Management Meeting with Equinor Low Carbon Solutions 07.05.2020

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

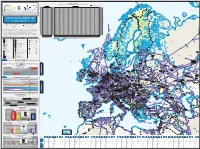

System Development Map 2019 / 2020 Presents Existing Infrastructure & Capacity from the Perspective of the Year 2020

7125/1-1 7124/3-1 SNØHVIT ASKELADD ALBATROSS 7122/6-1 7125/4-1 ALBATROSS S ASKELADD W GOLIAT 7128/4-1 Novaya Import & Transmission Capacity Zemlya 17 December 2020 (GWh/d) ALKE JAN MAYEN (Values submitted by TSO from Transparency Platform-the lowest value between the values submitted by cross border TSOs) Key DEg market area GASPOOL Den market area Net Connect Germany Barents Sea Import Capacities Cross-Border Capacities Hammerfest AZ DZ LNG LY NO RU TR AT BE BG CH CZ DEg DEn DK EE ES FI FR GR HR HU IE IT LT LU LV MD MK NL PL PT RO RS RU SE SI SK SM TR UA UK AT 0 AT 350 194 1.570 2.114 AT KILDIN N BE 477 488 965 BE 131 189 270 1.437 652 2.679 BE BG 577 577 BG 65 806 21 892 BG CH 0 CH 349 258 444 1.051 CH Pechora Sea CZ 0 CZ 2.306 400 2.706 CZ MURMAN DEg 511 2.973 3.484 DEg 129 335 34 330 932 1.760 DEg DEn 729 729 DEn 390 268 164 896 593 4 1.116 3.431 DEn MURMANSK DK 0 DK 101 23 124 DK GULYAYEV N PESCHANO-OZER EE 27 27 EE 10 168 10 EE PIRAZLOM Kolguyev POMOR ES 732 1.911 2.642 ES 165 80 245 ES Island Murmansk FI 220 220 FI 40 - FI FR 809 590 1.399 FR 850 100 609 224 1.783 FR GR 350 205 49 604 GR 118 118 GR BELUZEY HR 77 77 HR 77 54 131 HR Pomoriy SYSTEM DEVELOPMENT MAP HU 517 517 HU 153 49 50 129 517 381 HU Strait IE 0 IE 385 385 IE Kanin Peninsula IT 1.138 601 420 2.159 IT 1.150 640 291 22 2.103 IT TO TO LT 122 325 447 LT 65 65 LT 2019 / 2020 LU 0 LU 49 24 73 LU Kola Peninsula LV 63 63 LV 68 68 LV MD 0 MD 16 16 MD AASTA HANSTEEN Kandalaksha Avenue de Cortenbergh 100 Avenue de Cortenbergh 100 MK 0 MK 20 20 MK 1000 Brussels - BELGIUM 1000 Brussels - BELGIUM NL 418 963 1.381 NL 393 348 245 168 1.154 NL T +32 2 894 51 00 T +32 2 209 05 00 PL 158 1.336 1.494 PL 28 234 262 PL Twitter @ENTSOG Twitter @GIEBrussels PT 200 200 PT 144 144 PT [email protected] [email protected] RO 1.114 RO 148 77 RO www.entsog.eu www.gie.eu 1.114 225 RS 0 RS 174 142 316 RS The System Development Map 2019 / 2020 presents existing infrastructure & capacity from the perspective of the year 2020. -

Supreme Court of Norway

SUPREME COURT OF NORWAY On 28 June 2018, the Supreme Court gave judgment in HR-2018-1258-A (case no. 2017/1891), civil case, appeal against judgment, CapeOmega AS (Counsel Thomas G. Michelet) (Assisting counsel: Kyrre Eggen) Solveig Gas Norway AS Silex Gas Norway AS Infragas Norge AS (Counsel Jan B. Jansen Counsel Thomas K. Svensen) (Assisting counsel: Kyrre Eggen) v. The state represented by the Ministry of Petroleum and Energy (The Attorney-General represented Tolle Stabell and Christian Fredrik Michelet) (Assisting counsel: Håvard H. Holdø) VOTING : (1) Justice Bårdsen: The case concerns the validity of the Ministry of Petroleum and Energy's Regulations 26 June 2013 no. 792 relating to amendment of the Regulations relating to the stipulation of tariffs etc. for certain facilities (the Tariff Regulations), adopted under section 4-8 of the Petroleum Act, among others. 2 (2) The Tariff Regulations 20 December 2002 no. 1724 regulate the tariffs that third parties must pay for shipment of gas in the pipelines owned by the joint venture Gassled. The joint venture was established in 2003, and tariffs were stipulated in the Tariff Regulations for the various areas of the pipeline network. This network is the world’s biggest offshore system for transport and processing of gas, consisting of a number of gas pipelines on the seabed of the North Sea and the Norwegian Sea, some onshore processing plants in Norway and six receiving facilities in the UK, France, Belgium and Germany. The system is subject to licences from the Ministry of Petroleum and Energy pursuant to section 4-3 of the Petroleum Act. -

Europe, Middle East and North Africa Total 99 12 646 219

Europe, Middle East Europe,and North Africa Middle East andFact Sheet—March North 2021 Africa Fact Sheet—March 2021 ConocoPhillips has operated in Europe for more than 50 years, with significant developments in the 2020 Production Norwegian sector of the North Sea and in the Norwegian Sea. In Qatar, the company has interests in a producing field as well as liquefied natural gas production and export. The company also has Thousand interests in a concession in Libya. barrels of oil Operated assets in Europe include the Greater Ekofisk Area in Norway. The company also conducts 219 equivalent per day exploration activity in Norway. The company has leveraged its existing operations, infrastructure and basin expertise to create incremental growth projects in recent years, and development 2020 Proved Reserves* opportunities still exist in ConocoPhillips’ legacy areas. In Qatar, the Qatargas 3 joint venture continues providing stable production. Billion barrels of oil In Libya, the company has an interest in the Waha Concession in the Sirte Basin. Production equivalent operations in Libya and related oil exports have been periodically interrupted over the last several 0.6 years due to forced shutdowns of the Es Sider terminal. ConocoPhillips—Average Daily Net Production, 2020 Crude Oil NGL Natural Gas Total Area Interest Operator (MBD) (MBD) (MMCFD) (MBOED) Greater Ekofisk Area 30.7%-35.1% ConocoPhillips 46 2 39 55 Heidrun 24.0% Equinor 12 1 32 18 Aasta Hansteen 10.0% Equinor - - 82 14 Troll 1.6% Equinor 2 - 54 11 Visund 9.1% Equinor 2 1 40 10 Alvheim 20.0% Aker BP 8 - 13 10 Other Various Equinor 8 - 10 9 Norway Total 78 4 270 127 Qatargas 3 30.0% Qatargas Operating Co. -

Oil and Gas Fields in Norway

This book is a work of reference which provides an easily understandable Oil and gas fields in n survey of all the areas, fields and installations on the Norwegian continental shelf. It also describes developments in these waters since the 1960s, Oil and gas fields including why Norway was able to become an oil nation, the role of government and the rapid technological progress made. In addition, the book serves as an industrial heritage plan for the oil in nOrway and gas industry. This provides the basis for prioritising offshore installations worth designating as national monuments and which should be documented. industrial heritage plan The book will help to raise awareness of the oil industry as industrial heritage and the management of these assets. Harald Tønnesen (b 1947) is curator of the O Norwegian Petroleum Museum. rway rway With an engineering degree from the University of Newcastle-upon- Tyne, he has broad experience in the petroleum industry. He began his career at Robertson Radio i Elektro before moving to ndustrial Rogaland Research, and was head of research at Esso Norge AS before joining the museum. h eritage plan Gunleiv Hadland (b 1971) is a researcher at the Norwegian Petroleum Museum. He has an MA, majoring in history, from the University of Bergen and wrote his thesis on hydropower ????????? development and nature conser- Photo: Øyvind Hagen/Statoil vation. He has earlier worked on projects for the Norwegian Museum of Science and Technology, the ????????? Norwegian Water Resources and Photo: Øyvind Hagen/Statoil Energy Directorate (NVE) and others. 152 ThE TROLL aREa The Troll area of the northern North Sea lies in more than 300 metres of water, 65 kilometres west of Kollsnes near Bergen. -

Bringing Norwegian Gas to Europe

Melkøya Asterix Luva design by by design NORNE GAS colours TRANSPORT .no SYSTEM Zidane Skarv Bringing Norwegian gas Linnorm to Europe Njord www.gassco.no TAMPEN LINK TH LANGELED NOR Gjøa Valemon Gassco-operated systems at 2014 PIPELINE FROM TO LENGTH DIAMETER CAPACITY (Mscm/d) Haltenpipe Heidrun Tjeldbergodden 250 km 16” 7.0 mill Norne Gas Transport (NGTS) Norne Heidrun 128 km 16” 7.0 mill Åsgard Transport Åsgard Kårstø 707 km 42” 70.4 mill Kvitebjørn Pipeline Kvitebjørn Kollsnes 147 km 30” 26.5 mill Statpipe rich gas Statfjord Kårstø 308 km 30” 25.6 mill Statpipe Kårstø Draupner S 228 km 28” 21.1 mill Statpipe Draupner S Ekofisk Y 203 km 36” 44.4 mill Statpipe Heimdal Draupner S 155 km 36” 30.7 mill Zeepipe Sleipner Zeebrugge 813 km 40” 42,2 mill Zeepipe Sleipner Draupner S 38 km 30” 55.0 mill Zeepipe IIA Kollsnes Sleipner 299 km 40” 77.0 mill Zeepipe IIB Kollsnes Draupner E 301 km 40” 75.0 mill Europipe Draupner E Dornum/Emden 620 km 40” 45.7 mill Europipe II Kårstø Dornum 658 km 42” 71.9 mill Franpipe Draupner E Dunkerque 840 km 42” 54.8 mill H Norpipe Ekofisk Emden 440 km 36” 32.4 mill UT Vesterled Heimdal St Fergus 360 km 32” 38.9 mill Oseberg Gas Transport (OGT) Oseberg Heimdal 109 km 36” 35.0 mill Langeled North (LLN) Nyhamna Sleipner 627 km 42” 74.7 mill Langeled South (LLS) Sleipner Easington 543 km 44” 72.1 mill LANGELED SO Tampen Link Statfjord FLAGS 23 km 32” 25.0 mill Gjøa Gas Pipe Gjøa FLAGS 131 km 28” 17.8 mill Total 7928 km Onshore facilities: Zones and tarrifs Kårstø gas processing plant, Norway Gassled is divided into areas, with fixed tariffs for Kollsnes gas processing plant, Norway transport and/or processing within each of these. -

Bringing Gas to the Market

Bringing Gas to the Market Bringing Gas to the Market Gas Transit and Transmission Tariffs in Energy Charter Treaty Countries: Bringing Gas Regulatory Aspects and Tariff Methodologies Tariffs for the utilisation of gas transmission pipelines are an essential factor Gas Transit and Transmission Tariffs in Energy CharterTreaty Countries: Regulatory AspectsTariff and Methodologies to the Market determining the openness of international gas markets. The availability of interconnections and economically acceptable transportation costs are a condition for natural gas reaching consumer markets. With the dependence of major consuming countries on imported natural gas increasing – with the exception of countries that can rely on significant own reserves of unconventional gas – international trade in natural gas is expected to grow over the next decades. Common principles are necessary to enable such trade and to facilitate transit. Basic principles for transmission tariffs and some other aspects related to the utilisation of energy transport facilities have been elaborated in the Energy Charter. This study analyses methodologies and tariff principles for natural gas transmission Gas Transit and Transmission Tariffs in used in member countries of the Energy Charter Treaty, paying particular attention to developments in Europe, the Black Sea region and Central Asia. Common basic principles exist across this area, but concrete methodologies vary, as well as the Energy Charter Treaty Countries: choice of the market structure and the treatment of transit, in particular between the European Union on the one hand and some Eastern European and Central Asian countries on the other. The study compares the following aspects of regulatory regimes: Regulatory Aspects and - the role of the regulator, third-party access and unbundling; - the treatment of gas transit; Tariff Methodologies - methodologies to calculate capital and operational costs; - unit tariff methodologies. -

Processing Plant Like an Oasis, the Processing Plant Lights up the Coastal Landscape in Late Summer Evenings

FACTS Kollsnes Processing Plant Like an oasis, the processing plant lights up the coastal landscape in late summer evenings. The Kollsnes processing plant plays a key role in the transport of large quanti- ties of gas from fields in the Norwegian sector of the North Sea to customers in Europe. Gas from Kollsnes accounts for around 40 per cent of all Norwegian gas deliveries. The enormous quantities of gas in the Troll field started it all. Today, Kollsnes processing plant acts as goes further treatment and is fractioned Troll is the very corner- a centre for processing of gas from the into propane, butane and naphtha. stone of Norwegian Troll, Fram, Visund and Kvitebjørn fields. At Kollsnes, the gas is cleaned, dried and The processing plant itself consists gas production. When compressed before being transported as primarily of three dew point plants for dry gas through export pipes to Europe. treating gas, condensate and mono- the field was declared In addition, some gas is transported ethylene glycol (MEG) respectively. in separate pipes to Naturgassparken There is also a separate plant for the commercially viable in western Øygarden, where Gassnor production of Natural Gas Liquids in 1983, the question treats and distributes gas for domestic (NGL). In the plant, the wet gas (NGL) use. Condensate, or wet gas, which is is separated out first, and then the dry arose of what route made up of heavier components in the gas is pressurised using the six export gas, is transported via the Sture ter- compressors and sent into the transport the enormous quanti- minal through a pipeline to Mongstad system via the export pipelines Zeepipe ties of gas should take (Vestprosess). -

Om Uhellet Er Ute

Om uhellet er ute Orientering til allmennheten om sikkerhet og beredskap ved Kollsnes prosessanlegg og Stureterminalen Formålet med denne brosjyren Hva er en storulykke? er å informere offentligheten og naboer til Stureterminalen og En storulykke er en hendelse der det inngår ett eller flere farlige Kollsnes prosessanlegg om sikkerhetsforhold og beredskapstiltak kjemikalier, eksempelvis olje- og gassprodukter, som oppstår i tilknyttet aktivitetene ved virksomheten. en storulykkevirksomhet og som får en ukontrollert utvikling som Equinor ønsker på denne måten å bidra til økt kunnskap i umiddelbart eller senere medfører en alvorlig fare for eller skade på mennesker, miljø eller materielle verdier. Eksempler på storulykker er forbindelse med driften av anleggene på Sture og Kollsnes. omfattende branner, eksplosjoner og utslipp av olje. Stureterminalen og Kollsnes prosessanlegg er to av en rekke større virksomheter i Norge som håndterer kjemiske og brannfarlige stoffer, og som følge av dette er underlagt «Forskrift om tiltak for å avverge storulykker i virksomheter som håndterer farlige stoff» (Storulykkeforskriften). For Stureterminalen og Kollsnes prosessanlegg er det særlig Petroleums-tilsynet (Ptil) som er myndighetene sitt kontrollorgan, og som kontrollerer at Gassco og Equinor følger lover og pålegg relatert til sikkerhet. Også kommunale myndigheter, Kystverket og Direktoratet for samfunnsikkerhet og beredskap er med i dette arbeidet. Øvrige forskrifter som regulerer virksomheten, samt tilsynsrapporter kan fås ved henvendelse til Ptil. -

The Troll Story - EASEE - GAS March 2016

The Troll Story - EASEE - GAS March 2016 Knut Ivar Pettersen, VP Production Troll A 1 2 Classification: Internal 2014-10-31 The Troll Story - EASEE - GAS March 2016 Knut Ivar Pettersen, VP Production Troll A EASEE March 2016 3 Norwegian gas is key to European energy security Access to an integrated Large gas resource Proximity to markets and flexible pipeline potential on the NCS* infrastructure Pipeline Polarled LNG 1450 bn Sm3 Åsgard transport 1922 Norway Ormen Lange 3 400 – 1200 km Nyhamna bn Sm Russia Tampen Link Troll 6000 – 7000km Kollsnes Vesterled Kårstø 625 Sleipner Draupner 3 St Fergus bn Sm Europipe II Ekofisk Europipe I Norpipe Langeled Reserves Easington Emden/ Zeepipe Contingent resources Caspian Franpipe Dornum in fields/discoveries Zeebrugge Algeria Region Dunkerque Undiscovered ~3000 km ~4000 km Only one third of NCS resources have been produced to date Source: Norwegian Petroleum Directorate (NPD) resource account as of 31.12.2014 5 Classification: Internal 20 oktober 2015 © Statoil ASA Mongstad Kollsnes The Troll Story The Troll Story Troll Gas: A North Sea Giant Troll C − Located 80 km northwest of Bergen − Gas Reserves 1400 GSm3 Troll Oil: The impossible made possible Troll B − 2+ billion barrels − 120.000 bbls/day Kollsnes • Troll Area: Commercialize tie-ins Troll A − Fram Vest 60.000 bbls/day at peak − Fram Øst 55.000 bbls/day at peak − Other discoveries and prospects 20 km 6 Troll – gas for Europe • Gas is exported through three 36” pipelines from Troll A to Kollsnes • The gas is processed at Kollsnes and sent -

Troll on Stream; the Story and Its Perspectives))

NEI-NO--806 NO9705258 ^^ _ NORTHERN ONS SEAS ONS CONFERENCE 1996 27-30 AUGUST STAVANGER. NORWAY I'11'">11111NO9705258 Paper no. Cl Session: NATURAL GAS IN A CHANGING MARKET Paper title: «Troll on stream; The story and its perspectives)) Speaker: Peter Mellbye Statoil, Norway MASTER tmmmnw OF im DOCUMENT » UMJMITED DISCLAIMER Portions of this document may be lUegible in electronic Image products. Images are produced from the best available origina! document Troll on stream The story and its perspectives Offshore Northern Seas Peter Mellbye Stavanger Executive Vice President 28 August 1996 Statoil The Troll Platform Concepts POO 1986 Version Chosen Concept 1986 Plan for development and operation - fully integrated monotower platform (basis for Storting 1987 approval) - Weights (1000 tonnes): Gravity Base Structure 1000, topside 72 - Export capacity 27 BCM/y - Offshore personnel: 200 - Field investments: 39 bill. 1996-NOK (incl. pipelines) - Onshore gas processing was considered, but rejected As the planning continued, extensive studies and discussions on alternative development concepts were performed in the licence. Main purpose: Reduce costs The development operator Shell and Statoil agreed in 1988 to re-examine the possibility of onshore processing. Due to the new multiphase technology, shipping of the unprocessed gas to Koilsnes some 60 km away was proven possible Main issues considered - pipeline aspects : - Predict and control the unprocessed well stream (condensate, gas, water) - Control hydrating process - Monitor corrosion Final -

Natural Gas in Norway

TPG 4140 NTNU Natural Gas in Norway Professor Jon Steinar Gudmundsson Department of Petroleum Engineering and Applied Geophysics Norwegian University of Science and Technology Trondheim September 3, 2013 Oil Equivalent 1000 Sm3 gas = 1 Sm3 o.e. • The total petroleum production for the first seven months in 2013 was about 127.1 million standard cubic meters oil equivalents. (MSm3 o.e.), broken down as follows: about 49.5 MSm3 o.e. of oil, about 13.0 MSm3 o.e. of NGL and condensate and about 64.6 MSm3 o.e. of gas for sale. Outline • Actors in oil and gas industry • Blocks and fields offshore Norway • Receiving and processing terminals • Licence, partner and operator • Resources and reserves • Field development • Gas production and forecast • Gas transport system • Petoro, Gassled and Gassco • Tax and “Pension Fund” FACTS 2013 • Norwegian petroleum history • Framework and organization • The petroleum sector – Norway’s largest industry • Petroleum resources • Exploration activity • Development and operations • Gas export from the Norwegian shelf • Research in the oil and gas activities • Environmental considerations in the Norwegian petroleum Sector • Fields in production • Fields under development • Future developments • Fields where production has ceased • Pipelines and onshore facilities Oil and Gas Exporters 2011 State organization of petroleum activities Oil and gas names • Ministry of Petroleum and Energy (MPE) • Norwegian Petroleum Directorate (NPD) • Petroleum Safety Authority (PTIL) • Norwegian Climate and Pollution Agency (KLIF) -

Green H2 Webinar Hydrogen Transport the Norwegian Gas Transport System

Green H2 Webinar Hydrogen transport The Norwegian gas transport system Nyhamna Kollsnes Kårstø - Securing energy supply R&D PROGRAMS & PRIORITIES FUTURE EFFICIENT VALUE CREATION OPERATION Gassco Strategy 2021 SUSTAINABLE DEVELOPMENT A MBITION TECHNOLOGIES AND SOLUTIONS FOR LOW EMISSION VALUE CREATION M AIN PRIORITIES 2021 DEVELOP SOLUTIONS AND TECHNOLOGIES TO REDUCE EMISSIONS FROM NCS, AND TO BUILD KNOWLEDGE TO PREPARE NCS GAS INFRASTRUCTURE FOR LOW CARBON SOLUTIONS • REDUCE EMISSIONS – SCOPE 1 • LOW CARBON SOLUTIONS - CCS VALUE CHAIN • LOW CARBON SOLUTIONS - HYDROGEN VALUE CHAIN • LOW CARBON SOLUTIONS - FUTURE ENERGY SYSTEMS Hydrogen transport in existing pipelines … 2016 2017 New Hydrogen Pipeline from Norway to Netherlands H2 Production in Norway Concept Only - To Be Evaluated Blue Green Project Objectives / Strategic Drivers H2 H2 • Response to EU H2 strategy (Blue H2 import) The Value Chain ? • Access to H2 backbone originating at Groningen ? • Engagement directly with off-takers possible 11,600,000 x Norway • Offer optionality and scale of H2 (blue and green) H2 Consumption at Oil & Gas • Seat at the table in solving for EU energy transition • 12.000 MW Blue Hydrogen Installations • Decarbonisation of O&G installations • 1.000 MW Green Hydrogen • Consider H2 link between Kollsnes and Kårstø • Local use for industry and maritime fuel Key Challenges • Large commitment required (take-or-pay) 11,600,000 xOffshore • EU subsidies required via price, not via CAPEX • Long term gas supply outlook, consider LNG Imp? • H2 offer full decarb