 80 $29,120–$110,000 FOSTER % salary offers range COLLEGE 45% OF BUSINESS 92 salaries reported career outcomes 96% 72% 11% 17% $20,000–$58,600 SLANE salary offers range COLLEGE OF 25% COMMUNICATIONS % salaries -

Approved Storage Facilities Address City Province Postal 17Th Street Storage Ltd

APPROVED STORAGE FACILITIES ADDRESS CITY PROVINCE POSTAL 17TH STREET STORAGE LTD. 7403 - 17 STREET EDMONTON AB T6P 1P1 20/20 STORAGE RR #3 VEGREVILLE AB T9G 1T7 2-A MINI STORAGE 730 HIGHFIELD GATE CARSTAIRS AB T0M 0N0 A AWARD MOVING & STORAGE 6149 - 80 ST. EDMONTON AB T6E 2W8 A STORAGE COMPANY 815 MORAINE ROAD NE CALGARY AB T32 2A5 A STORAGE COMPANY BOX 1133 OKOTOKS AB T15 1B2 A STORAGE COMPANY INC 130 COMMERCIAL COURT CALGARY AB T3Z 2A5 A Z MINI STORAGE 6306 47TH AVE WETASKIWIN AB T9A 2G4 A-1 MOVING & STORAGE 12946 - 54 STREET EDMONTON AB T5A 5A8 A1 STORAGE 5505 BROADWAY AVENUE BLACKFALDS AB T0M 0J0 A-1 STORAGE FACILITY 5608 - 62 STREET TABER AB T1G 1Y5 AAA ACADIA MOVING & STORAGE 9976 - 29 AVENUE EDMONTON AB T6N 1A2 AAA APARTMENT MOVERS 16715 - 113 AVENUE EDMONTON AB T5L 4L6 AAA MOVING & STORAGE 1510 - 10 AVENUE SW CALGARY AB T3C 0J5 A-ABCAN MOVING 7516 - 36 ST. NE CALGARY AB T2E 6V2 AAIMS STORAGE 10812 - 99 STREET CLAIRMONT AB T0H 0W0 AB FIRST CHOICE 6321 -76TH AVENUE EDMONTON AB T6B 0A7 AB STORAGE 4904 - 79 STREET RED DEER AB T4P 2V2 AB STORAGE SOUTH 203 PETROLIUM PARK RED DEER AB T4E 8T6 AB STORAGE SOUTH 203-37565 HWY #2 RED DEER COUNTY AB T4E 1B4 ABUHLER'S MOVING & STORAGE BAY 36, 5225 - 5TH STREET NE CALGARY AB T2E 8T6 ACADEMY MOVING 4217 - 16A STREET SE CALGARY AB T2G 3T9 ACCESS MINI STORAGE 603 EASTLAKE ROAK, BOX 3474 AIRDRIE AB T4B 2B7 ACCESS MINI STORAGE 21211 - 100 AVENUE EDMONTON AB T5T 5X8 ACCESS SELF AND RV STORAGE 14255 100 ST. -

Economic Incentives and Compliance Report INDIANA ECONOMIC DEVELOPMENT CORPORATION

Economic Incentives and Compliance Report INDIANA ECONOMIC DEVELOPMENT CORPORATION For the Reporting Period January 1, 2005 – June 30, 2013 Indiana Economic Development Corporation | One North Capitol, Suite 700 | Indianapolis, Indiana 46204 800.463.8081 | tel 317.232.8800 | fax 317.232.4146 | iedc.in.gov ECONOMIC INCENTIVES AND COMPLIANCE REPORT For the Reporting Period January 1, 2005 – June 30, 2013 in thousands of new jobs for A MESSAGE FROM: Hoosiers and an improved standard of living. How do we do that? This report will give you the details so you are better able to understand how your tax dollars Dear Fellow Hoosiers: are being used to make your State The Indiana Economic better for you and your family. Development Corporation, which Our goal is to support and was formed in 2005 to succeed the VICTOR P. SMITH encourage our business economy, SECRETARY OF COMMERCE Department of Commerce, in alignment with the goals outlined continues to excel in new and in Governor Pence’s Roadmap for innovative ways. We’re a team of Making Indiana the State that professionals: sales managers, Works. See the Roadmap at marketing specialists, strategists, www.in.gov/gov/2530.htm. These and financial analysts to name a include increasing private sector few. We are the State that Works. employment, attracting new Our strategy has been a investment especially in certain resounding success. Since 2005, as sectors (manufacturing, the following report shows, we’ve agriculture, life sciences and played an integral role in bringing logistics), and improving our ERIC DODEN Hoosier workforce. PRESIDENT new businesses to Indiana, resulting Page 1 ECONOMIC INCENTIVES AND COMPLIANCE REPORT For the Reporting Period January 1, 2005 – June 30, 2013 To accomplish those goals, we understanding, stating how many performing and if they are meeting work with established contacts, jobs the company plans to create, or exceeding expectations. -

1. Appendix 1 Codes Prep Codes, Data Element 751

VOLVO Applications of ASC 12 Version: 9705-4 Published 2005-02-10 1. Appendix 1 Codes Prep Codes, Data element 751 00 According to Drawing 01 No Surface Treatment 02 Primer, Undercoats or Corr. Finish 03 Rustproof, parts ‘Y700/3’ 04 Top Coat 05 Zinc-plating 06 Hot Zinc Coat 09 Prep According to separate notes 14 Top Coat, Black 15 Top Coat, Black, High Gloss Packaging Codes, Data element 754 A Vendor packs in VTNA multiple package quantity B Vendor packages individually in suitable container C Vendor packs multiple components into individual kits D VTNA packs in selling multiple (corr container) E VTNA packs in selling multiple (merchandising carton) F VTNA packs individually (corr container) G VTNA packs individually (merchandise carton) H VTNA packs individually (wood crate) K VTNA packs multiple components into kits L VTNA packages individually (polybag) M VTNA packs in selling multiple (polybag) N Vendor: quantity ordered is for sets not pieces P VTNA special packaging instructions S Please cut and supply in .... foot lengths T Vendor cut and supply in .... meter lengths Z Package to VTNA work instruction 930.350 issue 02 VV Description gives an extended code, the Volvo company involved will gives a separate instruction about the codes. Appendix 1 Codes 1:1 VOLVO Applications of ASC 12 Version: 9705-4 Published 2005-02-10 Ship/Delivery or Calendar Pattern Codes, Data element 678 Code Description A Monday through Friday B Monday through Saturday C Monday through Sunday D Monday E Tuesday F Wednesday G Thursday H Friday J Saturday K Sunday L Monday through Thursday M Immediately N As Directed O Daily Mon. -

Reason for Removal of Companies from Sample

Schedule D-6 Part 12 Page 1 of 966 Number of Companies Sheet Name Beginning Ending Reason for Removal of Companies from Sample US Screen 2585 2283 Removed all companies incorporated outside of the US Equity Screen 2283 476 Removed all companies with 2007 common equity of less than $100 million, and all companies with missing or negative common equity in Market Screen 476 458 Removed all companies with less than 60 months of market data Dividend Screen 458 298 Removed all companies with no dividend payment in any quarter of any year Trading Screen 298 297 Removed all companies whose 2007 trading volume to shares outstanding percentage was less than 5% Rating Screen 297 238 Removed all companies with non-investment grade rating from S&P, and removed all companies with a Value Line Safety Rank of 4 or 5 Beta Screen 238 91 Removed all companies with Value Line Betas of 1 or more ROE Screen 91 81 Removed those companies whose average 1996-2007 ROE was outside a range of 1 std. deviation from the average Final Set 81 81 DivQtr04-08 data on quarterly dividend payouts MktHistory data on monthly price closes Trading Volume data on 2007 trading volume and shares outstanding S&P Debt Rating data on S&P debt ratings CEQ% data on 2006 and 2007 common equity ratios ROE data on ROE for 1996-2007 ROE Check calculation for ROE Screen Schedule D-6 Part 12 Page 2 of 966 any year 1991 through 2007 Schedule D-6 Part 12 Page 3 of 966 GICS Country of Economic Incorporati Company Name Ticker SymbSector on 1‐800‐FLOWERS.COM FLWS 25 0 3CI COMPLETE COMPLIANCE CORP TCCC 20 0 3D SYSTEMS CORP TDSC 20 0 3M CO MMM 20 0 4KIDS ENTERTAINMENT INC KDE 25 0 800 TRAVEL SYSTEMS INC IFLYQ 25 0 99 CENTS ONLY STORES NDN 25 0 A. -

TT100 For-Hire 07 Online.Qxd

A Word From the Publisher n this 2007 edition of the Trans- The shift to private owner- port Topics Top 100 For-Hire ship is also reflected in the pur- Carriers, the focus has shifted chase of Swift Transportation from Main Street to Wall Street. by its former chairman Jerry Private equity investment firms Moyes and the proposed buy- have become the driving force for out of U.S. Xpress Enterprises I by top executives of that com- change, based on our annual review of financial and operating statistics pany. for the nation’s top for-hire trucking No one knows how long this companies. trend will last, or even how suc- Of course, well-heeled investors cessful these new investment and Wall Street money managers strategies will be over the long have been involved in trucking term. But what is clear from a before, but today’s breed of money reading of the Transport Topics men appears to be taking a different Top 100 For-Hire Carriers list approach than did the corporate is a sense that the game has raiders in the 1980s who used high- Howard S. Abramson changed. interest debt to target vulnerable With private equity funds companies. And they are different from the Inter- providing a source of new capital, many carriers net-inspired corporate roll-ups that we saw in the are making investments in technology and 1990s when small companies were patched expanding services in order to increase their together to create new, bigger businesses that share of the freight market. were assumed to have magical superhero market They say you can’t tell the players without a power. -

Ctpf Illinois Economic Opportunity Report

CTPF ILLINOIS ECONOMIC OPPORTUNITY REPORT As Required by Public Act 096-0753 for the period ending June 30, 2021 202 1 TABLE OF CONTENTS TABLE I 1 Illinois-based Investment Manager Firms Investing on Behalf of CTPF TABLE II Illinois-based Private Equity Partnerships, Portfolio Companies, 2 Infrastructure, and Real Estate Properties in the CTPF Portfolio TABLE III 14 Illinois-based Public Equity Market Value of Shares Held in CTPF’s Portfolio TABLE IV 18 Illinois-based Fixed Income Market Value of Shares Held in CTPF’s Portfolio TABLE V Domestic Equity Brokerage Commissions Paid to Illinois-based 19 Brokers/Dealers TABLE VI 20 International Equity Brokerage Commissions Paid to Illinois-based Brokers/Dealers TABLE VII Fixed Income Volume Traded through Illinois-based Brokers/Dealers 21 (par value) 2021 CTPF ILLINOIS ECONOMIC OPPORTUNITY REPORT REQUIRED BY PUBLIC ACT 096-0753 FOR THE PERIOD ENDING JUNE 30, 2021 TABLE I Illinois-based Investment Manager Firms Investing on Behalf of CTPF Table I identifies the economic opportunity investments made by CTPF with Illinois-based investment management companies. As of June 30, 2021, Total Market/Fair Value of Illinois-based investment managers was $3,121,157,662.18 (23.74%) of the total CTPF investment portfolio of $13,145,258,889.14. Market/Fair Value % of Total Fund Investment Manager Firms Location As of 6/30/2021 (reported in millions) Adams Street Chicago $ 319.69 2.43% Ariel Capital Management Chicago 83.44 0.63% Attucks Asset Management Chicago 274.06 2.08% Ativo Capital Management1 Chicago -

Speaker Bios

36TH ANNUAL SEMINAR PRESENTED BY Wednesday, April 24th, 2019 Chicago’s Multi-Modal CSCMP CHICAGO, NASSTRAC, 8:00 am – 6:00 pm Supply Chain: and the TRAFFIC CLUB OF CHICAGO Air, Water, Rail, and Road Union League Club of Chicago SPEAKER BIOS George Abernathy Stephen Bindbeutel President Director of Product Solutions FreightWaves Truckstop.com George Abernathy is President at Stephen Bindbeutel grew up in the Metro FreightWaves. In this role, George over- Detroit area. After graduating from sees all revenue generating activities Michigan State University with a degree for the company and is flanked by one in Economics, he moved to Atlanta to of the deepest benches in the freight join AT&T’s Leadership Development startup scene. Program. Prior to joining FreightWaves,, Abernathy led the Transflo sales Bindbeutel joined Truckstop.com in Chicago as Director of Product and business development organization. He has also served as Solutions after spending nearly five years in the transportation President of Transplace during the company’s rapid ascension industry at Coyote Logistics. During that time he focused on into becoming a top 3PL, managing billions in North American understanding Carrier/Driver challenges, finding ways to make freight spend. Also at Transplace, he held the role of Executive the freight industry more efficient, and improving the digital Vice President and Chief Operating Officer and was a key products that helped carriers run their business. contributor in the company’s sale to Greenbriar Equity Partners in 2013. At Truckstop.com he will continue to work on improving digital service offerings, enhancing overall user experience, and will In addition to Transflo and Transplace, Abernathy has had an ex- lead the organization’s emerging technology and transportation tensive career that includes more than 30 years of supply chain market research. -

1991 Rail Vs Truck Fuel Efficiency

Rail vs. Truck Fuel Efficiency: U.S. Department The Relative Fuel Efficiency of Truck of Transportation Competitive Rail Freight and Federal Railroad Administration Truck Operations Compared in a Range of Corridors Office of Policy FINAL REPORT Abacus Technology Corporation Chevy Chase, Maryland Moving America New Directions, New Opportunities DOT/FRA/RRP-91/2 April 1991 Document is available to the public through the National Technical Information Service, Springfield, VA 22161 Technical Report Documentation Page 1 • R e p o rt N o . 2. Government Accession No. 3. Recipient's Catolog No. FRA-RRP-91-02 4. Title and Subtitle 5. Report Date Rail vs Truck Fuel Efficiency: The Relative Fuel Efficiency of Truck Competitive Rail Freight and Truck 6. Performing Organizotion Code Operations Compared in a Range of Corridors 8. -Performing Organization Report No. 7. Authors) Abacus Technology Corporation 9. Performing Organization Name and Address 10. Work Unit No. (TRAIS) Abacus Technology Corporation 5454 Wisconsin Avenue, Suite 1100 11. Contract or Grant No. DTFR-53-90-C-00017 Chevy Chase, Maryland 20815 13. Type of Report and Period Covered 12. Sponsoring Agency Name and Address U.S. Department of Transportation Final Report Federal Railroad Administration Office of Policy, RRP-32 14. Sponsoring Agency Code Washington, DC 20590 Federal Railroad Admin. 15. Supplementary Notes William Gelston (Chief, Economic Studies Division, FRA), Project Sponsor Marilyn W. Klein (Senior Policy Analyst, FRA), Project Monitor 16. Abstract This report summarizes the findings of a study to evaluate the fuel efficiency of rail freight operations relative to competing truckload service. The objective of the study was to identify the circumstances in which rail freight service offers a fuel efficiency advantage over alternative truckload options, and to estimate the fuel savings associated with using rail service. -

Spring 2012 / Printemps 2012 PUBLISHED APRIL 2012 Tél

C A N A D I A N Spring/Printemps 2012 E H T The Bi-Annual Magazine and Directory of the Canadian Association of Movers/ RevueMOVER semestrielle et annuaire de l’Association canadienne des déménageurs INSIDE — À L’INTERIEUR REALTOR® Advice to Consumers — REALTOR® conseils aux consommateurs Membership Listings — Liste des membres Insurance ♦ since 1924 Protect Your BOTTOM LINE YOUR RISKS > OUR SOLUTIONS “ Helping you to defi ne your risks and control them in the most cost effi cient way” > Improve your risk profi le > Reduce future claims > Control insurance costs ♦ Representing Movers across the country for over 20 years 55 York Street, Suite 200 ♦ Dedicated moving account team Toronto, Ontario M5J 1R7 ♦ Family run and managed, 85 years of history, Phone 416-777-2722 over 55 professionals, licensed in all Provinces ♦ Bilingual service available Fax 416-777-2716 ♦ Proud supporter of CALL US: 1-877-364-4589 www.moversinsurance.ca Published by/publié par : CANADIAN DÉMÉNAGEUR Canadian Association of Movers/ L’Association canadienne des LE H déménageurs THE MOVER CANADIEN PO Box 30039 RPO New Westminster The Bi-Annual Magazine and Directory of the Canadian Association of Movers/ Thornhill, ON L4J 0C6 Revue semestrielle et annuaire de l’Association canadienne des déménageurs Tel.: toll free 1-866-860-0065 Spring 2012 / Printemps 2012 PUBLISHED APRIL 2012 Tél. : sans frais 1-877-656-4993 Fax/Téléc. : 905-764-0765 Email/courriel : [email protected] TABLE OF CONTENTS/TABLE DES MATIÈRES Website/Site web : www.mover.net © 2012 Canadian Association of Movers. Chairman’s Message All rights reserved. The contents of this 6 Message du président du conseil publication may not be reproduced by any means, in whole or in part, without the President’s Message prior written consent of the publisher. -

Most Influential Commercial Real Estate Brokers in Chicago, a Lease in the Loop, and Blue Star Deerfield

CRAIN’S CUSTOM CONTENT BEN AZULAY JEFFREY BRAMSON Principal Senior Managing Director MOST INFLUENTIAL Bradford Allen HFF Since joining Earlier this Bradford year, Jeffrey Allen in 2004, Bramson was Ben Azulay recognized by COMMERCIAL has been a NAIOP Chicago significant for his role in contributor the team that to the success and growth of sold Chicago’s Old Main Post the company, supporting the Office. It’s among the highest- REAL ESTATE firm’s research and recruiting profile of the 88 deals valued efforts and mentoring new at more than $7 billion that he’s brokers—all while overseeing been involved with over the last the firm’s tenant representation three years. Other highlights BROKERS department. Over the last include the $467.5 million sale of three years he’s represented AMA Plaza in Chicago, the $185 GrubHub, MedSpeed, and million sale of 500 W. Adams Foley & Mansfield in Chicago- in Chicago, the sale of the IN CHICAGO area headquarters expansions. Riverway campus in Rosemont, He also represented Walton and the sale of the four-building Isaacson in securing a new Corporate 500 office park in Welcome to the inaugural edition of The Most Influential Commercial Real Estate Brokers in Chicago, a lease in the Loop, and Blue Star Deerfield. Notable clients include special custom content section from Crain’s Custom Media. Properties in the purchase of Intercontinental Real Estate a 26,000-square-foot office Corp., John Hancock Real Estate, The 60 entries featured alphabetically in these pages (with teams grouped together on the last three) building in the South Loop—also CBRE Global Investors, Cabor represent an impressive cross-section of the Chicago-area commercial real estate sales community, arranging for Baderbrau Brewing Properties, Lincoln Property many of whom have practiced with distinction for decades.