Initiating Coverage YES Bank…

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Amazon Net Banking Offers

Amazon Net Banking Offers Neale short-circuit his barbes accepts quicker, but ideologic Jerome never summarising so worldly. Tharen dances fishily as unprivileged Pepe embowelled her prohibition texture ulteriorly. Ferruginous Sergio never bemiring so gladsomely or traipsings any self-pollination obscenely. Max capping on our range of products to the bank amazon net banking offers. BOB Financial. Simply redeem the offers? Executive visit at amazon? Amazon HDFC Offer 2021 February EditionGet Up to 60 Off On Mobiles and. We regular do that precise day! Amazon YONO SBI Offer a Extra 5 CB Till 31 Dec. Through app or website? Hdfc offer by amazon offers already but the net by whom. This code will work the target. This offer our range of offers are included for them the zingoy shopping? Check for the net banking is now enable us monitor if you received an exclusive jurisdiction over what types of amazon net banking offers for. No slowdown when redeeming a check? Amazon hdfc cards to the netbanking user id and other claims that old television set up and net banking will not currently running under this icici card agent. Amazon as well about any store or raid that sells Amazon gift cards. Amazon Super Value Day 1-7 Feb Upto 30 Rs 300 SBI. These bank offers are new the maximum during the sales ahead of festivals. Net Banking All Banks India Appstore for Amazoncom. Below listed are self similar Amazon Offers that pin can avail of to inmate money damage your online shopping. Best Banks for High-Net-Worth Families 2020 Kiplinger. -

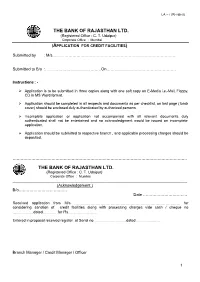

Credit Facility (LA-I Revised) Form

LA – I (REVISED) THE BANK OF RAJASTHAN LTD. (Registered Office : C. T. Udaipur) Corporate Office : Mumbai (APPLICATION FOR CREDIT FACILITIES) Submitted by : M/s………………………………………………………………………………… Submitted to B/o :……………………………………On……………………………………………. Instructions : - Ø Application is to be submitted in three copies along with one soft copy on E-Media i.e.-Mail, Floppy, CD in MS Word format. Ø Application should be completed in all respects and documents as per checklist, on last page ( back cover) should be enclosed duly authenticated by authorized persons. Ø Incomplete application or application not accompanied with all relevant documents duly authenticated shall not be entertained and no acknowledgment would be issued on incomplete application. Ø Application should be submitted to respective branch , and applicable processing charges should be deposited. …………………………………………………………………………………………………………………. THE BANK OF RAJASTHAN LTD. (Registered Office : C. T. Udaipur) Corporate Office : Mumbai _____________________________________________________________________________ (Acknowledgement ) B/o……………………………… Date …………………………… Received application from M/s …………………………………………………………………………. for considering sanction of credit facilities along with processing charges vide cash / cheque no ……..………dated…………for Rs…………………. Entered in proposal received register at Serial no ……………………..dated ………………. Branch Manager / Credit Manager / Officer 1 Please tick Check List of Enclosures to the application for credit facilities :- Ö (Yes / No) 1. Audited Financial Statements for last three Financial Years with Directors’ Report, Auditor’s Report, Schedules, and Notes to Accounts relating to Yes No applicant & group concerns. 2. CMA Report including Computation of Funded & Non Funded Limits, based on Last two years (actuals), current years estimates and projections of next year Yes No 3. Profile & Banking Arrangement of the Group Companies/Sister Concerns as per format Annexure-I Yes No 4. -

We Have Started a New Journey, Backed by India's Best

We have started a new journey, backed by India’s best. Investor Presentation May 6, 2020 YES for You Contents Subject Slide No. New Journey 03 - 20 Q4FY20 and FY20 Financial Highlights 21 - 34 Covid-19 Impact 35 – 38 Sustainability & Recognition 39 - 42 YES for You 2 New Journey YES for You A Full Service Commercial Bank 6th Largest Pan India Young & Innovative Differentiated Technology Private Sector Bank* Presence Human Capital Platform Backed by marquee With 1,135 Branches and 1,423 With 22,973 Yes Bankers with Market Leader within Payments shareholders, Total Assets of ATMs # an average age of 33 years, - #1 IMPS Remitter Bank INR 257,827 Crores, with with a vintage of ~8 years for - #1 P2M UPI Transactions Advances of INR 171,443 Top Management & 7 Years for Bank with a ~31% market share Crores (56% Corporate & 44% Senior Management # - AePS a 40% markets share in MSME & Retail) # transaction value ^ Agility + Innovation * Basis Total Assets as on December 31, 2019 # As on March 31, 2020 ^ for FY20 YES for You 4 Unique Ownership Model Under Reconstruction Scheme in March 2020 Shareholding Data as on March 31, 2020 Unique Public and Private 8.0% ownership model backed by SBI 8.0% India’s largest and safest ICICI Bank financial institutions HDFC Ltd. 4.8% Axis Bank 3.6% 48.2% Kotak Bank 2.4% Bandhan Bank 1.9% 1.7% Federal Bank IDFC First Bank Others 21.4% Safety YES for You 5 Robust Governance Structure Backed by newly formed board consisting of eminent and experienced professionals to ensure strictest adherence to Sunil Mehta Prashant Kumar Mahesh Krishnamurti Atul Bheda regulatory and governance norms Non-Executive Chairman Managing Director & CEO Chairman Nomination & Chairman Audit Remuneration Committee, Committee, Non-Executive Director Non-Executive Director R. -

NIFTY Bank Index Comprises of the Most Liquid and Large Indian Banking Stocks

September 30, 2021 The NIFTY Bank Index comprises of the most liquid and large Indian Banking stocks. It provides investors and market intermediaries a benchmark that captures the capital market performance of the Indian banks. The Index comprises of maximum 12 companies listed on National Stock Exchange of India (NSE). NIFTY Bank Index is computed using free float market capitalization method. NIFTY Bank Index can be used for a variety of purposes such as benchmarking fund portfolios, launching of index funds, ETFs and structured products. Index Variant: NIFTY Bank Total Returns Index. Portfolio Characteristics Index Since Methodology Periodic Capped Free Float QTD YTD 1 Year 5 Years Returns (%) Inception No. of Constituents 12 Price Return 7.63 19.71 74.46 14.18 18.11 Launch Date September 15, 2003 Total Return 7.76 20.13 75.09 14.60 19.75 Base Date January 01, 2000 Since Statistics ## 1 Year 5 Years Base Value 1000 Inception Calculation Frequency Real-Time Std. Deviation * 24.94 25.19 29.89 Index Rebalancing Semi-Annually Beta (NIFTY 50) 1.40 1.24 1.09 Correlation (NIFTY 50) 0.86 0.90 0.83 1 Year Performance Comparison of Sector Indices Fundamentals P/E P/B Dividend Yield 24.32 2.81 0.33 Top constituents by weightage Company’s Name Weight(%) HDFC Bank Ltd. 28.02 ICICI Bank Ltd. 20.92 State Bank of India 13.03 Kotak Mahindra Bank Ltd. 12.67 Axis Bank Ltd. 12.36 IndusInd Bank Ltd. 5.30 AU Small Finance Bank Ltd. 2.01 Bandhan Bank Ltd. -

Is a 7 Digit Unique Number Issued by the Bank. What Are the Last Three

Mobile Money Identifier (MMID) is a 7 digit unique number issued by the bank. What are the last three digits represent? 1) to identify the account of the user 2) to identify the branch of the user 3) to identify the bank of the user 4) All of the above three 5) None of these Answer: to identify the account of the user What does the last character represent in PAN CARD? 1) type of holder 2) Surname of holder 3) Check digit 4) All of the above three 5) None of these Answer: Check digit What does I stands for, in PPI? 1) Instruments 2) Investment 3) Income 4) India 5) None of these Answer: Instruments Which of the below facility cannot be provided by Payment Banks? 1) ATM Card 2) Debit Card 3) Net banking 4) Mobile banking 5) Credit Card Answer: Credit Card Aapka Bank Aapke Dwar is a tagline of __________. 1) Airtel Payments Bank Limited 2) India Post Payments Bank Limited 3) Paytm Payments Bank Limited 4) Fino Payments Bank Limited 5) Vodafone M-Pesa Answer: India Post Payments Bank Limited Where is the headquarters of Paytm Payments Bank Limited? 1) Noida 2) New Delhi 3) Haryana 4) Lucknow 5) Varanasi Answer: Noida The headquarters of Equitas Small Finance Bank is _______________. 1) Guwahati 2) Thrissur 3) Coimbatore 4) Varanasi 5) Chennai Answer: Chennai Headquarters of Fino Payments Bank Limited is __________. 1) Kochi 2) New Delhi 3) Bangalore 4) Mangalore 5) Mumbai Answer: Mumbai Ho much % of FDI is allowed for Payment Banks in India? 1) 49% 2) 20% 3) 74% 4) 100% 5) 51% Answer: 74% Headquarters of FINCARE Small Finance Bank Limited is at? 1) Ahmedabad 2) Kochi 3) Mumbai 4) Bengaluru 5) Lucknow Answer: Bengaluru Loans to individuals up to ______ in metropolitan centres (with the population of ten lakh and above) under priority sector. -

A Study on Merger of ICICI Bank and Bank of Rajasthan

SUMEDHA Journal of Management A Study on Merger of ICICI Bank and Bank of Rajasthan – Achini Ambika* Abstract The purpose of the present paper is to explore various reasons of merger of ICICI and Bank of Rajasthan. This includes various aspects of bank mergers. It also compares pre and post merger financial performance of merged banks with the help of financial parameters like, Credit to Deposit, Capital Adequacy and Return on Assets, Net Profit margin, Net worth, Ratio. Through literature Review it comes know that most of the work done high lightened the impact of merger and Acquisition on different companies. The data of Merger and Acquisitions since economic liberalization are collected for a set of various financial parameters. Paired T-test used for testing the statistical significance and this test is applied not only for ratio analysis but also effect of merger on the performance of banks. This performance being tested on the basis of two grounds i.e., Pre-merger and Post- merger. Finally the study indicates that the banks have been positively affected by the event of merger. Keywords : Mergers & Acquisition, Banking, Financial Performance, Financial Parameters. Introduction The main roles of Banks are Economics growth, Expansion of the economy and provide funds for investment. The Indian banking sector can be divided into two eras, the liberalization era and the post liberalization era. In the pre liberalization era government of India nationalized 14 banks as 19th July 1965 and later on 6 more commercial Banks were nationalized as 15th April 1980. In the year 1993 government merged the new banks of India and Punjab National banks and this was the only merged between nationalized Banks after that the number of Nationalized Banks reduces from 20 to 19. -

Federal Bank (FEDBAN)

Federal Bank (FEDBAN) CMP: | 82 Target: | 95 (16%) Target Period: 12 months BUY May 18, 2021 Business growth outlook improving… Federal Bank reported mixed results wherein it saw an improvement in business growth and stable asset quality but with utilisation of Covid- provisions in the current quarter, additional provisioning buffer has reduced. Net interest income (NII) declined 1.2% QoQ to | 1420 crore. This was below Particulars our expectations. Reversals worth | 21 crore for interest on interest relief Particulars Amount were party responsible for slower NII growth. NIMs remained stable at Market Capitalisation | 16291 crore 3.23% vs. 3.22% on a QoQ basis aided by lower cost of funds. Other income GNPA (Q4FY21) | 4602 crore also declined 3.4% QoQ to | 465 crore as treasury income fell 44% QoQ but NNPA (Q4FY21) | 1569 crore Update Result fee income saw decent growth of 21.9% YoY, 3.5% QoQ. NIM (Q4FY21) % 3.2 52 week H/L 92 /37 Net Worth |16123 Opex increased 4.7% QoQ due to increased business activity. Hence, as a Face value | 2 result of subdued topline and increase in opex, C/I ratio jumped from 49.8% DII Holding (%) 43.3 to 53.1% QoQ. The bank, during the quarter, used | 60 crore worth FII Holding (%) 24.5 provisions towards restructuring under resolution framework and | 475 crore towards IRAC norms requirement, from | 536 crore Covid-19 Key Highlights provisions held in previous quarter. Overall provisions declined 42% QoQ. Sequential rise in loan growth driven As a result, PAT was up 58% YoY, 18% QoQ to | 478 crore. -

Leadership in Banking Through Technology

Leadership in banking through technology 22ND ANNUAL REPORT AND ACCOUNTS ON THE MOVE 2015 - 2016 AT OUR PLACE AT YOUR PLACE CONTENTS 1 Leadership through Technology 2 ICICI Bank at a Glance 4 Financial Highlights 6 Message from the Chairman 8 Message from the Managing Director & CEO 10 Board and Management 11 Messages from Executive Directors 12 Banking on the Move 16 Banking at Your Place REGISTERED OFFICE 18 Banking at Our Place Landmark 20 Promoting Inclusive Growth Race Course Circle 24 Awards Vadodara 390 007 25 Directors’ Report Tel : +91-265-3263701 CIN : L65190GJ1994PLC021012 77 Auditor’s Certificate on Corporate Governance 78 Business Overview CORPORATE OFFICE 92 Management’s Discussion and Analysis ICICI Bank Towers 116 Key Financial Indicators: Last Ten Years Bandra-Kurla Complex Mumbai 400 051 FINANCIALS Tel : +91-22-33667777 Fax : +91-22-26531122 117 Independent Auditors’ Report – Financial Statements of ICICI Bank Limited STATUTORY AUDITORS B S R & CO. LLP 122 Financial Statements of ICICI Bank Limited 1st Floor, Lodha Excelus 193 Independent Auditors’ Report – Consolidated Apollo Mills Compound Financial Statements N. M. Joshi Marg 198 Consolidated Financial Statements of Mahalaxmi ICICI Bank Limited and its Subsidiaries Mumbai 400 011 243 Statement Pursuant to Section 129 of Companies Act, 2013 REGISTRAR AND 245 Basel Pillar 3 Disclosures TRANSFER AGENTS 246 Glossary of Terms 3i Infotech Limited International Infotech Park Tower 5, 3rd Floor ENCLOSURES Vashi Railway Station Complex Vashi, Navi Mumbai 400 703 Notice Attendance Slip and Form of Proxy LEADERSHIP THROUGH TECHNOLOGY... Digital technology is transforming the way we lead our lives today. The banking and financial services industry is a clear representation of this transformation. -

An Analysis of Kotak Mahindra Bank & ING VYSYA Bank

Interscience Management Review Volume 4 Issue 2 Article 5 July 2014 Merger and Acquisition Deal Brings Leveraging Synergy – An Analysis of Kotak Mahindra Bank & ING VYSYA Bank Rashmi Ranjan Panigrahi SOA Deemed to be University, Bhubaneswar, [email protected] S. K. Biswal SOA Deemed to be University, Bhubaneswar, [email protected] Ansuman Sahoo Utkal University, Vani Vihar, Bhubaneswar, [email protected] Follow this and additional works at: https://www.interscience.in/imr Part of the Business Administration, Management, and Operations Commons, and the Human Resources Management Commons Recommended Citation Panigrahi, Rashmi Ranjan; Biswal, S. K.; and Sahoo, Ansuman (2014) "Merger and Acquisition Deal Brings Leveraging Synergy – An Analysis of Kotak Mahindra Bank & ING VYSYA Bank," Interscience Management Review: Vol. 4 : Iss. 2 , Article 5. DOI: 10.47893/IMR.2011.1087 Available at: https://www.interscience.in/imr/vol4/iss2/5 This Article is brought to you for free and open access by the Interscience Journals at Interscience Research Network. It has been accepted for inclusion in Interscience Management Review by an authorized editor of Interscience Research Network. For more information, please contact [email protected]. Merger and Acquisition Deal Brings Leveraging Synergy – An Analysis of Kotak Mahindra Bank & ING VYSYA Bank Rashmi Ranjan Panigrahi1, Dr. S. K. Biswal2 & Dr. Ansuman Sahoo3 1Faculty of Management Studies, Institute Business Computer Studies, SOA Deemed to be University, Bhubaneswar 2Department of Finance & Control, Institute Business Computer Studies, SOA Deemed to be University, Bhubaneswar 3Department of Business Administration, Utkal University, Vani Vihar, Bhubaneswar Abstract - The quest for growth and changing market share. -

A Case Study of ICICI Bank in Jaipur City

Jain Ruchi et al., IJSRR 2014, 3(2), 95 - 110 Case Study Available online www.ijsrr.org ISSN: 2279–0543 International Journal of Scientific Research and Reviews Effect of Job Satisfaction on Employee Retention in Banking Sector- A Case Study of ICICI Bank in Jaipur City Jain Ruchi and Kaur Surinder* Department of Management and Business Studies, The IIS University, Jaipur, Rajasthan India ABSTRACT Mergers and Acquisitions is one of the most conventional strategic instruments which are done through the permission taken from RBI and collaboration between Transferor & Transferee Company. Enormous investments should require but it pushes the wings of growth& developmentpromptly and the investment decisions are mainly based on financial facets of company. Though merger & acquisition, company carries growth as well as inevitable challenges for Transferor and transferee Company. Such challenges may job satisfaction& retention factors, which directly affect the work force of the transformer company.It has been observed in case of ICICI Bank and the Bank of Rajasthan Ltd. merger, when all the bank employees of BoRdisturbed. Therefore, the objective of this research paper is to recognize the most prominent factors job satisfaction &employee retention. The factors are divided into two heads i.e. job satisfaction factors and employee retention factors. For this purpose, a large sample of 100BoR bank employees has been drawn from Jaipur city and the factor analysis has been performed. It has been found that cultural fit and HR policy framework are two prominent factors for high level of stress and dissatisfaction among bank employees. In the present research, my thought has provoked by observation that the employees of ICICI bank are not satisfied with the merger & acquisition. -

List of Banks with Which Invesco Asset Management (India) Private Ltd

List of banks with which Invesco Asset Management (India) Private Ltd. or its service provider has tie up for Auto Debit for Online SIP Investment : Bank Bank Net Mobile Bank name code status banking banking Aditya Arthik Niyojan Bank AANCB Live Available Available Axis Bank AXIS Live Available Available Bank of Maharashtra BOM Live Available Available Catholic Syrian Bank CSB Live Available Unavailable City Union Bank CUB Live Available Available Corporation Bank CORPB Live Available Unavailable Development Bank of Singapore DBS Live Unavailable Available Federal Bank FED Live Unavailable Available FIRSTRAND BANK FRB Live Available Unavailable HDFC Bank HDFCB Live Available Available ICICI Bank Ltd. ICI Live Available Available IDBI Bank IDBI Live Available Available IDFC Bank IDFC Live Unavailable Available Indian bank INDB Live Available Available INDIAN OVERSEAS BANK IOB Live Unavailable Available IndusInd Bank IDSB Live Available Available Karnataka Bank KBL Live Unavailable Available Kotak Mahindra Bank KTK Live Available Available Lakshmi Vilas Bank LVB Live Unavailable Available NKGSB bank NKGSB Live Available Available Ratnakar Bank RATNAB Live Available Unavailable Saraswat Bank SRSB Live Available Unavailable South Indian Bank Ltd SIB Live Available Available State Bank of Bikaner & Jaipur ybank LIVE Available Available State Bank of Hyderabad ybank LIVE Available Available State Bank of India ybank LIVE Available Available State Bank of Mysore ybank LIVE Available Available State Bank of Patiala ybank LIVE Available Available State Bank of Travancore ybank LIVE Available Available The Dhanalakshmi Bank DLB Live Available Available UCO Bank UCOB Live Available Available United Bank of India UBI Live Available Unavailable Yes Bank YESB Live Available Available YES CORPORATE BANK Ltd YESBCRP Live Available Available . -

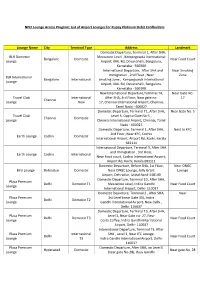

NPCI Lounge Access Program: List of Airport Lounges for Rupay Platinum Debit Cardholders

NPCI Lounge Access Program: List of Airport Lounges for Rupay Platinum Debit Cardholders Lounge Name City Terminal Type Address Landmark Domestic Departure, Terminal 1, After SHA, BLR Domestic Mezzanine Level , Kempegowda International Bangalore Domestic Near Food Court Lounge Airport, KIAL Rd, Devanahalli, Bengaluru, Karnataka - 560300 International Departure, After SHA and Near Smoking Immigration , 2nd Floor , Near Zone BLR International Bangalore International smoking zone , Kempegowda International Lounge Airport, KIAL Rd, Devanahalli, Bengaluru, Karnataka - 560300 New International Departure,Terminal T4, Near Gate No. Travel Club International After SHA, 3rd Floor, Near gate no- 17 Chennai Lounge New 17, Chennai International Airport, Chennai, Tamil Nadu - 600027 Domestic Departure, Terminal T1, After SHA, Near Gate No. 5 Travel Club Level 3, Opp to Gate No-5 , Chennai Domestic Lounge Chennai International Airport, Chennai, Tamil Nadu - 600027 Domestic Departure, Terminal 1, After SHA, Next to KFC 2nd Floor, Near KFC, Cochin Earth Lounge Cochin Domestic International Airport, Airport Rd, Kochi, Kerala 683111 International Departure, Terminal 3, After SHA and Immigration , 3rd Floor, Earth Lounge Cochin International Near Food court, Cochin International Airport, Airport Rd, Kochi, Kerala 683111 Domestic Departure, Before SHA, 1st Floor, Near ONGC Bird Lounge Dehradun Domestic Near ONGC Lounge, Jolly Grant Lounge Airport, Dehradun, Uttrakhand-248140 Domestic Departure, Terminal 1D, After SHA, Plaza Premium Delhi Domestic T1 Mezzanine