19.20 PENSIONS ANNUAL REPORT Final Version

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Staffordshire County Council Expenditure Over £500 October 2015

Staffordshire County Council Expenditure over £500 October 2015 OrganisationalUnit BeneficiaryName PaymentDate Amount Purpose Schools 3663 27/10/2015 574.09 Supplies and Services Schools 1 STOP JETTING LTD 13/10/2015 895.00 Premises Schools 123Comms Limited 07/10/2015 779.00Supplies and Services Schools 1ST CLASS FOOTBALL COACHING 07/10/2015 765.00 Employees Schools 1st Technologies Ltd T/A ICT D 26/10/2015 2685.00 Supplies and Services Schools 21ST CENTURY LEGACY 20/10/2015 648.00 Supplies and Services Other Education and Children's services 24HR WEST SIDE TAXIS 15/10/2015 29140.44Transport Schools 2SIMPLE SOFTWARE 02/10/2015 500.00 Supplies and Services Schools 2SIMPLE SOFTWARE 06/10/2015 1650.00 Supplies and Services Schools 2SIMPLE SOFTWARE 08/10/2015 1200.00 Supplies and Services Schools 2SIMPLE SOFTWARE 16/10/2015 750.00 Supplies and Services Schools 2SIMPLE SOFTWARE 22/10/2015 450.00 Supplies and Services Adult Social Care 3L CARE LTD 14/10/2015 10937.34 Supplies and Services Schools 4Imprint Direct Ltd 06/10/2015 1925.95Supplies and Services Schools 4Imprint Direct Ltd 21/10/2015 3104.00Supplies and Services Law & Governence 4th Codsall Guides 13/10/2015 500.00Third Party Other Education and Children's services 57 TAXIS 21/10/2015 10679.00 Transport Schools 6061 CARS 15/10/2015 2184.50 Transport Other Education and Children's services 6061 CARS 20/10/2015 11305.63 Transport Law & Governence 74TH SILVERDALE SCOUT GROUP 14/10/2015 1000.00 Third Party Other Education and Children's services A & K TRAVEL 21/10/2015 9123.18 Transport -

West Midlands Schools

List of West Midlands Schools This document outlines the academic and social criteria you need to meet depending on your current secondary school in order to be eligible to apply. For APP City/Employer Insights: If your school has ‘FSM’ in the Social Criteria column, then you must have been eligible for Free School Meals at any point during your secondary schooling. If your school has ‘FSM or FG’ in the Social Criteria column, then you must have been eligible for Free School Meals at any point during your secondary schooling or be among the first generation in your family to attend university. For APP Reach: Applicants need to have achieved at least 5 9-5 (A*-C) GCSES and be eligible for free school meals OR first generation to university (regardless of school attended) Exceptions for the academic and social criteria can be made on a case-by-case basis for children in care or those with extenuating circumstances. Please refer to socialmobility.org.uk/criteria-programmes for more details. If your school is not on the list below, or you believe it has been wrongly categorised, or you have any other questions please contact the Social Mobility Foundation via telephone on 0207 183 1189 between 9am – 5:30pm Monday to Friday. School or College Name Local Authority Academic Criteria Social Criteria Abbot Beyne School Staffordshire 5 7s or As at GCSE FSM or FG Alcester Academy Warwickshire 5 7s or As at GCSE FSM Alcester Grammar School Warwickshire 5 7s or As at GCSE FSM Aldersley High School Wolverhampton 5 7s or As at GCSE FSM or FG Aldridge -

Skills and Employability Support and Information During Covid-19

Skills and Employability Support and information during Covid-19 Call 0333 300 0050 Email [email protected] or visit www.entrust-ed.co.uk to find out more. Inspiring Futures Skills & Employability Support & information during Covid-19 Entrust Skills and Employability are still working during the school closure period and will be available throughout (including the school holiday period and beyond). How we can help Though we are not available for face to face information, advice and guidance we are available via phone, email and Microsoft Teams offering: • Phone information advice and guidance • Support with applications and transition to learning • Signposting to other services as required Contact to request support can be made by schools, colleges, training providers as well as by young people or parents. Contact Details Contact details for our school careers advisers, and district-based staff can be found here Inspiring Futures Skills & Employability Support & information during Covid-19 We have contacted all learning providers in Staffordshire and put together a summary of how the main types of learning provider are responding to the current crisis in relation to applications and recruitment. Sixth Forms • Sixth forms across county remain closed to students and face to face enquiries • Sixth Forms will be keen to ensure a place is secure for those who are holding an earlier conditional offer • Applications and enquiries to Sixth Forms are welcomed and potential students should continue to apply as directed prior to the close -

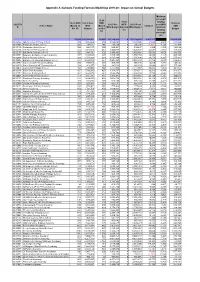

Appendix a Schools Funding Formula Modelling 2019-20

Appendix A -Schools Funding Formula Modelling 2019-20 - Impact on School Budgets Minimum per pupil 19-20 19-20 funding: 18-19 NOR 18-19 Post NOR Notional LAESTA 19-20 Pre MFG 19-20 Post post MFG School Name (Based on MFG (Based Variance SEN B MFG Budget Adjustm MFG Budget minimum Oct 17) Budget on Oct Budget ent funding 17) per pupil rate 35,098 160,922,501 35,098 163,129,918 0 163,129,918 2,207,417 25,262,269 8612033 Abbey Hulton Primary School 209 1,006,434 209 1,028,095 0 1,028,095 21,660 4,919 210,426 8612082 Alexandra Infants' School 166 790,527 166 786,530 0 786,530 (3,997) 4,738 111,840 8612119Alexandra Junior School 200 946,127 200 949,947 0 949,947 3,820 4,750 195,628 8612114 Ash Green Primary School 413 1,401,919 413 1,445,500 0 1,445,500 43,581 3,500 107,255 8612100 Ball Green Primary School 322 1,449,781 322 1,489,465 0 1,489,465 39,685 4,626 305,092 8612001 Belgrave St Bartholomew's Academy 427 1,738,576 427 1,755,158 0 1,755,158 16,582 4,110 265,195 8612064 Blurton Primary School 369 1,554,929 369 1,585,488 0 1,585,488 30,559 4,297 277,061 8612425 Burnwood Community Primary School 537 2,386,266 537 2,427,340 0 2,427,340 41,074 4,520 524,457 8612040 Carmountside Primary Academy 202 948,502 202 965,040 0 965,040 16,538 4,777 198,823 8613020 Christ Church CofE Primary School 204 921,975 204 942,624 0 942,624 20,649 4,621 157,194 8612075 Clarice Cliff Primary School 408 1,748,908 408 1,777,923 0 1,777,923 29,015 4,358 307,257 8612106 Eaton Park Academy 427 1,728,205 427 1,754,517 0 1,754,517 26,312 4,109 318,357 8612002 Etruscan -

Staffordshire Community Safety Partnership

One Staffordshire Information Sharing Protocol Document control: Version 9.0 August 2020 Contents Executive summary ................................................................................................... 1 1. Purpose ................................................................................................................. 2 2. Powers .................................................................................................................. 3 3. Partners ................................................................................................................ 4 4. Process for Sharing ............................................................................................... 5 5. Review ................................................................................................................ 10 Appendix A Signatories and Designated Officers Appendix B Legislation Summary Appendix C Conditions of Consent Appendix D Information Sharing Agreement Appendix E Information Sharing Health and Social Care Data Appendix F Fair Processing Appendix G Individual Information Sharing Agreements Appendix H Information Sharing Templates Executive summary The ‘One Staffordshire Information Sharing Protocol’ deals with the emerging issues surrounding information sharing between agencies and organisations that are delivering services for the social, economic and environmental wellbeing of the community. Promoting and achieving wellbeing is only likely to be successful where organisations work together to ensure that -

People Achieveto

® inspiring young people achieveto Annual Review 2014-2015 Including the Annual Report and Financial Statements THE DUKE OF EDINBURGH’S AWARD Contents Overview .................................................................... 3 Thank you to all our supporters .................................. 4 Our Licensed Organisation partners ............................ 6 Chairman’s Report .................................................... 10 Our strategic objectives ............................................ 12 Supporting DofE delivery .......................................... 13 Extending the reach .................................................. 13 Driving achievement ................................................. 13 Fuelling growth ......................................................... 15 Financial performance .............................................. 16 Funding the DofE ...................................................... 18 Trustees’ commitment .............................................. 19 Thank you ................................................................ 19 Independent Auditors’ Report ................................... 20 Statutory accounts ................................................... 22 Appendices .............................................................. 42 Trustees .................................................................... 49 The Trustees present their report and the financial statements of the Royal Charter Corporation for the year ended 31 March 2015. In preparing this report the -

City of Stoke-On-Trent Standing Advisory Council On

City of Stoke-on-Trent Standing Advisory Council on Religious Education Twenty First Annual Report – 2018 1 | P a g e Message from the Chair of SACRE, Councillor Abi Brown This is the twenty first annual report of the Stoke-on-Trent Standing Advisory Council on Religious Education, and it covers the period of the academic year 2017 - 2018. I am extremely pleased to say that in my second year of chairing SACRE, we have again achieved a great deal. Religious Education continues to be an essential part of education in Stoke-on-Trent, providing a host of opportunities for our children and young people to enhance their understanding of diversity, values, beliefs and ways of living around the world. It has been great to hear from so many SACRE Members this year about the positive work they have been involved in. SACRE have heard directly from those working in schools about the way Religious Education is explored, the activities pupils engage in and the enthusiasm for the subject. Schools continue to praise the Agreed Syllabus, noting how it has improved the way Religious Education is taught to our children and young people. SACRE have worked hard to create an online, interactive map, detailing the places of worship in the city. This was following a direct request from schools, which SACRE quickly responded to, with an online tool detailing the locations, contact details and practical information about the venues. Following on from previous years and positive feedback, we were also very pleased to be able to run two successful RE Pupil Days, along with a teacher training session network meetings. -

Statement of Accounts 2017/2018

Statement of Accounts for 2017/2018 This report is available in other formats such as in large print and Braille, or you can get it in other languages. If you need a copy of this report in another format or language, phone us on 01785 276065. Staffordshire County Council Contents Page Introduction 1-2 Narrative Statement by the Director of Finance and Resources 3-10 Audit Opinion 11 Statement of Responsibilities for the Statement of Accounts 18 Chairman’s Certificate 19 Statement of Accounting Policies 20-27 Comprehensive Income and Expenditure Statement 28 Movement in Reserves Statement 29 Balance Sheet 30 Cash Flow Statement 31 Notes to the Accounts 32-98 Staffordshire Pension Fund Financial Statements 1st April 2017 to 31st March 2018 99-136 Glossary 137-142 Staffordshire County Council Introduction This Statement of Accounts gives you an overall impression of our finances. Accounting rules and practices are complex and difficult to understand, and there are some technical words and terms that we have to use. We have tried to make this statement as clear and understandable as possible in the circumstances. To help you, at the back of this document, we have provided a glossary to explain some of the financial and accounting terms we have had to use. The Statement of Accounts for 2017/2018 was available for inspection from 18 June to 13 July 2018. The formal audit of our accounts began on 18 June 2018 and we received an unqualified opinion on the accounts on 31 July 2018. This means that, in the auditors’ opinion, our accounts presented a true and fair view of our financial position. -

Spf Final Pensions Annual Report 2019

Staffordshire Pension Fund Annual Report and Accounts 2018/19 www.staffspf.org.uk Annual Report and Accounts Staffordshire Pension Fund 2018/2019 Pension Staffordshire 1 Staffordshire Pension Fund Annual Report and Accounts 2018/19 www.staffspf.org.uk Contents Chairman’s Report 3 Fund Governance Governance 5 Pensions Committee 5 Pensions Panel 7 Local Pensions Board 8 Risk management 11 Scheme management and Advisors 13 Fund Administration Overview 15 Membership 17 Performance 19 Communication 27 Investment Report Global Economic Review 29 Major Asset Class Returns 30 Pension Fund Investment Returns 34 Responsible Investment report 36 LGPS Central LGPS Central Pool Reporting 2018/2019 39 Financial Statements 2018/2019 Pension Fund account 45 Net Assets Statement 46 Actuarial Statement 47 Pension Fund Accounts Reporting Requirement 49 Notes to the Accounts 52 Supporting Information Glossary of terms 87 How to Contact Us 88 Appendices List of participating Employers 90 2 Staffordshire Pension Fund Annual Report and Accounts 2018/19 www.staffspf.org.uk Welcome It gives us great pleasure to present the Annual Report and Accounts for the financial year ended 31 March 2019 for the Staffordshire Pension Fund. The Staffordshire Pension Fund has already made an initial transfer of administers the Fund on behalf of over Partner Fund assets and is 400 different Employers and once again aiming to deliver savings in excess of we are most grateful to the Pensions £250m over the next 16 years. team for the efficient service they have The Local Pensions Board, established Philip Atkins, provided to all of our Employers and their in accordance with the Public Service OBE continued professionalism in maintaining Pensions Act 2013 and Regulation 106 Chairman the highest standards of service to our (Pensions Panel) of the Local Government Pension Scheme, scheme members. -

System Leadership Development Directory

System Leadership Development Directory Teaching School: St. Joseph’s College Designation Specialism Name of SLE/LLE/NLE/NLG School Director of Teaching School: Simon Jones SLE, LLE, NLE, NLG Contact details: SLE Art (SASCAL subject lead) Ailee Millward Ormiston Horizon Academy SLE Behaviour and Discipline Sian Hughes Haywood Academy Angela Davies SLE Behaviour and Discipline/attendance Cath Machin St. Joseph’s College [email protected] SLE Computing (SASCAL subject lead) Rob Hampton Sandon Meridan Academy 01782 418211 SLE Computing (SASCAL subject lead) Martin Palmer Trentham Academy SLE CPD Kirstie Hicks Thistley Hough Academy SLE CPD Dominic McKenna St. Joseph’s College SLE CPD Clare Willis St. John Fisher SLE Curriculum John Bryden St. Joseph’s College SLE Drama/CPD Delia Byrne St. Joseph’s College SLE Drama (SASCAL subject lead) Sarah Price St. Joseph’s College SLE DT Suzanne Elson Ormiston Horizon Academy SLE DT (SASCAL subject lead) Steve Fergusson Haywood Academy SLE DT Simon Goodall St. Joseph’s College SLE English/CPD Sam Chater St. Joseph’s College SLE English (SASCAL subject lead) Emma Pass Excel Academy SLE English/CPD Matthew Taylor Biddulph High School SLE Geography (SASCAL subject lead) Amy Brockley St Margaret Ward Catholic Academy SLE Geography Cheryl Caine St Peter’s Academy SLE Geography/CPD/ITT Ed Leighton St. Joseph’s College SLE History (SASCAL subject lead) Lee Davies Sandon Meridian Academy SLE ITT/NQT/CPD Simon Jones St. Joseph’s College SLE ITT/NQT/CPD Sarah Williams Birches Head Academy SLE ITT/RE (SASCAL subject lead) Liz Gibson Excel Academy SLE Maths Rhiannon Bedford Excel Academy-Stoke MEP SLE Maths Craig Bloor The Discovery Academy SLE Maths Val Broomhall Stoke MEP SLE Maths (SASCAL subject lead) Simon Bullock Stoke MEP SLE Maths Samantha Coppenhall St Margaret Ward Catholic Academy SLE Maths Natalie Godwin The Co-operative Academy -Stoke MEP SLE Maths Rebecca Kirkman Trentham High-Stoke MEP SLE MFL/CPD (SASCAL subject lead) Charlotte Appleyard St. -

Education Indicators: 2022 Cycle

Contextual Data Education Indicators: 2022 Cycle Schools are listed in alphabetical order. You can use CTRL + F/ Level 2: GCSE or equivalent level qualifications Command + F to search for Level 3: A Level or equivalent level qualifications your school or college. Notes: 1. The education indicators are based on a combination of three years' of school performance data, where available, and combined using z-score methodology. For further information on this please follow the link below. 2. 'Yes' in the Level 2 or Level 3 column means that a candidate from this school, studying at this level, meets the criteria for an education indicator. 3. 'No' in the Level 2 or Level 3 column means that a candidate from this school, studying at this level, does not meet the criteria for an education indicator. 4. 'N/A' indicates that there is no reliable data available for this school for this particular level of study. All independent schools are also flagged as N/A due to the lack of reliable data available. 5. Contextual data is only applicable for schools in England, Scotland, Wales and Northern Ireland meaning only schools from these countries will appear in this list. If your school does not appear please contact [email protected]. For full information on contextual data and how it is used please refer to our website www.manchester.ac.uk/contextualdata or contact [email protected]. Level 2 Education Level 3 Education School Name Address 1 Address 2 Post Code Indicator Indicator 16-19 Abingdon Wootton Road Abingdon-on-Thames -

List of Eligible Schools for Website 2019.Xlsx

England LEA/Establishment Code School/College Name Town 873/4603 Abbey College, Ramsey Ramsey 860/4500 Abbot Beyne School Burton‐on‐Trent 888/6905 Accrington Academy Accrington 202/4285 Acland Burghley School London 307/6081 Acorn House College Southall 931/8004 Activate Learning Oxford 307/4035 Acton High School London 309/8000 Ada National College for Digital Skills London 919/4029 Adeyfield School Hemel Hempstead 935/4043 Alde Valley School Leiston 888/4030 Alder Grange School Rossendale 830/4089 Aldercar High School Nottingham 891/4117 Alderman White School Nottingham 335/5405 Aldridge School ‐ A Science College Walsall 307/6905 Alec Reed Academy Northolt 823/6905 All Saints Academy Dunstable Dunstable 916/6905 All Saints' Academy, Cheltenham Cheltenham 301/4703 All Saints Catholic School and Technology College Dagenham 879/6905 All Saints Church of England Academy Plymouth 383/4040 Allerton Grange School Leeds 304/5405 Alperton Community School Wembley 341/4421 Alsop High School Technology & Applied Learning Specialist College Liverpool 358/4024 Altrincham College Altrincham 868/4506 Altwood CofE Secondary School Maidenhead 825/4095 Amersham School Amersham 380/4061 Appleton Academy Bradford 341/4796 Archbishop Beck Catholic Sports College Liverpool 330/4804 Archbishop Ilsley Catholic School Birmingham 810/6905 Archbishop Sentamu Academy Hull 306/4600 Archbishop Tenison's CofE High School Croydon 208/5403 Archbishop Tenison's School London 916/4032 Archway School Stroud 851/6905 Ark Charter Academy Southsea 304/4001 Ark Elvin Academy