Taipei Fubon Commercial Bank

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Instagram Account Redefining Photojournalism November 2015

P earl R iver D elta Follow Us on WeChat Now 城市漫步珠三角 英文版 11 月份 国内统一刊号: CN 11-5234/GO China Intercontinental Press Advertising Hotline 400 820 8428 The Instagram Account Redefining Photojournalism NOVEMBER 2015 《城市漫步》珠江三角洲 英文月刊 主管单位 : 中华人民共和国国务院新闻办公室 General Manager Henry Zeng Supervised by the State Council Information Office of the People's Republic of China Operations Manager Rachel Tong 主办单位 : 五洲传播出版社 Accountant Annie Qi 地址 : 北京西城月坛北街 26 号恒华国际商务中心南楼 11 层文化交流中心 Production Supervisor Jack Lin Senior Designer Tawaka Jiang, Designer Claire Zheng 11th Floor South Building, HengHua linternational Business Center, 26 Yuetan North Street, Xicheng District, Beijing Sales Managers Celia Yu, Justin Lu http:>www.cicc.org.cn Account Manager Christy Cai 社长 President of China Intercontinental Press: 李红杰 Li Hongjie Account Executives Christina Zhuang, Cynthia Peng, Wesley Zhang, Nicole Tang 期刊部负责人 Supervisor of Magazine Department: 邓锦辉 Deng Jinhui Sales Assistant Sunnie Lü 编辑 : 刘扬 发行 / 市场 : 黄静 李若琳 广告 : 林煜宸 Business Development Manager Morri Qin Event Manager Valentina Latorraca Editor in Chief Tom Lee Senior Marketing Executive Rainbow Wu Guangzhou Editor Jocelyn Richards Marketing Executives Alice Wang, Nikki Li, Sally Xu Shenzhen Editor Christine Gilbert Distribution Luo Zhi, He Wei Wen National Lifestyle Editor Marianna Cerini National Arts Editor Andrew Chin CEO Leo Zhou Web Editor Matthew Bossons National Editorial Director Ned Kelly Editorial Assistants Ziyi Yuan, Tristin Zhang Digital Products Manager Vickie Guo Contributors Peter Fenton, Lena -

8Th Metro World Summit 201317-18 April

30th Nov.Register to save before 8th Metro World $800 17-18 April Summit 2013 Shanghai, China Learning What Are The Series Speaker Operators Thinking About? Faculty Asia’s Premier Urban Rail Transit Conference, 8 Years Proven Track He Huawu Chief Engineer Record: A Comprehensive Understanding of the Planning, Ministry of Railways, PRC Operation and Construction of the Major Metro Projects. Li Guoyong Deputy Director-general of Conference Highlights: Department of Basic Industries National Development and + + + Reform Commission, PRC 15 30 50 Yu Guangyao Metro operators Industry speakers Networking hours President Shanghai Shentong Metro Corporation Ltd + ++ Zhang Shuren General Manager 80 100 One-on-One 300 Beijing Subway Corporation Metro projects meetings CXOs Zhang Xingyan Chairman Tianjin Metro Group Co., Ltd Tan Jibin Chairman Dalian Metro Pak Nin David Yam Head of International Business MTR C. C CHANG President Taoyuan Metro Corp. Sunder Jethwani Chief Executive Property Development Department, Delhi Metro Rail Corporation Ltd. Rachmadi Chief Engineering and Project Officer PT Mass Rapid Transit Jakarta Khoo Hean Siang Executive Vice President SMRT Train N. Sivasailam Managing Director Bangalore Metro Rail Corporation Ltd. Endorser Register Today! Contact us Via E: [email protected] T: +86 21 6840 7631 W: http://www.cdmc.org.cn/mws F: +86 21 6840 7633 8th Metro World Summit 2013 17-18 April | Shanghai, China China Urban Rail Plan 2012 Dear Colleagues, During the "12th Five-Year Plan" period (2011-2015), China's national railway operation of total mileage will increase from the current 91,000 km to 120,000 km. Among them, the domestic urban rail construction showing unprecedented hot situation, a new round of metro construction will gradually develop throughout the country. -

Public Transport Policy

Centre for Science and Environment International Conclave Towards Clean and Low Carbon Mobility Session II: Affordability vs Financial Sustainability in Public Transport Policies on Public Transport Development and Financial Schemes in Taipei S.K. Jason Chang Professor, National Taiwan University Advisor, Taipei City Government [email protected] New Delhi, Sept 4, 2018 Agenda • Background Information • Integrated Transport Policy • Taipei Metro and Bus Systems • Full Trip Cost and Implications • National Policy and Programs • Concluding Remarks Taiwan and Taipei Metropolitan • Taiwan: 36,000 sq km, Pop 23.2 mi Car- 7.1 mi, Motorcycle- 13.8 mi • Taipei Metropolitan: 3,000 sq km, Pop 7.0 mi, Car- 2.5 m, Motorcycle- 3.2 mi MRT 136 km + BRT 60 km Public Bike: 36,800 bikes w/ 820 stns • PPP Transport Projects: (1) HSR- 15 Bi; (2) Kaohsiung Metro- 6 Bi; (3) ETC System- 300 mi; (4) City Bus Station- 200 mi; (5) Public Bike- 40 mi; (6) Smart Card System- 30 mi • Freeway Network: 1,000 Km MLFF ETC w/ distance-based charge • High Speed Rail: the journey b/w Taipei and Kaohsiung (345km) 90 minutes. Our Cities and Challenges • High Motorization • Diversity of Land Use • High Density of Population • Mixed Traffic Flow Characteristics • High Fatality in Traffic Accidents • Enforcement vs. Efficiency • Reforms being proposed: Low Carbon City, Green Mobility, Public Transport, Public Bike, Walk…… Integrated Urban Transport Policy • Sustainable Development (Environmental, Social, Economic/Financial and Governance) • Integration of Land Use/Development -

Taoyuan Metro TAIWAN – Taoyuan Metro ( Airport MRT) Case Introduction

Success Story Case Study www.ctcu.com Reliable CCTV Surveillance Network in Taoyuan Metro TAIWAN – Taoyuan Metro ( Airport MRT) Case Introduction Photo Source: Taoyuan Metro Corporation Taoyuan Metro, opened to the public on 2017, offers a rapid and reliable transportation for local commuters and travelers to travel between Taipei city, New Taipei, Taoyuan Airport and Taoyuan city. With providing pleasant on-board experiences to passengers in mind, Taoyuan metro has continu- ously searched for advanced technologies to provide connected services on board such as passen- ger information system, IP surveillance system, internet connections, broadcasting system and so on. However, to implement communication devices on metro trains, Taoyuan Metro faced several challenges: About CTC Union Requirements & Challenges • Harsh Condition. On-board communication devices must function properly in harsh and extreme CTC Union Technologies Co. Ltd., founded in 1993, proactively designs and manufac- conditions such as environment temperature from -40~75°C. tures telecommunications, data communi- • Difficult Environment. When metro trains are operating, communication devices should perform cations and industrial networking products perfectly under high shock and vibration environment. for a global market. With technologies • Lack of power supply support. Communication devices should provide flexibilities for connecting based on Ethernet and Optical transmis- to powered devices for extended networking services such as wireless access points, surveillance sion, CTC Union can effectively meet the requirements of voice and data carriers, cameras, and telephony services. enterprises, as well as industrial grade • Build a future-proof network. Communication devices should integrate or migrate to all IP Ethernet users. infrastructures easily and flexibly so as to provide modernized and efficient services in this Using the latest technologies, CTC Union fast-paced digital world. -

The Leading Event for Asia Pacific's Rail Industry

The leading event for Asia Pacific’s rail industry DATES VENUE 22–23 Hong Kong Convention & March 2016 Exhibition Centre www.terrapinn.com/aprail OVER 6,500KM OF RAIL PROJECTS Our story ARE CURRENTLY PLANNED AND ANNOUNCED IN ASIA. BILLIONS ARE BEING INVESTED INTO THE REGION, CREATING MASSIVE OPPORTUNITIES FOR THE Despite being the backbone of every transportation system, the rail industry has often been thought of as conservative and change-resistant. But not RAIL INDUSTRY. anymore. As we move into the age of the digital railway, passengers are not just commuters, but true consumers who expect a comfortable and “connected” experience. At the same time, railway operators are facing increasingly complex asset management issues, difficult high-speed construction challenges and tough operational efficiency targets. We bring together the entire rail industry in Asia to tackle these challenges and pave the way for the future of transport in the region. Welcome to Asia Pacific Rail. The most exclusive and influential railway gathering in the region, Asia Pacific Rail attracts over 1,000 attendees from Asia and across the globe each year. In 2016, Asia Pacific Rail will have more content than ever before, with 4 premium conference tracks. These tracks will feature exciting innovations in metro, high-speed rail, mainline passenger and freight, all focused on the theme enhancing operational excellence and passenger experience to improve your bottom line. Visionary keynotes will lay the foundations for two days of intensive learning, discussion and networking. Leading C-Level executives will share case studies from across the world, ensuring you can learn from the best of the best. -

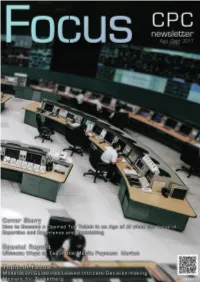

The Operation Control Centre of Taipei Metro Beats AI with Compassion and Flexibility

封面 Focus CPC NEWSLETTER Index 2 Perspective Productivity Again and the Strategies Cover Story 5 Part1 | Introduction How to Become a Desired Top Talent in an Age of AI When the Value of Expertise and Experience are Diminishing 9 Part2 | Case Study Taipei Metro System The Operation Control Centre of Taipei Metro Beats AI with Compassion and Flexibility Special Report 14 Part1 | Introduction Current Fervor for Beep to Pay Ultimate ways to tap in the mobile payment market 17 Part2 | Case Study Taishin Bank 3 Pay + 1 Pay - Diligent Players Raking in the Chips from the Mobile Economy 20 Topic of Focus Facebook under the Heat Moderation Guidelines Leaked Intricate Decision-making Moment for Zuckerberg Focus 2017 vol. 4 2017/8/29 Distributor: China Productivity Center Publisher: Pao Cheng Chang Editor-in-Chief: Eugene Y. Lin Administration Chief Editor: Li Chiu Huang, Yen Feng Kuo Managing Editor: Ann Lee, Yu Tzu Chen, Li Ting Pan Illustrator: Jie Yin Lin Designer: Ze Wei Pan Website: https://goo.gl/bvNgu7 All right reserved. No part of this publication may be reproduced in any form without permission from its publisher. 1 Perspective Focus Productivity Again and the Strategies industries. China has initiated a mega business environment re-engineering plan. The ASEAN markets seem to be booming with opportunities but with risks looming on the horizon. Looking back the course of development over the past decades, the disruptive innovations such as the IoT, cloud computing, artificial intelligence and machine learning have dramatically changed the existing market and value network around the globe, becoming the force behind the growth of modern businesses. -

The Analysis of Critical Success Factors for In-Town Check-In in Taiwan

sustainability Article The Analysis of Critical Success Factors for In-Town Check-In in Taiwan Cheng-Hua Yang 1 , Huei-Ju Chen 2,* , Li-Chu Lin 3 and Alastair M. Morrison 4 1 Department of Airline and Transport Service Management, National Kaohsiung University of Hospitality and Tourism, Kaohsiung City 812, Taiwan; [email protected] 2 Department of Leisure and Recreation Management, National Kaohsiung University of Hospitality and Tourism, Kaohsiung City 812, Taiwan 3 Department of Tourism and Hospitality, Private Chung-Hsin High School, Hsinchun County 304, Taiwan; [email protected] 4 Department of Marketing, Events and Tourism, Business School, University of Greenwich in London, London SE10 9LS, UK; [email protected] * Correspondence: [email protected]; Tel.: +886-7806-0505 (ext. 31405) Abstract: The Taoyuan International Airport in Taiwan encountered service capacity bottlenecks for insufficient facilities before COV-19 break. In order to increase the service capacity efficiency on check-in, security checks, and customs clearance, the Ministry of Transportation and Communications R.O.C. (MOTC), Taiwan, rerouted the airport traffic flow by implementing the in-town check-in (ITCI) concept to decrease crowding in the airport waiting hall. This research examined the structure of critical success factors (CSFs) for ITCIs, deriving three hierarchies of three dimensions, eight criteria, and 18 evaluation indexes from the previous literature, expert interviews, and analysis results from Analytic Network Process (ANP) via Super Decisions software. The three CSF dimensions were: first- level hierarchy “advantageous environments,” followed by “marketing” and “service value,” which is a second-level hierarchy. The study concluded that the third level item of “transferred vehicles system and management” can play an important key role in ITCTs and “users’ usage preference” has a high correlation to ITCT management strategy. -

Taoyuan Airport to Farglory Hotel Hualien

Taoyuan Airport to Farglory Hotel Hualien Route 1 City Bus→Airplane→City Bus or Taxi After arriving at Taoyuan Airport, please take Kuo-Kuang Motor Transport1840 to Taipei Songshan Airport. (Directorate General of Highways, MOTC, no. 1840) After arriving at Taipei Songshan Airport, please take the domestic flight to Hualien Airport. (Taipei Songshan Airport) ◆ The flight on Monday to Saturday will take off at 7:10 A.M. Estimated Arrival Time: 8:00 A.M. (UNI Air B78971) ◆ Only one flight takeoff at 8:50 A.M. on Sunday. Estimated Arrival Time: 9:40 A.M. (UNI Air B78975) ◆ The flight on Monday to Sunday will take off at 6:50 P.M. Estimated Arrival Time: 7:40 A.M. (UNI Air B78977) After arriving at Hualien Airport, please take Hualien bus 1123 to Hualien train station (Directorate General of Highways, MOTC, 1123) At Hualien train station, please take Hualien bus 1127, 1140 or 1145 to Farglory Ocean Park. (Directorate General of Highways, MOTC, 1127, 1140, 1145) After arriving at Farglory Ocean Park, there will be some shuttle buses to Farglory Hotel Hualien for free. ◆ Farglory Ocean Park→ Farglory Hotel Hualien 11:15 12:15 13:15 14:15 15:15 15:45 16:15 16:45 17:15(Last bus) ◆ Farglory Hotel Hualien→ Farglory Ocean Park 09:00 09:30 10:00 10:30 11:00 12:00 13:00 14:00 15:00(Last bus) As an alternative, At Hualien train station, please take a taxi to Farglory Hotel Hualien. ◆ The typical taxi fare: About NTD 500 Route 2 Taoyuan Airport MRT→metro Taipei Bannan Line→metro Taipei Wenhu line→Airplane→City Bus or Taxi After arriving at Taoyuan Airport, please take Taoyuan Airport MRT to Taipei Main station. -

Taoyuan Citizen Card: 6 Major Services, 31 Uses

Taoyuan Citizen Card: 6 Major Services, 31 Uses Public The card serves as tickets for: Transportation 1. City bus Tickets 2. Taxi rides for seniors & the disabled 3. Bike sharing system like Ubike 4. Taiwan Railway 5. Metro (Taoyuan Metro, Taipei Metro and Kaohsiung Metro) 6. National highway bus Special offers: City Bus “Buy 1 Get 1 Free”: first ride charged according to fare rules (NT$18 within 8 km, NT$2.58 per extra km); second ride comes with basic fare waiver (NT$18), maximum fare charged: NT$60) Taoyuan Metro Discounts: 20% off for General Card holders, 60% off for Senior Citizen Card and Disability Card holders and elementary students. Discount Bus Fare for Students: 50% off for elementary students, 25% off for students of junior/ senior high schools and colleges. Free Points for Senior Citizen Card and Disability Card holders: (1) 800 points offered for free each month for Senior Citizen Card and Disability Card holders (1000 points for those in Fuxing District); points will expire at the end of the month and do not accumulate across months. (2) Terms of Use: city bus, Taoyuan Metro, taxis for seniors & the disabled (less than NT$100: 36- point subsidy; NT$101 and above: 72-point subsidy), ticket to Taoyuan City Swimming Pool, fees for all facilities at Civil Sports Center (swimming pool, fitness center) and venue booking (badminton, table tennis, basketball courts, etc.). Public Services 7. Borrowing books from libraries 8. Paying government fees 1 9. Receiving push notifications from the App (events, government benefits, vaccination events, etc. -

Taipei Rapid Transit Corporation 2018 Annual Report

TAIPEI RAPID TRANSIT CORPORATION 2018 ANNUAL REPORT 2O18 TAIPEI RAPID TRANSIT CORPORATION ANNUAL REPORT Contents 006 Vision, Mission and Core Values 060 Business Diversification Affiliated Businesses : Commercial Areas in Metro Stations / Multimedia Advertisements / Beitou Resort 010 Data and Figures Contracted Businesses : Maokong Gondola / Taipei Arena /Taipei Children's Amusement Park TRTC’s Invested Companies : EasyCard Investment Holding Co., Ltd. / 014 Message From Top Management Metro Consulting Service Ltd. 020 Organization and Structure 082 Livable City Capital and Ownership Structure / Urban Aesthetics / Organizational Structure / Business Team / Cross-Industry Art and Cultural Activities / Financial Status Community Care and Local Marketing / Environmental Sustainability and Energy Conservation 030 Core Transit Business 102 Looking to the Future Operational Stability of the System / Ridership and Headways / Upgrading Transportation Capacity / Technology Sharing and Knowledge Export / Human Resources Empowerment 106 Milestones 048 Passenger Experience 112 Appendix Friendly and Convenient Riding Experience / Financial Statements and Report of Independent Accountants / Diverse Ticketing Options and Discounts Key Data 01 02 2O18 TAIPEI RAPID TRANSIT CORPORATION ANNUAL REPORT An urban project that opened 25 years ago has become an integral part of the cultural fabric of today’s Taipei. During the past 25 years, Taipei Metro has impacted people’s lives through technology and shaped urban appearances. Everywhere it has expanded seems -

12Th Railworld Summit 2014

Save up to 600 USD Early Bird for 12th RailWorld Summit 2014 Gain the comprehensive overview of the Asia Pacific Railway Industry Most Awaited Event to discuss Rail Investment, Technology, Current and Future Project October, 23-24︱Bangkok, Thailand SPEAKERS OF 2014 ChulaSUKMANOP YongsitROJSRIKUL SermantoDWIATMOKO Chamroon TonnyYEAP TommyJEN DirectorGeneral Governor DirectorateGeneralof TANGPAISALKIT HeadofSpecialProjects AssistantDirector, OfficeofTransportand MassRapidTransit Railway Chairman andTechnology DeputyHeadof TrafficPolicyand AuthorityofThailand Ministryof S.R.T.Electrified,Co.Ltd LandPublicTransport OperationControl Planning (MRTA) Transportation,Indonesia Commission(SPAD), Center MinistryofTransport, Malaysia TaiwanHighSpeed Thailand RailwayCorporation (THSRC),Taiwan Produced By Supported By Exhibition Sponsor StateRailway MassRapidTransitAuthority BangkokMass ofThailand ofThailand TransitPublicCo.Ltd +86 21 6840 7631 +86 21 6840 7633 Please scan and join our WeChat here. [email protected] www.cdmc.org.cn/2014/rwsa DAY 1, THURSDAY, OCT 23, 2014 0800 Registration & Coffee 0850 Welcome & Chairperson’s Opening Remark Session 1: Updates on the Rail Development in the Region 0900 Status of Rail Development under Transport Investment Plan in Thailand Brief introduction on the country's rail industry A modal shift in transport for greater competitiveness Investment scenario on railway specially high-speed railway and country linking lines Chula SUKMANOP, Director - General, Office of Transport and Traffic Policy and Planning, Ministry -

Resources for Flight Departments COVID-19 Outbreak April 10, 2020

Content Developed by our Partner: Max Security Solutions a world leader in threat intelligence Resources for Flight Departments COVID-19 Outbreak April 10, 2020 Current Situation The death toll from the COVID-19 pandemic that originated in Wuhan, China was reported to be 97,000 as of April 10, while the total number of confirmed cases has reached 1,617,000 worldwide. As of April 10, the first case of COVID-19 was reported in Yemen, while Djibouti reported its first virus-related death. Argentina extended its nationwide quarantine until April 23, while Honduras extended its nationwide curfew until April 19. Panama announced that a full quarantine will be enforced nationwide on April 11-12. In Guatemala, the government ordered all people to wear masks in public starting April 13. In Cambodia, all forms of travel between districts and provinces are restricted until April 16 with limited exceptions. East Timor has closed its borders and banned any entry and exit, regardless of citizenship, to take effect on April 13. Authorities imposed a partial lockdown in Jakarta, Indonesia, with security forces deployed to enforce social distancing. Brussels Airline suspended flights to eight destinations in Europe and North Africa for one year, while Air France-KLM grounded more than 90 percent of flights over the next two months. Denmark authorities issued an advisory to its citizens to avoid traveling outside of the country until May 10. Hungary announced that the national lockdown would be extended indefinitely, and Ireland extended its lockdown by two weeks. The Kurdistan Regional Government extended the curfew in its territory until April 16.