Cru Investment Research January 11Th 2019

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

WINE LIST 2018 Mb.Xlsx

Wines by the Glass sparkling LaLuca | Crisp pear, lemon curd, off dry 10 R. Dumont de Fils, Brut | Dry with lemon zest, toasted bread, green apple, and 15 seafoam. white 12 2016 Cyprus Chardonnay, Russian River Valley | Baked apple, crisp acidity, 100% French Oak 2016 Albert Bichot Saint Veran, Burgandy | hazelnut, vanilla, buttery and complex 14 2017 Château Ducasse, Bordeaux | bright, fresh, crisp fruit 13 2017 Elena Walch Pinot Grigio | green apple, citrus, hint of pear, fresh clean finish 14 rosé 2017 Vie Vite, Provence | subtle citrus and lavender, with an elegant mineral finish. 14 red 2017 Willamette Valley Vineyards Pinot Noir, Willamette | vibrant, juicy, ripe cherry, 14 vanilla, refreshing acidity 2016 Substance Cabernet Sauvignon, Columbia Valley| sleek black fruit, fresh herbs 14 and firm tannins 2015 Berger Zweigelt, Kremstal light, dusty fruit, charming, direct 10 15 2015 Ampeleia Kepos, Tuscany | a perfumey Southern Rhone Blend with floral, berry and mineral notes. 2016 Autour de l'Anne Pot d' Anne, Languedoc | 100% Cinsault Medium-bodied, dry 13 and savoury, with clean fruit and bright acidity 1 Half Bottles sparkling 109 Veuve Cliqeout Champagne, France 100 113 M.V. Krug Champagne, France 150 white 382 2005 Donnhoff Oberhauser Brucke Riesling, Germany 85 383 2005 Donnhoff Schlossbockelheimer Felsenberg Riesling, Germany 70 390 2004 Gunderloch Nackenheimer Rothenberg Riesling Gold Kapsule, Germany 70 393 2013 Schloss Gobelsburg Gruner Veltliner, Austria 50 red 461 2009 Araujo "Eisele Vineyard" Cabernet Sauviugn, Califorina 200 598 2010 Araujo Estate "Altagracia" Bordeux Blend, California 90 2 Sparkling 131 Wolfberger Cremant D' Alsace Brut Rosé, Alsace, France 80 108 N.V. -

Complex Burgundy Hierarchy the Hierarchy of Burgundy, to Some, Is Considered Complex

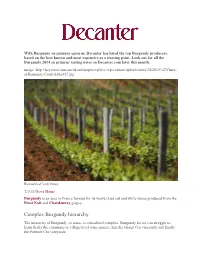

With Burgundy en primeur upon us, Decanter has listed the top Burgundy producers, based on the best known and most expensive as a starting point. Look out for all the Burgundy 2014 en primeur tasting notes on Decanter.com later this month. image: http://keyassets.timeincuk.net/inspirewp/live/wp-content/uploads/sites/34/2015/12/Vines- at-Romanee-Conti-630x417.jpg Romanée-Conti vines TAGS:News Home Burgundy is an area in France famous for its world class red and white wines produced from the Pinot Noir and Chardonnay grapes. Complex Burgundy hierarchy The hierarchy of Burgundy, to some, is considered complex. Burgundy lovers can struggle to learn firstly the commune or village level wine names, then the Grand Cru vineyards and finally the Premier Cru vineyards. A recent piece by journalist John Elmes, who is currently learning about wine for the first time with the WSET, was in high contrast to the in-depth piece by Benjamin Lewin MW on Burgundian classification. It served as a reminder of the breadth of knowledge needed to understand the Burgundy classification system. Burgundy producer types Due to this complexity, finding your favourite Burgundian producers can be much more fruitful in the long term when purchasing wine. This, once again, is not a simple as it sounds. The Burgundian wine trade is split in two between growers and négociants. This has arisen due to a law attributed to Napoleonic times – the laws of equal inheritance. When applied to the vineyards of Burgundy, over time, it has meant that individual growers may only own a small row of vines. -

1 We Proudly Offer a Selection of 1966 Individual Wines, Making Ours One

We proudly offer a selection of 1966 individual wines, making ours one of the largest wine lists in England in terms of producers, regions…diversity Our wish is to showcase up-and-coming styles that we deem quirky and individual, whilst tipping our hat to the most reputable wine regions. We endorse the UK wine industry with the country’s largest selection of sparklings wines from across England and Wales, and we take great pleasure and pride in offering 100 Dessert Wines expecially selected to pair our pudding seasonal offer. The Sommelier Team is on hand to offer guidance and to serve our wines with passion and enthusiasm. We hope that you enjoy perusing our MULTI-AWARDED WINE LIST The Sommelier Team “Wine is Sunlight, held together by Water” Galileo Galilei 1 WHAT YOU WILL FIND IN OUR WINE LIST CHAMPAGNE, SPARKLING AND ROSE’ SELECTED FOR YOU…4 WHITES AND REDS BY THE GLASS SELECTED BUT NOT LIMITED TO…EXPLORE THE WINE LIST… 5 PUDDING WINES WITH….PUDDING AND/OR CHEESE…TIPS…6 THE WINES TO MAKE YOU FEEL AT HOME…THE £30 LIST…7 OPPORTUNITIES ALIAS DEAL OF THE WEEK AND BIN ENDS…8 EXPLORE THE WINE LIST….THE FINEST WINE SELECTION…BY CORAVIN…9 ENGLISH SPARKLINGS…LARGEST COLLECTION…10 TAITTINGER….CHAMPAGNES & CHAMPAGNE IN 1995…12 BAROLO COLLECTION…..CIABOT BERTON…50 FOOD & WINE TIPS…NEXT PAGE 2 ROSES & DRESSED DEVONSHIRE CRAB…15 FANCY RIESLING...16 MUSCADET & OYSTER…18 CHABLIS & HALIBUT…20 ALOXE-CORTON & SCALLOPS…21 THE OUTSIDER…24 VIOGNIER & POUISSIN…25 CHARDONNAY & TWICE BAKED CHEESE SOUFFLE’…27 VERMENTINO & LOBSTER CURRY…28 SOMLO WINES & SOY CURED CHALKSTREAM …32 SAUVIGNON BLANC & TUNA TATAKI…37 CHATEAUNEUF-DU-PAPE & VEAL LOIN…47 NEBBIOLO (NOT JUST BAROLO) & CHATEAUBRIAND…52 TOURIGA NACIONAL & RACK OF LAMB…59 PINOT NOIR & QUANTOCK DUCK BREAST…62 Some of our wines will be flagged as per below VG-Vegan VE-Vegetarian B-Biodynamic O-Organic LS-Low Sulphur NS-No Sulphur MOST OF OUR WINES CONTAIN SULPHITES PRICES ARE IN POUNDS STERLING & INCLUDE VALUE ADDED TAX. -

Wine Menu Champagne by the Bottle Champagne

WINE MENU CHAMPAGNE BY THE BOTTLE CHAMPAGNE NON-VINTAGE VEUVE CLICQUOT YELLOW LABEL NV 795 REIMS R DE RUINART BRUT NV 1350 REIMS LAURENT-PERRIER BRUT NV 995 TOURS-SUR-MARNE BILLECART-SALMON BRUT SOUS BOIS NV 1400 REIMS KRUG GRANDE CUVÉE, BRUT, NV 4500 REIMS ROSÉ TAITTINGER, PRESTIGE ROSÉ BRUT NV 2000 REIMS MOËT & CHANDON ROSÉ IMPÉRIAL NV 1000 ÉPERNAY VINTAGE DOM PÉRIGNON 3750 ÉPERNAY BOLLINGER GRANDE ANNÉE 3000 AŸ CRISTAL, LOUIS ROEDERER 6000 REIMS All prices are in United Arab Emirates Dirham and inclusive of 5% VAT, 10% Service Charge and 7% Municipality Fee. Please note that the menu items and prices are subject to change without prior notice. SPARKLING CLASSIC CUVÉE, BRUT, NV 920 NYETIMBER, SUSSEX, ENGLAND PONGRÁCZ, CAP CLASSIQUE, NV 495 PONGRÁCZ, WESTERN CAPE, SOUTH AFRICA JEIO, PROSECCO VALDOBBIADENE 445 BISOL, VALDOBBIADENE, VENETO, ITALY CAVA, BRUT NV 360 PARÉS BALTÀ, PENEDÈS, SPAIN FERRARI BRUT, NV 845 FERRARI FRATELLI LUNELLI TRENTO, ITALY STE. MICHELLE, BRUT ROSÉ, NV 390 CHATEAU STE. MICHELLE, WASHINGTON, USA All prices are in United Arab Emirates Dirham and inclusive of 5% VAT, 10% Service Charge and 7% Municipality Fee. Please note that the menu items and prices are subject to change without prior notice. WHITE WINE BY THE BOTTLE LIGHT AND FRUITY SYLVANER RÉSERVE 845 DOMAINE WEINBACH, ALSACE, FRANCE PICPOUL DE PINET 280 MOULIN DE GASSAC, LANGUEDOC, FRANCE MELON DE BOURGOGNE, MUSCADET SUR LIE 390 CHÉREAU CARRÉ, PAYS NANTAIS - MUSCADET, LOIRE, FRANCE GAVI DI GAVI 550 ENRICO SERAFINO, PIEDMONT, ITALY FIANO FALANGHINA 550 MASSERIA ALTEMURA, ÀPULO, SALENTO, ITALY INZOLIA 300 SALLIER DE LA TOUR, SICILY, ITALY PINOT NERO BIANCO 465 TORTI, LOMBARDY, ITALY PINOT GRIGIO, MONGRIS 510 MARCO FELLUGA, FRIULI-VENEZIA GIULIA, ITALY GRÜNER VELTLINER, SINGING 390 LAURENZ V, KREMSTAL, AUSTRIA CHENIN BLANC 210 SULA VINEYARDS, NASHIK INDIA SAUVIGNON BLANC 510 KIM CRAWFORD, MARLBOROUGH, NEW ZEALAND DRY FURMINT 350 GRAND TOKAJ, TOKAJ-HEGYALJA, HUNGARY All prices are in United Arab Emirates Dirham and inclusive of 5% VAT, 10% Service Charge and 7% Municipality Fee. -

IG-Quarterly Newsletter Q1 16

| Ontario’s first live wine auction since 2014 occurred the last week of February in Toronto thanks to our friends at Waddington’s. This is great for Ontario buyers, particularly restaurants who have no other buying options for back vintage wine. Hart Davis Hart kicked off what promises to be Other Old World wines from the Rhône Valley, Italy a tremendous auction year with a blockbuster and Spain also continued to command top prices; The total auction had between 100% sold February auction that brought in a while wines from the new world also piqued the $590K and $690K available of total of $6.3 million against presale estimates of interest of bidders. which $359K sold representing $4.1-6.2 million. Hammer prices in this auction a sell through rate (STR) of were the highest since September 2014. Highlights: 77%. While this may be a low • Shortridge Lawton & Co.: 22 lots sold for $43,438 (est. STR by world standards, The two-day auction featured remarkable $23,150-34,850) Waddington’s is making sure treasures from virtually every wine and spirit • Domaine de la Romanée-Conti: 163 lots sold for their consignors aren’t selling region. For example: A library of Madeira from $1,633,744.25 (est. $1,116,550-1,679,500) too low. the iconic cellar of Mr. Lenoir Josey achieved • Henri Jayer: 14 lots sold for $224,540 (est. $147,900- truly remarkable results. There was a flurry of 217,400) As has always been the case in bidding for the 96 lots of rarest Madeira, which • Armand Rousseau: 27 lots sold for $114,302 (est. -

OLIVIER RIVIÈRE Gabaxo Rioja

OLIVIER RIVIÈRE Gabaxo Rioja With just shy of twenty hectares of vineyards that are rented, farmed or owned outright in Rioja Alta, Rioja Baja, Rioja Alavesa and Arlanza, and splitting his time between his own wines and those of Bodegas Lacus, it would be a gross understatement to say that Olivier Rivière is a busy man. Originally lured to Spain in 2004 by Telmo Rodriguez to convert his vineyards to biodynamics, Olivier came to appreciate the rich history of Rioja, and the diversity of its soils and grape varieties. In 2006 he started his own project and owing to the high cost of land in Rioja he traded his farming abilities for access to grapes from the best sites he could find. In 2009 he joined Luis Arnedo at Bodegas Lacus and found a more permanent home for his growing portfolio of wines. ORIGIN Olivier, as you might guess, is not Spanish but French. We was born and Spain raised in Cognac, studied enology (with an emphasis on biodynamic farming practices) in Bordeaux and gained practical experience there and in APPELLATION Burgundy. The list of estates where he has worked is impressive by anyone’s Rioja standards from the most dedicated fans of natural wines (Elian da Ros) to ultra-traditionalists (Domaine Leroy.) When his plans to set up a domaine in Fitou fell through, Olivier decided to spend a few years consulting in SOIL Clay limestone, sand Spain, and he’s never left. Coming from France, Olivier has an innate sense of terroir. Unlike most AGE OF VINES 20–65 of his peers in Rioja, he bases his cuvées not on political boundaries or the length of barrel aging but on terroir. -

SOMMELIER RECOMMENDATION Our Team of Sommeliers Are More Than Happy to Share Their Most Recent Discoveries in the World of Wines

SOMMELIER RECOMMENDATION Our team of sommeliers are more than happy to share their most recent discoveries in the world of wines. COCKTAIL - GRAZIE A CAMILLO NEGRONI ! Barrel-aged Negroni Legend has it that in the year 1919 Count Camillo Negroni was in dire need of a twist to his favourite cocktail. 'The Americano'. His bartender Fosco Scarselli substituted the soda part with Gin and as they say…the rest is history. Fast forward and the year is 2020 and we as Dinner by Heston Blumenthal Sommeliers couldn't resist creating our very own Negroni by carefully aging it in our 5 litres Whisky barrel for a few weeks. See if we succeeded. Dinner NEGRONI £21,00 CHAMPAGNE - FATHER AND SON ! 2007 Thienot 'Cuvée Stanislas' Blanc de Blancs, Brut, Reims, France It takes real nerve to set up your own Champagne House, the very first Houses such as Veuve Clicquot, Bollinger & Moët & Chandon began their existence more than three centuries ago. In 1985 Alain Thienot showed not only courage but more than 20 years of experience as a wine broker. His in-depth knowledge of the vineyards and region with the help of his son Stanislas created this complex yet still refreshing Blanc de Blancs. Try with our Meat Fruit. Bottle (750ml) £ 165,00 WHITE - WHEN YOU HAVE PLAYED THE GAME SINCE 1385 ! 2018 San Giovanni della Sala, Orvieto, Castello della Sala, Umbria, Italy 26 generations of Antinori and yes, that may sound a touch 'old-fashioned' but very few wine families in the world have preserved their heritage so well whilst remaining so innovative at the same time. -

Why We Do the Things We Do at Ninety Acres

WHY WE DO THE THINGS WE DO AT NINETY ACRES We believe in using Biodynamic, Organic and Sustainable ingredients and wines whenever possible. We believe it's not only important to support local agriculture, but that food and wine produced in this way can lend tastes and textures that make the dining experience incredibly unique. Sustainable agriculture refers to the ability of a farm to produce food indefinitely, without causing irreversible damage to ecosystem health. Two key issues are biophysical (the long-term effects of various practices on soil properties and processes essential for crop productivity) and socio-economic (the long-term ability of farmers to obtain inputs and manage resources such as labor). Organic farming is a form of agriculture which avoids or largely excludes the use of synthetic fertilizers and pesticides, plant growth regulators, and livestock feed additives. As far as possible, organic farmers rely on crop rotation, crop residues, animal manures and mechanical cultivation to maintain soil productivity and tilth to supply plant nutrients, and to control weeds, insects and other pests. Biodynamic agriculture, or biodynamics is an organic farming system (but predates the term). It is based on the anthroposophical teachings of Rudolf Steiner, particularly on the eight lectures given by him in 1924 at Schloss Koberwitz in what was then Silesia, Germany nowadays Poland (close to Wrocław). At the time Steiner believed that the introduction of chemical farming was a major problem. Steiner was convinced that the quality of food in his time was degraded, and he believed the source of the problem were artificial fertilizers and pesticides. -

Launceston Place Wine List

Launceston Place Wine List Wines by the glass 3 Half bottles, Sweet and Fortified wines by the glass 4 Champagne & Sparkling Wine 5 White Wines France Bordeaux 6 Burgundy 6 Alsace 7 Loire, Jura 7 Rhone 8 Languedoc, Roussillon 8 England 8 Germany 9 Austria 9 Italy 10 Spain 10 Portugal 10 Australia 11 New Zealand 11 South Africa 11 United States of America 12 Red Wines France 13 Alsace 13 Bordeaux 13, 14 South West 14 Loire Valley 14 Burgundy 15 Rhone 16 Provence 16 Corsica 16 Spain 17 Italy 18 Portugal 19 Austria 19 Greece 19 Hungary 19 Australia 20 New Zealand 20 South Africa 20 Argentina 21 United States of America 21 Chile 22 Rosé Wines 22 Orange Wines 22 Sweet & Fortified Wines 22,23 Cocktails, spirits and beers 24-27 All prices are inclusive of VAT at 20% and are in Great British Pounds. All wines contain sulfites. If you have any question regarding allergies, please speak to our sommelier. Sommelier Selection Champagne 750ml Fleury, Blanc de Noirs, Brut 43 NV Champagne, France 110.00 to add richness to the final blend. Very warm, rich nose with some honeyed, nutty character. The palate is broad and focused with a herby, nutty richness and finish with fresh raspberry flavours. White Wines 750ml Vieilles Vignes, Domaine de la Motte 173 2017 Chablis, Burgundy, France 53.00 has added complexity, richness and depth of flavour. The palate remains on fresh citrusy notes to the finish. This is a textured and full flavoured expression of Chablis. Müller-Thurgau, Pojer e Sandri, Palai 121 2017 Trentino-Alto Aldig, Italy 55.00 Müller-Thurgau is a crossing of Riesling and Madeleine Royale, it was created in 1882 by Dr. -

The Queen of Burgundy - FT.Com

The queen of Burgundy - FT.com ft.com > life&arts > Sign in Site tour Register Subscribe News Quotes Search Food & Drink Advanced search Home World Companies Markets Global Economy Lex Comment Management LifeArts & ArtsFT Magazine Food & Drink House & Home Style Books Pursuits Travel How To Spend It Tools Last updated: April 7, 2012 12:10 am Share Clip Reprints Print Email The queen of Burgundy By Jancis Robinson Lalou Bize-Leroy is famous for her elfin looks, her control freakery and the speed at which she tastes... ny idea what “onenttaion” is? A Apparently the 2010s of Domaine Editor’s Choice Leroy have more of it than the 2009s. LUNCH WITH THE FT HOW TO SPEND IT And Leroy’s Clos Vougeot 2010 in particular is “vy conn ad ar”. These puzzling typos resulted from perhaps the fastest wine tasting I have ever ©James Ferguson undertaken, and the sad part is that Larry David: ‘The real me Home-made: Artisanal ©Colin Hampden-White the 44 wines tasted in under two hours is the problem’ gelato and sorbet Lalou Bize-Leroy were some of the most exciting, and expensive, burgundies ever likely to come my way. It is not easy to get a tasting appointment with Lalou Bize-Leroy, owner of Domaine Leroy (and shareholder in Domaine de la Romanée-Conti, also in the small village of Vosne-Romanée). In fact, her UK importer, Hew Blair of Justerini & Brooks, describes it as “probably the single most difficult thing in Burgundy”. I try every year when I go to taste the latest vintage and all but twice Madame has been absent. -

Bill of Goods Wine by the Glass Provisions

OFFICIAL USE ONLY @cadet_wineandbeer CADET BILL OF GOODS REV. 1 WINE BY THE GLASS 2 PROVISIONS SPARKLING PISTACHIOS 3 Veuve Fourny, Grande Reserve, 1er Cru, Vertus Chardonnay Blend NV 18 Huet, Vouvray Chenin Blanc 2012 14 Stein, Rosé, Rosecco, Mosel Pinot Noir NV 11 OLIVES 4 Castelvetrano WHITE Frog’s Leap, Napa Valley Sauvignon Blanc 2014 9 GRILLED CHEESE 9 Von Oetinger, Jott, Rheingau Müller -Thurgau 2014 11 Central Coast Creamery cow’s milk, pesto, pickles Calder, Galleon Vineyard, Rutherford Chenin Blanc 2015 10 Add prosciutto $3 Héritiers du Comte Lafon, Mâcon-Villages, Mâcon Chardonnay 2015 11 ROSÉ CONSERVA PLATE 12 Minerva Portuguese tinned seafood, toast, caper berries Charles Joguet, Chinon Cabernet Franc 2015 9 Codfish in Olive Oil or Mackerel Fillets with pickles RED Guy Breton, Régnié Gamay 2015 13 SALUMI PLATE 15 Joseph Swan, Saralee’s Vineyard, Sonoma Pinot Noir 2012 16 Selection of Oenotri salumi, toast, olives, mustard Krutzler, Reserve, Sudburgenland, Austria Blaufränkisch 2014 15 Gallica, Shake Ridge Ranch, Amador County Grenache Blend 2011 11 CHEESE PLATE 15 Robert Sinskey, POV, Carneros Bordeaux Blend 2012 16 Selection of artisanal cheeses, toast, olives SHERRY/MADEIRA La Guita, En Rama, Sanlúcar de Barrameda Manzanilla MV 12 CADET COMBO 15/35 Guitiérrez Colosia, Puerto de Santa Maria Amontillado MV 7 Selection of salumi and cheeses, toast, olives Broadbent, 10 year Boal Madeira MV 14 PROSCIUTTO 15/35 DESSERT WINE La Quercia Berkshire Prosciutto, fromage blanc, toast Topaz, Sauvignon Blanc/Semillon, Napa Valley Late -

TABLE of CONTENTS Page

TABLE OF CONTENTS Page # WINES BY THE GLASS Champagne & Sparkling, White, Rose, Red, Tasting Flights, Non-Alcoholic 2-6 & TASTING FLIGHTS HALF BOTTLES (375ml) Bubbly, White Wines & Red Wines of the World 7-8 FULL BOTTLES (750ml) BUBBLY French Champagne & French Grower Champagne 9 Other Sparkling Wines from around the World 10 THE WORLD’S WHITE WINES Italian White Wines 10 Muscadet, Alvarinho, Altesse, Chasselas, Grüner Veltliner, 11 Kener, Müller-Thurgau 11 Riesling - Germany, Alsace & Other Parts of the World 11-12 A Blend of Alsace, Sylvaner, 12 Muscat, Gewürztraminer, Pinot d’Alsace, Pinot Blanc, Pinot Gris 13 The White Wines of Georgia, Chenin Blanc, Sémillon 14 Sauvignon Blanc of the World, The White Wines of Rhône Valley 15 Rhône-Like White Wines, The White Wines of Spain/Portugal 16 The White Wines of Slovenia & Hungary 16 Chardonnay of the World - New World & Burgundy 16-17 Savagnin/Chardonnay Blend 17 Other White Wines, Rosé & Blush Wines of the World, Non Alcoholic Wines 18 THE WORLD’S RED WINES Gamay - The Region of Beaujolais, Pinot Noir - New World 19 Pinot Noir – Burgundy 20 Pinot Meunier, Blaufränkisch 21 Rhône-Like Red Wines – Grenache/Syrah/Petite Sirah (Durif) 21-22 The Red Wines of Rhône Valley – Southern/Northern 22-24 The Red Wines of Provence, Languedoc-Roussillon, Vin De Pays L'Aude 24 Carignan, The Red Wines of Italy 24 Italian Red Varieties of the World, Zinfandel of California 26 The Red Table Wines of Spain/Portugal 26-27 THE GRAPES OF BORDEAUX OF THE WORLD - NEW WORLD & THE REGION OF BORDEAUX: Merlot, Petit Verdot of the World 27 Malbec, Cabernet Franc, Cabernet Sauvignon, Red Blend - Meritage 28-29 The Region of Bordeaux, Other Red Wines of the World 30-31 LARGE BOTTLES Magnums and Bigger Size Bottles 31 DESSERT WINES Natural Dessert Wines, Fortified Dessert Wines - Port, Madeira, etc 32-33 NOTES Grower Champagne, Praise for Uncle Yu’s at the Vineyard 34-35 CORKAGE POLICY $15 per 750ml, 2nd bottle - $25, 3rd - $35, 4th - $45.